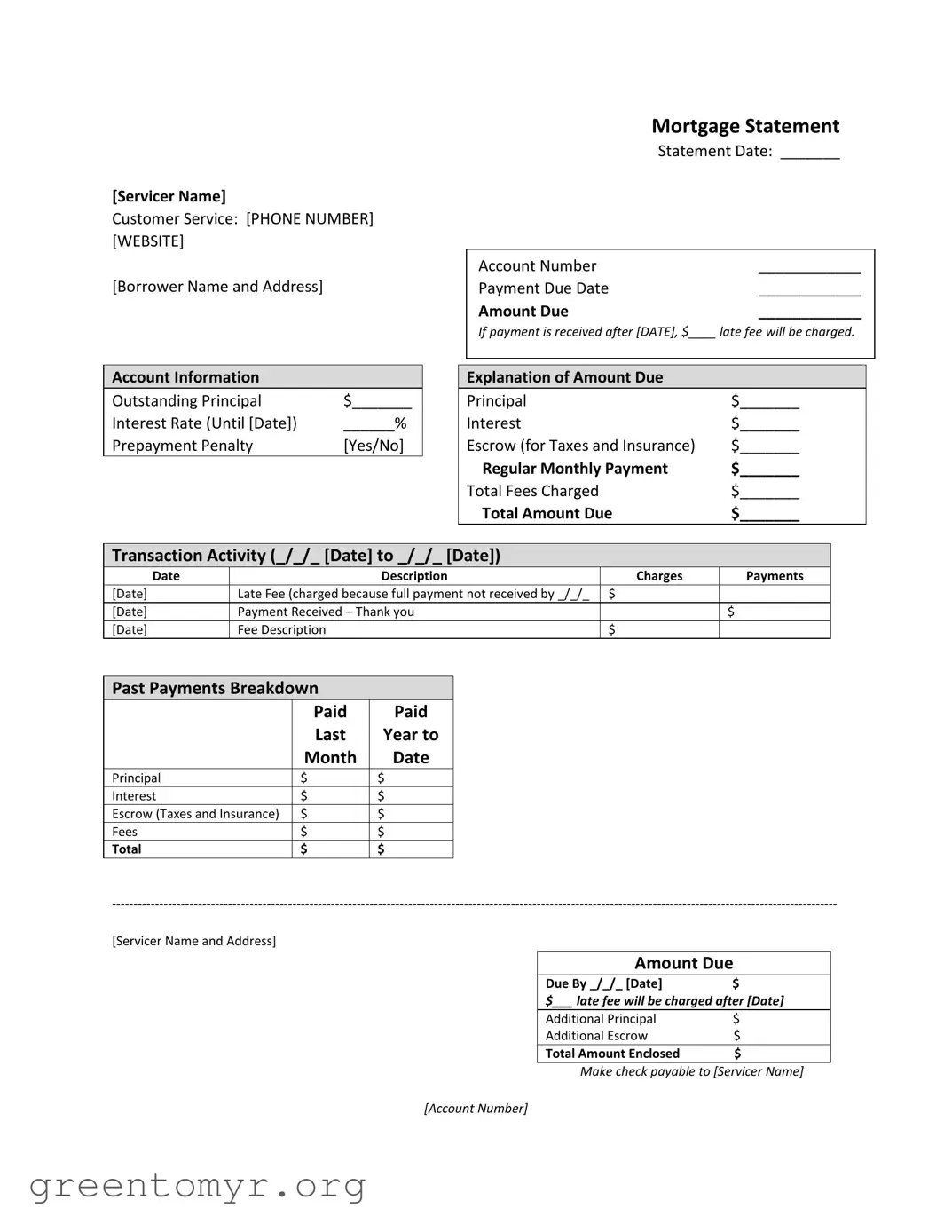

Understanding your mortgage statement is crucial for maintaining your financial health and ensuring timely payments. This document, issued by your mortgage servicer, provides a comprehensive overview of your account status, including the outstanding principal balance, interest rate, and any late fees that may apply if payments are not made on time. Key details such as your account number, payment due date, and the total amount due are prominently displayed, allowing you to quickly assess your obligations. The statement also breaks down the amount due into principal, interest, and escrow for taxes and insurance, giving you clarity on how your payments are allocated. Additionally, transaction activity over a specified period shows recent charges and payments, helping you track your payment history. Important messages regarding partial payments and potential delinquency serve as reminders of the consequences of missed payments, including fees and the risk of foreclosure. If you find yourself facing financial difficulties, the statement provides resources for mortgage counseling, emphasizing the importance of seeking help early to avoid further complications.

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.

| Fact Name | Description |

|---|---|

| Servicer Information | The mortgage statement includes the servicer's name, customer service phone number, and website for borrower inquiries. |

| Payment Details | It specifies the payment due date, amount due, and potential late fees if the payment is not received by the stated date. |

| Account Information | The statement provides a breakdown of the outstanding principal, interest rate, and whether a prepayment penalty applies. |

| Transaction Activity | A section details recent transaction activity, including charges, payments, and any late fees incurred. |

| Delinquency Notice | The statement includes a notice if the borrower is late on payments, outlining the consequences of continued delinquency. |

| Financial Assistance | Information about mortgage counseling or assistance is provided for borrowers experiencing financial difficulty. |

Filling out the Mortgage Statement form requires attention to detail. After completing the form, you will have a clear overview of your mortgage account, including amounts due and payment history. This information is essential for managing your mortgage effectively.

A Mortgage Statement is a document provided by your mortgage servicer that outlines your mortgage account details. It includes information such as your outstanding principal balance, interest rate, payment due date, and any fees that may apply. This statement helps you keep track of your payments and understand your financial obligations.

Your Mortgage Statement typically contains the following key information:

This information helps you stay informed about your mortgage status and any payments you need to make.

If you miss a payment, a late fee may be charged. Your Mortgage Statement will specify the amount of the late fee and the date by which your payment must be received to avoid this fee. Consistent late payments can lead to serious consequences, including potential foreclosure.

A prepayment penalty is a fee that some lenders charge if you pay off your mortgage early. This penalty is designed to protect the lender's expected interest income. Your Mortgage Statement will indicate whether a prepayment penalty applies to your loan.

Partial payments are amounts that are less than your total monthly payment. If you make a partial payment, it will not be applied directly to your mortgage. Instead, it is held in a suspense account until you pay the remaining balance. Once the full amount is paid, it will be applied to your mortgage account.

If you are facing financial difficulties, it is crucial to reach out to your mortgage servicer as soon as possible. They can provide information about mortgage counseling or assistance programs that may help you manage your payments and avoid foreclosure.

Your Mortgage Statement includes contact information for your servicer, including a phone number and website. It is advisable to reach out to them directly with any questions or concerns regarding your mortgage account.

Mortgage Statements are typically sent monthly. However, the frequency may vary depending on your lender's policies. Always check your statement for the date it was issued and any specific instructions regarding payments.

Filling out a Mortgage Statement form can be a complex process. Many individuals make common mistakes that can lead to delays or complications. Understanding these mistakes can help ensure the form is completed correctly.

One frequent error is failing to provide accurate personal information. The borrower's name and address must be correct and match the information on file with the mortgage servicer. Any discrepancies can result in confusion or miscommunication regarding the account.

Another mistake involves overlooking the payment due date. It is essential to pay attention to this date to avoid late fees. If a payment is made after the specified due date, a late fee will be charged. Many borrowers do not realize how significant these fees can become over time.

Inaccurate account numbers are also a common issue. The account number must be filled out precisely as it appears on previous statements. A simple typographical error can lead to payments being misapplied or not processed at all.

Some individuals neglect to review the transaction activity section. This section provides a history of payments and charges. Understanding this information is crucial for tracking past payments and ensuring that all transactions are accounted for correctly.

Additionally, borrowers often fail to check the amount due section carefully. It is important to confirm that the total amount reflects all necessary charges, including principal, interest, and any applicable fees. Miscalculating the total can lead to underpayment and further complications.

Lastly, many people do not pay attention to the delinquency notice included in the statement. This notice provides critical information about the status of the mortgage and the potential consequences of late payments. Ignoring this section can result in severe repercussions, including foreclosure.

By avoiding these common mistakes, individuals can ensure that their Mortgage Statement form is completed accurately and efficiently. This attention to detail is essential for maintaining a healthy mortgage account.

When managing a mortgage, several important documents complement the Mortgage Statement form. Each of these documents plays a vital role in understanding your mortgage obligations and financial standing. Below is a list of commonly used forms that you may encounter.

Understanding these documents is essential for effective mortgage management. Each form provides valuable insights into your financial responsibilities and rights as a borrower. By staying informed, you can make better decisions regarding your mortgage and ensure you remain on track with your payments.

The Mortgage Statement form is a crucial document for homeowners, providing an overview of their mortgage account. It shares similarities with several other important documents in the realm of home financing. Here’s a list of nine documents that are similar to the Mortgage Statement form, along with explanations of how they relate:

Understanding these documents can empower homeowners to manage their mortgage effectively. Stay informed, and take action promptly to ensure your financial health and home security.

When filling out the Mortgage Statement form, follow these guidelines to ensure accuracy and clarity.

By following these steps, you can help ensure a smooth process with your mortgage servicer.

This is not entirely accurate. While the statement prominently displays the amount due, it also provides a detailed breakdown of various components such as principal, interest, and escrow for taxes and insurance. This breakdown helps borrowers understand how their payments are allocated.

Many borrowers believe that any payment made is instantly applied to their mortgage. However, the statement clarifies that partial payments are held in a suspense account until the full amount is received. This means that only when the total due is paid will the funds be applied to the mortgage.

While it is true that late fees can be charged, the statement provides a clear warning about when these fees will apply. Borrowers are informed of the specific date by which payment must be received to avoid incurring additional charges.

This is a common assumption, but the mortgage statement indicates that the interest rate may change. It specifies that the rate is applicable until a certain date, after which it may adjust. Borrowers should be aware of the terms of their loan agreement regarding interest rate adjustments.

Some borrowers think that all possible fees are included in the statement. However, it typically lists only the fees that are current or applicable. Additional fees may arise based on individual circumstances, and borrowers should refer to their loan agreement for a comprehensive understanding.

Many people believe that they only need to pay attention to the mortgage statement if they are behind on payments. In reality, regular review of the statement is essential. It provides valuable information about payment history and outstanding balances, helping borrowers stay informed about their mortgage status.

Some borrowers may overlook the resources available for those experiencing financial difficulties. The statement often includes information about mortgage counseling or assistance programs. This can be a crucial resource for borrowers who may need help managing their payments.

When filling out and using the Mortgage Statement form, there are several important points to keep in mind:

By keeping these takeaways in mind, you can navigate your mortgage statement with confidence and ensure timely payments.