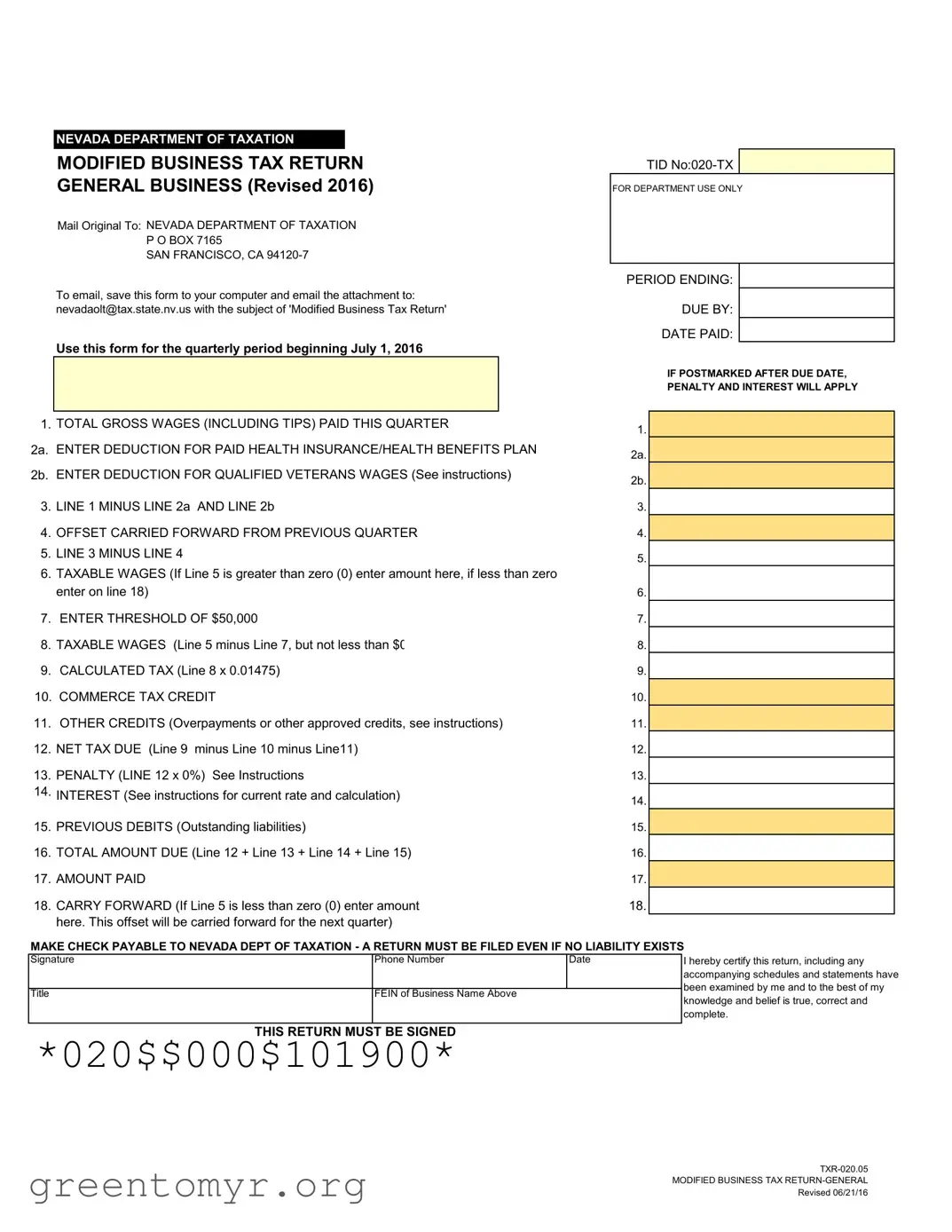

The Modified Business Tax (MBT) form is an essential document for employers in Nevada, designed to facilitate the reporting of taxable wages and the calculation of tax liabilities. This form must be completed quarterly, with specific deadlines for submission. Employers are required to report total gross wages paid, including tips, and can claim deductions for paid health insurance and qualified veterans' wages. The form guides users through a series of calculations, starting with gross wages and deducting applicable amounts to arrive at net taxable wages. A threshold of $50,000 is established, beyond which tax is calculated at a specified rate. Additionally, the form allows for the application of various credits, including the Commerce Tax Credit and other approved credits, which can reduce the overall tax liability. It is important to note that penalties and interest may apply for late submissions or payments, emphasizing the need for timely and accurate filing. The form must be signed and submitted to the Nevada Department of Taxation, ensuring compliance with state tax regulations.

|

NEVADA DEPARTMENT OF TAXATION |

|

|

|

|

|

|

|

|

|

|

|

MODIFIED BUSINESS TAX RETURN |

|

TID |

|

|

||||||

|

GENERAL BUSINESS (Revised 2016) |

|

FOR DEPARTMENT USE ONLY |

|

|||||||

|

Mail Original To: NEVADA DEPARTMENT OF TAXATION |

|

|

|

|

|

|

||||

|

P O BOX 7165 |

|

|

|

|

|

|

|

|

|

|

|

SAN FRANCISCO, CA |

|

|

|

|

|

|

|

|

|

|

|

To email, save this form to your computer and email the attachment to: |

|

PERIOD ENDING: |

|

|

||||||

|

|

|

|

DUE BY: |

|

|

|||||

|

[email protected] with the subject of 'Modified Business Tax Return' |

|

|

|

|

|

|||||

|

Use this form for the quarterly period beginning July 1, 2016 |

|

|

DATE PAID: |

|

|

|||||

|

|

|

IF POSTMARKED AFTER DUE DATE, |

||||||||

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

PENALTY AND INTEREST WILL APPLY |

|||

|

|

|

|

|

|

|

|

|

|

||

1. |

TOTAL GROSS WAGES (INCLUDING TIPS) PAID THIS QUARTER |

|

1. |

|

|

|

|

||||

2a. |

ENTER DEDUCTION FOR PAID HEALTH INSURANCE/HEALTH BENEFITS PLAN |

|

2a. |

|

|

|

|

||||

2b. |

ENTER DEDUCTION FOR QUALIFIED VETERANS WAGES (See instructions) |

|

2b. |

|

|

|

|

||||

3. |

LINE 1 MINUS LINE 2a AND LINE 2b |

|

|

|

|

|

3. |

|

|

|

|

4. |

OFFSET CARRIED FORWARD FROM PREVIOUS QUARTER |

|

4. |

|

|

|

|

||||

5. |

LINE 3 MINUS LINE 4 |

|

|

|

|

|

5. |

|

|

|

|

6. |

TAXABLE WAGES (If Line 5 is greater than zero (0) enter amount here, if less than zero |

|

|

|

|

|

|||||

|

|

|

|

|

|

||||||

|

enter on line 18) |

|

|

|

|

|

6. |

|

|

|

|

7. |

ENTER THRESHOLD OF $50,000 |

|

|

|

|

|

7. |

|

|

|

|

8. |

TAXABLE WAGES (Line 5 minus Line 7, but not less than $0 |

|

8. |

|

|

|

|

||||

9. |

CALCULATED TAX (Line 8 x 0.01475) |

|

|

|

|

|

9. |

|

|

|

|

10. COMMERCE TAX CREDIT |

|

|

|

|

|

10. |

|

|

|

|

|

11. |

OTHER CREDITS (Overpayments or other approved credits, see instructions) |

|

11. |

|

|

|

|

||||

12. |

NET TAX DUE (Line 9 minus Line 10 minus Line11) |

|

12. |

|

|

|

|

||||

13. |

PENALTY (LINE 12 x 0%) See Instructions |

0 |

|

|

|

|

13. |

|

|

|

|

14. |

INTEREST (See instructions for current rate and calculation) |

|

14. |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

15. |

PREVIOUS DEBITS (Outstanding liabilities) |

|

|

|

|

|

15. |

|

|

|

|

16. |

TOTAL AMOUNT DUE (Line 12 + Line 13 + Line 14 + Line 15) |

|

16. |

|

|

|

|

||||

17. |

AMOUNT PAID |

|

|

|

|

|

17. |

|

|

|

|

18. |

CARRY FORWARD (If Line 5 is less than zero (0) enter amount |

|

18. |

|

|

|

|

||||

|

here. This offset will be carried forward for the next quarter) |

|

|

|

|

|

|

||||

MAKE CHECK PAYABLE TO NEVADA DEPT OF TAXATION - A RETURN MUST BE FILED EVEN IF NO LIABILITY EXISTS |

|||||||||||

Signature |

|

|

Phone Number |

Date |

|

|

I hereby certify this return, including any |

||||

|

|

|

|

|

|

|

|

|

accompanying schedules and statements have |

||

|

|

|

|

|

|

|

|

|

been examined by me and to the best of my |

||

Title |

|

|

|

FEIN of Business Name Above |

|

|

|

||||

|

|

|

|

|

|

knowledge and belief is true, correct and |

|||||

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

complete. |

||

|

THIS RETURN MUST |

BE SIGNED |

|

|

|

|

|

|

|||

*020$$000$101900* |

|

|

101900 |

|

|||||||

|

|

|

|

|

|

|

|||||

MODIFIED BUSINESS TAX

INSTRUCTIONS - MODIFIED BUSINESS TAX RETURN - GENERAL BUSINESSES ONLY

(Financial Institutions need to use the form developed specifically for them,

IF YOU COMPLETE THIS FORM ONLINE THE CALCULATIONS WILL BE MADE FOR YOU

Line 1. Total Gross Wages - Enter the total amount of all gross wages and reported tips paid this calendar quarter Line 2a. Employer paid health care costs, paid this calendar quarter, as described in NRS 363B.115.

Line 2b. Enter deduction for qualified Veterans wages. Attach employee verification of Unemployment Benefits and signed affidavit that employee meets the requirements pursuant to AB71 of the 78th (2015) legislative session.

Line 3. Net taxable wages. Add Line 2a and Line 2b. Subtract this sum from Line 1.

Line 4. Offsets carried forward are created when allowable health care costs exceed gross wages in the previous quarter. If applicable, enter the previous quarter's offset here. This is not a credit against any tax due. This reduces the wage base upon which the tax is calculated.

Line 5. Line 3 minus Line 4.

Line 6. Net taxable wages is the amount that will be used in the calculation of the tax. If line 5 is greater than zero, this is the taxable wages. If line 5 is less than zero, then no tax is due. (This amount will be entered on line 18 as the offset carried forward for the next quarter. The offset carried forward is only limited to the health care deduction. This excludes the deduction for veteran wages.)

Line 7. Enter the threshold of $50,000.00. SB483 set the threshold to $50,000.00 for quarterly wages. Tax is calculated on wages over this threshold. Line 8. Taxable wages. The threshold in Line 7 is subtracted from Line 5 to calculate taxable wages; do not enter an amount if less than 0.

Line 9. Calculated Tax. Multiply Line 8 x .01475, the rate established by SB483.

Line 10. Commerce Tax Credit – Enter 50% of the Commerce Tax paid in the prior tax year up to the amount of MBT tax owed. Do not enter an amount less than zero. If the credit amount is higher than the MBT tax owed it may be carried forward up to the fourth quarter immediately following the end of the Commerce Tax year for which Commerce Tax is paid.

Line 11. Other Credits - Enter amount of overpayment of Modified Business Tax (MBT) made in prior reporting periods for which you have received a Department of Taxation credit notice. Credit notices received from the Department are not cumulative. Do not take the credit if you have applied for a refund. NOTE: Only credits established by the Department may be used. The 78th (2015) legislative session enacted several Bills that created credits towards the MBT that may be taken on this tax return if qualified. These credits except for the college savings plan contributions require prior approval by the Department and a credit notice. Please attach credit notice and/or College Savings Plan Contributions Form to this return.

Line 12. Net Tax Due - Line 9 minus Line 10. This amount is due and payable by the due date; the last day of the month following the applicable quarter. If payment of the tax is late, penalty and interest (as calculated below) are applicable.

Line 13. Penalty - If this return will not be submitted/postmarked and the taxes paid on or before the due date as shown on the face of this return, the amount of penalty due is based on the number of days late payment is made per NAC 360.395. Determine the number of days the payments is late and multiply the net tax owed by the appropriate rate based on the table below. The result is the amount of penalty that should be entered. For example, if the taxes were due January 31, but not paid until February 15. The number of days late is 15 so the penalty is 4%. The maximum penalty amount is 10%.

|

Number of days late |

Penalty Percentage |

Multiply By |

|

|||

|

|

|

|

|

2% |

0.02 |

|

4% |

0.04 |

||

|

16 - 20 |

6% |

0.06 |

21- 30 |

8% |

0.08 |

|

|

31 + |

10% |

0.1 |

Line 14. Interest: To calculate interest for each month late, multiply Line 11 x 0.75% (or .0075).

Line 15. Previous Debits - Enter only those liabilities that have been established for prior quarters by the Department and for which you have received a liability notice.

Line 16. Total Amount Due

Line 18. Carry Forward - If line 5 is less than zero enter figure here. This amount will be carried forward to the next quarter (offset)

GENERAL INFORMATION:

GENERAL BUSINESSES MUST USE FORM

Who Must File: Every employer who is subject to the Nevada Unemployment Compensation Law (NRS 612) except for

Businesses that have ceased doing business (gone out of business) in Nevada must notify the Employment Security Division and the Department of Taxation in writing, the date the business ceased doing business. The Department will send written notice when a credit request has been processed and the credit is available for use/refund.

Please do not use/apply a credit prior to receiving Departmental notification that it is available.

** For up to date information on tax issues, be sure to check our website

| Fact Name | Description |

|---|---|

| Governing Law | The Modified Business Tax is governed by Nevada Revised Statutes (NRS) 363B.115 and NRS 612. |

| Filing Frequency | Employers must file the Modified Business Tax return quarterly. |

| Threshold Amount | The tax applies only to wages exceeding $50,000 per quarter, as established by SB483. |

| Tax Rate | The tax rate is set at 1.475% of taxable wages, as per SB483. |

| Penalties for Late Filing | If the return is filed late, penalties range from 2% to 10%, depending on how many days late it is. |

| Who Must File | All employers subject to the Nevada Unemployment Compensation Law must file, excluding certain organizations. |

Completing the Modified Business Tax form is a straightforward process, but attention to detail is crucial. Follow these steps carefully to ensure accurate reporting and compliance with tax obligations.

Once you have completed the form, ensure that you either mail the original to the Nevada Department of Taxation or email it as an attachment. It is essential to keep a copy for your records. Timely submission will help avoid any penalties or interest charges.

The Modified Business Tax (MBT) form is a tax return that businesses in Nevada must file quarterly. It is primarily used to report and calculate taxes owed based on the total gross wages paid to employees. The form includes deductions for health benefits and qualified veterans' wages, which can reduce the taxable amount. It is essential for businesses that fall under the Nevada Unemployment Compensation Law to ensure compliance with this requirement.

Every employer subject to the Nevada Unemployment Compensation Law must file the MBT form. This includes most businesses, except for non-profit organizations recognized under section 501(c), Indian tribes, and political subdivisions. If your business has ceased operations in Nevada, you must notify both the Employment Security Division and the Department of Taxation in writing.

To calculate your taxable wages, follow these steps:

If you fail to file the MBT form or pay the tax by the due date, penalties and interest may apply. The penalty amount depends on how many days late the payment is made, with rates ranging from 2% to a maximum of 10%. Interest is calculated at a rate of 0.75% for each month the payment is late. It is crucial to be aware of these penalties to avoid additional costs.

Two primary deductions can be claimed on the MBT form:

These deductions can significantly reduce your taxable wages, so it is important to keep accurate records and submit the required documentation.

The MBT form can be submitted either by mail or email. If mailing, send the original form to the Nevada Department of Taxation at the address provided on the form. If you choose to email, save the completed form and send it as an attachment to [email protected] with the subject line 'Modified Business Tax Return'. Ensure that your submission is made by the due date to avoid penalties.

If you have previous debits or outstanding liabilities, you must report these on the MBT form. Enter the total amount of these liabilities in the designated section. This amount will be added to your total amount due, so it is essential to keep track of any past obligations to avoid confusion and ensure accurate reporting.

For the latest information on tax issues, including changes that may affect the MBT, it is advisable to check the Nevada Department of Taxation's website regularly. They publish updates every January, April, July, and October. Staying informed can help you meet your tax obligations and take advantage of any new credits or deductions that may become available.

Filling out the Modified Business Tax form can be challenging. Many individuals make common mistakes that can lead to errors in reporting and potential penalties. One frequent error is failing to accurately report the total gross wages on Line 1. This figure should include all wages and reported tips for the quarter. Omitting any amounts can result in an incorrect tax calculation.

Another mistake involves the deductions on Lines 2a and 2b. Some filers neglect to include deductions for paid health insurance or qualified veterans wages. It's crucial to enter these deductions accurately to ensure the taxable wages are calculated correctly. Miscalculating these deductions can lead to an inflated tax liability.

Many people also overlook the importance of Line 4, where they must enter any offsets carried forward from the previous quarter. If this line is left blank or filled incorrectly, it can drastically affect the calculation of taxable wages on Line 5. This oversight may lead to overpayment or underpayment of taxes.

Line 7 requires filers to enter the threshold of $50,000. Some individuals mistakenly enter a different amount or forget this step altogether. This error can skew the calculation of taxable wages on Line 8, resulting in inaccurate tax obligations.

When calculating the tax on Line 9, it is essential to multiply the correct amount from Line 8 by the established rate. Errors in this multiplication can lead to significant discrepancies in the total tax due. Moreover, some filers may not take into account the Commerce Tax Credit on Line 10, which can reduce the overall tax liability if applicable.

Another common mistake is in the calculation of penalties and interest on Lines 13 and 14. Filers sometimes miscalculate these amounts, either by failing to apply the correct percentage or by not accounting for the number of days late. This can lead to unexpected charges and complications.

Line 16, which totals the amount due, is often filled out incorrectly due to errors in previous lines. It is vital to double-check all calculations to ensure accuracy before submitting the form. Any discrepancies here can result in payment issues.

Additionally, some individuals forget to sign the form before submission. A missing signature can delay processing and lead to additional penalties. Finally, failing to keep copies of the submitted form and any accompanying documentation can create challenges if questions arise later.

By being aware of these common mistakes, filers can take steps to ensure their Modified Business Tax form is completed accurately and submitted on time. Proper attention to detail can help avoid unnecessary complications and financial penalties.

The Modified Business Tax form is a crucial document for businesses operating in Nevada. However, it often accompanies several other forms and documents that provide additional information or fulfill specific requirements. Understanding these related documents can help ensure compliance and streamline the filing process.

Being aware of these forms and documents can significantly ease the filing process for the Modified Business Tax. Each plays a role in ensuring that businesses remain compliant with state regulations while maximizing potential credits and deductions.

When filling out the Modified Business Tax form, it is essential to follow certain guidelines to ensure accuracy and compliance. Here are four things you should and shouldn't do:

Understanding the Modified Business Tax (MBT) form can be challenging due to common misconceptions. Here are nine prevalent misunderstandings along with clarifications:

Clarifying these misconceptions can help ensure compliance and reduce errors when filing the Modified Business Tax form.

Filling out the Modified Business Tax form can be a straightforward process if you understand the key components. Here are some important takeaways to consider:

By keeping these points in mind, you can navigate the Modified Business Tax form more effectively and ensure compliance with Nevada tax regulations.