For taxpayers navigating the complexities of federal income taxes, understanding the IRS Schedule D attached to the 1040 or 1040-SR form is crucial. This schedule is specifically designed for reporting capital gains and losses, which can significantly impact one's overall tax liability. It is essential for individuals who have sold investments, such as stocks, bonds, or real estate, during the tax year. The form requires detailed information about each transaction, including the asset's acquisition date, sale date, and the net gain or loss incurred. Additionally, special considerations may apply, such as the distinction between short-term and long-term gains, with different tax rates governing each. Accurate completion of Schedule D can lead to potential tax savings, while mistakes can result in unnecessary penalties or an increased tax burden. Thus, taxpayers must familiarize themselves with this important document to ensure compliance with IRS guidelines and to optimize their tax outcomes.

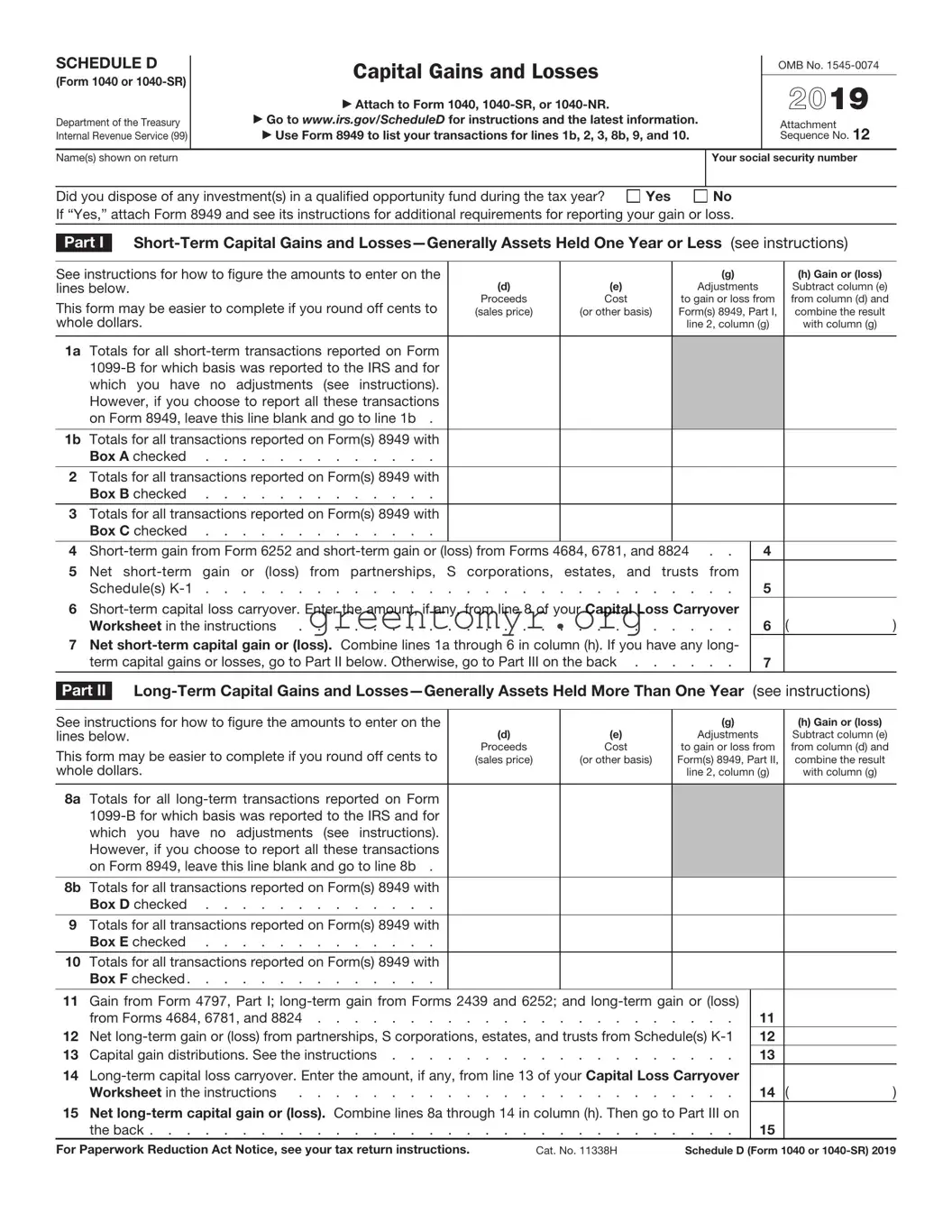

SCHEDULE D |

Capital Gains and Losses |

|

|

|

|

OMB No. |

|||||||

(Form 1040 or |

|

|

|

|

|

2019 |

|||||||

|

|

|

|

|

|

|

|

||||||

|

|

|

|

Attach to Form 1040, |

|

|

|

|

|

||||

Department of the Treasury |

Go to www.irs.gov/ScheduleD for instructions and the latest information. |

|

|

|

Attachment |

12 |

|||||||

Internal Revenue Service (99) |

Use Form 8949 to list your transactions for lines 1b, 2, 3, 8b, 9, and 10. |

|

|

|

Sequence No. |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|||

Name(s) shown on return |

|

|

|

|

|

Your social security number |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|||

Did you dispose of any investment(s) in a qualified opportunity fund during the tax year? |

Yes |

|

No |

|

|

|

|||||||

If “Yes,” attach Form 8949 and see its instructions for additional requirements for reporting your gain or loss. |

|

|

|

||||||||||

|

|

|

|

|

|

||||||||

Part I |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See instructions for how to figure the amounts to enter on the |

|

|

|

|

(g) |

|

(h) Gain or (loss) |

||||||

lines below. |

|

|

(d) |

(e) |

|

Adjustments |

|

Subtract column (e) |

|||||

This form may be easier to complete if you round off cents to |

Proceeds |

Cost |

|

to gain or loss from |

from column (d) and |

||||||||

(sales price) |

(or other basis) |

Form(s) 8949, Part I, |

combine the result |

||||||||||

whole dollars. |

|

|

|

|

line 2, column (g) |

with column (g) |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

1a |

Totals for all |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

|

which you have no adjustments (see instructions). |

|

|

|

|

|

|

|

|

|

|||

|

However, if you choose to report all these transactions |

|

|

|

|

|

|

|

|

|

|||

|

on Form 8949, leave this line blank and go to line 1b . |

|

|

|

|

|

|

|

|

|

|||

1b |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box A checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

2 |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box B checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

3 |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box C checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

4 |

. . |

|

4 |

|

|

||||||||

5 |

Net |

from |

|

|

|

|

|||||||

|

Schedule(s) |

. |

. . |

|

5 |

|

|

||||||

6 |

|

|

( |

) |

|||||||||

|

Worksheet in the instructions |

. |

. . |

|

6 |

||||||||

7 |

Net |

|

|

|

|

||||||||

|

term capital gains or losses, go to Part II below. Otherwise, go to Part III on the back . . . |

. |

. . |

|

7 |

|

|

||||||

|

|

|

|||||||||||

Part II |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

See instructions for how to figure the amounts to enter on the |

|

|

|

|

(g) |

|

(h) Gain or (loss) |

||||||

lines below. |

|

|

(d) |

(e) |

|

Adjustments |

|

Subtract column (e) |

|||||

This form may be easier to complete if you round off cents to |

Proceeds |

Cost |

|

to gain or loss from |

from column (d) and |

||||||||

(sales price) |

(or other basis) |

Form(s) 8949, Part II, |

combine the result |

||||||||||

whole dollars. |

|

|

|

|

line 2, column (g) |

with column (g) |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

8a |

Totals for all |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||

|

which you have no adjustments (see instructions). |

|

|

|

|

|

|

|

|

|

|||

|

However, if you choose to report all these transactions |

|

|

|

|

|

|

|

|

|

|||

|

on Form 8949, leave this line blank and go to line 8b . |

|

|

|

|

|

|

|

|

|

|||

8b |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box D checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

9 |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box E checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

10 |

Totals for all transactions reported on Form(s) 8949 with |

|

|

|

|

|

|

|

|

|

|||

|

Box F checked |

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11Gain from Form 4797, Part I;

|

from Forms 4684, 6781, and 8824 |

11 |

12 |

Net |

12 |

13 |

Capital gain distributions. See the instructions |

13 |

14

Worksheet in the instructions |

14 ( |

) |

15Net

the back |

15 |

For Paperwork Reduction Act Notice, see your tax return instructions. |

Cat. No. 11338H |

Schedule D (Form 1040 or |

Schedule D (Form 1040 or |

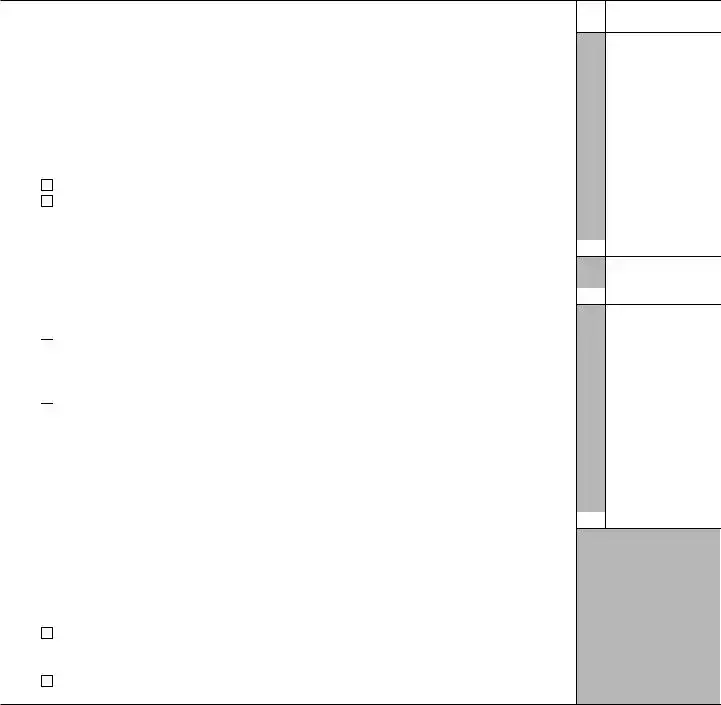

Page 2 |

|

|

Summary |

|

Part III |

|

|

16 Combine lines 7 and 15 and enter the result . . . . . . . . . . . . . . . . . .

•If line 16 is a gain, enter the amount from line 16 on Form 1040 or

•If line 16 is a loss, skip lines 17 through 20 below. Then go to line 21. Also be sure to complete line 22.

•If line 16 is zero, skip lines 17 through 21 below and enter

17Are lines 15 and 16 both gains?

Yes. Go to line 18.

No. Skip lines 18 through 21, and go to line 22.

18If you are required to complete the 28% Rate Gain Worksheet (see instructions), enter the

amount, if any, from line 7 of that worksheet . . . . . . . . . . . . . . . . .

19 If you are required to complete the Unrecaptured Section 1250 Gain Worksheet (see instructions), enter the amount, if any, from line 18 of that worksheet . . . . . . . . .

20Are lines 18 and 19 both zero or blank?

Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Forms 1040 and

Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Forms 1040 and

No. Complete the Schedule D Tax Worksheet in the instructions. Don’t complete lines 21 and 22 below.

No. Complete the Schedule D Tax Worksheet in the instructions. Don’t complete lines 21 and 22 below.

21If line 16 is a loss, enter here and on Form 1040 or

• The loss on line 16; or |

} |

• ($3,000), or if married filing separately, ($1,500) |

Note: When figuring which amount is smaller, treat both amounts as positive numbers.

22Do you have qualified dividends on Form 1040 or

Yes. Complete the Qualified Dividends and Capital Gain Tax Worksheet in the instructions for Forms 1040 and

16

18

19

21 ( |

) |

No. Complete the rest of Form 1040,

Schedule D (Form 1040 or

| Fact Name | Description |

|---|---|

| Purpose | Schedule D is used for reporting capital gains and losses from the sale of assets to calculate tax liability. |

| Eligibility | Taxpayers who have sold capital assets, such as stocks or real estate, during the tax year must file this schedule. |

| Filing Requirements | Individuals filing Form 1040 or 1040-SR and reporting capital gains or losses must include Schedule D with their return. |

| State-Specific Considerations | Some states require additional forms or information regarding capital gains based on local tax laws; exact requirements vary by state. |

Once you have gathered all necessary information, it's time to complete the IRS Schedule D. Make sure you have your tax documents handy, as they will help streamline the process. Follow these steps carefully to fill out the form accurately.

After completing the Schedule D, it will be ready to attach to your Form 1040 or 1040-SR when you file your taxes. Double-check all figures one last time to ensure everything matches. This will help avoid any delays in processing your return.

IRS Schedule D is a form used to report capital gains and losses from the sale of securities and other assets. It is attached to Form 1040 or 1040-SR when filing your federal income tax return. The primary purpose of Schedule D is to help taxpayers calculate their net capital gain or loss, which is essential for determining the amount of tax owed or refund due. Understanding how to fill out this schedule correctly can significantly impact your overall tax liability.

Not everyone is required to file Schedule D. Generally, you need to complete this form if:

If your transactions fall into these categories, it's essential to include Schedule D with your tax return to ensure proper reporting of any gains or losses.

To report your capital gains or losses, follow these steps:

Double-check your calculations and make sure to include any necessary supporting documents when filing.

When you have both gains and losses, the IRS allows you to offset them against each other. Start by totaling your short-term gains and losses in Part I, then do the same for long-term gains and losses in Part II. Once you have these totals:

If any remaining losses persist after that, they can be carried over to future tax years. Keeping accurate records will assist in this process and make filing easier in the long run.

When filling out the IRS Schedule D 1040 or 1040-SR form, many taxpayers encounter common pitfalls that can lead to complications in their tax returns. One significant mistake is failing to report all capital gains and losses. Taxpayers often overlook certain transactions, especially if they occurred throughout the year in various accounts. Each sale of stock or property that results in a gain or loss needs to be included to avoid penalties and potential audits.

Another common error is miscalculating the basis of an asset. It’s crucial to determine the original purchase price plus any associated costs, such as commissions or improvements, when figuring out gains or losses. If an incorrect basis is reported, it can considerably alter the taxable amount. Double-checking calculations can help prevent this costly mistake.

Many individuals also neglect to distinguish between short-term and long-term capital gains. The IRS treats these categories differently, with long-term gains typically taxed at a lower rate. Misclassifying a sale could result in overpayment of taxes. It’s essential to understand the holding period for each asset before marking its sale on Schedule D.

Accuracy in reporting losses is equally important. Taxpayers sometimes exceed the limits on capital losses that can be deducted in a given tax year. Currently, the maximum loss that can be deducted against ordinary income is $3,000 for individuals and married couples filing jointly. Awareness of these caps is vital to ensure compliance with tax regulations.

Another frequent oversight is the lack of supporting documentation for transactions reported on Schedule D. Taxpayers must keep accurate records, including purchase confirmations and sale receipts, to validate their claims. Failing to provide this evidence can create issues during reviews or audits.

Lastly, many people simply forget to sign and date their returns. Omitting these steps can lead the IRS to treat the submission as incomplete, causing delays and potential penalties. Ensuring that all parts of the form are finalized is a small but essential step in the process.

The IRS Schedule D is an important tax document for individuals reporting capital gains and losses. However, it often accompanies several other forms and documents to ensure accurate reporting of an individual's financial situation. Below are six common forms and documents that are frequently used alongside Schedule D.

The IRS Schedule D Form, which is used to report capital gains and losses, has similarities with several other tax documents. Understanding these parallels can help clarify your overall tax situation. Here are four documents that are similar to the Schedule D Form:

When filling out the IRS Schedule D 1040 or 1040-SR form, it's essential to follow certain best practices while avoiding common pitfalls. Here’s a concise list of dos and don’ts.

Here are eight common misconceptions about the IRS Schedule D 1040 or 1040-SR form, which is used to report capital gains and losses:

Understanding these misconceptions can help ensure that individuals file their taxes correctly and are aware of their responsibilities. It’s always advisable to stay informed about tax rules and consult a tax professional if unsure.

When filling out the IRS Schedule D 1040 or 1040-SR form, it is crucial to keep several important points in mind. These takeaways will guide you through the process efficiently.

It is essential to approach this process thoughtfully to ensure compliance and maximize your tax benefits.