The Profit and Loss form is an essential tool for businesses of all sizes to track financial performance over a specific period. By summarizing revenues, costs, and expenses, this document provides a clear view of a company’s profitability, enabling owners and stakeholders to make informed decisions. Each entry on the form—be it sales revenue, cost of goods sold, or operating expenses—contributes to a comprehensive picture of financial health. Additionally, the form offers insights into trends, helping to gauge performance relative to previous periods or set benchmarks. Understanding this form allows business owners to identify areas of strength and opportunities for improvement. Ultimately, the Profit and Loss statement is not just a record; it’s a vital roadmap that navigates the financial landscape, guiding future strategies and growth initiatives.

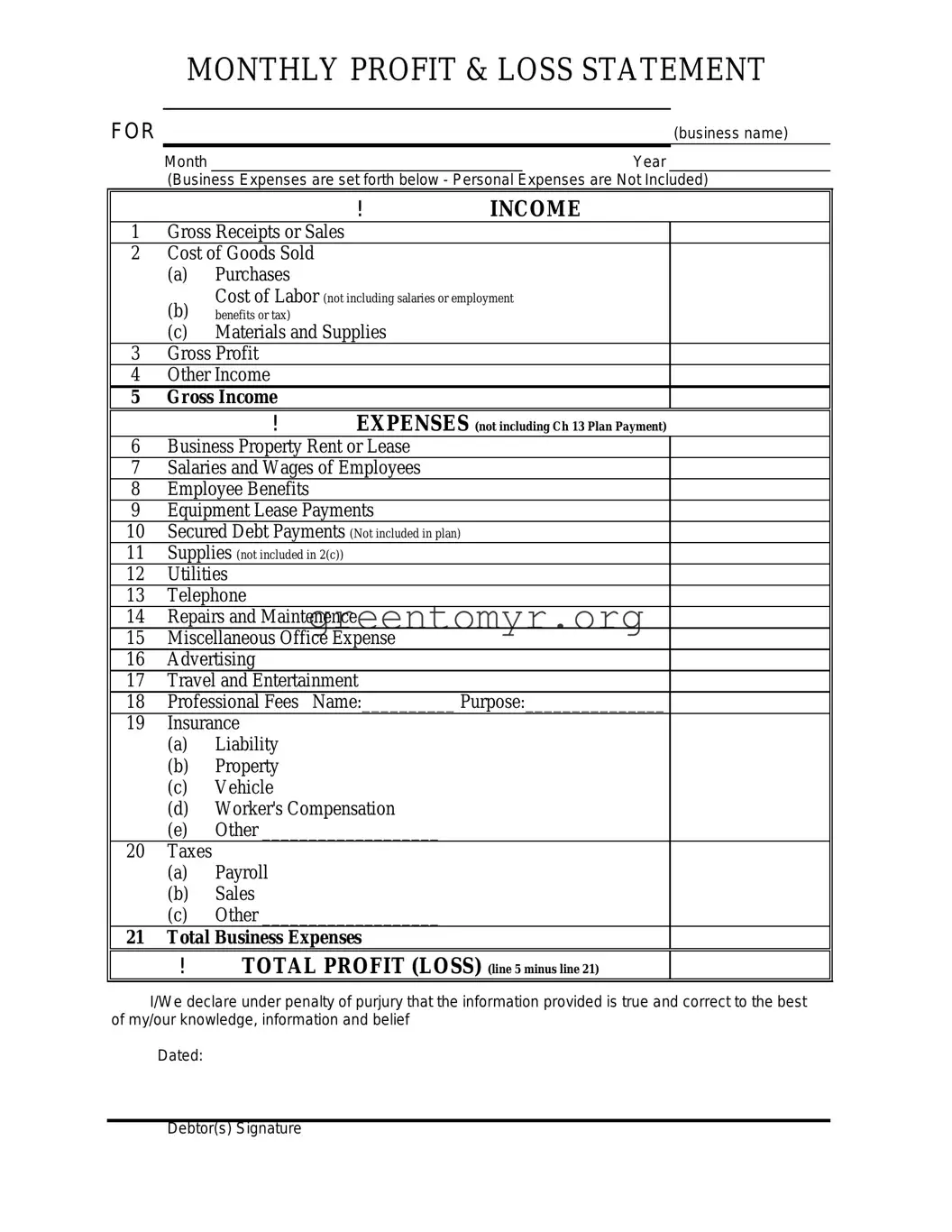

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

| Fact Name | Description |

|---|---|

| Purpose | The Profit and Loss form is used by businesses to summarize their revenues, expenses, and profits over a specific period, typically quarterly or annually. |

| Importance for Taxation | This form plays a critical role in determining a business's taxable income, as the figures reported influence the amount of tax owed to federal and state governments. |

| State-Specific Requirements | Depending on the state, certain governing laws dictate the additional information that must be included, such as California's Revenue and Taxation Code, Sections 17141-17147. |

| Monitoring Business Health | Regularly completing a Profit and Loss form allows business owners to track their financial performance and make informed decisions based on the profit margins and expense trends. |

Filling out the Profit and Loss form requires careful attention to detail. Accurate information is essential for understanding financial performance, including income and expenses. Follow these steps to complete the form successfully.

A Profit and Loss form, commonly referred to as a P&L statement, is a financial document that summarizes a company's revenues, costs, and expenses during a specific period. It provides insight into the business's ability to generate profit by subtracting total expenses from total revenues. The P&L is essential for understanding how well a business is performing financially and is often used by investors, management, and stakeholders to make informed decisions.

The Profit and Loss form typically includes several key components:

The Profit and Loss form serves multiple purposes, including:

The frequency for preparing a Profit and Loss form can vary based on the business's size and needs. Generally, small businesses may prepare it monthly or quarterly to track progress and identify trends. Larger companies often generate P&L statements monthly for more detailed financial oversight. Regardless of frequency, regular updating ensures that business owners have real-time data to aid in decision-making.

The Profit and Loss Form and Balance Sheet are both essential financial statements, but they serve different purposes. The P&L statement focuses on a company's performance over a particular period, detailing how much money was made and spent. In contrast, the Balance Sheet provides a snapshot of the business's financial position at a specific point in time, showing what the company owns (assets), owes (liabilities), and the equity held by owners. Together, these statements offer a comprehensive view of a business's financial health.

When filling out a Profit and Loss form, many individuals make common mistakes that can lead to confusion and inaccuracies. One of the biggest mistakes is failing to accurately record all income. People often overlook certain revenue sources or misclassify them. This can result in a distorted view of overall profitability, which can affect business decisions.

Another frequent error is mixing personal and business expenses. It's important to keep these two categories separate. When individuals mix them, it becomes difficult to track true business performance. This can lead to incorrect deductions and potential issues with tax authorities.

Many also forget to account for all operating expenses. It's easy to miss items like utilities, office supplies, and other recurring costs. Not including these expenses can inflate profit figures, leading to unrealistic expectations about the business's financial health.

While some might focus on one month or one quarter, failing to analyze trends over a longer period is a critical mistake. Businesses can benefit greatly from seeing long-term patterns in their Profit and Loss statements. Without this analysis, it’s tough to identify growth or areas needing improvement.

Additionally, rounding figures can lead to inaccuracies. While it might seem harmless, even small rounding errors can accumulate to significant discrepancies. It's better to report exact amounts for a precise understanding of the financial situation.

Lastly, not reviewing the Profit and Loss statement regularly is a mistake many make. Keeping track of financial performance should be a continual process. Regular reviews help adjust strategies and anticipate any cash flow problems before they become severe.

When managing a business's finances, several documents often work in tandem with the Profit and Loss (P&L) form. Each of these documents provides unique insights into your business's financial health and operational efficiency. Understanding them can enhance your ability to make informed decisions.

By utilizing these documents alongside the Profit and Loss form, businesses gain a more comprehensive picture of their financial standing. Each piece of documentation plays a vital role in shaping strategies for growth and stability.

The Profit and Loss form, commonly known as an income statement, bears similarities to several other financial documents. Understanding these similarities can provide clarity on financial health and performance. Below are four documents that share characteristics with the Profit and Loss form.

When filling out a Profit and Loss (P&L) form, attention to detail is crucial. Below are nine guidelines representing best practices and pitfalls to avoid.

Following these guidelines fosters a more accurate and useful Profit and Loss form, which ultimately aids in making informed business decisions.

Understanding the Profit and Loss form is essential for any business, yet several misconceptions can cloud its true purpose and the information it provides. Here’s a list of common misunderstandings:

By dispelling these misconceptions, business owners can leverage the Profit and Loss form as a powerful tool for financial insight and strategic planning.

When filling out and using the Profit and Loss form, keep the following key points in mind: