In the realm of personal and business finance, a Promissory Note serves as a vital tool for establishing clear agreements between parties regarding the repayment of borrowed money. In New Hampshire, this legally binding document outlines the terms of the loan, including the principal amount, interest rate, payment schedule, and any applicable late fees. By clearly defining the obligations of both the borrower and the lender, the New Hampshire Promissory Note form helps to prevent misunderstandings and disputes down the line. Additionally, it may include provisions for default, which detail the actions that can be taken if the borrower fails to meet their repayment obligations. Understanding the nuances of this form is essential for anyone looking to engage in a loan agreement, whether for personal use or business purposes. With its straightforward structure, the New Hampshire Promissory Note not only facilitates trust between the parties involved but also provides a legal framework that can be referenced in case of any disagreements.

New Hampshire Promissory Note Template

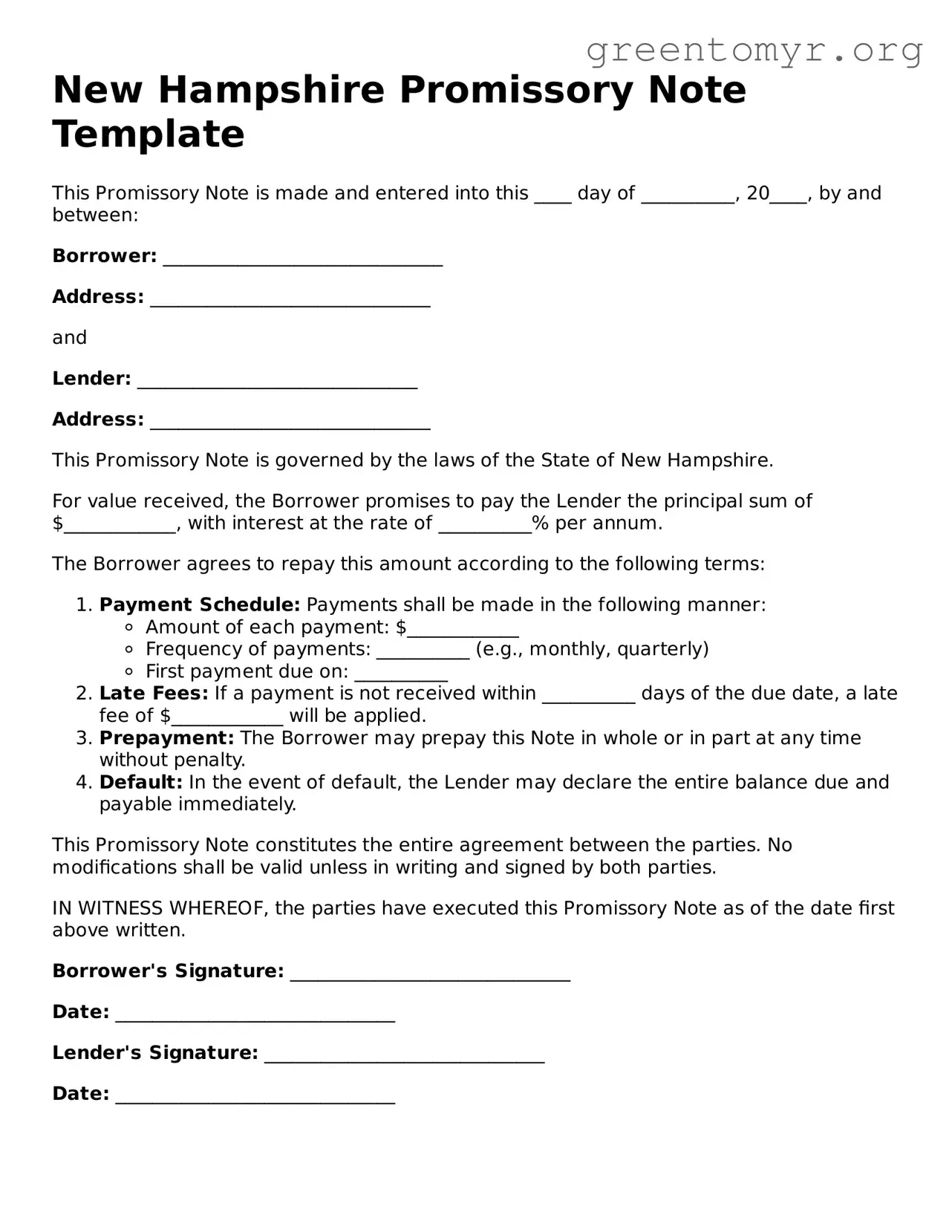

This Promissory Note is made and entered into this ____ day of __________, 20____, by and between:

Borrower: ______________________________

Address: ______________________________

and

Lender: ______________________________

Address: ______________________________

This Promissory Note is governed by the laws of the State of New Hampshire.

For value received, the Borrower promises to pay the Lender the principal sum of $____________, with interest at the rate of __________% per annum.

The Borrower agrees to repay this amount according to the following terms:

This Promissory Note constitutes the entire agreement between the parties. No modifications shall be valid unless in writing and signed by both parties.

IN WITNESS WHEREOF, the parties have executed this Promissory Note as of the date first above written.

Borrower's Signature: ______________________________

Date: ______________________________

Lender's Signature: ______________________________

Date: ______________________________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person at a specified time. |

| Governing Law | The New Hampshire Uniform Commercial Code (UCC) governs promissory notes in the state. |

| Parties Involved | Typically, there are two parties: the maker (borrower) and the payee (lender). |

| Essential Elements | A valid promissory note must include the amount, interest rate, due date, and the signatures of the parties involved. |

| Interest Rates | New Hampshire allows for both fixed and variable interest rates to be specified in the note. |

| Enforceability | For a promissory note to be enforceable, it must be clear, definite, and signed by the maker. |

| Default Consequences | If the maker defaults, the payee can pursue legal action to recover the owed amount. |

| Transferability | Promissory notes can be transferred to other parties, making them negotiable instruments under UCC guidelines. |

| Statute of Limitations | The statute of limitations for enforcing a promissory note in New Hampshire is typically 3 years from the date of default. |

| Common Uses | Promissory notes are commonly used for personal loans, business financing, and real estate transactions. |

Once you have the New Hampshire Promissory Note form in hand, you will need to fill it out carefully. This document will require specific information regarding the loan agreement. Ensure that you have all necessary details ready before you begin.

After completing the form, ensure that both parties retain a copy for their records. This will help in keeping track of the loan and the repayment process.

A promissory note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. In New Hampshire, this document serves as a legal instrument that outlines the terms of a loan agreement between the borrower and the lender. It includes essential details such as the principal amount, interest rate, repayment schedule, and any collateral involved.

A typical promissory note in New Hampshire contains several critical components:

If a borrower fails to repay the loan as agreed, the lender has the right to enforce the promissory note. This typically involves sending a formal demand for payment. If the borrower still does not comply, the lender may take legal action by filing a lawsuit in a New Hampshire court. The court can then order the borrower to pay the amount owed, including any interest and fees as specified in the note.

Yes, a promissory note can be modified after it is signed, but both parties must agree to the changes. Any modifications should be documented in writing and signed by both the borrower and the lender to be legally enforceable. This ensures that all parties are aware of the new terms and helps avoid future disputes regarding the agreement.

Filling out a New Hampshire Promissory Note form requires careful attention to detail. One common mistake is failing to include the correct names of the borrower and lender. It’s crucial to use full legal names to avoid confusion later on. Abbreviations or nicknames can lead to complications.

Another frequent error is neglecting to specify the loan amount clearly. Writing the amount in both numerical and written form helps prevent misunderstandings. For instance, if the amount is $5,000, it should be written as “Five Thousand Dollars ($5,000).” This clarity is essential for both parties.

People often overlook the interest rate, which can lead to disputes. If the loan carries interest, the rate must be clearly stated. Leaving this blank or writing it ambiguously can result in confusion and potential legal issues down the line.

Additionally, not including the repayment schedule is a common mistake. It’s important to specify when payments are due and the total duration of the loan. A clear schedule helps both the borrower and lender understand their obligations.

Some individuals forget to sign the document. A Promissory Note is not valid without the signatures of both parties. Ensure that both the borrower and lender sign and date the form to make it legally binding.

Another mistake is not having a witness or notary present during the signing process. While not always required, having a witness can add an extra layer of security to the agreement. It’s a good practice to have someone observe the signing.

People sometimes fail to keep copies of the signed Promissory Note. It’s essential for both parties to retain a copy for their records. This helps in case any disputes arise in the future.

Not including any additional terms or conditions can also be a problem. If there are specific agreements, such as late fees or prepayment penalties, these should be clearly stated in the document to avoid misunderstandings.

Finally, individuals may rush through the process without reading the entire document. Taking the time to review each section ensures that all information is accurate and complete. This careful approach can save both parties from potential issues later on.

When dealing with financial transactions, a New Hampshire Promissory Note is often accompanied by various other forms and documents. Each of these documents serves a specific purpose and helps clarify the terms of the agreement between the parties involved. Below is a list of commonly used forms that may be relevant.

Understanding these documents can help ensure that all parties are on the same page and that the loan process runs smoothly. Each form plays a vital role in protecting the interests of both the lender and the borrower.

Loan Agreement: Similar to a promissory note, a loan agreement outlines the terms of a loan, including repayment schedules and interest rates. However, it typically includes more detailed provisions regarding the rights and obligations of both parties.

Mortgage: A mortgage is a specific type of loan agreement secured by real property. Like a promissory note, it involves a promise to repay, but it also grants the lender a claim on the property if the borrower defaults.

Credit Agreement: This document governs the terms under which a borrower can access credit. It is similar to a promissory note in that it outlines repayment terms, but it often includes revolving credit options.

Installment Agreement: An installment agreement allows a borrower to repay a debt in fixed amounts over time. Like a promissory note, it requires the borrower to make regular payments, but it may specify different terms for each installment.

Secured Note: A secured note is backed by collateral, similar to a promissory note, which represents a promise to pay. The key difference lies in the additional security provided to the lender through the collateral.

Personal Guarantee: A personal guarantee is a promise made by an individual to repay another's debt. While it shares the essence of a promissory note, it often serves to reassure lenders about the borrower's commitment.

Lease Agreement: A lease agreement, while primarily for renting property, can resemble a promissory note in that it outlines payment obligations. Both documents establish a financial commitment from one party to another.

Debt Settlement Agreement: This document outlines the terms under which a debtor agrees to settle a debt for less than the full amount owed. It is similar to a promissory note in that it formalizes a payment arrangement.

IOU (I Owe You): An IOU is a simple acknowledgment of a debt, much like a promissory note. While less formal, it still indicates a promise to repay a specified amount.

When filling out the New Hampshire Promissory Note form, it’s important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

Following these guidelines will help ensure that the form is completed correctly and can be processed without delays.

When discussing the New Hampshire Promissory Note form, several misconceptions often arise. Understanding these misconceptions can help clarify the purpose and function of this important financial document.

By addressing these misconceptions, individuals can better navigate the complexities of promissory notes and make informed decisions regarding their financial agreements.

When filling out and using the New Hampshire Promissory Note form, it's important to understand several key aspects to ensure the document is both valid and effective. Below are essential takeaways to consider: