The IRS Schedule M-3 is an essential form for corporations that require transparency in their financial reporting, particularly for those with total assets exceeding $10 million. Designed to supplement Form 1120, Schedule M-3 provides a detailed reconciliation of financial income and tax income. This schedule helps the IRS and taxpayers alike understand the differences arising from various accounting methods. It covers major aspects such as income adjustments, income statement items, and tax adjustments that impact tax liabilities. By requiring these disclosures, the IRS aims to enhance compliance and minimize tax avoidance. Corporations need to ensure that they complete this form accurately and thoroughly to avoid potential audits or penalties. Understanding the intricacies of Schedule M-3 can help businesses navigate their tax responsibilities more effectively.

SCHEDULE

(Rev. December 2019)

Department of the Treasury

Internal Revenue Service

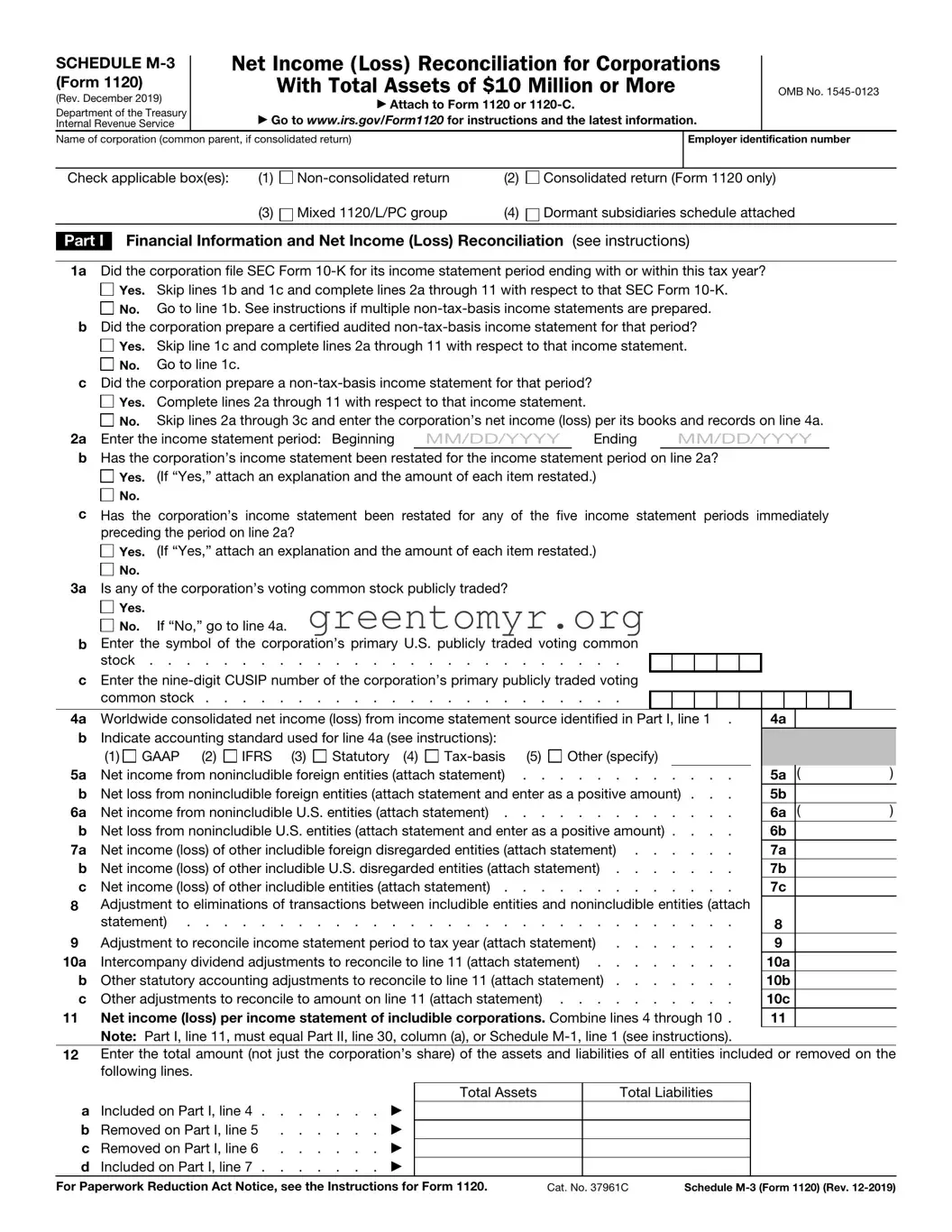

Net Income (Loss) Reconciliation for Corporations

With Total Assets of $10 Million or More

▶Attach to Form 1120 or

▶Go to www.irs.gov/Form1120 for instructions and the latest information.

OMB No.

Name of corporation (common parent, if consolidated return)

Employer identification number

Check applicable box(es): |

(1) |

(2) |

Consolidated return (Form 1120 only) |

|

|

(3) |

Mixed 1120/L/PC group |

(4) |

Dormant subsidiaries schedule attached |

|

|

|

|

|

Part I Financial Information and Net Income (Loss) Reconciliation (see instructions)

1a Did the corporation file SEC Form

Yes. Skip lines 1b and 1c and complete lines 2a through 11 with respect to that SEC Form

Yes. Skip lines 1b and 1c and complete lines 2a through 11 with respect to that SEC Form

No. Go to line 1b. See instructions if multiple

No. Go to line 1b. See instructions if multiple

bDid the corporation prepare a certified audited

Yes. Skip line 1c and complete lines 2a through 11 with respect to that income statement.

Yes. Skip line 1c and complete lines 2a through 11 with respect to that income statement.

No. Go to line 1c.

No. Go to line 1c.

cDid the corporation prepare a

Yes. Complete lines 2a through 11 with respect to that income statement.

Yes. Complete lines 2a through 11 with respect to that income statement.

No. Skip lines 2a through 3c and enter the corporation’s net income (loss) per its books and records on line 4a.

No. Skip lines 2a through 3c and enter the corporation’s net income (loss) per its books and records on line 4a.

2a Enter the income statement period: Beginning MM/DD/YYYY Ending MM/DD/YYYY

bHas the corporation’s income statement been restated for the income statement period on line 2a?

Yes. (If “Yes,” attach an explanation and the amount of each item restated.)

Yes. (If “Yes,” attach an explanation and the amount of each item restated.)

No.

No.

cHas the corporation’s income statement been restated for any of the five income statement periods immediately preceding the period on line 2a?

Yes. (If “Yes,” attach an explanation and the amount of each item restated.)

Yes. (If “Yes,” attach an explanation and the amount of each item restated.)

No.

No.

3a Is any of the corporation’s voting common stock publicly traded?

Yes.

Yes.

No. If “No,” go to line 4a.

bEnter the symbol of the corporation’s primary U.S. publicly traded voting common

stock . . . . . . . . . . . . . . . . . . . . . . . . . .

cEnter the

common stock . . . . . . . . . . . . . . . . . . . . . . .

4a Worldwide consolidated net income (loss) from income statement source identified in Part I, line 1 .

bIndicate accounting standard used for line 4a (see instructions):

(1) GAAP (2) |

IFRS (3) |

Statutory (4) |

Other (specify) |

5a Net income from nonincludible foreign entities (attach statement) . . . . . . . . . . . .

bNet loss from nonincludible foreign entities (attach statement and enter as a positive amount) . . .

6a Net income from nonincludible U.S. entities (attach statement) . . . . . . . . . . . . .

bNet loss from nonincludible U.S. entities (attach statement and enter as a positive amount) . . . .

7a |

Net income (loss) of other includible foreign disregarded entities (attach statement) |

b |

Net income (loss) of other includible U.S. disregarded entities (attach statement) |

c |

Net income (loss) of other includible entities (attach statement) |

8Adjustment to eliminations of transactions between includible entities and nonincludible entities (attach

|

statement) |

9 |

Adjustment to reconcile income statement period to tax year (attach statement) |

10a |

Intercompany dividend adjustments to reconcile to line 11 (attach statement) |

b |

Other statutory accounting adjustments to reconcile to line 11 (attach statement) |

c |

Other adjustments to reconcile to amount on line 11 (attach statement) |

11 |

Net income (loss) per income statement of includible corporations. Combine lines 4 through 10 . |

4a

|

|

|

5a |

( |

) |

5b |

|

|

6a |

( |

) |

6b |

|

|

7a |

|

|

7b |

|

|

7c |

|

|

8 |

|

|

9 |

|

|

10a |

|

|

10b |

|

|

10c |

|

|

11 |

|

|

Note: Part I, line 11, must equal Part II, line 30, column (a), or Schedule

12Enter the total amount (not just the corporation’s share) of the assets and liabilities of all entities included or removed on the following lines.

a |

Included on Part I, line 4 . |

. |

. . . |

. |

. |

▶ |

b Removed on Part I, line 5 |

. |

. . . |

. |

. |

▶ |

|

c Removed on Part I, line 6 |

. |

. . . |

. |

. |

▶ |

|

d |

Included on Part I, line 7 . |

. |

. . . |

. |

. |

▶ |

Total Assets

Total Liabilities

For Paperwork Reduction Act Notice, see the Instructions for Form 1120. |

Cat. No. 37961C |

Schedule |

Schedule |

Page 2 |

Name of corporation (common parent, if consolidated return)

Employer identification number

Check applicable box(es): (1) |

Consolidated group |

(2) |

Parent corp |

(3) |

Consolidated eliminations |

(4) |

Subsidiary corp (5) |

Mixed 1120/L/PC group |

Check if a |

1120 group (7) |

1120 eliminations |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Name of subsidiary (if consolidated return) |

|

|

|

|

|

Employer identification number |

||

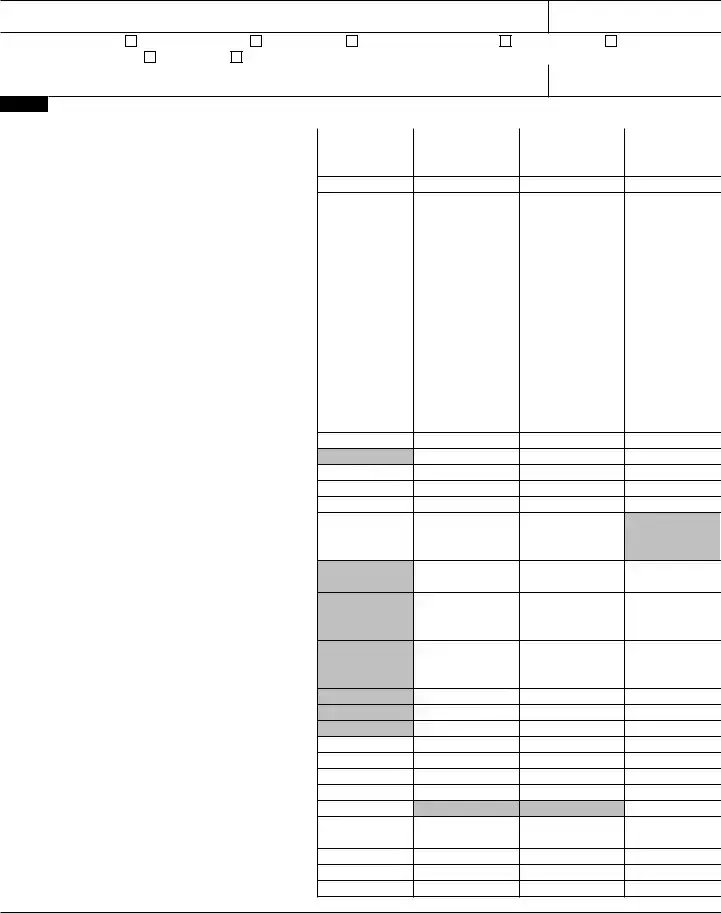

Part II Reconciliation of Net Income (Loss) per Income Statement of Includible Corporations With Taxable Income per Return (see instructions)

Income (Loss) Items |

(a) |

(b) |

(c) |

(d) |

Income (Loss) per |

Temporary |

Permanent |

Income (Loss) |

|

(Attach statements for lines 1 through 12) |

Income Statement |

Difference |

Difference |

per Tax Return |

1 Income (loss) from equity method foreign corporations |

|

|

|

|

2Gross foreign dividends not previously taxed . . .

3 |

Subpart F, QEF, and similar income inclusions . . |

|

|

|

|

|

4 |

|

|

|

|

|

|

5 |

Gross foreign distributions previously taxed . . . |

|

|

|

|

|

6 |

Income (loss) from equity method U.S. corporations |

|

|

|

|

|

7 |

U.S. dividends not eliminated in tax consolidation . |

|

|

|

|

|

8 |

Minority interest for includible corporations . . . |

|

|

|

|

|

9 |

Income (loss) from U.S. partnerships |

|

|

|

|

|

10 |

Income (loss) from foreign partnerships . . . . |

|

|

|

|

|

11 |

Income (loss) from other |

|

|

|

|

|

12 |

Items relating to reportable transactions . . . . |

|

|

|

|

|

13 |

Interest income (see instructions) |

|

|

|

|

|

14 |

Total accrual to cash adjustment |

|

|

|

|

|

15 |

Hedging transactions |

|

|

|

|

|

16 |

|

|

|

|

||

17 |

Cost of goods sold (see instructions) . . . . . ( |

) |

( |

) |

||

18Sale versus lease (for sellers and/or lessors) . . .

19 |

Section 481(a) adjustments |

20 |

Unearned/deferred revenue |

21 |

Income recognition from |

22Original issue discount and other imputed interest .

23a Income statement gain/loss on sale, exchange, abandonment, worthlessness, or other disposition of assets other than inventory and

b Gross capital gains from Schedule D, excluding amounts from

c Gross capital losses from Schedule D, excluding amounts from

d Net gain/loss reported on Form 4797, line 17, excluding amounts from

e Abandonment losses . . . . . . . . . .

f Worthless stock losses (attach statement) . . . .

g Other gain/loss on disposition of assets other than inventory

24Capital loss limitation and carryforward used . . .

25Other income (loss) items with differences (attach statement)

26Total income (loss) items. Combine lines 1 through 25

27Total expense/deduction items (from Part III, line 39)

28 Other items with no differences . . . . . . .

29a Mixed groups, see instructions. All others, combine lines 26 through 28 . . . . . . . . . . .

b PC insurance subgroup reconciliation totals . . .

c Life insurance subgroup reconciliation totals . . .

30Reconciliation totals. Combine lines 29a through 29c

Note: Line 30, column (a), must equal Part I, line 11, and column (d) must equal Form 1120, page 1, line 28.

Schedule

Schedule |

Page 3 |

Name of corporation (common parent, if consolidated return)

Employer identification number

Check applicable box(es): (1) |

Consolidated group |

(2) |

Parent corp |

(3) |

Consolidated eliminations |

(4) |

Subsidiary corp (5) |

Mixed 1120/L/PC group |

Check if a |

1120 group (7) |

1120 eliminations |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Name of subsidiary (if consolidated return) |

|

|

|

|

|

Employer identification number |

||

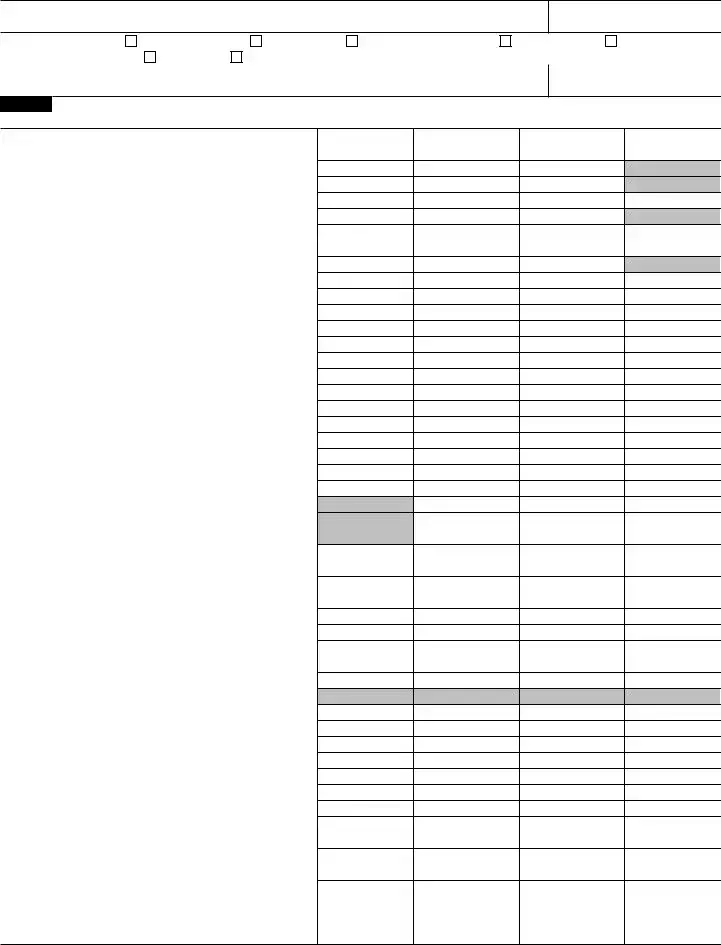

Part III Reconciliation of Net Income (Loss) per Income Statement of Includible Corporations With Taxable Income per

|

Expense/Deduction Items |

1 |

U.S. current income tax expense |

2 |

U.S. deferred income tax expense |

3 |

State and local current income tax expense . . . |

4State and local deferred income tax expense . . .

5Foreign current income tax expense (other than

foreign withholding taxes) . . . . . . . . .

6 |

Foreign deferred income tax expense |

7 |

Foreign withholding taxes |

8 |

Interest expense (see instructions) |

9 |

Stock option expense |

10 |

Other |

11 |

Meals and entertainment |

12 |

Fines and penalties |

13 |

Judgments, damages, awards, and similar costs . |

14 |

Parachute payments |

15Compensation with section 162(m) limitation . . .

16Pension and

17 |

Other |

18 |

Deferred compensation |

19Charitable contribution of cash and tangible property

20 |

Charitable contribution of intangible property |

. . |

21 |

Charitable contribution limitation/carryforward . . |

|

22Domestic production activities deduction (see

instructions) . . . . . . . . . . . . . .

23Current year acquisition or reorganization

investment banking fees . . . . . . . . .

24Current year acquisition or reorganization legal and

accounting fees . . . . . . . . . . . .

25Current year acquisition/reorganization other costs .

26 Amortization/impairment of goodwill |

. . . . . |

27Amortization of acquisition, reorganization, and

28 |

Other amortization or impairment |

29 |

Reserved |

30 |

Depletion |

31 |

Depreciation |

32 |

Bad debt expense |

33 |

Corporate owned life insurance premiums . . . |

34 |

Purchase versus lease (for purchasers and/or lessees) . |

35 |

Research and development costs |

36Section 118 exclusion (attach statement) . . . .

37Section

large financial institutions (see instructions) . . .

38Other expense/deduction items with differences

(attach statement) |

. . . . . . . . . . . |

39Total expense/deduction items. Combine lines 1 through 38. Enter here and on Part II, line 27, reporting positive amounts as negative and negative amounts as positive . . . . . . . .

(a)

Expense per

Income Statement

(b)

Temporary Difference

(c) Permanent Difference

(d)

Deduction per

Tax Return

Schedule

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule M-3 (Form 1120) is used by corporations to reconcile financial accounting income with taxable income. |

| Filing Requirement | Corporations with total assets of $10 million or more must file Schedule M-3, as mandated by the IRS. |

| Form Components | Schedule M-3 consists of three parts: the identification and financial data, reconciliation of income, and the balance sheet. |

| Tax Year | Schedule M-3 must be filed along with Form 1120 for the corporation's tax year ending date. |

| State-Specific Forms | Some states require their own equivalents of Schedule M-3, governed by local tax laws. |

| Penalties for Non-Compliance | Failing to file Schedule M-3 when required may result in penalties from the IRS. |

Filling out the IRS Schedule M-3 1120 form is a straightforward process that allows you to report your corporation's income, deductions, and adjustments. Completing this form correctly is essential to ensure compliance and avoid potential issues with the IRS. To get started, follow these detailed steps.

After completing the form, it's essential to keep a copy for your records. Accurate reporting makes tax season smoother and helps you avoid common pitfalls associated with corporate filings.

IRS Schedule M-3 is an attachment to Form 1120, which corporations use to report their financial activities. This specific schedule focuses on the differences between book income and taxable income. Corporations with total assets of $10 million or more must file this form to provide transparency regarding their accounting methods and any discrepancies between their financial statements and tax returns.

Any corporation that meets the following criteria must file Schedule M-3:

If a corporation does not meet these criteria, it can file Schedule M-1 instead, which is a simpler form for reconciling book income to taxable income.

When completing Schedule M-3, the following information is typically required:

It is essential to provide accurate and thorough documentation to avoid penalties and ensure compliance with IRS regulations.

Failure to file Schedule M-3 when required can lead to penalties. The IRS may impose monetary fines for non-compliance. Additionally, not filing can result in delays in processing the corporation’s tax return. In some cases, this could attract further scrutiny from the IRS. It is crucial for corporations to adhere to their filing obligations to maintain good standing and avoid unnecessary complications.

Filling out the IRS Schedule M-3 for Form 1120 can be a daunting task. Many taxpayers and corporations encounter pitfalls that can lead to mistakes. Understanding these common errors can help ensure proper compliance and avoid potential penalties.

One significant mistake is providing inaccurate financial information. This can occur when the amounts reported on Schedule M-3 do not align with the data on the corporate tax return. Discrepancies can raise red flags with the IRS and may prompt further examination or audits. Always double-check figures to ensure consistency across all documents.

Another frequent error is misclassifying items. Certain income or expenses must be categorized correctly to comply with tax regulations. For instance, distinguishing between permanent and temporary differences can be particularly tricky. Misclassification can distort the true financial picture of the corporation and lead to inflated or deflated tax obligations.

Some individuals overlook the importance of adequate documentation. Supporting records for adjustments and reconciliations are crucial. When these documents are missing or incomplete, it becomes challenging to substantiate claims made on Schedule M-3. Keep comprehensive files to justify entries in case of an IRS inquiry.

Moreover, failing to report all required adjustments is a common oversight. Schedule M-3 requires a detailed analysis of book-to-tax differences. Omitting any necessary adjustments can lead to incorrect tax calculations. Be thorough and ensure that all required changes are reflected accurately.

Finally, many taxpayers underestimate the complexity of the form and fail to seek help when needed. The Schedule M-3 has multiple layers of detail that can be easily misunderstood. Consulting a tax professional can help catch errors before they become expensive troubles. Don’t hesitate to reach out for guidance, especially if the form seems overwhelming.

The IRS Schedule M-3 is an important form that corporations use to report their income, deductions, and other tax information. However, it is often accompanied by additional forms and documents that provide more context and details about the corporation's financial situation. Understanding these supplementary documents can help ensure compliance and accuracy in tax reporting.

By being aware of these accompanying documents, corporations can enhance their tax reporting process. Proper preparation and understanding of each form contribute to a well-rounded tax strategy and compliance with IRS guidelines. This knowledge ultimately assists in fostering a positive relationship with the tax authorities.

When filling out the IRS Schedule M-3 (Form 1120), it’s essential to approach this task carefully. Here’s a list of things to do and avoid to help ensure accuracy and compliance.

Here are ten common misconceptions about the IRS Schedule M-3 (Form 1120) and explanations for each:

It is only for large corporations. Many believe that only large corporations need to file Schedule M-3; however, it is required for certain entities with total assets exceeding $10 million, regardless of their size.

Schedule M-3 is the same as Schedule M-1. Some assume that Schedule M-3 and M-1 serve the same purpose. In reality, Schedule M-3 provides more detailed financial information and is used for larger corporations, while M-1 is simpler and for smaller businesses.

Filing Schedule M-3 is optional. A misconception exists that filing Schedule M-3 is optional for qualifying corporations. In fact, it is mandatory for those with total assets over $10 million.

It covers all tax issues of a corporation. Many think that Schedule M-3 addresses every tax matter for a corporation. However, it focuses primarily on reconciling book income to tax income, not on every tax aspect.

Only tax accountants can fill it out. Some individuals believe only professional accountants can prepare Schedule M-3. In truth, any person who understands the corporation's financial statements can fill it out, though professional help is often beneficial.

It can be ignored if inaccurate information is provided. There is a belief that if errors are made on Schedule M-3, they can be overlooked. Incorrect information can lead to penalties and audits, making accuracy crucial.

Filing late has no consequences. Some think that filing Schedule M-3 late will not result in repercussions. However, late filings may incur penalties and interest, affecting the corporation's financial situation.

It is unnecessary if a corporation has no changes in income. There is a misconception that if a corporation has consistent income, Schedule M-3 isn't needed. This form must still be filed regardless of income changes if total assets exceed the threshold.

Information from previous years can be reused without updates. Some believe they can simply copy information from previous years. Updates and current year figures are necessary for an accurate filing.

Schedule M-3 filing is straightforward. While it may seem simple, many find the process complex and challenging, especially when accounting for various adjustments and reconciliations.

The IRS Schedule M-3 (Form 1120) is specifically designed for corporations that may have a need to reconcile their financial statements with their tax returns. Here are some key takeaways to consider when filling out and using the form:

By keeping these points in mind, individuals and businesses can navigate the complexities of the Schedule M-3 effectively. Proper preparation will contribute to a smoother tax filing process.