The Medicaid Income Trust form, commonly referred to as a Qualified Income Trust (QIT), serves as a vital tool for individuals whose income exceeds the Medicaid eligibility limits for long-term care services, including nursing home care. By utilizing a QIT, individuals can place their excess income into a designated account each month, thereby allowing them to qualify for Medicaid assistance. Establishing this trust requires a formal written agreement and the creation of a special account where monthly deposits are made. It is essential for those with income surpassing the thresholds set for various Medicaid programs, such as the Institutional Care Program (ICP) or the Home and Community Based Services (HCBS) waivers, to consider setting up a QIT. While professional guidance can be beneficial in drafting the agreement, it is not mandatory. The trust must meet specific criteria, including being irrevocable and stipulating that any remaining funds at the time of the individual’s death will revert to the state, up to the amount of Medicaid benefits received. Monthly contributions to the QIT must be sufficient to ensure that the individual's income falls within the allowable limits for Medicaid eligibility, and any income withdrawn from the trust will count against their income for the month. Understanding the intricacies of the QIT process is crucial for those seeking long-term care services while navigating the complexities of Medicaid eligibility.

Qualified Income Trust Information Sheet

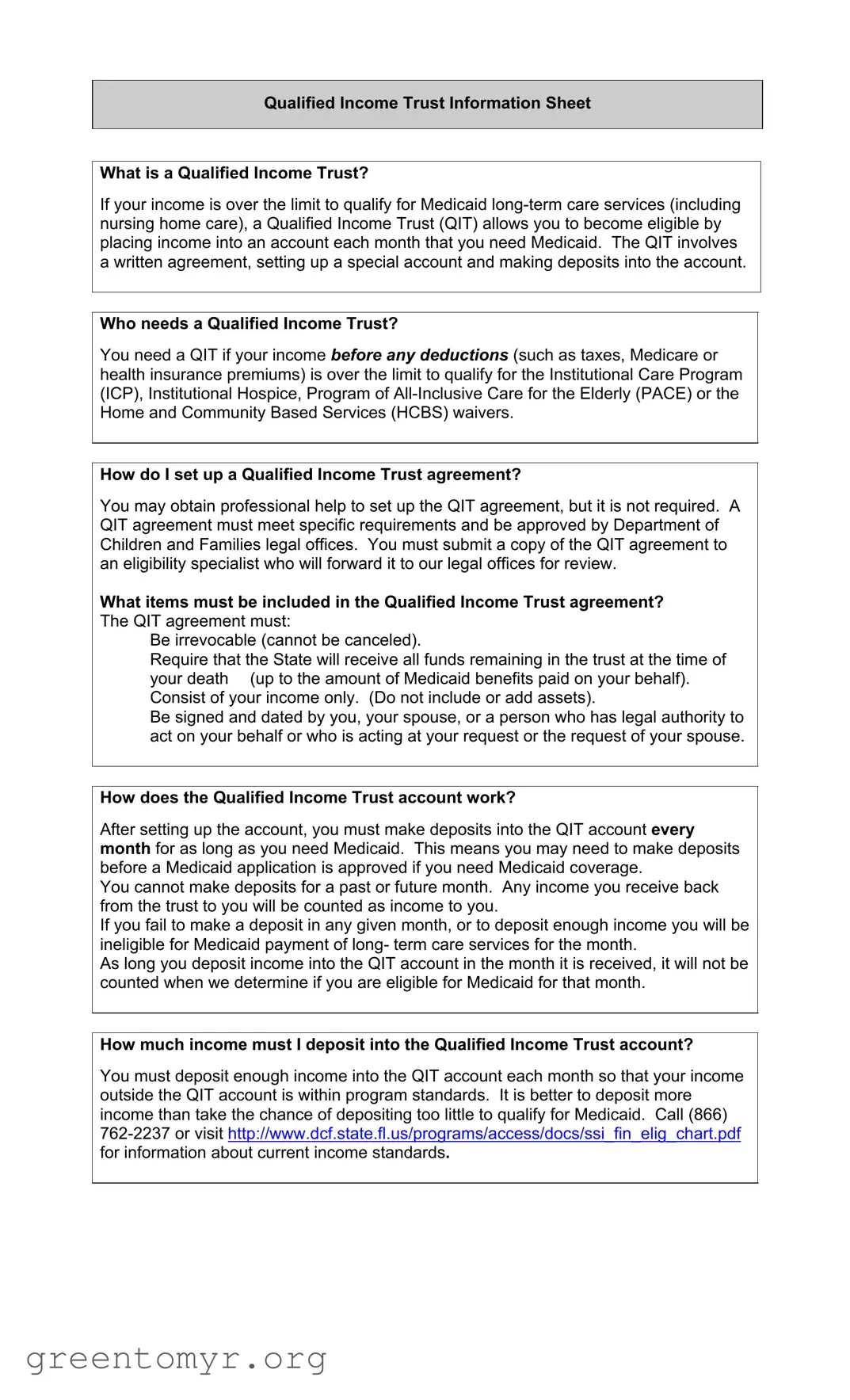

What is a Qualified Income Trust?

If your income is over the limit to qualify for Medicaid

Who needs a Qualified Income Trust?

You need a QIT if your income before any deductions (such as taxes, Medicare or health insurance premiums) is over the limit to qualify for the Institutional Care Program (ICP), Institutional Hospice, Program of

How do I set up a Qualified Income Trust agreement?

You may obtain professional help to set up the QIT agreement, but it is not required. A QIT agreement must meet specific requirements and be approved by Department of Children and Families legal offices. You must submit a copy of the QIT agreement to an eligibility specialist who will forward it to our legal offices for review.

What items must be included in the Qualified Income Trust agreement? The QIT agreement must:

Be irrevocable (cannot be canceled).

Require that the State will receive all funds remaining in the trust at the time of your death (up to the amount of Medicaid benefits paid on your behalf). Consist of your income only. (Do not include or add assets).

Be signed and dated by you, your spouse, or a person who has legal authority to act on your behalf or who is acting at your request or the request of your spouse.

How does the Qualified Income Trust account work?

After setting up the account, you must make deposits into the QIT account every month for as long as you need Medicaid. This means you may need to make deposits before a Medicaid application is approved if you need Medicaid coverage.

You cannot make deposits for a past or future month. Any income you receive back from the trust to you will be counted as income to you.

If you fail to make a deposit in any given month, or to deposit enough income you will be ineligible for Medicaid payment of long- term care services for the month.

As long you deposit income into the QIT account in the month it is received, it will not be counted when we determine if you are eligible for Medicaid for that month.

How much income must I deposit into the Qualified Income Trust account?

You must deposit enough income into the QIT account each month so that your income outside the QIT account is within program standards. It is better to deposit more income than take the chance of depositing too little to qualify for Medicaid. Call (866)

What happens to the income I deposit in the Qualified Income Trust account?

The income you have in and out of the QIT is used to calculate your patient responsibility. If you do have a patient responsibility, you are responsible for paying that amount. If there is money left in the QIT upon your death, it is paid to the State, up to an amount equal to the total medical assistance paid on your behalf by the state while the trust was in effect.

How to pay funds remaining in the QIT to the State?

The QIT trustee or other individual acting on your behalf should contact the long term care facility to see if any refund for the month of death is due back to the trust. The balance of the QIT at the date of death, plus any refund from the long term care facility is to be paid to the State.

Mail a check payable to the “Agency for Health Care Administration” to: Xerox State Healthcare, LLC

PO Box 12188 Tallahassee, FL

A brief cover letter or note should state that the payment is for a QIT and include your name, Social Security number, and/or Medicaid ID number. Enclose a copy of the QIT bank statement covering the date of death to confirm the check is for the balance. Also, include documentation of any refunds received from the long term care facility. Contact Xerox State Healthcare, LLC at (877)

| Fact Name | Details |

|---|---|

| Definition of QIT | A Qualified Income Trust (QIT) allows individuals with income over Medicaid limits to qualify for long-term care services by depositing income into a special account. |

| Eligibility Requirement | Individuals whose income exceeds Medicaid limits for services like Institutional Care Program (ICP) or Home and Community Based Services (HCBS) need a QIT. |

| Setting Up a QIT | While professional help is not mandatory, a QIT agreement must be approved by the Department of Children and Families and submitted to an eligibility specialist. |

| Required Agreement Items | The QIT must be irrevocable, state that remaining funds go to the State upon death, and include only your income. |

| Monthly Deposits | Deposits must be made monthly into the QIT account. Failure to deposit the required amount can lead to ineligibility for Medicaid coverage. |

| Income Calculation | Income in the QIT is used to determine patient responsibility. Any excess funds after death are paid to the State, equal to Medicaid benefits received. |

| Payment to the State | Upon death, the QIT trustee must contact the long-term care facility for any refunds and send the remaining balance to the State. |

| Governing Laws | QITs are governed by state-specific laws, including Florida Statutes Chapter 409.913 and related Medicaid regulations. |

Filling out the Medicaid Income Trust form is an essential step for individuals seeking Medicaid long-term care services. This process involves several key steps to ensure that the Qualified Income Trust (QIT) is properly established and compliant with state requirements. Follow these instructions carefully to complete the form accurately.

Once the form is completed and submitted, you will await confirmation from the Department of Children and Families. This approval is crucial for moving forward with your Medicaid application. Ensure you maintain communication with your eligibility specialist throughout the process to address any questions or concerns that may arise.

A Qualified Income Trust (QIT) is a financial tool that allows individuals with income exceeding the Medicaid eligibility limit to qualify for long-term care services. By depositing income into a designated account each month, individuals can meet Medicaid requirements. The QIT involves a written agreement and the establishment of a special account where monthly deposits are made.

A QIT is necessary for individuals whose income, before any deductions such as taxes or health insurance premiums, exceeds the limit set for various Medicaid programs. These programs include the Institutional Care Program (ICP), Institutional Hospice, the Program of All-Inclusive Care for the Elderly (PACE), and Home and Community Based Services (HCBS) waivers.

Setting up a QIT agreement can be done with or without professional assistance. The agreement must comply with specific requirements and needs approval from the Department of Children and Families legal offices. Once the agreement is drafted, a copy should be submitted to an eligibility specialist for review and approval.

The QIT agreement must include the following elements:

Once the QIT account is established, monthly deposits must be made for as long as Medicaid coverage is needed. It is essential to deposit income in the month it is received, as past or future deposits are not allowed. If deposits are not made or are insufficient, Medicaid eligibility for long-term care services may be affected.

Individuals must deposit enough income each month to ensure that their income outside the QIT account remains within the program standards. It is advisable to deposit more income than the minimum requirement to avoid disqualification. For current income standards, individuals can call (866) 762-2237 or visit the relevant state website.

The income deposited in the QIT is used to calculate any patient responsibility. If there is a patient responsibility, the individual must pay that amount. Upon the individual's death, any remaining funds in the QIT will be paid to the State, up to the total amount of medical assistance provided during the trust's duration.

The trustee or authorized individual should contact the long-term care facility to determine if any refunds are due for the month of death. The balance of the QIT, along with any refunds, should be paid to the State. Payments should be made via check to the “Agency for Health Care Administration” and mailed to:

Xerox State Healthcare, LLC

PO Box 12188

Tallahassee, FL 32317-2188

A brief cover letter should accompany the payment, stating that it is for a QIT and include the individual's name, Social Security number, and/or Medicaid ID number. It is also important to enclose documentation, such as the QIT bank statement and any refund records from the long-term care facility. For questions regarding payment, individuals can contact Xerox State Healthcare, LLC at (877) 357-3268.

Filling out the Medicaid Income Trust form can be a complex process, and mistakes can lead to delays or even denial of benefits. One common mistake is failing to understand the **irrevocable** nature of the Qualified Income Trust (QIT). Many individuals mistakenly believe they can change or cancel the trust after it is established. This misunderstanding can lead to significant issues when applying for Medicaid.

Another frequent error is not including all required parties in the signing process. The QIT agreement must be signed and dated by the individual, their spouse, or a legally authorized representative. Omitting signatures can result in the form being rejected, causing unnecessary delays in receiving benefits.

Inadequate deposits into the QIT account can also jeopardize eligibility. Some individuals underestimate the amount they need to deposit each month. If the income outside the QIT exceeds the program limits, it can lead to ineligibility for Medicaid long-term care services. It's crucial to deposit enough income to ensure compliance with the program standards.

Failing to submit the QIT agreement to an eligibility specialist is another mistake that can have serious consequences. After setting up the trust, the agreement must be forwarded for review. Neglecting this step can leave individuals without the necessary approval, impacting their Medicaid application.

Additionally, some people forget to keep accurate records of their deposits and transactions related to the QIT. Documentation is essential for tracking compliance and ensuring that the correct amounts are being deposited each month. Without proper records, it may be challenging to prove eligibility or resolve any disputes that arise.

Another common oversight is misunderstanding how income is calculated. Any income received back from the trust is considered personal income. Individuals may not realize that this could affect their eligibility for Medicaid. It’s important to be aware of how these calculations work to avoid surprises later on.

Some applicants fail to recognize the importance of contacting the long-term care facility regarding any refunds due upon death. The QIT trustee must ensure that any remaining funds are properly addressed. Ignoring this step can lead to complications in settling the trust and ensuring that funds are appropriately paid to the State.

Lastly, not reaching out for professional assistance can be a significant mistake. While it is not required, consulting with a legal expert can provide valuable guidance. They can help ensure that the QIT agreement meets all necessary requirements, reducing the risk of errors that could affect Medicaid eligibility.

When setting up a Qualified Income Trust (QIT) for Medicaid eligibility, several other documents and forms may be required or beneficial to complete the process. Each of these documents serves a specific purpose in ensuring compliance with Medicaid regulations and facilitating the management of your trust and eligibility.

Having these documents prepared and organized can streamline the process of establishing and maintaining a Qualified Income Trust. Each document plays a vital role in ensuring compliance with Medicaid regulations and protecting your eligibility for necessary healthcare services.

The Medicaid Income Trust form shares similarities with several other legal documents that serve specific purposes in financial and estate planning. Below are ten documents that are comparable to the Qualified Income Trust (QIT) form, highlighting their similarities:

When filling out the Medicaid Income Trust form, it is crucial to follow specific guidelines to ensure compliance and eligibility. Here are seven important dos and don’ts to keep in mind:

Following these guidelines will help ensure that your Medicaid application process goes smoothly. Always remember that proper management of your Qualified Income Trust is essential for maintaining your eligibility for long-term care services.

Misconceptions about the Medicaid Income Trust form can lead to confusion and mistakes in managing eligibility for Medicaid long-term care services. Here are ten common misconceptions clarified:

Understanding these misconceptions can help individuals navigate the complexities of Medicaid eligibility and ensure compliance with the requirements of a Qualified Income Trust.

Filling out and using the Medicaid Income Trust form can be a vital step for individuals seeking Medicaid long-term care services. Here are some key takeaways to consider: