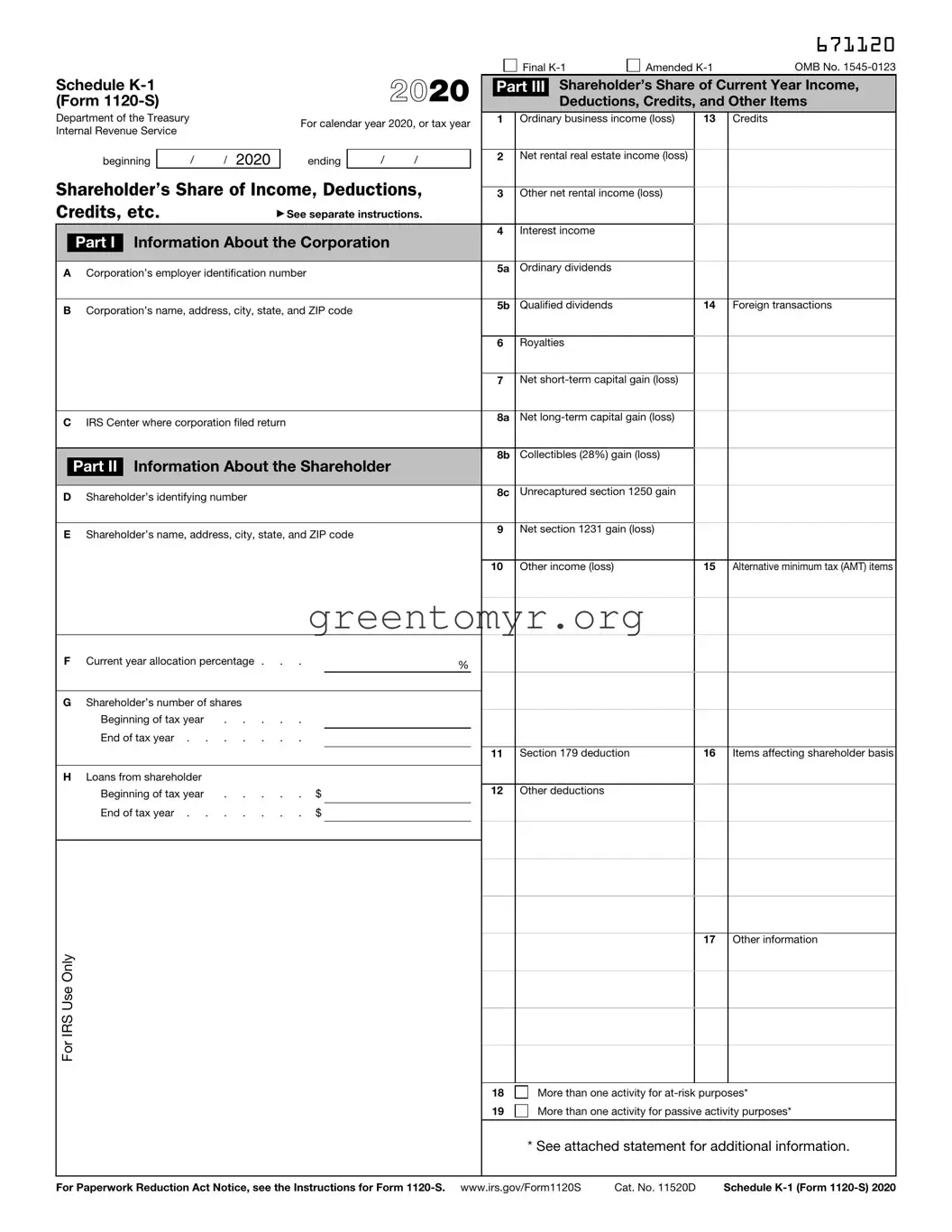

The IRS Schedule K-1 1120-S form plays a crucial role in the tax process for S corporations, serving as a means to report the income, deductions, and credits passed from the corporation to its shareholders. Designed for S corporations, this form provides a detailed breakdown of each shareholder's share of the entity's earnings or losses, ensuring that individual shareholders can accurately report their income on their personal tax returns. Each K-1 includes essential information such as the shareholder's identification details, their proportionate share of the S corporation’s income, and any applicable deductions or credits. Understanding the components of the Schedule K-1 is vital for shareholders as they navigate their personal tax obligations, given that taxes are not directly levied on the S corporation itself. Instead, the IRS allows the income to be reported on the owners’ personal tax forms, creating a pass-through taxation system. This feature distinguishes S corporations from other business structures and highlights the importance of the K-1 form in maintaining compliance with federal tax regulations.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

671120 |

|

|

|

|

|

|

|

|

|

|

2020 |

|

|

|

Final |

Amended |

OMB No. |

|||

Schedule |

|

|

|

|

|

|

|

Part III |

Shareholder’s Share of Current Year Income, |

||||||||||

(Form |

|

|

|

|

|

|

|

Deductions, Credits, and Other Items |

|||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

Department of the Treasury |

|

|

|

For calendar year 2020, or tax year |

|

1 |

Ordinary business income (loss) |

13 |

Credits |

||||||||||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

beginning |

|

/ |

/ 2020 |

|

ending |

|

/ |

/ |

|

2 |

Net rental real estate income (loss) |

|

|

||||

Shareholder’s Share of Income, Deductions, |

|

|

|

|

|||||||||||||||

|

3 |

Other net rental income (loss) |

|

|

|||||||||||||||

Credits, etc. |

|

|

▶ See separate instructions. |

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Interest income |

|

|

|

||

|

|

Part I |

Information About the Corporation |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A |

Corporation’s employer identification number |

|

|

|

|

5a |

Ordinary dividends |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B |

Corporation’s name, address, city, state, and ZIP code |

|

|

|

|

5b |

Qualified dividends |

|

14 |

Foreign transactions |

|||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

Royalties |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Net |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

C |

IRS Center where corporation filed return |

|

|

|

|

8a |

Net |

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8b |

Collectibles (28%) gain (loss) |

|

|

||

|

|

Part II |

Information About the Shareholder |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

D |

Shareholder’s identifying number |

|

|

|

|

|

|

|

8c |

Unrecaptured section 1250 gain |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

E |

Shareholder’s name, address, city, state, and ZIP code |

|

|

9 |

Net section 1231 gain (loss) |

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

10 |

Other income (loss) |

|

15 |

Alternative minimum tax (AMT) items |

|||

F Current year allocation percentage . . . |

% |

|

GShareholder’s number of shares

Beginning of tax year |

. . . . . |

|

|

|

|

|

|

|

End of tax year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11 |

Section 179 deduction |

16 Items affecting shareholder basis |

|

|

|

|

|

|

|

|

|

|

H Loans from shareholder |

|

|

|

|

|

|

|

|

Beginning of tax year |

. . . . . |

$ |

|

12 |

Other deductions |

|

||

|

|

|

|

|

|

|||

End of tax year . . |

. . . . . |

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

17 Other information

For IRS Use Only

18 More than one activity for

19 More than one activity for passive activity purposes*

* See attached statement for additional information.

For Paperwork Reduction Act Notice, see the Instructions for Form |

Cat. No. 11520D |

Schedule |

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule K-1 (Form 1120-S) is used to report income, deductions, and credits from an S corporation to its shareholders. |

| Filing Requirement | Each S corporation must file a Schedule K-1 for every shareholder who was active during the tax year. |

| Deadline | The form must be distributed to shareholders by the 15th day of the 3rd month after the end of the S corporation's tax year. |

| Tax Treatment | Income reported on the K-1 is generally passed through to shareholders, who report it on their personal tax returns. |

| State Specific Requirements | States may have their own forms similar to the federal K-1; for instance, California requires Form 568 for LLCs, governed under California Revenue and Taxation Code. |

| Components | The K-1 includes important information such as the shareholder's share of the corporation's income, losses, deductions, and credits. |

| Multiple Shareholdings | A shareholder who owns shares at different points during the year may receive multiple K-1s to reflect their varying ownership levels. |

| Amendments | If an S corporation makes adjustments after issuing a K-1, it may need to issue a corrected K-1 to reflect these changes. |

| Record Keeping | Shareholders should keep the K-1 for their records, as it may be needed for future tax filings or audits. |

| IRS Support | The IRS provides instructions and support for filling out Schedule K-1, which can greatly assist both corporations and shareholders. |

Completing the IRS Schedule K-1 (Form 1120-S) is a crucial task that allows shareholders of an S corporation to report their share of the corporation’s income, deductions, and credits on their personal tax returns. Once you have filled out the necessary details, ensure to review all entries for accuracy before submission to ensure compliance and avoid potential issues with the IRS.

The IRS Schedule K-1 1120-S form is used to report income, deductions, and credits from an S corporation. It is also known as the “Shareholder’s Share of Income, Deductions, Credits, etc.” This form provides detailed information to shareholders about their share of the corporation’s financial activities for the tax year.

The S corporation itself must file Form 1120-S with the IRS. Each shareholder then receives a Schedule K-1 that reflects their portion of the corporation’s income, losses, and other tax items. If you are a shareholder in an S corporation, you will receive this form.

