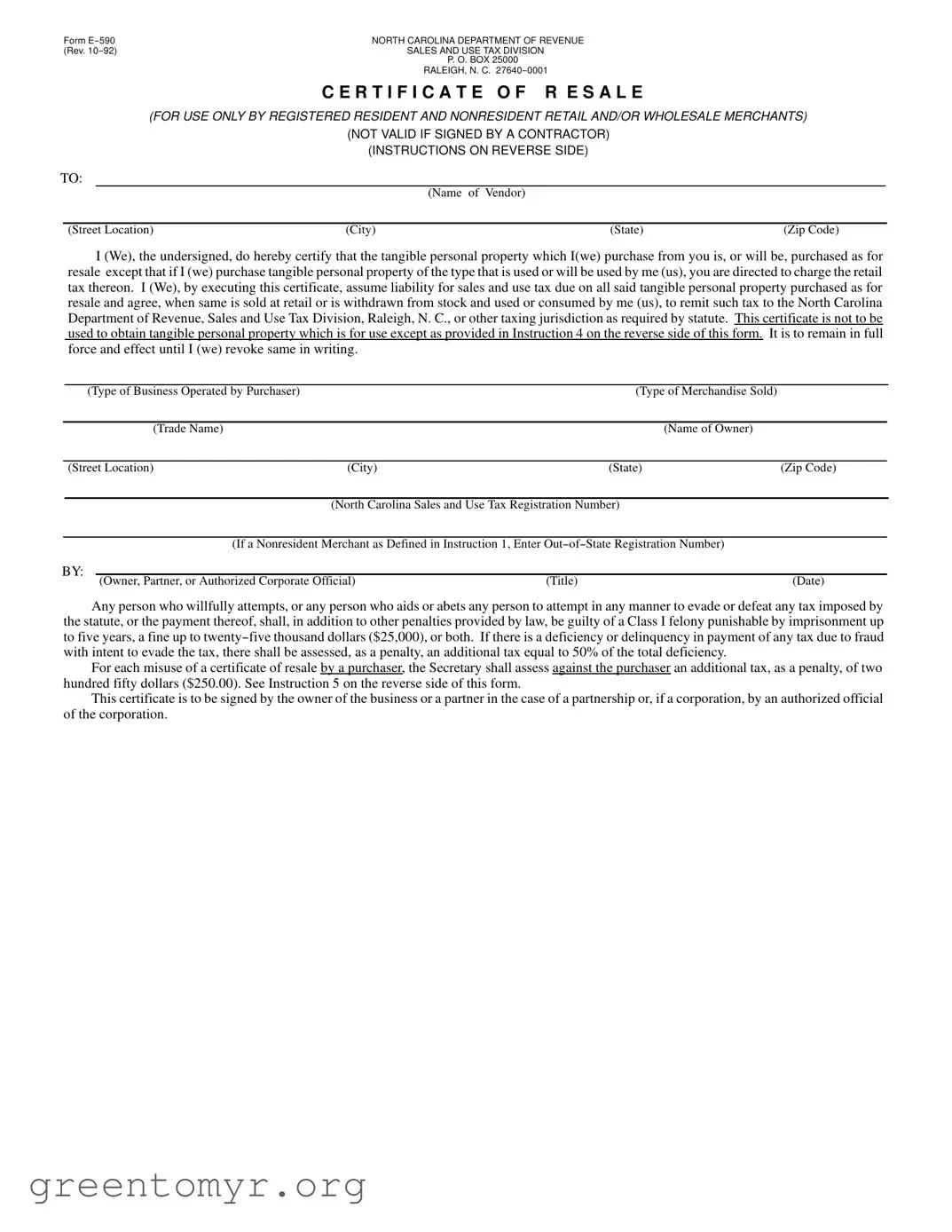

The North Carolina Certificate of Resale, known as FORM E-590, serves a critical function for both resident and nonresident retail and wholesale merchants. This form allows businesses to purchase tangible personal property without paying sales tax, provided the items are intended for resale. However, it is important to note that this certificate cannot be used by contractors, as they are considered the end users of the materials they purchase. To complete the form, merchants must provide essential information such as their business name, type of merchandise sold, and their North Carolina Sales and Use Tax Registration Number. The certificate must be signed by an authorized individual, ensuring accountability for any tax liabilities that may arise from the resale of the purchased goods. Additionally, merchants are responsible for maintaining accurate records of the certificate and understanding the limitations on its use, particularly regarding items that may be consumed rather than resold. Misuse of the certificate can lead to significant penalties, including fines and potential criminal charges. Understanding the nuances of the Certificate of Resale is vital for merchants to navigate their tax responsibilities effectively.

| Fact Name | Description | Governing Law |

|---|---|---|

| Eligibility | This form is for registered resident and nonresident retail and wholesale merchants only. | North Carolina Sales and Use Tax Law |

| Liability | The purchaser assumes liability for sales and use tax on all tangible personal property purchased for resale. | North Carolina General Statutes § 105-164.4 |

| Validity | The certificate is invalid if signed by a contractor, as they are considered users of the property. | North Carolina Sales and Use Tax Administrative Rules |

| Record Keeping | Merchants must keep a copy of the executed certificate in their records for verification purposes. | North Carolina Sales and Use Tax Administrative Rules |

Filling out the North Carolina Certificate of Resale form is an important step for registered merchants who wish to purchase tangible personal property for resale. Once you have completed the form, it will serve as a declaration that the items you buy are intended for resale, and it will help you avoid paying sales tax at the time of purchase. Make sure all information is accurate and complete to ensure compliance with state regulations.

After completing the form, make sure to keep a copy for your records. This will help you maintain compliance and provide documentation if needed in the future. If there are any changes in your business ownership or if you need to revoke the certificate, be sure to follow the proper procedures as outlined in the instructions.

The North Carolina Certificate of Resale is a document that allows registered retail and wholesale merchants to purchase tangible personal property without paying sales tax, as long as the property is intended for resale. This certificate is specifically designed for merchants who are either residents or nonresidents of North Carolina and must be filled out correctly to be valid.

This certificate can only be used by registered resident and nonresident retail and wholesale merchants. Nonresident merchants are those who do not have a physical business location in North Carolina but are registered for sales tax purposes in another state. It is important to note that this certificate is not valid if signed by a contractor, as contractors are considered users or consumers of the property they purchase.

To complete the certificate, the merchant must provide specific information, including:

Each of these details is essential for the certificate to be valid and effective.

By using the Certificate of Resale, the purchaser assumes liability for any sales and use tax due on the property purchased. This means that if the property is not resold and is instead used or consumed, the purchaser must remit the appropriate tax to the North Carolina Department of Revenue. Failure to do so may result in penalties.

Merchants making frequent purchases for resale can present one certificate to their suppliers, which will cover multiple transactions. However, for occasional or infrequent purchases, it is advisable to provide a copy of the certificate with each purchase order. This practice ensures that suppliers have the necessary documentation for tax exemption.

If a purchaser misuses the Certificate of Resale, they may face significant penalties. Each misuse can result in an additional tax penalty of $250. Moreover, if the misuse is deemed fraudulent, the purchaser could be subject to more severe penalties, including fines and potential imprisonment.

If there is a change in ownership of a business for which a Certificate of Resale is on file, the vendor must obtain a corrected certificate. This ensures that the new ownership is properly documented and compliant with sales tax regulations. Vendors can verify changes in ownership with the North Carolina Department of Revenue.

Filling out the North Carolina Certificate of Resale form can be straightforward, but several common mistakes can lead to issues. One frequent error is neglecting to include the North Carolina Sales and Use Tax Registration Number. This number is essential for validating the purchaser's registration status. Without it, the certificate may be considered invalid.

Another common mistake involves the signature. The form must be signed by the owner, a partner, or an authorized corporate official. If the signature is missing or does not match the name of the person listed as the purchaser, the certificate may be rejected. Ensuring that the correct individual signs the document is crucial.

Many people also fail to specify the type of business operated and the type of merchandise sold. This information is necessary to demonstrate the nature of the business and the items being purchased for resale. Omitting these details can lead to confusion and potential penalties.

Another mistake is using the certificate for items that are not intended for resale. The form is strictly for tangible personal property purchased for resale. If a purchaser uses the certificate to buy items for personal use, they may face tax liabilities. It is important to understand the limitations of the certificate.

Some individuals may not keep a copy of the executed certificate in their records, which is required by law. This oversight can create problems if the North Carolina Department of Revenue requests proof of the certificate's validity. Maintaining accurate records is a vital part of compliance.

Additionally, failing to update the certificate after a change in ownership can lead to issues. If the business changes ownership, a corrected certificate must be obtained. Not doing so can result in penalties and complications regarding tax responsibilities.

Lastly, individuals sometimes misunderstand the rules regarding nonresident merchants. Nonresident merchants must provide their out-of-state registration number on the form. Failure to include this information can lead to the rejection of the certificate. Understanding the requirements for nonresident status is essential for compliance.

The North Carolina Certificate of Resale form is an important document for merchants who purchase tangible personal property for resale. However, several other forms and documents are often used in conjunction with this certificate to ensure compliance with state tax laws. Below is a list of these related documents, each serving a specific purpose in the resale process.

Understanding these documents and their purposes can help businesses navigate the complexities of sales tax compliance in North Carolina. Proper use of the Certificate of Resale and related forms is essential for maintaining good standing with the state tax authorities.

The North Carolina Certificate of Resale form is similar to several other documents used in business transactions, particularly in the context of sales tax and resale. Here are six documents that share similarities with the NC Certificate of Resale form:

When filling out the North Carolina Certificate of Resale form, it’s important to follow specific guidelines to ensure compliance with state regulations. Here are some key dos and don’ts to consider:

Following these guidelines will help ensure that your use of the Certificate of Resale is valid and compliant with North Carolina tax laws.

Understanding the North Carolina Certificate of Resale can be challenging. Here are ten common misconceptions about this form, along with clarifications to help you navigate its requirements.

It is crucial to understand these points to ensure compliance with North Carolina tax laws. If you have further questions or need assistance, consider reaching out to a tax professional.

Filling out and using the North Carolina Certificate of Resale form is an important process for businesses engaged in retail and wholesale activities. Here are key takeaways to consider:

Understanding these key points will help ensure compliance with North Carolina's sales and use tax regulations when using the Certificate of Resale form.