The Loan Estimate form is a crucial document for anyone considering a mortgage. It provides a clear overview of the loan terms, including the loan amount, interest rate, and monthly payments. Applicants can find essential information about the loan type, which may include conventional, FHA, or VA options. The form also outlines the estimated closing costs and cash to close, helping borrowers understand the financial obligations involved in securing a loan. Additionally, it details the projected payments over the loan's duration, including principal, interest, and any applicable insurance or taxes. Important features, such as prepayment penalties and balloon payments, are also highlighted, ensuring that borrowers are fully informed. By comparing the Loan Estimate with the Closing Disclosure, applicants can track any changes that may occur before finalizing their mortgage. This document serves as a vital tool for making informed decisions in the home-buying process.

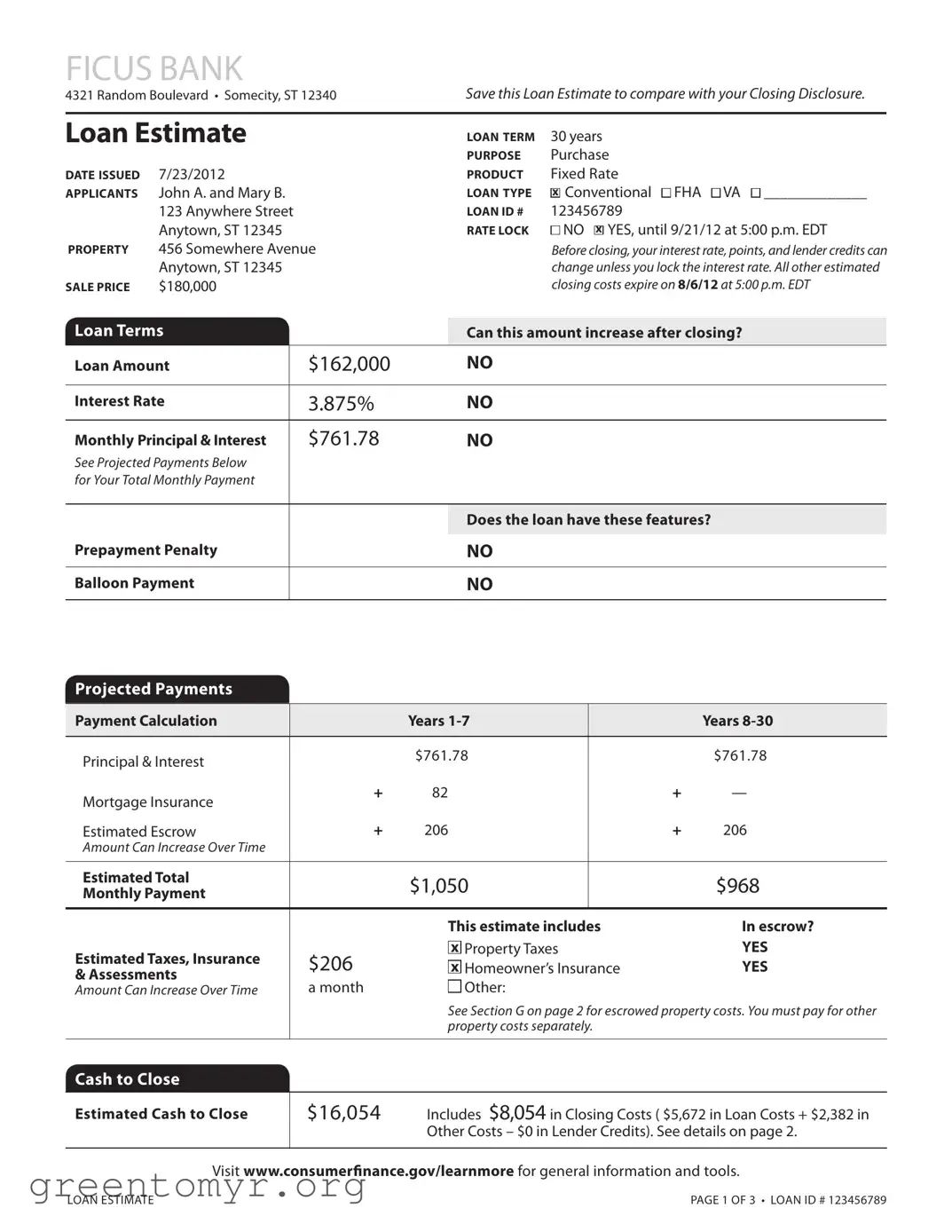

FICUS BANK

4321 Random Boulevard • Somecity, ST 12340Save this Loan Estimate to compare with your Closing Disclosure.

Loan estimate |

LOAN TeRM |

30 years |

|

|

|

PuRPOse |

Purchase |

DATe IssueD |

7/23/2012 |

PRODuCT |

Fixed Rate |

APPLICANTs |

John A. and Mary B. |

LOAN TyPe |

x Conventional FHA VA _____________ |

|

123 Anywhere Street |

LOAN ID # |

123456789 |

|

Anytown, ST 12345 |

RATe LOCK |

NO x YES, until 9/21/12 at 5:00 p.m. EDT |

PROPeRTy |

456 Somewhere Avenue |

|

Before closing, your interest rate, points, and lender credits can |

|

Anytown, ST 12345 |

|

change unless you lock the interest rate. All other estimated |

sALe PRICe |

$180,000 |

|

closing costs expire on 8/6/12 at 5:00 p.m. EDT |

Loan Terms |

|

Can this amount increase after closing? |

Loan Amount |

$162,000 |

NO |

|

|

|

Interest Rate |

3.875% |

NO |

|

|

|

Monthly Principal & Interest |

$761.78 |

NO |

See Projected Payments Below |

|

|

for Your Total Monthly Payment |

|

|

|

|

|

|

|

Does the loan have these features? |

Prepayment Penalty |

|

|

|

NO |

|

|

|

|

Balloon Payment |

|

NO |

|

|

|

Projected Payments

Payment Calculation |

|

years |

|

|

years |

|

|

|

|

|

|

Principal & Interest |

|

$761.78 |

|

|

$761.78 |

|

|

|

|

|

|

Mortgage Insurance |

+ |

82 |

|

+ |

— |

|

|

|

|

|

|

Estimated Escrow |

+ |

206 |

|

+ |

206 |

Amount Can Increase Over Time |

|

|

|

|

|

|

|

|

|

|

|

estimated Total |

|

$1,050 |

|

|

$968 |

Monthly Payment |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This estimate includes |

|

In escrow? |

|

estimated Taxes, Insurance |

$206 |

x Property Taxes |

|

yes |

|

x Homeowner’s Insurance |

|

yes |

|||

& Assessments |

|

||||

a month |

Other: |

|

|

||

Amount Can Increase Over Time |

|

|

|||

|

|

See Section G on page 2 for escrowed property costs. You must pay for other |

|||

|

|

property costs separately. |

|

|

|

|

|

|

|

|

|

Cash to Close |

|

|

|

|

|

|

|

|

|

||

estimated Cash to Close |

$16,054 |

Includes $8,054 in Closing Costs ( $5,672 in Loan Costs + $2,382 in |

|||

|

|

Other Costs – $0 in Lender Credits). See details on page 2. |

|||

|

|

|

|

|

|

Visit www.consumerinance.gov/learnmore for general information and tools.

LOAN ESTIMATE |

page 1 of 3 • Loan ID # 123456789 |

Closing Cost Details

Loan Costs

A. Origination Charges |

$1,802 |

.25 % of Loan Amount (Points) |

$405 |

Application Fee |

$300 |

Underwriting Fee |

$1,097 |

Other Costs

e. Taxes and Other Government Fees |

$85 |

||||||

Recording Fees and Other Taxes |

|

|

$85 |

||||

Transfer Taxes |

|

|

$0 |

||||

|

|

|

|

|

|

|

|

F. Prepaids |

|

|

$867 |

||||

Homeowner’s Insurance Premium ( |

6 months) |

$605 |

|||||

|

|

|

|

|

|

|

|

Mortgage Insurance Premium ( 0 |

months) |

$0 |

|||||

|

|

|

|

|

|

||

Prepaid Interest ( $17.44 per day for 15 days @ 3.875%) |

$262 |

||||||

Property Taxes ( 0 months) |

|

|

$0 |

||||

|

|

|

|

|

|

|

|

B. services you Cannot shop For |

$672 |

Appraisal Fee |

$405 |

Credit Report Fee |

$30 |

Flood Determination Fee |

$20 |

Flood Monitoring Fee |

$32 |

Tax Monitoring Fee |

$75 |

Tax Status Research Fee |

$110 |

G. Initial escrow Payment at Closing |

|

|

$413 |

|

Homeowner’s Insurance |

$100.83 per month for |

23mo. $202 |

||

Mortgage Insurance |

per month for |

0 |

mo. |

|

Property Taxes |

$105.30 per month for |

2 |

mo. |

$211 |

H. Other |

$1,017 |

Title – Owner’s Title Policy (optional) |

$1,017 |

C. services you Can shop For |

$3,198 |

Pest Inspection Fee |

$135 |

Survey Fee |

$65 |

Title – Insurance Binder |

$700 |

Title – Lender’s Title Policy |

$535 |

Title – Title Search |

$1,261 |

Title – Settlement Agent Fee |

$502 |

D. TOTAL LOAN COsTs (A + B + C) |

$5,672 |

I. TOTAL OTHeR COsTs (e + F + G + H) |

$2,382 |

|

|

J. TOTAL CLOsING COsTs |

$8,054 |

|

|

D + I |

$8,054 |

Lender Credits |

$0 |

Calculating Cash to Close |

|

|

|

Total Closing Costs (J) |

$8,054 |

Closing Costs Financed (Included in Loan Amount) |

$0 |

Down Payment/Funds from Borrower |

$18,000 |

Deposit |

– $10,000 |

Funds for Borrower |

$0 |

Seller Credits |

$0 |

Adjustments and Other Credits |

$0 |

estimated Cash to Close |

$16,054 |

|

|

LOAN ESTIMATE |

page 2 of 3 • Loan ID # 123456789 |

Additional Information About This Loan

LeNDeR NMLs/LICeNse ID

LOAN OFFICeR

NMLs ID

PHONe

Ficus Bank

Joe Smith 12345 [email protected]

MORTGAGe BROKeR NMLs/LICeNse ID LOAN OFFICeR NMLs ID

eMAIL PHONe

Comparisons |

use these measures to compare this loan with other loans. |

||

|

|

|

|

In 5 years |

$56,582 |

Total you will have paid in principal, interest, mortgage insurance, and loan costs. |

|

$15,773 |

Principal you will have paid of. |

||

|

|||

|

|

|

|

Annual Percentage Rate (APR) |

4.494% |

Your costs over the loan term expressed as a rate. This is not your interest rate. |

|

|

|

|

|

Total Interest Percentage (TIP) |

69.447% |

The total amount of interest that you will pay over the loan term as a |

|

|

|

percentage of your loan amount. |

|

|

|

|

|

Other Considerations

Appraisal |

We may order an appraisal to determine the property’s value and charge you for this |

|

appraisal. We will promptly give you a copy of any appraisal, even if your loan does not close. |

|

You can pay for an additional appraisal for your own use at your own cost. |

Assumption |

If you sell or transfer this property to another person, we |

|

will allow, under certain conditions, this person to assume this loan on the original terms. |

|

x will not allow this person to assume this loan on the original terms. |

Homeowner’s |

This loan requires homeowner’s insurance on the property, which you may obtain from a |

Insurance |

company of your choice that we ind acceptable. |

Late Payment |

If your payment is more than 15 days late, we will charge a late fee of 5% of the monthly |

|

principal and interest payment. |

Reinance |

Reinancing this loan will depend on your future inancial situation, the property value, and |

|

market conditions. You may not be able to reinance this loan. |

servicing |

We intend |

|

to service your loan. If so, you will make your payments to us. |

|

x to transfer servicing of your loan. |

Conirm Receipt

By signing, you are only conirming that you have received this form. You do not have to accept this loan because you have signed or received this form.

Applicant Signature |

Date |

Date |

LOAN ESTIMATE |

page 3 of 3 • Loan ID #123456789 |

| Fact Name | Description |

|---|---|

| Purpose | The Loan Estimate form provides a standardized summary of the key loan terms and estimated closing costs for borrowers. |

| Loan Term | The typical loan term for the example provided is 30 years, which is common for fixed-rate mortgages. |

| Interest Rate | The interest rate listed is 3.875%, which impacts the monthly payment amount. |

| Loan Amount | The example shows a loan amount of $162,000, which is the amount borrowed by the applicants. |

| Projected Payments | Monthly payments for principal and interest are estimated at $761.78 for the first 30 years. |

| Cash to Close | The estimated cash to close is $16,054, which includes various closing costs. |

| Closing Costs | Total closing costs are estimated at $8,054, which includes loan costs and other fees. |

| APR | The Annual Percentage Rate (APR) is 4.494%, reflecting the total cost of borrowing over the loan term. |

| Assumption | The loan may not allow for assumption by a new buyer under the original terms, depending on conditions. |

| Late Payment Fee | A late payment fee of 5% will be charged if the payment is more than 15 days late. |

Filling out the Loan Estimate form is a crucial step in understanding the financial aspects of a mortgage. This document provides detailed information about the loan terms, costs, and other essential factors that will influence your borrowing decision. After completing the form, you will have a clearer picture of your potential mortgage, which can help you compare different loan offers.

A Loan Estimate form is a document that lenders provide to borrowers within three business days of receiving a loan application. It outlines the key details of the loan, including the estimated interest rate, monthly payments, and closing costs. This form helps borrowers understand the terms of their mortgage and compare different loan offers.

The Loan Estimate is crucial because it provides transparency regarding the costs associated with a mortgage. It allows borrowers to make informed decisions by comparing offers from different lenders. By reviewing the Loan Estimate, borrowers can identify potential fees and understand the total cost of the loan over its term.

The Loan Estimate is valid for ten business days after it is issued. During this period, borrowers can use the information to compare loan offers. After ten days, the estimates may change, especially if interest rates fluctuate or if the borrower’s financial situation changes.

The Loan Estimate includes several key pieces of information:

Yes, the terms in the Loan Estimate can change before closing. However, if the borrower locks in the interest rate, the rate and points will remain fixed. Other costs may still fluctuate based on final assessments and other factors.

If discrepancies are found in the Loan Estimate, borrowers should contact their lender immediately. It’s important to clarify any unclear charges or terms. The lender is obligated to provide explanations and ensure that borrowers fully understand their loan terms.

If a borrower decides not to proceed with the loan after receiving the Loan Estimate, there are no penalties. The form serves merely as a disclosure of loan terms. Borrowers are not obligated to accept the loan simply because they received the Loan Estimate.

To effectively compare different lenders, borrowers should look at the following:

By analyzing these factors, borrowers can make a more informed decision about which loan offer best suits their financial needs.

Filling out the Loan Estimate form can be daunting. Many people make common mistakes that can lead to confusion later on. One frequent error is not reading the entire document. This form contains crucial information about your loan, including interest rates and costs. Skimming through it might cause you to miss important details that could affect your decision.

Another mistake is overlooking the interest rate lock. If you don’t check whether your rate is locked, you could face unexpected changes in your interest rate before closing. It’s essential to clarify this point to avoid surprises that could increase your monthly payments.

Some individuals fail to compare estimated closing costs with other offers. Each lender may provide different estimates. By not comparing these costs, you might miss out on a better deal that could save you money in the long run.

Additionally, people sometimes neglect to check the loan terms thoroughly. Understanding whether there are prepayment penalties or balloon payments is vital. These features can significantly impact your financial situation, so it’s important to be aware of them upfront.

Another common oversight is not considering additional costs that may arise. For example, property taxes and homeowner’s insurance are often included in the estimated monthly payment, but they can change. Being aware of these costs can help you budget more effectively.

Lastly, many applicants forget to sign and date the form properly. This step is crucial as it confirms that you have received the Loan Estimate. Without a signature, your application may face delays. Always double-check that you’ve completed every part of the form before submitting it.

The Loan Estimate form is an important document that helps borrowers understand the costs associated with their mortgage. Along with this form, there are several other documents that are commonly used in the loan process. Each of these documents provides essential information that can aid in making informed decisions about the loan.

Understanding these documents is crucial for borrowers as they navigate the mortgage process. Each one plays a role in ensuring transparency and clarity, helping individuals make the best choices for their financial future.

When filling out the Loan Estimate form, it is essential to approach the process with care and attention. Below are five recommendations on what to do and what to avoid.

Many people believe that the Loan Estimate is a binding contract. In reality, it is simply an estimate of the costs and terms associated with the loan. You are not obligated to proceed with the loan just because you received this document.

Some individuals assume that the costs presented in the Loan Estimate are set in stone. However, these costs can change before closing, especially if you do not lock in your interest rate. It’s important to stay informed about any potential changes.

People often think that the Loan Estimate covers every possible fee associated with the loan. While it provides a comprehensive overview, some costs, such as certain closing costs or fees related to specific services, may not be included. Always ask for clarification if you have questions.

Many borrowers equate a lower interest rate with a better loan. However, it’s essential to consider other factors, such as fees and loan terms. A loan with a slightly higher interest rate but lower fees may be more cost-effective in the long run.

When filling out and using the Loan Estimate form, several key points should be noted to ensure a clear understanding of the loan terms and conditions. Here are eight essential takeaways: