Creating a monthly budget can be a crucial step toward achieving financial stability. The Monthly Budget Worksheet is a practical tool designed to help you track your income and expenses effectively. By using this worksheet for two or three consecutive months, you can gain valuable insights into your spending habits. The form is organized into various categories, including income, housing, utilities, health and medical expenses, transportation, and more. Each category allows you to estimate your monthly budget alongside your actual spending, helping you identify discrepancies and areas for improvement. Additionally, the worksheet includes notes on expenses that may not occur monthly, encouraging you to set aside funds for those occasional bills. If you find yourself struggling to meet your financial obligations, the worksheet also provides resources for seeking assistance, such as contacting a HUD-certified housing counselor. With this comprehensive approach, the Monthly Budget Worksheet empowers you to take control of your finances and work toward a more secure future.

Monthly Budget Worksheet

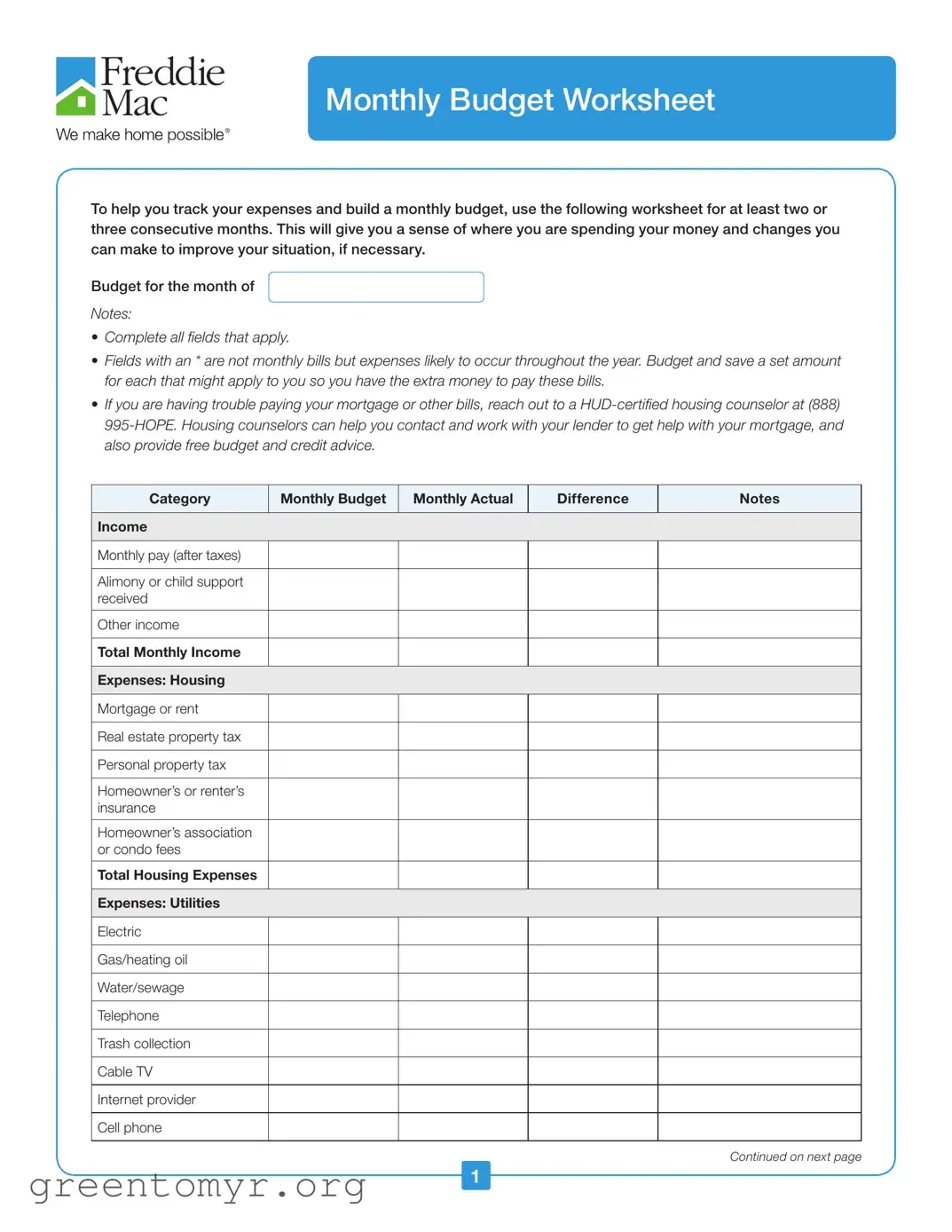

To help you track your expenses and build a monthly budget, use the following worksheet for at least two or three consecutive months. This will give you a sense of where you are spending your money and changes you can make to improve your situation, if necessary.

