In the realm of financial agreements, the Kansas Promissory Note form serves as a crucial document for individuals and businesses alike. This form outlines a borrower's promise to repay a specified amount of money to a lender, establishing clear terms for repayment. Key elements of the form include the principal amount, interest rate, repayment schedule, and any late fees that may apply. Additionally, it addresses the rights and responsibilities of both parties, ensuring transparency and mutual understanding. The Kansas Promissory Note can be tailored to meet specific needs, whether for personal loans, business financing, or real estate transactions. By using this form, parties can avoid misunderstandings and provide a solid foundation for their financial relationship.

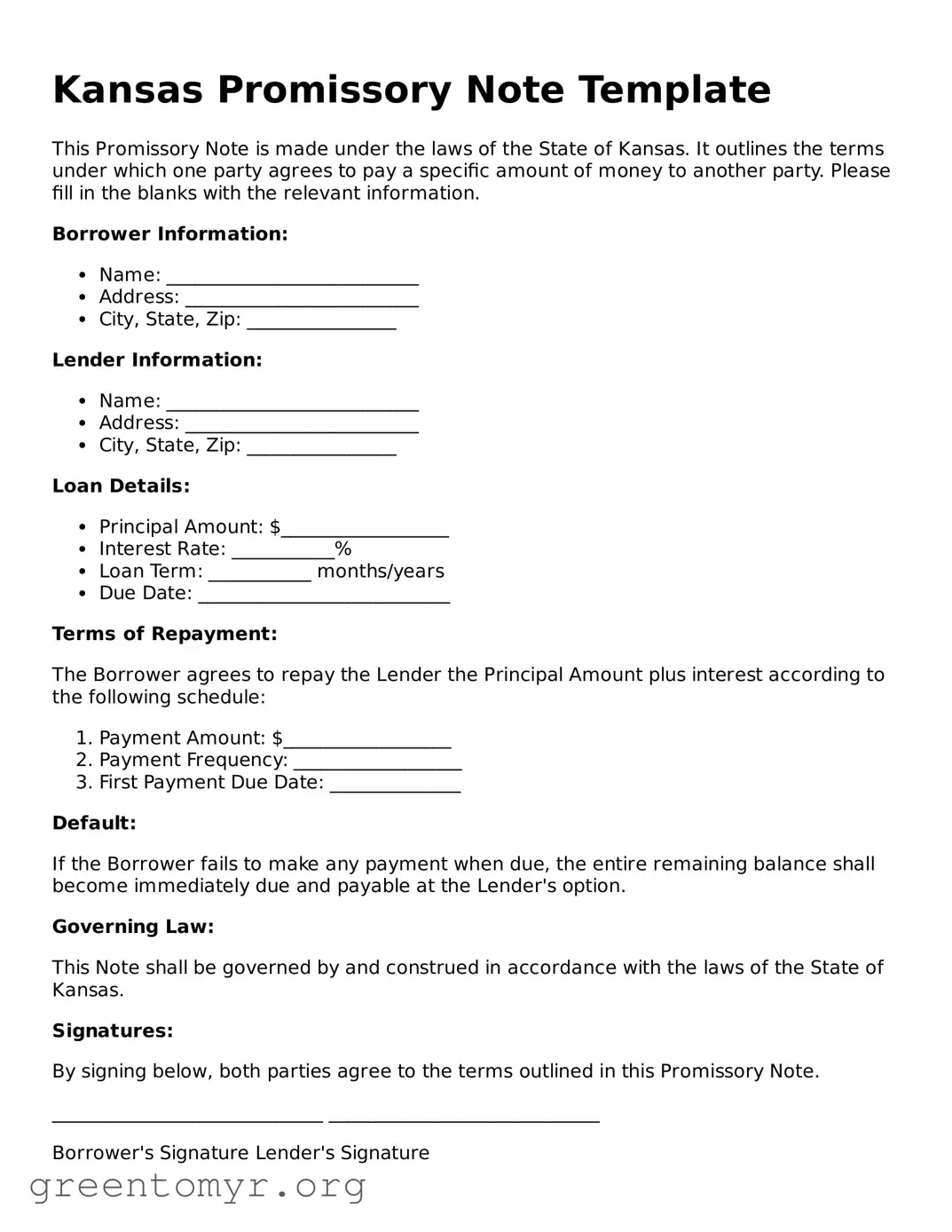

Kansas Promissory Note Template

This Promissory Note is made under the laws of the State of Kansas. It outlines the terms under which one party agrees to pay a specific amount of money to another party. Please fill in the blanks with the relevant information.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

The Borrower agrees to repay the Lender the Principal Amount plus interest according to the following schedule:

Default:

If the Borrower fails to make any payment when due, the entire remaining balance shall become immediately due and payable at the Lender's option.

Governing Law:

This Note shall be governed by and construed in accordance with the laws of the State of Kansas.

Signatures:

By signing below, both parties agree to the terms outlined in this Promissory Note.

_____________________________ _____________________________

Borrower's Signature Lender's Signature

Date: _________________________ Date: ______________________

| Fact Name | Details |

|---|---|

| Definition | A promissory note in Kansas is a written promise to pay a specified amount of money to a designated person or entity at a future date or on demand. |

| Governing Law | The Kansas Uniform Commercial Code (UCC) governs promissory notes, specifically under Article 3, which deals with negotiable instruments. |

| Requirements | The note must include essential elements such as the amount owed, the due date, the interest rate (if applicable), and the signatures of the parties involved. |

| Enforceability | To be enforceable, the promissory note must be clear and unambiguous. Any alterations or missing information can affect its validity. |

Once you have the Kansas Promissory Note form ready, you will need to fill it out accurately to ensure that all necessary details are captured. This document will serve as a written promise to pay a specified amount, and it is essential to complete it carefully to avoid any future disputes.

A Kansas Promissory Note is a legal document that outlines a borrower's promise to repay a specified amount of money to a lender at a defined time. This document includes details such as the loan amount, interest rate, payment schedule, and consequences for default. It serves as a formal agreement between the two parties involved in the transaction.

A typical Kansas Promissory Note includes several essential elements:

While it is not legally required to have a lawyer review your Promissory Note, it is highly advisable. A legal professional can ensure that the document complies with Kansas law and adequately protects your interests. They can also help clarify any terms that may be confusing, reducing the risk of disputes in the future.

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. Any modifications should be documented in writing and signed by both the borrower and the lender. This ensures that there is a clear record of the new terms, which can help prevent misunderstandings down the line.

If the borrower defaults, the lender has several options. They may choose to pursue repayment through legal action, which could include filing a lawsuit to recover the owed amount. The lender may also have the right to charge late fees or take possession of any collateral if it was included in the agreement. It’s crucial for both parties to understand the default terms outlined in the Promissory Note to avoid complications.

Filling out a Kansas Promissory Note form can seem straightforward, but many people make mistakes that can lead to complications later. One common error is failing to include all required information. The form typically asks for specific details about the borrower, lender, loan amount, and repayment terms. Omitting even one piece of information can render the note incomplete.

Another frequent mistake is not clearly stating the loan amount. If the amount is ambiguous or improperly written, it may lead to misunderstandings. Always ensure that the loan amount is clearly indicated in both numbers and words. This clarity helps prevent disputes about how much is owed.

Some individuals neglect to specify the interest rate. If the note is meant to carry interest, it is essential to state the rate explicitly. Without this information, the borrower may not understand their financial obligations, which could result in confusion or conflict.

Additionally, people sometimes forget to include the repayment schedule. A well-defined schedule outlines when payments are due and how much is to be paid. Without this, both parties may have different expectations, leading to potential issues in the future.

Another mistake involves not signing the document correctly. Both the borrower and lender must sign the promissory note for it to be valid. If one party fails to sign, the note may not hold up in a legal context, making it crucial to double-check that all signatures are present.

Lastly, many overlook the importance of keeping a copy of the signed note. After filling out the form, it is essential for both parties to retain a copy for their records. This document serves as proof of the agreement and can be vital if any disputes arise later.

When preparing a Kansas Promissory Note, several other documents may be necessary to ensure a comprehensive understanding of the agreement between the parties involved. Each document serves a specific purpose, helping to clarify the terms of the loan and protect the interests of both the lender and the borrower.

These documents work together to create a clear and enforceable agreement. Properly preparing and understanding each of these forms can help prevent misunderstandings and disputes in the future.

A Promissory Note is a financial document that outlines a promise to pay a specific amount of money to a designated person or entity. Several other documents share similarities with a Promissory Note. Here are nine of them:

When filling out the Kansas Promissory Note form, it’s important to follow certain guidelines to ensure accuracy and compliance. Here are ten things to keep in mind:

When it comes to the Kansas Promissory Note form, there are several misconceptions that can lead to confusion. Understanding these can help ensure that individuals use the form correctly and effectively.

While both documents are related to borrowing money, they serve different purposes. A Promissory Note is a written promise to pay back a specific amount, while a loan agreement outlines the terms and conditions of the loan, including interest rates and repayment schedules.

In Kansas, notarization is not a requirement for a Promissory Note to be legally binding. However, having it notarized can provide additional proof of authenticity and can be helpful in case of disputes.

This is not true. A Promissory Note can be used for any amount of money, whether it’s a small personal loan between friends or a larger transaction. The key is to clearly outline the terms of repayment.

Although a Promissory Note is a binding agreement, parties can mutually agree to modify the terms. Any changes should be documented in writing and signed by both parties to avoid misunderstandings.

When filling out and using the Kansas Promissory Note form, keep these key points in mind:

Following these steps will help ensure that the promissory note is completed correctly and serves its intended purpose. Always consult a legal professional if you have specific questions or concerns.