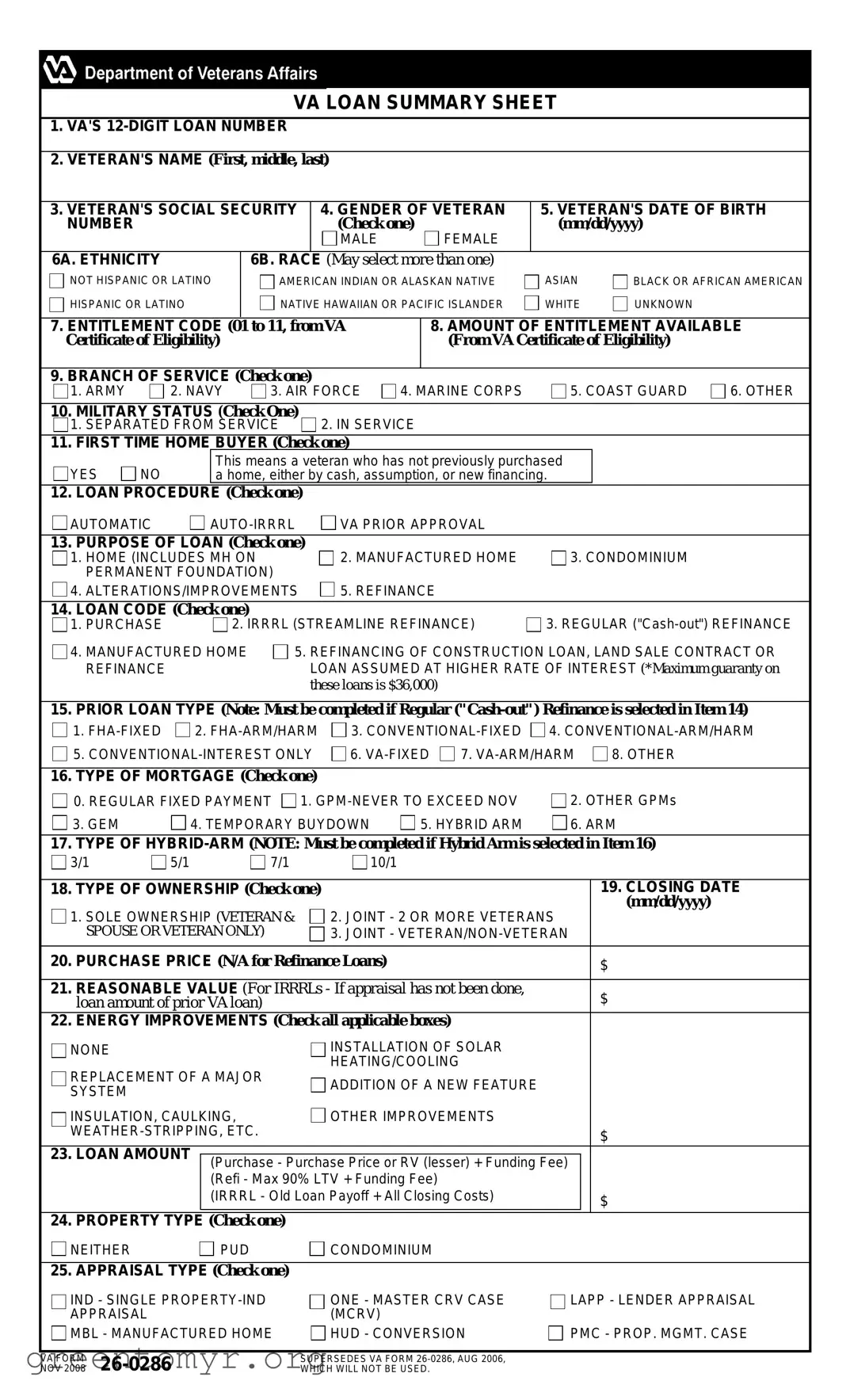

The Loan Summary Sheet is an essential document for veterans seeking to utilize their benefits for home financing. This form collects vital information that helps streamline the loan application process, ensuring that veterans receive the assistance they need in a timely manner. It includes the veteran's personal details, such as their name, social security number, and date of birth, as well as demographic information like gender and ethnicity. Additionally, the form captures the veteran's military service details, including branch of service and current military status. The Loan Summary Sheet also outlines the specifics of the loan being requested, including the type of mortgage, purpose of the loan, and the amount of entitlement available. Furthermore, it provides a section for financial details, such as credit score, income, and debt-to-income ratio, which are critical in assessing the veteran's eligibility for the loan. By consolidating all these elements, the Loan Summary Sheet serves as a comprehensive overview that facilitates the approval process and helps veterans navigate their home buying journey with confidence.

VA LOAN SUMMARY SHEET

1.VA'S

2.VETERAN'S NAME (First, middle, last)

|

|

|

|

|

|

||||

3. VETERAN'S SOCIAL SECURITY |

|

4. GENDER OF VETERAN |

5. VETERAN'S DATE OF BIRTH |

||||||

NUMBER |

|

|

|

(Check one) |

(mm/dd/yyyy) |

|

|||

|

|

|

|

MALE |

|

FEMALE |

|

|

|

6A. ETHNICITY |

|

6B. RACE (May select more than one) |

|

|

|

||||

NOT HISPANIC OR LATINO |

AMERICAN INDIAN OR ALASKAN NATIVE |

ASIAN |

BLACK OR AFRICAN AMERICAN |

||||||

HISPANIC OR LATINO |

NATIVE HAWAIIAN OR PACIFIC ISLANDER |

WHITE |

UNKNOWN |

|

|||||

|

|

|

|

|

|||||

7. ENTITLEMENT CODE (01 to 11, from VA |

|

8. AMOUNT OF ENTITLEMENT AVAILABLE |

|||||||

Certificate of Eligibility) |

|

|

|

|

(From VA Certificate of Eligibility) |

|

|||

|

|

|

|

|

|

|

|

||

9. BRANCH OF SERVICE (Check one) |

|

4. MARINE CORPS |

5. COAST GUARD |

6. OTHER |

|||||

1. ARMY |

2. NAVY |

3. AIR FORCE |

|||||||

10. MILITARY STATUS (Check One) |

2. IN SERVICE |

|

|

|

|||||

1. SEPARATED FROM SERVICE |

|

|

|

||||||

11. FIRST TIME HOME BUYER (Check one)

YES |

NO |

This means a veteran who has not previously purchased |

|

|

|

a home, either by cash, assumption, or new financing. |

|

|

|||

|

|

|

|

|

|

12. LOAN PROCEDURE |

(Check one) |

|

|

|

|

AUTOMATIC |

VA PRIOR APPROVAL |

|

|

||

13. PURPOSE OF LOAN (Check one) |

2. MANUFACTURED HOME |

3. CONDOMINIUM |

|||

1. HOME (INCLUDES MH ON |

|||||

PERMANENT FOUNDATION) |

|

|

|

||

4. ALTERATIONS/IMPROVEMENTS |

5. REFINANCE |

|

|

||

14.LOAN CODE (Check one)

1. PURCHASE |

2. IRRRL (STREAMLINE REFINANCE) |

3. REGULAR |

|

4. MANUFACTURED HOME |

5. REFINANCING OF CONSTRUCTION LOAN, LAND SALE CONTRACT OR |

||

REFINANCE |

|

LOAN ASSUMED AT HIGHER RATE OF INTEREST (*Maximum guaranty on |

|

|

|

these loans is $36,000) |

|

15.PRIOR LOAN TYPE (Note: Must be completed if Regular

1.

5. |

6. |

8. OTHER |

|||

|

|

|

|

|

|

16. TYPE OF MORTGAGE (Check one) |

|

|

|

|

|

0. REGULAR FIXED PAYMENT 1. |

2. OTHER GPMs |

||||

3. GEM |

4. TEMPORARY BUYDOWN |

5. HYBRID ARM |

6. ARM |

||

17.TYPE OF

3/1 |

5/1 |

7/1 |

10/1 |

|

|

|

18. TYPE OF OWNERSHIP (Check one) |

|

19. CLOSING DATE |

1. SOLE OWNERSHIP (VETERAN & |

2. JOINT - 2 OR MORE VETERANS |

(mm/dd/yyyy) |

|

||

SPOUSE OR VETERAN ONLY) |

3. JOINT - |

|

|

|

|

20. PURCHASE PRICE (N/A for Refinance Loans) |

$ |

|

|

|

|

21. REASONABLE VALUE (For IRRRLs - If appraisal has not been done, |

$ |

|

loan amount of prior VA loan) |

|

|

22.ENERGY IMPROVEMENTS (Check all applicable boxes)

NONE |

|

INSTALLATION OF SOLAR |

|

REPLACEMENT OF A MAJOR |

HEATING/COOLING |

|

|

ADDITION OF A NEW FEATURE |

|

||

SYSTEM |

|

|

|

|

|

|

|

INSULATION, CAULKING, |

OTHER IMPROVEMENTS |

|

|

|

$ |

||

23. LOAN AMOUNT |

|

|

|

(Purchase - Purchase Price or RV (lesser) + Funding Fee) |

|

||

|

|

||

|

(Refi - Max 90% LTV + Funding Fee) |

|

|

|

(IRRRL - Old Loan Payoff + All Closing Costs) |

$ |

|

|

|

|

|

24. PROPERTY TYPE |

(Check one) |

|

|

NEITHER |

PUD |

CONDOMINIUM |

|

25. APPRAISAL TYPE (Check one)

IND - SINGLE

MBL - MANUFACTURED HOME

ONE - MASTER CRV CASE |

LAPP - LENDER APPRAISAL |

(MCRV) |

|

HUD - CONVERSION |

PMC - PROP. MGMT. CASE |

NOV 2008 |

WHICH WILL NOT BE USED. |

VA FORM |

SUPERSEDES VA FORM |

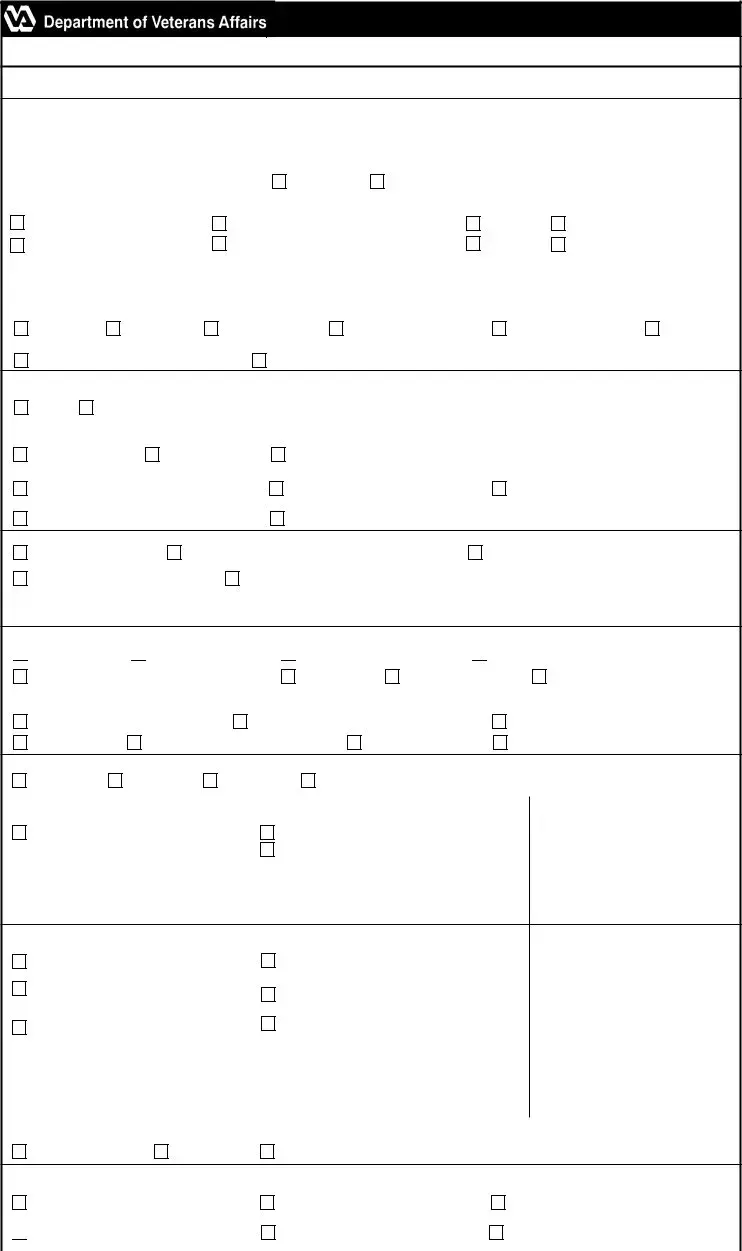

26. TYPE OF STRUCTURE (Check one)

1. CONVENTIONAL |

2. SINGLEWIDE M/H |

3. DOUBLEWIDE M/H |

CONSTRUCTION |

|

|

4. M/H LOT ONLY |

5. PREFABRICATED HOME |

6. CONDOMINIUM CONVERSION |

27. PROPERTY DESIGNATION (Check one)

1. EXISTING OR USED HOME, CONDO, M/H |

2. APPRAISED AS PROPOSED CONSTRUCTION |

|||

3. NEW EXISTING - NEVER OCCUPIED |

4. ENERGY IMPROVEMENTS |

|||

|

|

|

|

|

28. NO. OF UNITS (Check one) |

|

|

29. MCRV NO. |

|

SINGLE |

TWO UNITS |

THREE UNITS |

FOUR OR MORE |

|

|

|

|||

30. MANUFACTURED HOME CATEGORY(Check one) |

||||

0. OTHER - NOT M/H |

|

1. M/H ONLY (RENTED SPACE) |

||

2. M/H ONLY |

|

7. M/H ON PERMANENT FOUNDATION |

||

31. PROPERTY ADDRESS |

|

|

|

32. CITY |

33. STATE |

34. ZIP CODE |

35. COUNTY |

36. LENDER VA ID NUMBER |

37. AGENT VA ID NUMBER (If applicable) |

38. LENDER LOAN NUMBER |

|

FOR LAPP CASES ONLY

|

|

|

39. LENDER SAR ID NUMBER |

|

|

|

|

|

40. GROSS LIVING AREA |

41. AGE OF PROPERTY (Yrs.) |

42. DATE SAR ISSUED NOTIFICATION |

(Square Feet) |

|

OF VALUE (mm/dd/yyyy) |

|

|

|

43. TOTAL ROOM COUNT |

44. BATHS (No.) |

45. BEDROOMS (No.) |

46.IF PROCESSED UNDER LAPP, WAS THE FEE APPRAISER'S ORIGINAL VALUE ESTIMATE CHANGED OR REPAIR RECOMMENDATIONS REVISED, OR DID THE SAR OTHERWISE MAKE SIGNIFICANT ADJUSTMENTS?

YES (If "Yes," there must be written justification by fee appraiser and/or SAR) |

NO |

|

||||

|

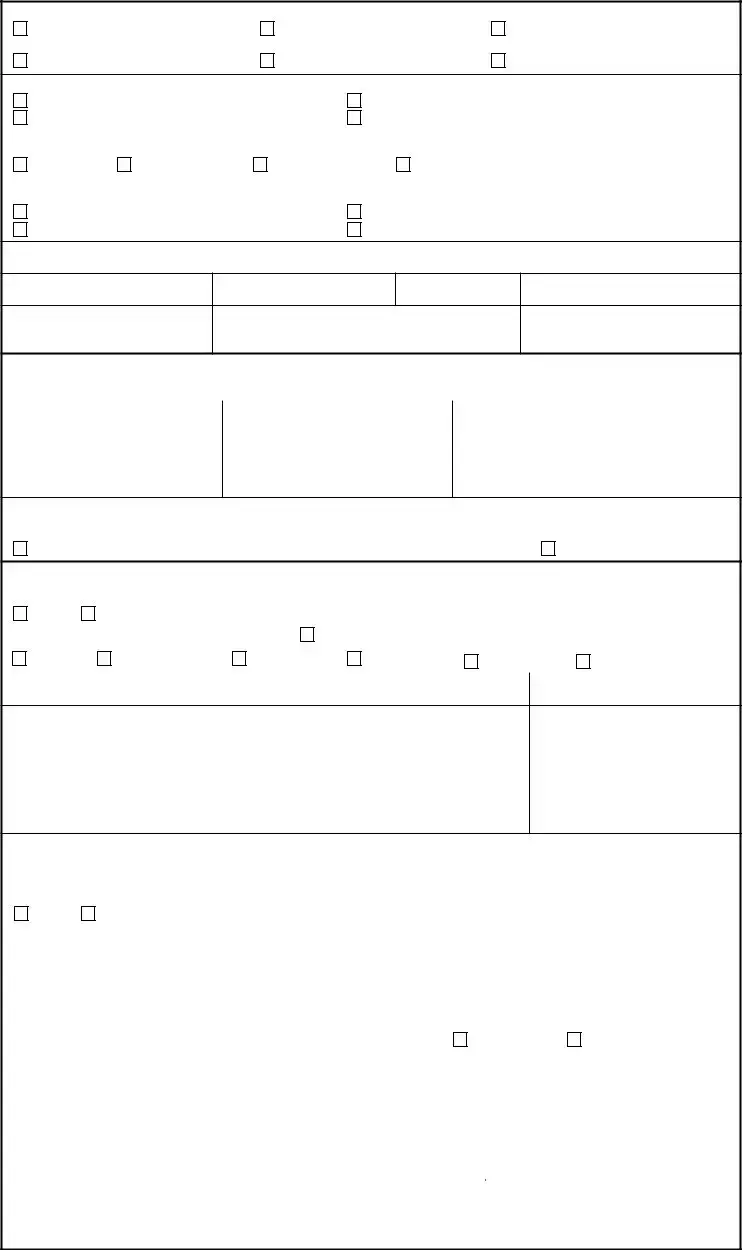

INCOME INFORMATION (Not Applicable for IRRRLs) |

|

||||

47A. LOAN PROCESSED UNDER VA RECOGNIZED AUTOMATED UNDERWRITING SYSTEM |

||||||

YES |

NO (If "Yes," Complete Item 47B and 47C) |

|

|

|||

47B. WHICH SYSTEM WAS USED? |

01. LP |

|

47C. RISK CLASSIFICATION |

|||

02. DU |

03. PMI AURA |

04. CLUES |

05. ZIPPY |

|

1. APPROVE |

2. REFER |

|

|

|

|

|

|

|

48.CREDIT SCORE (Enter the median credit score for the veteran only)

49. LIQUID ASSETS |

|

$ |

|

|

|

|

|

|

50. TOTAL MONTHLY GROSS INCOME |

(Item 31+Item 38 from |

$ |

VA Form |

|

|

51. RESIDUAL INCOME |

|

$ |

|

|

|

|

|

|

52. RESIDUAL INCOME GUIDELINE |

|

$ |

|

|

53.DEBT- INCOME RATIO (If Income Ratio is over 41% and Residual Income is not 120% of guideline, statement of justification signed by underwriter's supervisor must be included on or with VA Form

|

|

|

|

|

|

|

|

|

% |

54. SPOUSE INCOME CONSIDERED |

|

55. SPOUSE'S INCOME AMOUNT (If considered) |

|||||||

YES |

NO |

(If "Yes," Complete Item 55) |

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

DISCOUNT INFORMATION (Applicable for All Loans) |

|

||||||

56. DISCOUNT POINTS CHARGED |

|

|

|

% OR |

$ |

|

|||

|

|

|

|

|

|

|

|

||

57. DISCOUNT POINTS PAID BY VETERAN |

|

|

|

% OR |

$ |

|

|||

|

|

|

|

|

|

|

|

||

58. TERM (Months) |

|

59. INTEREST RATE |

|

|

60. FUNDING FEE EXEMPT |

||||

|

|

|

|

|

% |

|

Y - EXEMPT |

N - NOT EXEMPT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FOR IRRRLS ONLY |

|

|

|

|||

61. PAID IN FULL VA LOAN NUMBER |

|

|

|

|

|

||||

|

|

|

|

|

|

||||

62. ORIGINAL LOAN AMOUNT |

|

63. ORIGINAL INTEREST RATE |

|||||||

$ |

|

|

|

|

|

|

|

|

% |

|

|

|

|

|

|

|

|

|

|

64. REMARKS |

|

|

|

|

|

|

|

|

|

VA FORM

| Fact Name | Details |

|---|---|

| Loan Number | The form requires a 12-digit VA loan number to identify the loan. |

| Veteran Information | Essential details such as name, social security number, gender, and date of birth are collected. |

| Entitlement Code | The form includes an entitlement code ranging from 01 to 11, derived from the VA Certificate of Eligibility. |

| Loan Purpose | Borrowers must specify the purpose of the loan, which can include home purchase, refinance, or improvements. |

| Governing Law | This form is governed by federal regulations under the Department of Veterans Affairs. |

Completing the Loan Summary Sheet requires careful attention to detail. Each section must be filled out accurately to ensure a smooth processing of your loan application. Follow the steps below to fill out the form correctly.

The Loan Summary Sheet is used to collect essential information about a VA loan. This form helps streamline the loan process by providing details such as the veteran's name, loan amount, and property type. It ensures that all necessary information is gathered for the loan application and approval process.

Several key pieces of information are required, including:

Completing all sections accurately is crucial for processing the loan effectively.

The Loan Summary Sheet should be completed by the veteran or an authorized representative, such as a loan officer. It is important that the person filling out the form has accurate and up-to-date information to ensure a smooth loan application process.

If a mistake is made, it is important to correct it as soon as possible. Errors can lead to delays in the loan approval process. You can either cross out the incorrect information and write the correct details or fill out a new form. Ensure that any changes are clear and legible.

The completed Loan Summary Sheet can be submitted electronically or in paper form, depending on the lender's requirements. Check with your lender for their preferred submission method. Ensure that all required documents accompany the form to avoid processing delays.

Filling out the Loan Summary Sheet form can be a daunting task, and many individuals make mistakes that can delay the approval process. One common error is failing to provide the correct VA's 12-digit loan number. This number is essential for tracking the loan and ensuring that all documentation is properly associated. Omitting or miswriting this number can lead to significant confusion and delays.

Another frequent mistake involves inaccuracies in the veteran's personal information. Errors in the veteran's name, social security number, or date of birth can create complications. These details must match the official records exactly. Even a minor typo can result in a denial or a request for further documentation, prolonging the process unnecessarily.

Many applicants also overlook the importance of selecting the correct branch of service and military status. Incorrect selections can lead to misunderstandings regarding eligibility. It is vital to check the appropriate box carefully, as this information directly impacts the loan's processing and approval.

In addition, applicants often fail to provide accurate figures for the loan amount and purchase price. These numbers should reflect the actual costs involved in the transaction. Discrepancies can trigger additional scrutiny from lenders, potentially jeopardizing the approval timeline.

Another mistake that can be easily overlooked is the failure to check the energy improvements section. This section allows veterans to indicate any enhancements that may affect the loan's value. Not completing this part can result in missed opportunities for financial benefits related to energy-efficient upgrades.

Lastly, individuals frequently neglect to review the credit score and debt-income ratio sections thoroughly. Providing inaccurate financial information can lead to complications in the underwriting process. Ensuring that these figures are correct is crucial for a smooth approval experience.

The Loan Summary Sheet is a vital document in the VA loan process, providing essential information about the veteran and the loan details. Alongside this form, several other documents are commonly utilized to ensure a smooth transaction. Each of these documents serves a specific purpose, contributing to the overall clarity and effectiveness of the loan application process.

Incorporating these documents alongside the Loan Summary Sheet streamlines the VA loan application process. Each plays a critical role in ensuring that all necessary information is available for a successful loan approval. Understanding their importance can lead to a more efficient borrowing experience for veterans.

The Loan Summary Sheet form shares similarities with several other documents in the mortgage and lending landscape. Each document serves a specific purpose but contains overlapping information relevant to loan processing and borrower identification. Below is a list of documents that are similar to the Loan Summary Sheet form:

When filling out the Loan Summary Sheet form, attention to detail is crucial. Here are some important dos and don'ts to keep in mind:

By following these guidelines, you can help ensure a smoother process for your loan application. Attention to detail makes a significant difference!

Understanding the Loan Summary Sheet form is crucial for veterans seeking VA loans. However, several misconceptions can lead to confusion. Here are four common misunderstandings:

This is not true. While the form does ask if the veteran is a first-time homebuyer, it is also applicable for veterans who have purchased homes before. It includes various options for refinancing and other loan purposes.

Not all sections are mandatory for every loan. For example, some questions only apply to specific loan types, such as refinancing. Understanding which sections are relevant can simplify the process.

While the loan amount is a significant aspect, the form also collects information about the veteran's personal details, military service, and property type. This information is essential for processing the loan accurately.

This is misleading. The Loan Summary Sheet is just one part of the application process. Additional documents, such as the Certificate of Eligibility and income verification, are also required to complete the application.

When filling out the Loan Summary Sheet form, several important points should be considered to ensure accuracy and completeness. Here are some key takeaways:

By keeping these takeaways in mind, individuals can navigate the Loan Summary Sheet with greater confidence and efficiency.