Budget for the month of

NOTES:

•Complete all ields that apply.

•Fields with an * are not monthly bills but expenses likely to occur throughout the year. Budget and save a set amount for each that might apply to you so you have the extra money to pay these bills.

•If you are having trouble paying your mortgage or other bills, reach out to a

Category

Monthly Budget

Monthly Actual

Difference

Notes

Income

Monthly pay (after taxes)

Alimony or child support received

Other income

Total Monthly Income

Expenses: Housing

Mortgage or rent

Real estate property tax

Personal property tax

Homeowner’s or renter’s insurance

Homeowner’s association or condo fees

Total Housing Expenses

Expenses: Utilities

Electric

Gas/heating oil

Water/sewage

Telephone

Trash collection

Cable TV

Internet provider

Cell phone

Continued on next page

1

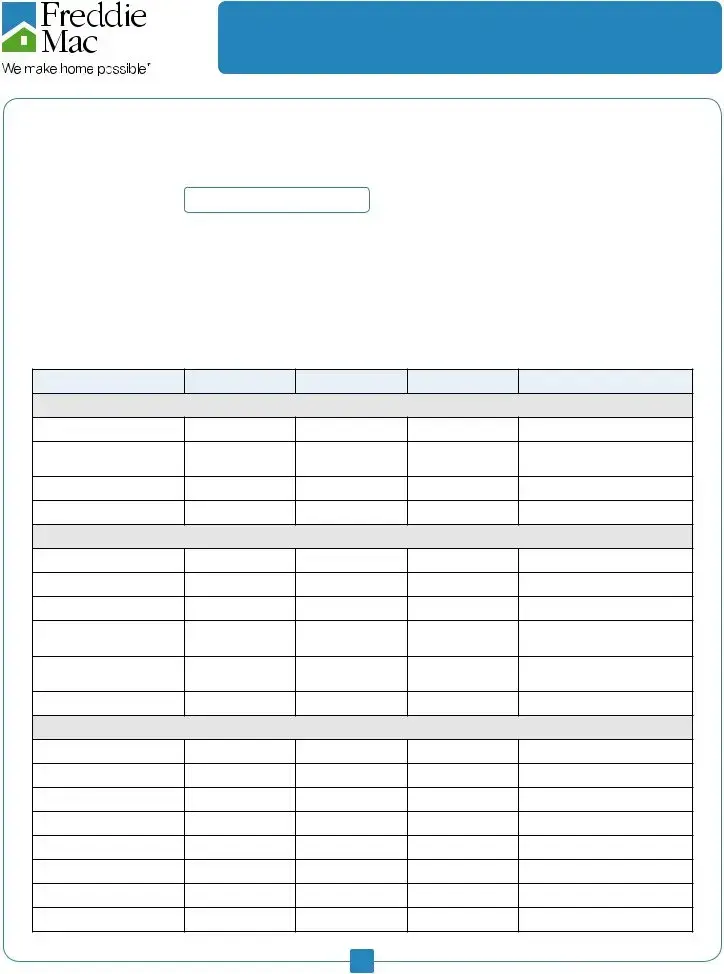

Monthly Budget Worksheet

Category

Monthly Budget

Monthly Actual

Difference

Notes

Expenses: Health/Medical

*Expenses that you can budget for, so you have money saved to pay for unplanned or annual bills.

Medical insurance

Dental insurance

Doctor/lab*

Dentist*

Orthodontist*

Therapist*

Eyeglasses/ophthalmolo-

Hospital/emergency*

Medicines*

Other

Total Health/Medical

Expenses

Expenses: Transportation

*Expenses you can budget for, so you have money saved to pay for unplanned or annual bills.

Car payments

Car insurance

Car maintenance/repair*

Mass transit costs

Gas

Parking/tolls

Tags/inspection*

Total Transportation

Expenses

Expenses: Credit Cards, Loans, OE

*Expenses you can budget for, so you have money saved to pay for unplanned or annual bills.

Credit Card:

Balance:

Credit Card:

Balance:

Credit Card:

Balance:

Student Loans

Legal Fees

Alimony/child support paid

Total Credit Card/Loan/

Other Balances and Fees

Continued on next page

2

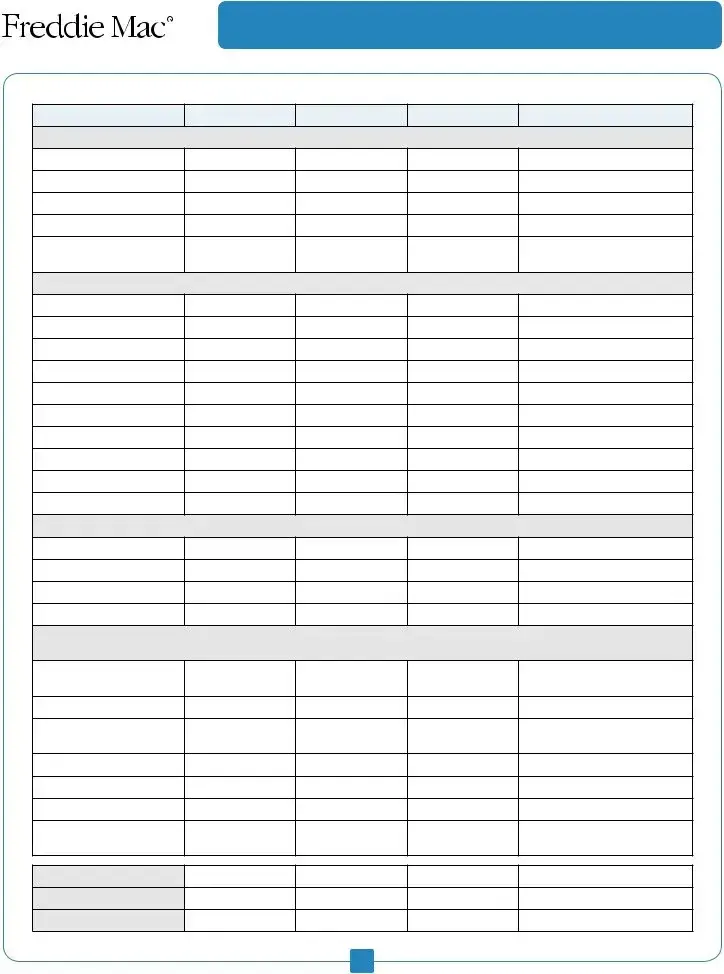

Monthly Budget Worksheet

Category

Monthly Budget

Monthly Actual

Difference

Notes

Expenses: Food and Entertainment

Groceries

Meals out

Entertainment (movies, etc.)

Hobbies

Total Food and

Entertainment

Expenses: Children

Child care

School tuition

Lunch money

School supplies

Lessons/sports

New clothing

Personal grooming

Allowances

Other

Total Children Expenses

Expenses: Personal

Dry cleaning/laundry

Personal grooming

New clothing

Total Personal Expenses

Expenses: Savings/Large Expenses

*Expenses you can budget for, so you have money saved to pay for unplanned or annual bills.

Savings amount going into an account each month

Gifts (holiday, birthday)*

House maintenance/ repairs*

Furniture*

Church/charity*

Vacation*

Total Savings/Large

Expenses

Total Monthly Income

Total Monthly Expenses

Difference

3

| Fact Name | Details |

|---|---|

| Purpose | The Monthly Budget Worksheet is designed to help individuals track their expenses and create a monthly budget over a period of two to three months. |

| Categories | The worksheet includes various categories such as income, housing, utilities, health/medical, transportation, credit cards/loans, food and entertainment, children, personal expenses, and savings/large expenses. |

| Annual Expenses | Certain fields marked with an asterisk (*) represent expenses that are not monthly bills but rather costs that may occur throughout the year, encouraging users to budget for these in advance. |

| Assistance Resources | The worksheet advises individuals facing difficulties with mortgage or other bills to contact a HUD-certified housing counselor for assistance and guidance. |

| State-Specific Laws | In some states, budgeting practices may be influenced by local laws regarding financial planning and consumer protection. For example, California's Financial Literacy Education Act promotes budgeting education. |

Filling out the Monthly Budget Worksheet is a straightforward process that will help you gain insight into your financial situation. By carefully recording your income and expenses, you can identify areas for improvement and make informed decisions about your finances. Follow these steps to complete the form effectively.

The Monthly Budget Worksheet is designed to help you track your expenses and manage your finances effectively. By using this worksheet for at least two or three consecutive months, you can gain insight into your spending habits and identify areas for improvement. It encourages you to be proactive in budgeting and saving, ultimately leading to better financial stability.

To fill out the worksheet, complete all applicable fields. Start by listing your income sources, including your monthly pay, alimony, or any other income. Next, categorize your expenses into housing, utilities, health/medical, transportation, credit cards/loans, food and entertainment, children, personal expenses, and savings. Make sure to include both monthly bills and expenses that may occur throughout the year, such as medical insurance or car maintenance. Fields marked with an asterisk (*) indicate expenses you can plan for, so budget accordingly.

If you find yourself struggling to pay your mortgage or other bills, it’s important to seek help. Contact a HUD-certified housing counselor at (888) 995-HOPE. These counselors can assist you in communicating with your lender and exploring options for mortgage relief. They also provide free budget and credit advice to help you manage your finances better.

Tracking both your budgeted and actual expenses allows you to see where your money is going. By comparing the two, you can identify discrepancies and understand your spending patterns. This practice helps you adjust your budget as needed and can reveal areas where you may need to cut back or save more effectively.

The worksheet includes a section for savings and large expenses. You can allocate a specific amount each month for anticipated costs, such as home repairs, vacations, or gifts. By budgeting for these expenses in advance, you can avoid financial strain when they arise. Regular contributions to a savings account will help you build a safety net for these larger financial commitments.

Yes, the Monthly Budget Worksheet can be adapted for irregular income. If your income fluctuates, estimate your average monthly income based on past earnings. Use this figure to create your budget. Remember to account for any months when your income may be lower, and consider setting aside funds during higher-earning months to cover leaner times.

If you have expenses that are not explicitly listed on the worksheet, feel free to add them in the notes section or create additional categories. The goal is to capture all of your financial obligations accurately. Customizing the worksheet to fit your unique situation will provide you with a more comprehensive view of your finances.

Filling out the Monthly Budget Worksheet can be a helpful way to manage your finances, but many people make common mistakes that can hinder its effectiveness. One frequent error is not completing all applicable fields. Each category is designed to capture different aspects of your financial situation. When you leave out important information, you miss out on a complete picture of your income and expenses. This oversight can lead to inaccurate budgeting and unexpected shortfalls.

Another mistake is failing to differentiate between fixed and variable expenses. Fixed expenses, like rent or mortgage payments, remain constant each month. In contrast, variable expenses, such as groceries or entertainment, can fluctuate. By not clearly identifying these categories, you may underestimate your monthly spending. This can create a false sense of security, making it easy to overspend in areas where you should be more cautious.

Some individuals also neglect to budget for irregular expenses. The worksheet includes fields for expenses that may not occur every month, such as car maintenance or medical bills. If you don’t allocate funds for these costs, you may find yourself unprepared when they arise. It’s essential to set aside a specific amount each month to cover these expenses, ensuring you have the necessary funds when the time comes.

Lastly, many people forget to review their actual spending against their budget. After filling out the worksheet, it’s important to track your actual expenses and compare them to your budgeted amounts. This practice can highlight areas where you may need to adjust your spending habits. Regularly reviewing your budget helps you stay accountable and make informed financial decisions moving forward.

The Monthly Budget Worksheet is a vital tool for managing finances effectively. However, it is often used in conjunction with other important documents that can provide a more comprehensive view of one’s financial situation. Below is a list of five additional forms and documents that can enhance your budgeting process.

Utilizing these documents alongside the Monthly Budget Worksheet can lead to better financial management. By keeping track of expenses, income, debts, savings, and goals, individuals can make informed decisions that improve their overall financial health.

The Monthly Budget Worksheet form is a useful tool for tracking expenses and planning finances. Several other documents serve similar purposes, helping individuals manage their budgets and financial situations effectively. Below is a list of seven documents that share similarities with the Monthly Budget Worksheet.

When filling out the Monthly Budget Worksheet, it’s important to approach the task with care. Here are five things you should and shouldn’t do to ensure accurate and effective budgeting.

Here are nine common misconceptions about the Monthly Budget Worksheet form:

Understanding these misconceptions can help you make the most of the Monthly Budget Worksheet and improve your financial health.

Using the Monthly Budget Worksheet can significantly enhance your financial awareness and planning. Here are key takeaways to keep in mind: