The MetLife Annuity Loan Application form is a critical document for individuals seeking to borrow against their annuity contracts. This form collects essential account information, including the borrower's name, address, Social Security number, and employment status. It also requires the borrower to specify the desired loan amount, either by entering a specific figure or opting for the maximum available loan based on their contract terms. Furthermore, the form outlines the intended use of the loan proceeds, distinguishing between loans for acquiring a primary residence and those for other purposes, each with specific repayment terms. Borrowers must acknowledge existing loans from retirement plans, as outstanding defaults can hinder the processing of new loan requests. The application also includes sections for spousal consent, particularly for ERISA plans, ensuring compliance with federal regulations. Lastly, the form emphasizes the borrower's responsibility to understand the terms and conditions of the loan, including potential tax implications and the requirement for quarterly repayments. Overall, the MetLife Annuity Loan Application serves as a comprehensive guide for borrowers navigating the loan process while ensuring adherence to legal and financial obligations.

MetLife Insurance Company of Connecticut

Annuity Loan Application and Agreement

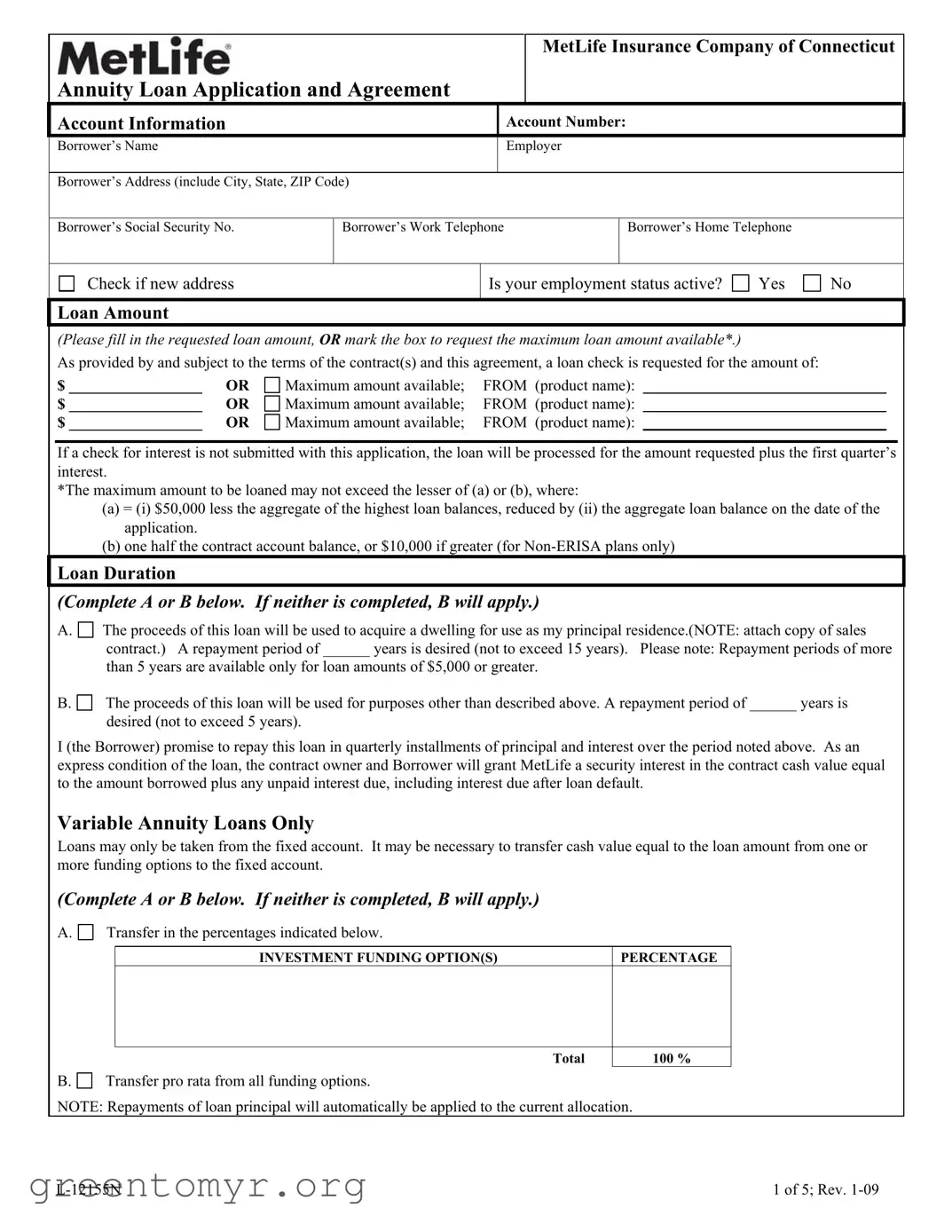

Account Information |

|

|

|

Account Number: |

|

|

|

Borrower’s Name |

|

|

|

Employer |

|

|

|

|

|

|

|

|

|

|

|

Borrower’s Address (include City, State, ZIP Code) |

|

|

|

|

|||

|

|

|

|

|

|

||

Borrower’s Social Security No. |

Borrower’s Work Telephone |

|

Borrower’s Home Telephone |

|

|||

|

|

|

|

|

|

||

Check if new address |

|

Is your employment status active? |

Yes |

No |

|||

|

|

|

|

|

|

|

|

Loan Amount

(Please fill in the requested loan amount, OR mark the box to request the maximum loan amount available*.)

As provided by and subject to the terms of the contract(s) and this agreement, a loan check is requested for the amount of:

$ _________________ |

OR |

Maximum amount available; |

FROM (product name): |

|

$ _________________ |

OR |

Maximum amount available; |

FROM |

(product name): |

$ _________________ |

OR |

Maximum amount available; |

FROM |

(product name): |

If a check for interest is not submitted with this application, the loan will be processed for the amount requested plus the first quarter’s interest.

*The maximum amount to be loaned may not exceed the lesser of (a) or (b), where:

(a) = (i) $50,000 less the aggregate of the highest loan balances, reduced by (ii) the aggregate loan balance on the date of the application.

(b) one half the contract account balance, or $10,000 if greater (for

Loan Duration

(Complete A or B below. If neither is completed, B will apply.)

A.

The proceeds of this loan will be used to acquire a dwelling for use as my principal residence.(NOTE: attach copy of sales

contract.) A repayment period of ______ years is desired (not to exceed 15 years). Please note: Repayment periods of more

than 5 years are available only for loan amounts of $5,000 or greater.

B.

The proceeds of this loan will be used for purposes other than described above. A repayment period of ______ years is

desired (not to exceed 5 years).

I (the Borrower) promise to repay this loan in quarterly installments of principal and interest over the period noted above. As an express condition of the loan, the contract owner and Borrower will grant MetLife a security interest in the contract cash value equal to the amount borrowed plus any unpaid interest due, including interest due after loan default.

Variable Annuity Loans Only

Loans may only be taken from the fixed account. It may be necessary to transfer cash value equal to the loan amount from one or more funding options to the fixed account.

(Complete A or B below. If neither is completed, B will apply.)

A.

Transfer in the percentages indicated below.

INVESTMENT FUNDING OPTION(S)

PERCENTAGE

Total

100 %

B. |

Transfer pro rata from all funding options. |

NOTE: Repayments of loan principal will automatically be applied to the current allocation.

1 of 5; Rev. |

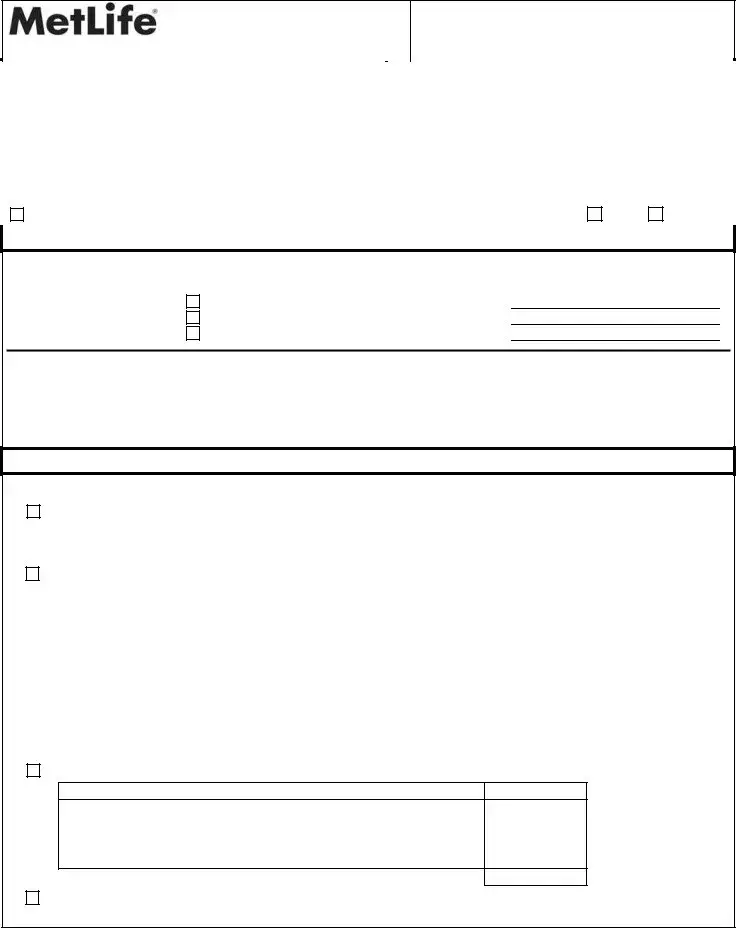

Group Plans Only

(Check A or B below. If neither is completed, B will apply.)

A.

B.

Cash Value attributable to employer contributions (other than contributions derived from salary reduction) may be used to secure this loan.

Cash Value attributable to employer contributions (other than contributions derived from salary reduction) may not be used to secure this loan.

Loan Request Information

List all outstanding loans from any retirement plan of the employer (or related employer) during the previous 12 months, including defaulted loans which have not been repaid or offset.* A loan will not be processed if the participant has an outstanding loan

under any retirement plan of the employer (or related employer) which has defaulted, but not been repaid or offset.

Company Name

Certificate or

Contract Number

Current Vested

Account Balance

Current Loan

Balance

Highest Loan Balance

During Past 12

Months

In Default But Not Yet Offset?

Acknowledgement and Signatures

I authorize the loan check and bills to be sent to this billing address:

Street |

City, State, Zip Code |

I (the borrower) understand that federal income tax loan regulations will be enforced to the extent necessary to keep the annuity contract qualified under applicable Internal Revenue Code provisions and under other applicable tax and benefits plan laws and regulations. I understand that I may have only one loan at a time from this contract or certificate. I may not have another loan from this contract or certificate until the outstanding loan and interest are repaid in full.

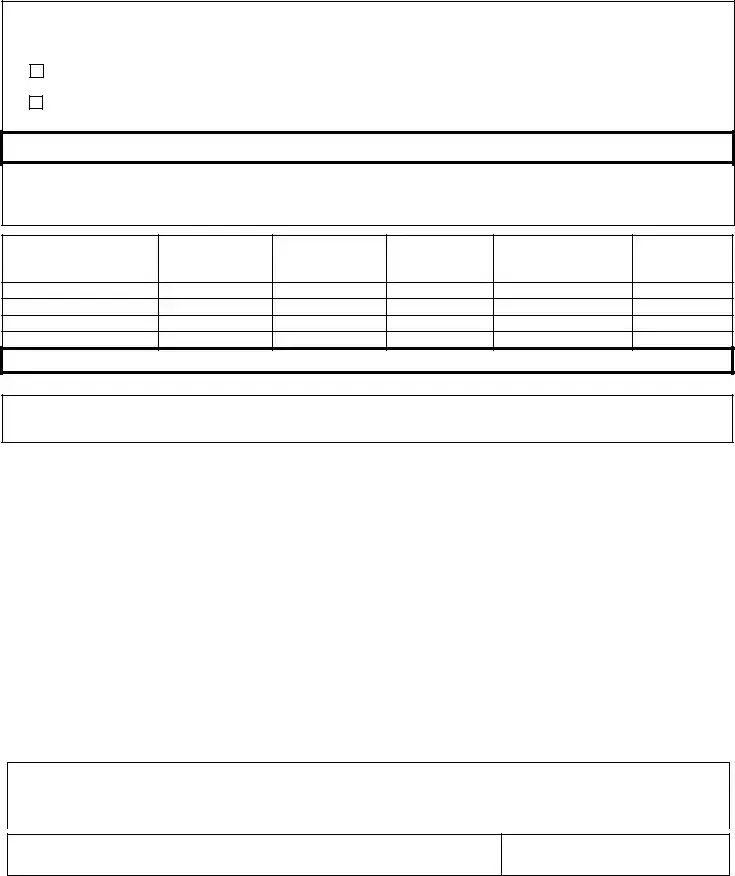

I understand that a loan is not permitted if I have a loan from 1) any of my employer’s retirement plans or 2) from retirement plans of a related employer, that is in default and is still outstanding due to tax law restrictions on offset; and I certify that I do not have any such previously defaulted loans.

I understand that I am responsible for ensuring that I do not borrow an amount in excess of the loan amount permitted under section 72(p) of the Internal Revenue Code of 1986, as amended ( the “Code”); and that adverse tax consequences, including treatment of such excess amounts as deemed distributions, will result in such case.

I (borrower and/or contract owner) understand and accept the terms and conditions applicable to this loan, including the special terms and conditions described in the "Contract Loan Terms and Conditions" section of this agreement, and accept full responsibility for compliance with these requirements. I/we also understand that MetLife accepts no responsibility concerning adherence to these requirements and that contract values are assigned to MetLife as sole security of the loan.

I acknowledge that I have read and understood the terms and conditions of this loan agreement:

I certify this withdrawal is permissible under the terms of the Plan.

Signature of Plan Administrator/Authorized Representative |

Date |

|

|

Borrower’s Signature

Date

*A loan offset occurs when your accrued plan benefit is reduced (offset) in order to repay the loan (including the enforcement of our security interest in your accrued benefit).

2 of 5; Rev. |

Spousal Consent – ERISA Plans Only

I hereby consent to the loan request by the contract owner as set forth above. I understand that if I am married, I must obtain my spouse's consent to this loan. I understand that a spouse is guaranteed certain rights to assets in this retirement account by federal law and these rights include the right to a preretirement survivor's annuity and the right to a joint and survivor annuity and these rights could be diminished by an annuity loan which is not repaid. This consent cannot be revoked once given.

__ I certify that I am not married and therefore spousal consent to this loan is not required __ I am married and my spouse's consent to this loan is provided below

__ I am married and certify my spouse's consent cannot be obtained or is not required because: (Check only one box below) __ My spouse cannot be found

__ My spouse is legally incompetent to give consent (spouse's legal guardian may give consent)

__ I am legally separated from or have been abandoned by my spouse (within the meaning of local law) and have a court order to such effect and no qualified domestic relations order exists that requires spousal consent to this loan.

Borrower’s Signature

Date

Spouse’s Name (Please print)

Spouse’s Signature

Date

I certify that the

Notary Public’s Signature

Date

Plan Administrator’s Signature

Date

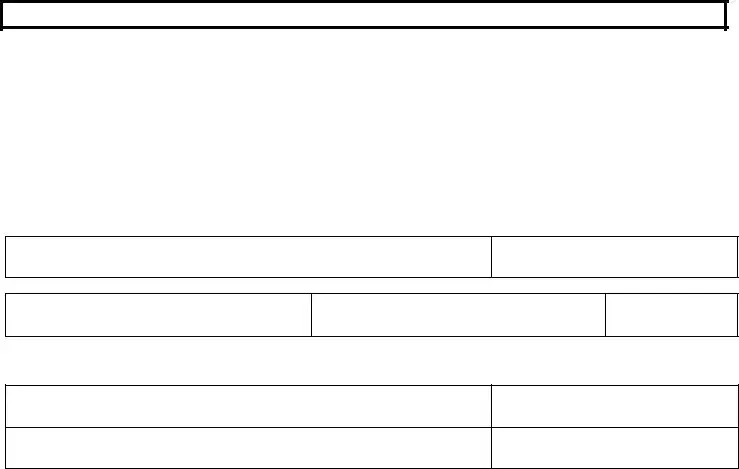

|

Mailing Instructions |

|

Mail this form to: |

Overnight mail only: |

Fax to: |

MetLife |

MetLife |

|

P.O. Box 572 |

4700 Westown Parkway, Ste. 200 |

|

Des Moines, IA |

West Des Moines, IA 50266 |

|

SEE NEXT TWO PAGES FOR LOAN TERMS AND CONDITIONS

3 of 5; Rev. |

MetLife Insurance Company of Connecticut

Annuity Contract

Loan Terms and Conditions

Minimum and Maximum Loan Amounts

•Minimum: $1,000*

•Maximum:

The maximum amount that can be borrowed is an amount which when added to the other outstanding loan balances under plans of the same or related employer ( the “Plan”) does not exceed the lesser of:

1.$50,000 reduced by the excess ( if any) of :(a) the highest total amount of the Plan loans outstanding during the twelve

month period ending on the day before this loan over (b) the outstanding plan loan amount on the date of this loan.

2.

In addition to the above limits, in no event may the loan amount under this Contract exceed :

Vested Contract Cash Value |

Additional loan limitation under this Contract |

$1,250 - $12,500 |

80 % of vested Contract cash value for |

|

50% of vested Contract cash value for ERISA Plan |

Over $12,500 - $20,000 |

$10,000 for |

|

50%of vested Contract cash value for ERISA Plan |

Over $20,000 |

Lesser of |

|

(a)50% of the vested contract cash value or (b) $50,000.reduced by the highest Plan loan balance |

|

during the previous 12 nmonths |

|

|

*For the following contract holders in the state of New Jersey, the minimum loan amount is $500.00 - PrimElite II; Portfolio Architect 3; Universal Annuity (Individual); Vintage; Vintage II; Vintage II Series II; Vintage 3

Loan Duration

Repayments of principal and interest must be made in quarterly installments from one to five years. If the proceeds of the loan are used to acquire the Borrower’s principal residence, the loan repayment period may be extended to fifteen (15) years. Repayment periods of more than five (5) years are available only for loan amounts of $5,000 or greater.

The Borrower may have only one outstanding loan per contract.

Loan Billing and Repayment

Loan proceeds and bills will be mailed to the billing address noted in this agreement. If no address is specified, the check and all correspondence will be mailed to the most current address on our records for the Borrower.

A bill in the amount of the quarterly repayment due (to include principal and interest) will be mailed 45 days prior to the repayment due date. Repayments will be applied first to unpaid interest due, then to loan principal. If the repayment amount exceeds the total amount billed, the excess money will be applied towards the outstanding loan principal, not to future quarterly repayments.

Acceptable methods for repayment are personal checks or bank checks.

Interest Charged

Quarterly loan interest must be paid in advance. Interest charged will be at the rate in effect at the time the request is received in good order at MetLife Home Office. The loan’s first quarter interest may be paid from the loan proceeds, or by check at the time the loan is made.

If the original loan check is returned within twenty (20) days of the date of the loan check, loan interest will be waived.

The loan interest rate is determined by whether the plan or contract is subject to ERISA.

4 of 5; Rev. |

ERISA Loans:

The interest rate charged at the inception of the loan will remain in effect for one year from the loan effective date. The interest rate may change annually. Notification of any change in the interest rate charged will be made at least thirty (30) days prior to its taking effect. If the interest rate changes, required quarterly repayments will change.

The interest rate charged at the loan’s effective date will remain in effect for the duration of the loan.

Current loan interest rates can be obtained by contacting your MetLife representative directly or by calling our Annuity Customer Service Center.

Loan Default and Taxation

You may repay amounts after a loan default. Such repayments will prevent any additional interest from accruing on the repaid amounts and will reduce the amount of your outstanding loan balance for purposes of determining the amount of any additional loans you may have under retirement plans of your employer. However, such repayments after the administrative grace period will not reverse the default or the deemed distribution of the unpaid loan balance that is reportable for federal income tax purposes. (See below.)

If a quarterly repayment has not been received

If a repayment is not received within ninety (90) days of its due date and the billed amount has not been paid as described in the previous paragraph, the entire loan will be placed in default. A tax report will be produced for the calendar year the loan was placed in default, reporting to the IRS as a deemed distribution the outstanding loan amount. Interest will be charged on the defaulted loan amount until it is repaid. The defaulted loan can be repaid at any time to avoid the interest charge accrual. At the time the contract cash value becomes available for loan repayment under federal tax law or regulation, and to the extent permissible under applicable state regulations, the cash value will be reduced by the amount of the loan outstanding and any unpaid interest due. Any applicable deferred sales charges or surrender penalties will be taken. The loan will no longer be outstanding.

The loan plus any unpaid interest due must be repaid in full at the time of an allowable full surrender, including a direct rollover or transfer. Amounts available for partial surrender , including a direct rollover or transfer, will be limited to the cash surrender value of the contract minus the loan amount outstanding, including amounts in default, minus unpaid interest due.

In the event the Borrower files a bankruptcy petition while the loan remains in effect, an exemption will be elected for the annuity contract, including but not limited to its cash value, pursuant to Section 522 of Federal Bankruptcy Code or under a state law exemption at least as broad in scope as Section 522.

PLEASE RETAIN THIS COPY FOR YOUR RECORDS

5 of 5; Rev. |

| Fact Name | Description |

|---|---|

| Loan Amount Limits | The minimum loan amount is $1,000, while the maximum is determined by the lesser of $50,000 or half of the contract account balance, with specific conditions for non-ERISA plans. |

| Loan Duration Options | Borrowers can choose a repayment period of up to 15 years if the loan is used for purchasing a principal residence, otherwise, it is limited to 5 years. |

| Security Interest | MetLife will hold a security interest in the contract's cash value equal to the borrowed amount plus any unpaid interest. |

| Spousal Consent Requirement | For ERISA plans, spousal consent is necessary if the borrower is married, as federal law protects spousal rights to retirement assets. |

| State-Specific Regulations | In New Jersey, the minimum loan amount for certain contracts is reduced to $500, highlighting the need to be aware of state-specific regulations. |

Filling out the MetLife Annuity Loan Application form is a straightforward process that requires careful attention to detail. Once completed, this form will facilitate the processing of your loan request. Below are the steps to help you navigate the application smoothly.

The application requires several key pieces of information. You will need to provide your account number, full name, employer details, and contact information, including both work and home telephone numbers. Additionally, you must indicate your employment status and specify the loan amount you are requesting. If applicable, you should also include details about any outstanding loans from retirement plans associated with your employer.

The minimum loan amount you can request is $1,000. The maximum amount varies based on your specific situation. Generally, it cannot exceed the lesser of $50,000 reduced by outstanding loans or one-half of your non-forfeitable accrued benefit under the plan, with a minimum of $10,000 for non-ERISA plans. For New Jersey contract holders, the minimum loan amount is $500 for certain plans.

Loan repayments are typically made in quarterly installments of both principal and interest. The repayment period can vary depending on the purpose of the loan. If the loan is used to acquire a principal residence, the repayment period can extend up to 15 years. For other purposes, the maximum repayment period is 5 years. It's important to note that you can only have one outstanding loan at a time from your contract.

If a repayment is not received within 31 days after its due date, the loan may be considered in default. In this case, the outstanding amount will be reported to the IRS as a deemed distribution, which may have tax implications. You can still repay the loan after default, but this will not reverse the default status. It is crucial to stay current with repayments to avoid additional interest and potential tax consequences.

Filling out the MetLife Annuity Loan Application form can be straightforward, but many people make common mistakes that can delay the process or even lead to rejection. One frequent error is failing to provide complete account information. This includes not filling in the account number, borrower’s name, or address accurately. Missing or incorrect details can create confusion and slow down the processing of the loan.

Another mistake is not specifying the loan amount correctly. Applicants often either leave this section blank or request an amount that exceeds the allowable limits. It’s essential to understand the maximum loan amount you can request based on your contract. If the application does not reflect the correct figures, it may be rejected or require additional clarification, causing unnecessary delays.

People sometimes overlook the importance of indicating their employment status. Not checking the box for "active" employment can lead to complications. If your employment status is not current, it may affect your eligibility for the loan. Always ensure that this section is filled out accurately to avoid misunderstandings.

Additionally, some applicants neglect to provide information about outstanding loans from other retirement plans. If there are any loans that have not been repaid or offset, it is critical to disclose this information. Failing to do so can lead to the loan request being denied outright, as MetLife requires a full account of any existing debts.

Lastly, many people forget to review the acknowledgment and signatures section. This part confirms that you understand the terms of the loan and that you have provided accurate information. Without the necessary signatures, the application may be deemed incomplete. Always double-check that all required signatures are in place before submitting the form.

When applying for a MetLife Annuity Loan, several additional forms and documents may be required to ensure a smooth processing experience. Below is a list of commonly used documents that accompany the loan application. Each document serves a specific purpose and may be necessary for the approval of your loan request.

Gathering these documents in advance can expedite the loan application process. Ensure that each document is completed accurately and submitted alongside your MetLife Annuity Loan Application form to avoid delays. If you have questions about any of these documents, consult with a financial advisor or legal expert for guidance.

The MetLife Annuity Loan Application form shares similarities with several other financial and legal documents. Below is a list of nine documents that are comparable to the MetLife Annuity Loan Application form, along with a brief explanation of how they are similar.

When filling out the MetLife Annuity Loan Application form, there are important dos and don'ts to keep in mind. Here’s a helpful list to guide you through the process.

Here are eight misconceptions about the MetLife Annuity Loan Application form along with explanations for each:

The maximum loan amount is limited. It cannot exceed $50,000 or one-half of your contract account balance, whichever is less. Always check the specific limits applicable to your plan.

You may only have one loan outstanding from your contract at any given time. You must repay any existing loan before taking out another.

Loan interest must be paid in advance. If the first quarter's interest is not paid, it will be added to the loan amount.

The application requires you to specify the purpose of the loan. If it is for acquiring a principal residence, specific documentation is needed.

You must disclose all outstanding loans from any retirement plan with your employer or related employers. Failure to do so can result in the denial of your loan application.

The repayment period varies based on the loan amount and purpose. Loans for acquiring a home can extend up to 15 years, while other loans are limited to 5 years.

If you are married, you must obtain your spouse's consent for the loan. This is a requirement under federal law to protect spousal rights.

Loan defaults can have serious tax consequences. If a repayment is not made within 90 days, the loan will be placed in default, and it will be reported to the IRS as a deemed distribution.