Understanding the IRS Schedule K-1 1041 form is essential for beneficiaries of estates or trusts as it provides a detailed overview of income, deductions, and credits they need to report on their personal tax returns. This document, often generated by the estate or trust, breaks down the individual's share of income, ensuring transparency and accuracy in tax liability. Billions of dollars pass through these entities annually, making the information on a K-1 form quite significant. It includes key details, such as interest, dividends, capital gains, and other sources of income, allowing the recipient to assess their financial situation properly. Additionally, the K-1 1041 plays a crucial role in the distribution of income; it helps beneficiaries understand not just what they received but also how it fits into the larger context of their tax obligations. With the right guidance, navigating the intricacies of this form can be a straightforward process, helping ensure that beneficiaries comply with tax regulations while maximizing potential benefits.

Schedule |

|

|

|

2019 |

||

(Form 1041) |

|

|

|

|||

Department of the Treasury |

|

|

For calendar year 2019, or tax year |

|||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

|

|

beginning |

|

/ |

/ 2019 |

ending |

/ |

/ |

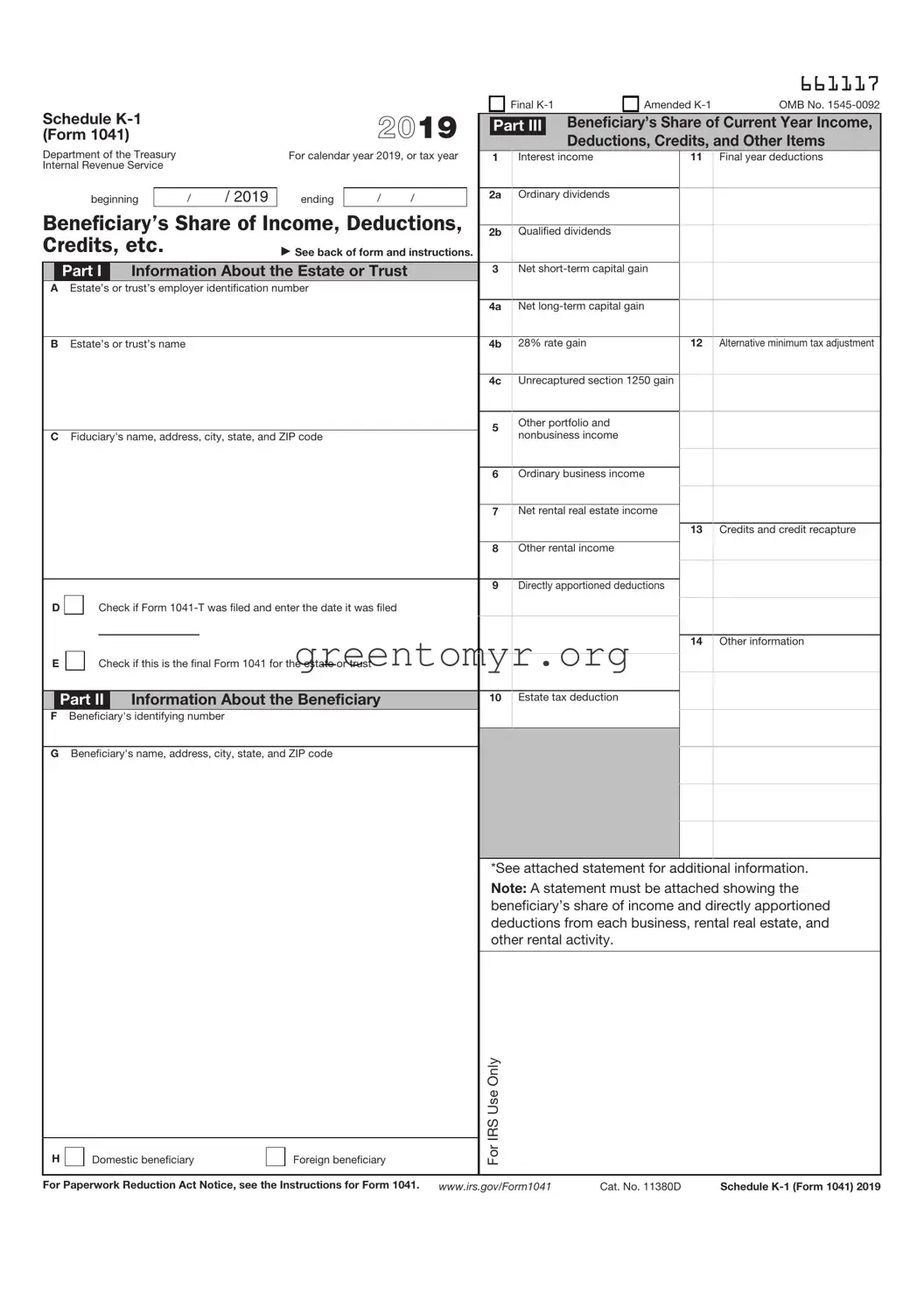

Beneficiary’s Share of Income, Deductions, Credits, etc.

Part I Information About the Estate or Trust

AEstate’s or trust’s employer identification number

BEstate’s or trust’s name

CFiduciary's name, address, city, state, and ZIP code

D |

|

|

Check if Form |

|

E |

|

|

|

|

|

|

Check if this is the final Form 1041 for the estate or trust |

||

|

|

|||

Part II Information About the Beneficiary

FBeneficiary's identifying number

GBeneficiary's name, address, city, state, and ZIP code

H |

|

Domestic beneficiary |

|

Foreign beneficiary |

|

|

|

|

|

|

|

661117 |

|

|

Final |

|

Amended |

OMB No. |

||

|

Part III |

|

Beneficiary’s Share of Current Year Income, |

||||

|

|

|

|

Deductions, Credits, and Other Items |

|||

1 |

Interest income |

11 |

Final year deductions |

||||

|

|

|

|

|

|||

2a |

Ordinary dividends |

|

|

|

|||

|

|

|

|

|

|||

2b |

Qualified dividends |

|

|

|

|||

3Net

4a |

Net |

|

4b |

28% rate gain |

12 Alternative minimum tax adjustment |

|

|

|

4c |

Unrecaptured section 1250 gain |

|

5Other portfolio and nonbusiness income

6Ordinary business income

7Net rental real estate income

13 Credits and credit recapture

8Other rental income

9Directly apportioned deductions

14 Other information

10Estate tax deduction

*See attached statement for additional information.

Note: A statement must be attached showing the beneficiary’s share of income and directly apportioned deductions from each business, rental real estate, and other rental activity.

For IRS Use Only

For Paperwork Reduction Act Notice, see the Instructions for Form 1041. |

www.irs.gov/Form1041 |

Cat. No. 11380D |

Schedule |

Schedule |

Page 2 |

This list identifies the codes used on Schedule

Report on

Form 1040 or

Form 1040 or

Form 1040 or

Schedule D, line 5

Schedule D, line 12

28% Rate Gain Worksheet, line 4 (Schedule D Instructions)

Unrecaptured Section 1250 Gain

Worksheet, line 11 (Schedule D

Instructions)

Schedule E, line 33, column (f)

Schedule E, line 33, column (d) or (f)

Schedule E, line 33, column (d) or (f)

Schedule E, line 33, column (d) or (f)

9. Directly apportioned deductions |

|

|

Code |

|

|

A Depreciation |

Form 8582 or Schedule E, line |

|

|

33, column (c) or (e) |

|

B Depletion |

Form 8582 or Schedule E, line |

|

|

33, column (c) or (e) |

|

C Amortization |

Form 8582 or Schedule E, line |

|

|

33, column (c) or (e) |

|

10. Estate tax deduction |

Schedule A, line 16 |

|

11. Final year deductions |

|

|

A Excess deductions |

See the beneficiary's instructions |

|

B |

Schedule D, line 5 |

|

C |

Schedule D, line 12; line 5 of the |

|

|

wksht. for Sch. D, line 18; and |

|

|

line 16 of the wksht. for Sch. D, |

|

|

line 19 |

|

D Net operating loss carryover — |

Form 1040 or |

|

regular tax |

1, line 8 |

|

E Net operating loss carryover — |

Form 6251, line 2f |

|

minimum tax |

} |

|

12. Alternative minimum tax (AMT) items |

|

|

A Adjustment for minimum tax purposes |

Form 6251, line 2j |

|

B AMT adjustment attributable to |

|

|

qualified dividends |

|

|

C AMT adjustment attributable to |

|

|

net |

|

|

D AMT adjustment attributable to |

|

|

net |

|

See the beneficiary’s |

|

|

|

E AMT adjustment attributable to |

|

instructions and the |

unrecaptured section 1250 gain |

|

Instructions for Form 6251 |

F AMT adjustment attributable to 28% rate gain

G Accelerated depreciation

HDepletion

IAmortization

J Exclusion items |

2020 Form 8801 |

|

Code |

|

|

Report on |

|

A Credit for estimated taxes |

|

|

Form 1040 or |

|

|

|

|

3, line 8 |

|

B Credit for backup withholding |

|

|

Form 1040 or |

|

C |

|

|

|

|

D Rehabilitation credit and energy credit |

|

|

|

|

E Other qualifying investment credit |

|

|

|

|

F Work opportunity credit |

|

|

|

|

G Credit for small employer health |

|

|

|

|

insurance premiums |

|

|

|

|

H Biofuel producer credit |

|

|

|

|

I Credit for increasing research activities |

|

|

|

|

J Renewable electricity, refined coal, |

|

|

|

|

and Indian coal production credit |

|

|

|

|

K Empowerment zone employment credit |

See the beneficiary’s instructions |

||

|

L Indian employment credit |

|

}Form 1040 or |

|

|

M Orphan drug credit |

|

||

|

N Credit for |

|||

|

care and facilities |

|

||

|

O Biodiesel and renewable diesel |

fuels |

||

|

credit |

|

||

|

P Credit to holders of tax credit bonds |

|||

|

Q Credit for employer differential wage |

|||

|

payments |

|

||

|

R Recapture of credits |

|

||

|

Z Other credits |

|

||

14. |

Other information |

|

||

A |

|

|||

|

B Foreign taxes |

|

|

Form 1040 or |

|

|

|

|

3, line 1 or Sch. A, line 6 |

|

C Reserved |

|

|

|

|

D Reserved |

|

|

|

|

E Net investment income |

|

|

Form 4952, line 4a |

|

F Gross farm and fishing income |

|

|

Schedule E, line 42 |

|

G Foreign trading gross receipts |

|

|

See the Instructions for |

|

(IRC 942(a)) |

|

|

Form 8873 |

|

H Adjustment for section 1411 net |

|

|

Form 8960, line 7 (also see the |

|

investment income or deductions |

|

beneficiary's instructions) |

|

|

I Section 199A information |

|

|

See the beneficiary’s instructions |

|

Z Other information |

|

|

See the beneficiary’s instructions |

|

|

|

|

|

Note: If you are a beneficiary who does not file a Form 1040 or 1040- SR, see instructions for the type of income tax return you are filing.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule K-1 (Form 1041) is used to report income, deductions, and credits from estates and trusts to beneficiaries. |

| Who Reports | Fiduciaries of estates or trusts complete the form to provide required information to the IRS and to the recipients. |

| Recipient's Role | Beneficiaries receiving the Schedule K-1 use it to report their share of income and deductions on their individual tax returns. |

| State-Specific Forms | Some states have their own versions of the K-1 for state tax purposes, governed by local tax laws. |

| Filing Deadlines | The Schedule K-1 must be issued to beneficiaries by the tax filing deadline of the estate or trust, typically April 15 for calendar-year tax returns. |

When preparing to fill out the IRS Schedule K-1 (Form 1041), it’s important to gather all required information about the estate or trust and its beneficiaries. After you complete this form, it will help you accurately report income, deductions, and credits on your tax return.

Completing this form accurately is crucial. Once finished, the Schedule K-1 must be distributed to each beneficiary involved, which allows them to report their share of the income on their personal tax returns.

The IRS Schedule K-1 1041 form is a tax document used to report income, deductions, and credits for beneficiaries of estates and trusts. Each beneficiary receives a K-1 that details their share of the estate’s or trust’s financial activity for the year. This form helps individuals accurately report their income on their personal tax returns.

Fiduciaries of estates or trusts are responsible for filing Schedule K-1 1041. If an estate or trust generates income, the fiduciary must prepare and distribute K-1 forms to beneficiaries. Individuals receiving distributions from estates or trusts will also need this form to report their income.

Schedule K-1 1041 reports various types of income that include:

Each beneficiary will receive a detailed breakdown of their share of these earnings.

When preparing your tax return, you'll use the information from Schedule K-1 1041 to complete the appropriate sections. Generally, the income reported on the K-1 will flow into different lines in Form 1040, depending on the type of income received. For example:

Always double-check with current IRS guidelines or a tax professional to ensure accurate reporting.

Typically, beneficiaries receive Schedule K-1 1041 after the trust or estate files its tax return. This usually happens by the tax deadline, which is generally April 15. However, if the estate or trust cannot finalize its tax return on time, beneficiaries may experience delays in receiving their K-1 forms.

If the deadline has passed and you have not received your K-1, it is advisable to first contact the fiduciary or administrator of the trust or estate. They can provide information regarding the status of the filings. Additionally, keep in mind that some estates or trusts may issue amended K-1 forms if adjustments are required.

In cases where you discover errors on your K-1, reach out to the fiduciary immediately to request a correction. You may need the corrected form for your tax filings. Once you receive the amended K-1, ensure that you properly replace the incorrect information on your tax return.

Yes, failing to report income received from Schedule K-1 1041 can lead to penalties from the IRS. These may include interest charges on unpaid taxes and potential fines for underreporting income. It's essential to include any K-1 income on your tax return to avoid complications and ensure compliance with tax regulations.

Filling out the IRS Schedule K-1 Form 1041 can feel daunting, especially if you're doing it for the first time. This form is crucial for reporting income, deductions, and credits from estates and trusts, but many make common mistakes that can lead to complications. Understanding these pitfalls can help ensure that your submission goes smoothly and accurately.

One prevalent mistake is not providing the correct taxpayer identification number (TIN). Every beneficiary must ensure that their TIN is accurate and matches their Social Security number or business identification. Errors in this area can lead to delays or issues with the IRS. Precision matters; double-check the numbers before submitting.

Another mistake often made is neglecting to report all income accurately. Beneficiaries might overlook certain types of income, such as capital gains or interest that were distributed throughout the year. It’s important to review what is reported on the K-1 carefully. Comprehensive reporting ensures that you’re compliant and reduces the risk of an audit.

Many also forget to verify the distribution amounts reported by the trust or estate. If the K-1 shows a distribution total that doesn’t match your records, it’s essential to communicate with the fiduciary responsible for the trust. Clarifying discrepancies early can save a lot of time and potential headaches later.

Using the wrong tax form is another common error. Some beneficiaries mistakenly file their K-1 information on the wrong type of tax return. For example, individuals must use Form 1040 for personal income, while entities like corporations and partnerships have different forms. Ensure you’re using the appropriate form to avoid issues with the IRS.

Underestimating the importance of checking for updated instructions can result in submitting outdated information. Tax laws often change, and the IRS regularly updates forms and guidelines. Before filling out the K-1, make sure to review the current year's instructions. Staying informed can help you avoid last year’s mistakes.

Another frequent oversight involves not keeping accurate records of distributions received. Remembering every detail can be challenging, particularly if distributions occurred throughout the year. Keeping thorough documentation not only aids during tax season but also helps track any discrepancies in the future.

Lastly, a lack of communication with the trustee or executor can lead to various misunderstandings and errors. Being proactive can help clarify any uncertainties regarding your K-1. Don’t hesitate to ask questions if anything seems unclear. Effective communication with the person managing the trust or estate is essential for a smooth filing process.

The IRS Schedule K-1 (Form 1041) is often part of various tax documents that provide essential information on the distribution of income, deductions, and credits from estates or trusts. When dealing with estates or trusts, it is helpful to understand the other forms and documents that often accompany the Schedule K-1. Each of these has its purpose and plays a role in the overall tax filing process. Here’s a brief overview of these related forms and documents.

Understanding these forms and documents is essential for ensuring compliance and accurate tax reporting. Each plays a distinct role in the process and contributes to a clearer picture of an estate or trust’s financial standing for both the fiduciaries and the beneficiaries. Proper documentation can make tax filing smoother and provide peace of mind.

The IRS Schedule K-1 (Form 1041) is used to report income, deductions, and credits from estates and trusts. Several other documents share similarities with the Schedule K-1 in terms of their purpose and reporting mechanisms. Below is a list of nine documents that have comparable functions.

Each of these documents plays a unique role in the tax reporting system but ultimately serves the same purpose: to ensure that income and deductions are accurately reported and accounted for by individuals and entities alike.

Filling out the IRS Schedule K-1 (Form 1041) requires attention to detail and can impact your tax responsibilities. Here are some important do's and don'ts to keep in mind:

The IRS Schedule K-1 (Form 1041) is an important document for beneficiaries of estates and trusts, yet there are several misconceptions surrounding it. Here are six common misunderstandings:

This is not true. While estates and partnerships commonly use this form, trusts also file Schedule K-1. It is essential for determining how income is distributed among beneficiaries.

Not necessarily. While K-1 reports your share of income, deductions, and credits, it does not automatically trigger taxes. Your tax liability depends on your overall tax situation.

This is a misconception. Certain types of income may not be taxable. For example, distributions from a trust can include tax-exempt income or returns of principal.

The issuance of Schedule K-1 can vary. Trusts and estates have deadlines for filing that can differ from individual tax returns, often leading to delays.

Actually, providing a K-1 to beneficiaries is required when the trust or estate has reportable income. This helps beneficiaries report their share accurately on their tax returns.

This is misleading. Beneficiaries also need the K-1 for their personal tax records and to file accurate tax returns. Keeping a copy is crucial for future reference.

IRS Schedule K-1 (Form 1041) is used to report income, deductions, and credits from an estate or trust to the beneficiaries. Understanding this form is key for both the fiduciaries and the recipients.

Each beneficiary receives their own K-1, which details their share of the estate or trust income. The information provided helps beneficiaries accurately report income on their individual tax returns.

Filing deadlines are crucial. The estate or trust must file Form 1041 by the 15th day of the fourth month after the end of the tax year. Ensure that K-1s are distributed to beneficiaries by this deadline to avoid last-minute complications.

Keep accurate records. Both the fiduciary and beneficiaries should maintain records related to the K-1, including any supporting documents. This aids in clarifying any potential questions or audits from the IRS.