The Schedule K-1 must be provided to shareholders by the due date of the S corporation's tax return. Typically, this is March 15 for calendar year filers. However, if the corporation has filed for an extension, the due date may be later.

Shareholders must report the amounts listed on the Schedule K-1 on their personal tax returns. Specifically, they will use the information to report their share of the S corporation’s income, losses, deductions, and credits on their Form 1040.

If you do not receive your Schedule K-1 in a timely manner, you should contact the S corporation. It is important to obtain this form to accurately report your income. You may need to file for an extension or estimate your tax liability if there are delays.

It is not advisable to file without the Schedule K-1. This document contains crucial information about your income from the S corporation. Filing without it may result in errors or underreporting your income, which could lead to penalties.

If you believe there is an error, contact the S corporation immediately. They will need to issue a corrected K-1 if there is indeed a mistake. It is essential to ensure that the information is accurate before you file your taxes.

Yes, foreign shareholders may have additional reporting requirements. They may be subject to U.S. tax on their share of income from the S corporation. It is advisable for foreign shareholders to consult with a tax professional to understand their specific obligations.

The IRS website offers forms, instructions, and a variety of resources related to Schedule K-1. You may also wish to consult with a tax professional or accountant for personalized assistance.

The IRS Schedule K-1 (Form 1120-S) plays a crucial role in reporting income, deductions, and credits from S corporations. However, many people make common mistakes when filling it out, which can lead to delays, errors in tax filings, or even audits. One major mistake involves incorrect reporting of shareholder information. It's essential to double-check names, Social Security numbers, and addresses. Even a simple typo can cause significant issues.

Another frequent error is the miscalculation of income or losses. Shareholders might overlook certain types of income or deductions, or they might incorrectly allocate amounts reported by the corporation. This can result in incorrect tax liabilities for the shareholders, leading to disputes with the IRS. A thorough review of the S corporation’s financial statements can help prevent these oversights.

Many individuals also fail to account for special allocations. S corporations can allocate income, deductions, and credits differently among shareholders, which may not always reflect their ownership percentage. Neglecting to follow these allocations can lead to incorrectly reported income on the K-1, which may not match the shareholder’s actual income. It’s vital to refer to both the corporate bylaws and the shareholder agreement during this process.

Finally, missing the filing deadline can have serious consequences. The Schedule K-1 must be provided to each shareholder by the S corporation before the shareholder files their tax return. If a K-1 arrives late, it can delay the shareholder’s tax filing. Additionally, it’s crucial that shareholders keep a copy of their K-1 for their records, as the IRS may request it during an audit. Ensuring timely distribution and documentation of the K-1 can help avoid unnecessary complications.

The IRS Schedule K-1 (Form 1120-S) is an important document that partnerships and S corporations use to report income, deductions, and credits. To ensure accurate tax reporting, several other forms and documents are often utilized alongside the K-1. Below is a list of commonly associated forms:

In conclusion, understanding these associated forms and documents is crucial for accurate tax preparation. Each document serves a specific purpose and will assist taxpayers in effectively reporting their income from S corporations or partnerships as detailed on their Schedule K-1.

When filling out the IRS Schedule K-1 (1120-S) form, it is important to ensure accuracy and completeness. Below is a list of things you should and shouldn’t do during this process.

Understanding the IRS Schedule K-1 1120-S form can be challenging, leading to several misconceptions. Below are seven common misunderstandings about this important tax document.

This is not entirely true. Only S Corporations that have shareholders need to issue a Schedule K-1 to report each shareholder's share of income, deductions, and credits.

Not all items reported on a K-1 result in taxable income. Some items may be tax-exempt or may allow you to deduct losses. Always review each item carefully.

This common misconception overlooks that employees or other non-owner recipients may also receive a K-1 if they have income or other allocations from an S Corporation.

Not necessarily. While receiving a K-1 may lead to tax reporting requirements, it does not automatically mean you will owe more taxes. Individual circumstances will vary.

While S Corporations strive for accuracy, errors can occur. Therefore, it is essential to verify the information provided on the K-1 against your records.

This is a misunderstanding, as K-1s can differ based on the type of business entity. Each kind of entity, like partnerships or estates, has its own format and reporting requirements.

This belief can be misleading. Regardless of total income, if you receive a K-1, you usually have an obligation to report that information on your tax return.

Being aware of these misconceptions can help individuals better navigate their tax obligations and improve their understanding of the Schedule K-1 form.

This list outlines important points to remember when filling out and using the IRS Schedule K-1 (1120-S) form: