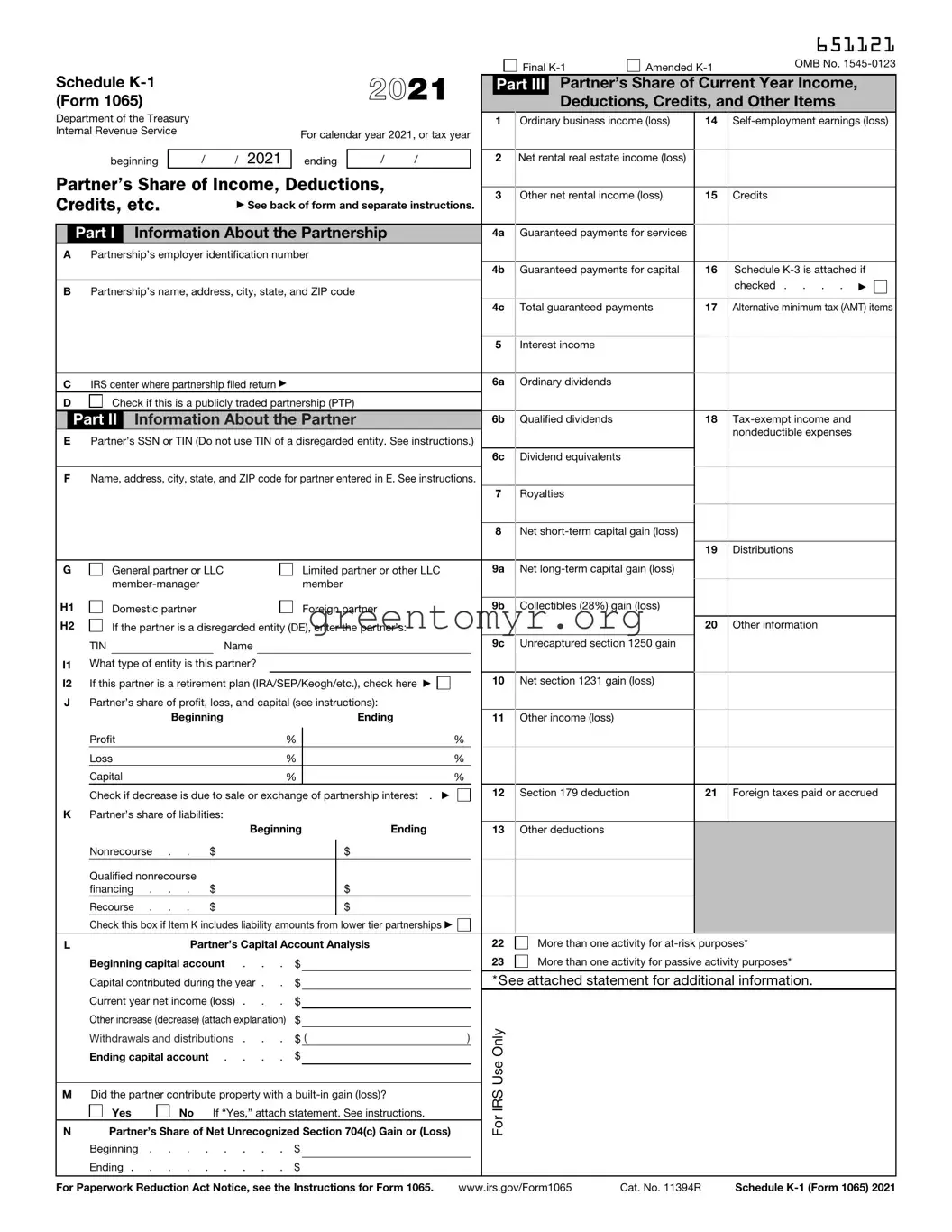

When it comes to understanding your tax obligations as a partner in a partnership, the IRS Schedule K-1 (Form 1065) is a crucial document to familiarize yourself with. This form provides a detailed account of your share of the partnership's income, deductions, and credits, ensuring transparency and accuracy in reporting your earnings to the IRS. Each partner receives a Schedule K-1, which breaks down their individual financial stake in the partnership, including details on profits, losses, and other relevant financial activities. It's important to note that this form does not reflect taxes owed; instead, it shows how much of the partnership's financial performance must be reported on your personal tax return. Missing or misreporting this information can lead to complications with the IRS, making it essential to handle the Schedule K-1 correctly. With deadlines approaching and tax season on the horizon, taking the time to gather and review this information can help you navigate your responsibilities effectively and avoid potential pitfalls.

Schedule |

|

|

|

2019 |

||

(Form 1065) |

|

|

|

|||

Department of the Treasury |

|

|

|

|

|

|

Internal Revenue Service |

|

|

For calendar year 2019, or tax year |

|||

|

|

|

|

|||

|

|

|

|

ending |

|

|

beginning |

|

/ |

/ 2019 |

/ |

/ |

|

Partner’s Share of Income, Deductions, Credits, etc.

Part I Information About the Partnership

APartnership’s employer identification number

BPartnership’s name, address, city, state, and ZIP code

CIRS Center where partnership filed return

D |

Check if this is a publicly traded partnership (PTP) |

Part II Information About the Partner

EPartner’s SSN or TIN (Do not use TIN of a disregarded entity. See inst.)

FName, address, city, state, and ZIP code for partner entered in E. See instructions.

G |

General partner or LLC |

Limited partner or other LLC |

|

member |

|

H1 |

Domestic partner |

Foreign partner |

H2 |

If the partner is a disregarded entity (DE), enter the partner’s: |

|

|

TIN |

|

Name |

|

|

I1 |

What type of entity is this partner? |

|

|||

I2 |

If this partner is a retirement plan (IRA/SEP/Keogh/etc.), check here |

||||

JPartner’s share of profit, loss, and capital (see instructions):

Beginning |

|

Ending |

|

Profit |

% |

|

% |

Loss |

% |

|

% |

Capital |

% |

|

% |

Check if decrease is due to sale or exchange of partnership interest . . |

|

||

KPartner’s share of liabilities:

|

|

|

Beginning |

Ending |

|

||||

|

Nonrecourse . . |

$ |

|

|

|

$ |

|

|

|

|

Qualified nonrecourse |

|

|

|

|

|

|

|

|

|

financing . . . |

$ |

|

|

|

$ |

|

|

|

|

Recourse . . . |

$ |

|

|

|

$ |

|

|

|

|

Check this box if Item K includes liability amounts from lower tier partnerships. |

|

|||||||

L |

Partner’s Capital Account Analysis |

|

|

||||||

|

Beginning capital account . . . |

$ |

|

|

|

|

|||

|

Capital contributed during the. year |

. |

$ |

|

|

|

|

||

|

Current year net income (loss) . . . |

$ |

|

|

|

|

|||

|

Other increase (decrease) (attach explanation) |

$ |

|

|

|

|

|||

|

Withdrawals & distributions |

. . . |

$ ( |

|

) |

|

|||

|

Ending capital account . . . . |

$ |

|

|

|

|

|||

MDid the partner contribute property with a

Yes |

No If “Yes,” attach statement. See instructions. |

NPartner’s Share of Net Unrecognized Section 704(c) Gain or (Loss)

Beginning . . . . . . .$ .

Ending . . . . . . . .$ .

651119

Final |

Amended |

OMB No. |

|

Part III Partner’s Share of Current Year Income, Deductions, Credits, and Other Items

1 |

Ordinary business income (loss) |

15 Credits |

2Net rental real estate income (loss)

3 |

Other net rental income (loss) |

16 Foreign transactions |

4a |

Guaranteed payments for services |

|

|

||

4b |

Guaranteed payments for capital |

|

|

||

4c |

Total guaranteed payments |

|

|

5Interest income

6a |

Ordinary dividends |

|

6b |

Qualified dividends |

|

|

||

6c |

Dividend equivalents |

17 Alternative minimum tax (AMT) items |

7Royalties

8Net

9a |

Net |

18 |

|

|

|

|

nondeductible expenses |

9b |

Collectibles (28%) gain (loss) |

|

|

9c |

Unrecaptured section 1250 gain |

|

|

|

|

||

10 |

Net section 1231 gain (loss) |

|

|

|

|

||

|

|

|

|

|

|

19 |

Distributions |

11Other income (loss)

20 Other information

12Section 179 deduction

13Other deductions

14

21 More than one activity for

22 More than one activity for passive activity purposes*

*See attached statement for additional information.

For IRS Use Only

For Paperwork Reduction Act Notice, see Instructions for Form 1065. |

www.irs.gov/Form1065 |

Cat. No. 11394R |

Schedule |

Schedule |

Page 2 |

This list identifies the codes used on Schedule

1.Ordinary business income (loss). Determine whether the income (loss) is passive or nonpassive and enter on your return as follows.

Report on

See the Partner’s Instructions

Schedule E, line 28, column (h)

See the Partner’s Instructions

Schedule E, line 28, column (k)

See the Partner’s Instructions

4a. Guaranteed payment Services

4b. Guaranteed payment Capital

4c. Guaranteed payment Total

5. Interest income

6a. Ordinary dividends

6b. Qualified dividends

6c. Dividend equivalents

7. Royalties

8. Net

9a. Net

9b. Collectibles (28%) gain (loss)

9c. Unrecaptured section 1250 gain

10. Net section 1231 gain (loss)

11.Other income (loss)

Code |

|

|

|

A |

Other portfolio income (loss) |

|

See the Partner’s Instructions |

B |

Involuntary conversions |

|

See the Partner’s Instructions |

C |

Sec. 1256 contracts & straddles |

|

Form 6781, line 1 |

D |

Mining exploration costs recapture |

See Pub. 535 |

|

E |

Cancellation of debt |

|

|

F |

Section 743(b) positive adjustments |

|

|

G |

Section 965(a) inclusion |

} |

See the Partner’s Instructions |

H |

Income under subpart F (other |

||

|

than inclusions under sections |

|

|

|

951A and 965) |

|

|

IOther income (loss)

12. |

Section 179 deduction |

} |

See the Partner’s Instructions |

|

13. |

Other deductions |

|

||

|

A |

Cash contributions (60%) |

|

|

|

B |

Cash contributions (30%) |

|

|

|

C |

Noncash contributions (50%) |

|

|

|

D |

Noncash contributions (30%) |

See the Partner’s Instructions |

|

|

E |

Capital gain property to a 50% |

||

|

|

|||

|

F |

organization (30%) |

|

|

|

Capital gain property (20%) |

|

||

|

G |

Contributions (100%) |

|

|

|

H |

Investment interest expense |

|

Form 4952, line 1 |

|

I |

|

Schedule E, line 19 |

|

|

J |

Section 59(e)(2) expenditures |

|

See the Partner’s Instructions |

|

K |

Excess business interest expense |

See the Partner’s Instructions |

|

|

L |

|

Schedule A, line 16 |

|

|

M |

Amounts paid for medical insurance |

Schedule A, line 1, or Schedule 1 |

|

|

N |

|

|

(Form 1040 or |

|

Educational assistance benefits |

|

See the Partner’s Instructions |

|

|

O |

Dependent care benefits |

|

Form 2441, line 12 |

|

P |

Preproductive period expenses |

|

See the Partner’s Instructions |

QCommercial revitalization deduction

R |

from rental real estate activities |

|

See Form 8582 instructions |

Pensions and IRAs |

|

See the Partner’s Instructions |

|

S |

Reforestation expense deduction |

See the Partner’s Instructions |

|

T |

through U |

} |

Reserved for future use |

V |

Section 743(b) negative adjustments |

|

|

W |

Other deductions |

See the Partner’s Instructions |

|

X |

Section 965(c) deduction |

|

|

14.

Note: If you have a section 179 deduction or any

ANet earnings (loss) from

B |

} |

Schedule SE, Section A or B |

|

Gross farming or fishing income |

See the Partner’s Instructions |

||

C |

Gross |

See the Partner’s Instructions |

|

15. Credits |

|

||

A |

|

||

|

(section 42(j)(5)) from |

|

|

B |

buildings |

|

|

|

|||

C |

(other) from |

|

|

|

|||

|

(section 42(j)(5)) from |

|

|

D |

See the Partner’s Instructions |

||

|

|||

|

(other) from |

|

|

E |

buildings |

|

|

Qualified rehabilitation |

|

||

|

expenditures (rental real estate) |

|

|

FOther rental real estate credits G Other rental credits

Code |

|

Report on |

|

H |

Undistributed capital gains credit |

Schedule 3 (Form 1040 or |

|

I |

|

|

line 13, box a |

Biofuel producer credit |

} |

See the Partner’s Instructions |

|

J |

Work opportunity credit |

|

|

K |

Disabled access credit |

|

|

L |

Empowerment zone |

|

|

M |

employment credit |

|

|

Credit for increasing research |

|

See the Partner’s Instructions |

|

|

activities |

|

|

N |

|

|

|

Credit for employer social |

|

|

|

|

security and Medicare taxes |

|

|

OBackup withholding P Other credits

16. Foreign transactions |

} |

|

|

A |

Name of country or U.S. |

|

|

B |

possession |

Form 1116, Part I |

|

Gross income from all sources |

|||

C |

Gross income sourced at |

|

|

partner level |

|

||

Foreign gross income sourced at partnership level |

|||

D |

Reserved for future use |

} |

|

E |

Foreign branch category |

|

|

F |

Passive category |

|

Form 1116, Part I |

G |

General category |

|

|

|

|

||

HOther

Deductions allocated and apportioned at partner level

I |

Interest expense |

Form 1116, Part I |

J |

Other |

Form 1116, Part I |

Deductions allocated and apportioned at partnership level to foreign source income

KReserved for future use L Foreign branch category

M Passive category |

}Form 1116, Part I |

NGeneral category O Other

Other information

P |

Total foreign taxes paid |

Form 1116, Part II |

Q |

Total foreign taxes accrued |

Form 1116, Part II |

R |

Reduction in taxes available for credit Form 1116, line 12 |

|

S |

Foreign trading gross receipts |

Form 8873 |

T |

Extraterritorial income exclusion |

Form 8873 |

U |

through V |

Reserved for future use |

W |

Section 965 information |

} See the Partner’s Instructions |

X |

Other foreign transactions |

|

17. Alternative minimum tax (AMT) items |

||

A |

See the Partner’s |

|

B |

Adjusted gain or loss |

|

C |

Depletion (other than oil & gas) |

Instructions and |

D |

Oil, gas, & |

the Instructions for |

E |

Oil, gas, & |

}Form 6251 |

F Other AMT items

18.

|

A |

|

Form 1040 or |

|

|

B |

Other |

|

See the Partner’s Instructions |

|

C |

Nondeductible expenses |

|

See the Partner’s Instructions |

19. |

Distributions |

} |

|

|

|

A |

Cash and marketable securities |

See the Partner’s Instructions |

|

|

B |

Distribution subject to section 737 |

||

|

C |

Other property |

|

|

20. |

Other information |

|

|

|

|

A |

Investment income |

|

Form 4952, line 4a |

|

B |

Investment expenses |

|

Form 4952, line 5 |

|

C |

Fuel tax credit information |

} |

Form 4136 |

|

D |

Qualified rehabilitation expenditures |

|

|

|

E |

(other than rental real estate) |

|

See the Partner’s Instructions |

|

Basis of energy property |

|

||

Fthrough G

H |

Recapture of investment credit |

|

See Form 4255 |

I |

Recapture of other credits |

|

See the Partner’s Instructions |

J |

|

|

|

K |

|

See Form 8697 |

|

|

|||

L |

method |

} |

See Form 8866 |

Dispositions of property with |

|

||

M |

section 179 deductions |

|

|

Recapture of section 179 deduction |

|

||

N |

Interest expense for corporate |

|

|

|

partners |

|

|

O |

through Y |

|

|

Z |

Section 199A information |

|

|

AA |

Section 704(c) information |

See the Partner’s Instructions |

|

AB |

Section 751 gain (loss) |

||

AC |

Section 1(h)(5) gain (loss) |

|

|

AD |

Deemed section 1250 |

|

|

AE |

unrecaptured gain |

|

|

Excess taxable income |

|

||

AF |

Excess business interest income |

|

|

AG |

Gross receipts for section 59A(e) |

|

|

AH |

Other information |

|

|

| Fact Name | Description |

|---|---|

| What is Schedule K-1? | Schedule K-1 (Form 1065) is used to report income, deductions, and credits from partnerships. It provides information to both the IRS and individual partners. |

| Who Receives a K-1? | Each partner in a partnership receives a K-1 after the partnership files its Form 1065. This includes general partners and limited partners alike. |

| Filing Requirements | Partnerships must file Form 1065 yearly, and they are required to issue K-1 forms to all partners. Timeliness is crucial to avoid penalties. |

| Tax Implications | Partners report their share of the partnership's income or loss on their personal tax returns. This can affect their overall tax liability. |

| State-Specific Forms | Some states have their own versions of K-1, like California. Governing laws may differ, so it's essential for partners to check specific state requirements. |

| Information Included | A K-1 includes vital details such as the partner's share of income, gains, losses, and other tax-related information pertinent to each partner's tax situation. |

| Schedule K-1 Deadlines | Typically, Schedule K-1 must be issued by the partnership by March 15, aligning with the partnership tax return due date to facilitate timely personal filings. |

| Common Mistakes | Accuracy is key! Common errors include incorrect partner information or misreported amounts. Such mistakes can lead to issues during tax time. |

Once you have gathered all necessary financial information, you can begin filling out the IRS Schedule K-1 (Form 1065) for a partnership. This form is crucial for reporting each partner's share of income, deductions, and credits from the partnership. Follow the steps outlined below to ensure accurate completion.

After completing this form, ensure that you incorporate the information into your personal tax return accurately. The data reported on your K-1 will inform how you report your share of the partnership income on Form 1040.

The IRS Schedule K-1 1065 form is used to report income, deductions, and credits from partnerships. When a partnership files its annual tax return using Form 1065, each partner receives a K-1 that outlines their share of the partnership's earnings and losses. This information is crucial for partners to accurately complete their individual tax returns.

Every partner in a partnership will receive a Schedule K-1 1065. This includes both general partners, who manage the partnership, and limited partners, who typically invest but do not take part in day-to-day operations. Each partner's K-1 reflects their individual share of the partnership's financial activities for the tax year.

Partners use the information on their K-1 to report their portions of the partnership’s income or losses on their personal tax returns. This typically involves transferring relevant figures from the K-1 to the appropriate lines on IRS Form 1040. It's essential for partners to accurately report this information to avoid issues with the IRS.

If you notice errors on your K-1, contact the partnership as soon as possible. They may issue a corrected K-1 if necessary. If the K-1 is used to file your tax return, it is crucial to amend the return if you receive a corrected version after you’ve already submitted your tax forms. Ensuring accuracy with this information helps to maintain compliance with tax regulations.

Partnerships are typically required to issue K-1s by March 15 of each year. However, this can vary based on the partnership's specific filing deadline and structure. It is advisable to allow time for the preparation and distribution of these forms, as they are an integral part of the overall tax process.

If you do not receive your K-1 by the expected date, reach out to the partnership directly for assistance. They can provide updates on the status of your K-1. In situations where the partnership is unresponsive, it may be necessary to consult with a tax professional to discuss alternative approaches to filing your tax return, ensuring not to miss out on reporting your income correctly.

Filing the IRS Schedule K-1 (Form 1065) can be a complex process, and mistakes can easily happen. One common mistake is failing to report all sources of income. Partnerships often have multiple streams of income, such as interest or rental income. If a partner neglects to include these amounts, it can lead to discrepancies in their tax obligations.

Another frequent error involves incorrect or incomplete identification information. This includes the partner's name, address, and taxpayer identification number (TIN). A simple typographical error can delay processing and may cause issues with matching records at the IRS.

Inaccurate distributions are also a common pitfall. When partners receive various forms of distributions, they must be reported correctly on the K-1. Sometimes partners misinterpret the distribution amounts or mix them up with unrelated income, leading to incorrect filings.

Some individuals misunderstand the reporting of losses. While it's common for partners to have losses, they must be reported accurately to claim tax benefits. Ignoring these losses, or declaring them incorrectly, can trigger audits or reduce potential deductions.

Omitting necessary disclaimers is another mistake that shouldn’t be overlooked. Partners need to understand if they are passive or active in the business and how that status affects their reporting responsibilities. This information must be clearly indicated on the form to avoid later complications.

Additionally, failing to sign and date the form can render it invalid. Partnerships require all involved partners to sign, confirming their agreement with the information on the K-1. If any partner neglects this step, the filing may not be accepted by the IRS.

Lastly, some partners neglect the importance of reviewing their K-1 before submitting their tax returns. It is advisable to cross-verify the information with the partnership's records. Accuracy at this stage can save partners from unnecessary headaches when filing their personal tax returns.

The IRS Schedule K-1 (Form 1065) serves as an essential document for reporting income, deductions, and credits for partnerships. However, it often accompanies other important forms to give a complete financial picture. These documents ensure that all partners understand their tax obligations and the financial state of the partnership. Below is a list of related forms and documents that are commonly used in conjunction with the K-1.

Using these forms in conjunction with the Schedule K-1 helps create a comprehensive view of the partnership's financial activities. This thorough approach aids partners in meeting their tax responsibilities accurately and efficiently, fostering transparency and trust within the partnership.

When filling out the IRS Schedule K-1 (Form 1065), it's important to take special care. Here is a list of what you should and shouldn't do:

The IRS Schedule K-1 (Form 1065) is crucial for reporting income from partnerships. Misunderstandings about this form can lead to significant tax complications. Here are seven misconceptions regarding the Schedule K-1 that investors and partners often have:

Understanding these misconceptions can help partners better navigate their tax responsibilities and avoid potential pitfalls associated with the Schedule K-1.

The IRS Schedule K-1 (Form 1065) is used to report income, deductions, and credits for partnerships.

Each partner receives their own Schedule K-1, which details their share of the partnership's income and expenses.

Correctly completing the K-1 is essential for partners to accurately report their income on their personal tax returns.

K-1 forms should be issued to partners by the partnership after the partnership's tax return has been filed.

Information on the K-1 includes the partner's name, tax identification number, and their specific share of the partnership's items.

Ppartners may need to consult with a tax professional for guidance on how to properly report K-1 income.

It’s important to keep K-1 forms for records, as they may be needed for future tax returns or audits.

Filing deadlines for Schedule K-1 follow the partnership’s tax return deadlines, typically April 15 for most partnerships.