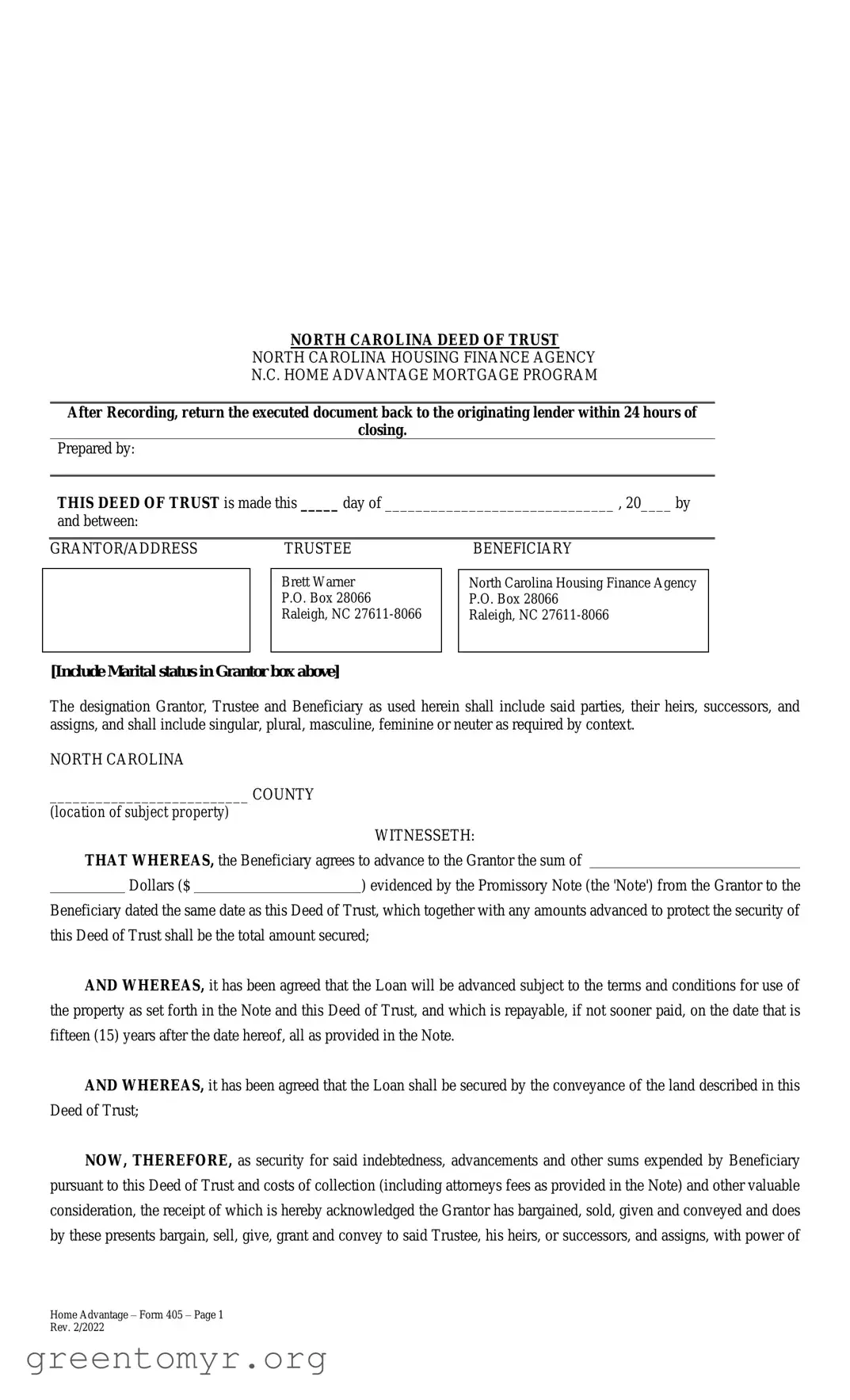

The North Carolina Deed of Trust is a crucial legal document that serves as a security instrument in real estate transactions, particularly for loans facilitated through the North Carolina Housing Finance Agency's Home Advantage Mortgage Program. This form outlines the relationship between three primary parties: the Grantor, who is the borrower; the Trustee, who holds the legal title to the property; and the Beneficiary, typically the lender, who is entitled to the repayment of the loan. The Deed of Trust specifies the terms under which the loan is secured, including the amount borrowed, the repayment schedule, and the conditions that must be met to avoid default. In the event of a default, the document grants the Trustee the authority to sell the property at public auction to recover the owed amount. Furthermore, it includes various covenants that the Grantor must adhere to, such as maintaining insurance on the property, paying taxes, and not committing waste. The Deed of Trust is designed to protect the interests of the Beneficiary while providing a clear framework for the rights and responsibilities of all parties involved. Understanding its components is essential for anyone participating in real estate financing in North Carolina.

| Fact Name | Details |

|---|---|

| Governing Law | This Deed of Trust is governed by the laws of the State of North Carolina. |

| Parties Involved | The Grantor, Trustee, and Beneficiary are the primary parties in this agreement, including their heirs and assigns. |

| Loan Duration | The loan is typically repayable in 15 years, as specified in the Deed of Trust. |

| Insurance Requirement | The Grantor must maintain insurance on the property for the benefit of the Beneficiary, covering specific risks. |

| Default Conditions | Defaults can occur due to non-payment or failure to comply with the terms outlined in the Deed of Trust. |

| Foreclosure Process | In case of default, the Trustee may sell the property at public auction after appropriate notice and legal proceedings. |

| Trustee's Commission | The Trustee is entitled to a commission of 5% of the gross proceeds from a completed foreclosure sale. |

| Property Transfer Restrictions | The Grantor cannot sell or transfer the property without the Beneficiary's prior written consent. |

After gathering all necessary information, the next step involves accurately filling out the North Carolina Deed of Trust form. This document is crucial for securing a loan with the property as collateral. Ensure that all details are correct and complete to avoid any potential issues during the closing process.

A North Carolina Deed of Trust is a legal document used in real estate transactions. It secures a loan by transferring the title of the property to a trustee, who holds it on behalf of the lender (beneficiary) until the borrower (grantor) repays the loan. This arrangement protects the lender's interest while allowing the borrower to retain use of the property.

There are three main parties involved:

If the borrower fails to make payments or violates the terms of the Deed of Trust, the trustee can initiate foreclosure proceedings. This process involves selling the property at public auction to recover the loan amount. The trustee must follow legal procedures, including providing notice and advertising the sale.

The typical repayment period for a loan secured by a Deed of Trust in North Carolina is 15 years. However, this period can vary based on the terms outlined in the Promissory Note associated with the Deed of Trust.

The borrower has several key responsibilities, including:

The borrower may sell the property, but they must obtain the lender's consent first. If the property is sold without permission, the lender may declare the entire loan amount due immediately. This restriction helps protect the lender's interest in the property.

The trustee acts as a neutral party who holds the title to the property on behalf of the lender. If the borrower defaults, the trustee is responsible for managing the foreclosure process, ensuring compliance with legal requirements, and distributing the proceeds from the sale of the property to the lender.

A Deed of Trust can impact the borrower's credit score. Timely payments can improve the borrower's credit, while defaults or foreclosures can significantly harm it. Maintaining good financial habits and adhering to the terms of the Deed of Trust is crucial for protecting one's credit standing.

Filling out the North Carolina Deed of Trust form requires careful attention to detail. One common mistake is failing to include the marital status of the Grantor in the designated box. This information is crucial as it can affect the legal standing of the document and the rights of the parties involved.

Another frequent error is leaving the amount of the loan blank. The form must specify the sum of money being advanced by the Beneficiary to the Grantor. Omitting this detail can lead to confusion and complications later in the process.

Many individuals neglect to provide the correct property description. The Deed of Trust must include a clear and accurate description of the property being secured. An incomplete or incorrect description can create legal issues and hinder the enforcement of the trust.

Inaccurate dates are also a common mistake. The date on which the Deed of Trust is executed should be filled in accurately. This date is essential for determining timelines related to payments and potential defaults.

Some people forget to sign the document in the presence of a notary public. A notary’s signature and seal are necessary to validate the document. Without this, the Deed of Trust may not be legally enforceable.

Another mistake involves failing to provide the trustee's information. The form requires the name and address of the trustee, who will manage the trust. Omitting this information can delay the process or render the document invalid.

Additionally, individuals often overlook the need to include exhibits or attachments if applicable. If there are exceptions to the title or other relevant documents, they should be referenced and attached to the Deed of Trust.

Lastly, some individuals do not keep a copy of the completed form for their records. It is important to retain a copy of the signed and notarized Deed of Trust for future reference, as it serves as a legal record of the agreement between the parties.

The North Carolina Deed of Trust is a crucial document in real estate transactions, particularly when it comes to securing a loan. However, it often accompanies several other forms and documents that play significant roles in the overall process. Understanding these additional documents can provide clarity and ensure that all parties are well-informed. Below is a list of commonly used forms and documents that often accompany the North Carolina Deed of Trust.

Each of these documents plays a vital role in the real estate transaction process, ensuring that both the lender's interests and the borrower's rights are protected. By understanding these forms, all parties involved can navigate the complexities of real estate transactions with greater confidence and clarity.

The North Carolina Deed of Trust form serves as a crucial document in real estate transactions, particularly in securing loans. It shares similarities with several other legal documents, each serving a unique purpose while maintaining fundamental characteristics of property and loan agreements. Below are seven documents that are similar to the Deed of Trust, along with explanations of how they relate to it.

Misconception 1: A Deed of Trust is the same as a mortgage.

While both serve as security for a loan, a Deed of Trust involves three parties: the borrower (Grantor), the lender (Beneficiary), and a third party (Trustee). In contrast, a mortgage only involves two parties: the borrower and the lender.

Misconception 2: The Grantor loses all rights to the property.

This is not true. The Grantor retains ownership of the property and can live in it as long as they meet the terms of the Deed of Trust. Only if they default on the loan can the Trustee sell the property.

Misconception 3: A Deed of Trust is only used for residential properties.

A Deed of Trust can be used for both residential and commercial properties. Its flexibility makes it a common choice for various types of real estate transactions.

Misconception 4: Once signed, a Deed of Trust cannot be changed.

In fact, modifications can be made if all parties agree. Changes must be documented and may require additional legal steps, but they are possible.

Misconception 5: The Trustee has no responsibilities.

This is incorrect. The Trustee has specific duties, including managing the Deed of Trust and overseeing the foreclosure process if necessary. They act in the best interest of the Beneficiary while ensuring the Grantor's rights are respected.

Filling out and using the North Carolina Deed of Trust form requires careful attention to detail. Below are key takeaways to consider:

These points highlight the importance of understanding the responsibilities and implications of the Deed of Trust. Proper execution ensures the protection of all parties involved.