A Promissory Note serves as a crucial instrument in financial transactions, typically involving loans between two parties. This legal document outlines the borrower’s commitment to repay the lender a specified amount of money, along with any applicable interest within an agreed-upon timeframe. The form includes essential elements such as the names and addresses of both the borrower and lender, the principal sum being borrowed, the interest rate, and the maturity date when the final payment is due. Additionally, it may specify the repayment schedule, the consequences of defaulting on the loan, and the applicable governing laws. By clearly delineating these terms, the Promissory Note protects both the lender’s investment and the borrower’s obligations, creating a mutually agreed framework for repayment and financial accountability. Understanding the elements contained in this form is vital for anyone looking to engage in lending or borrowing arrangements, ensuring all parties are aware of their rights and responsibilities.

Promissory Note Template

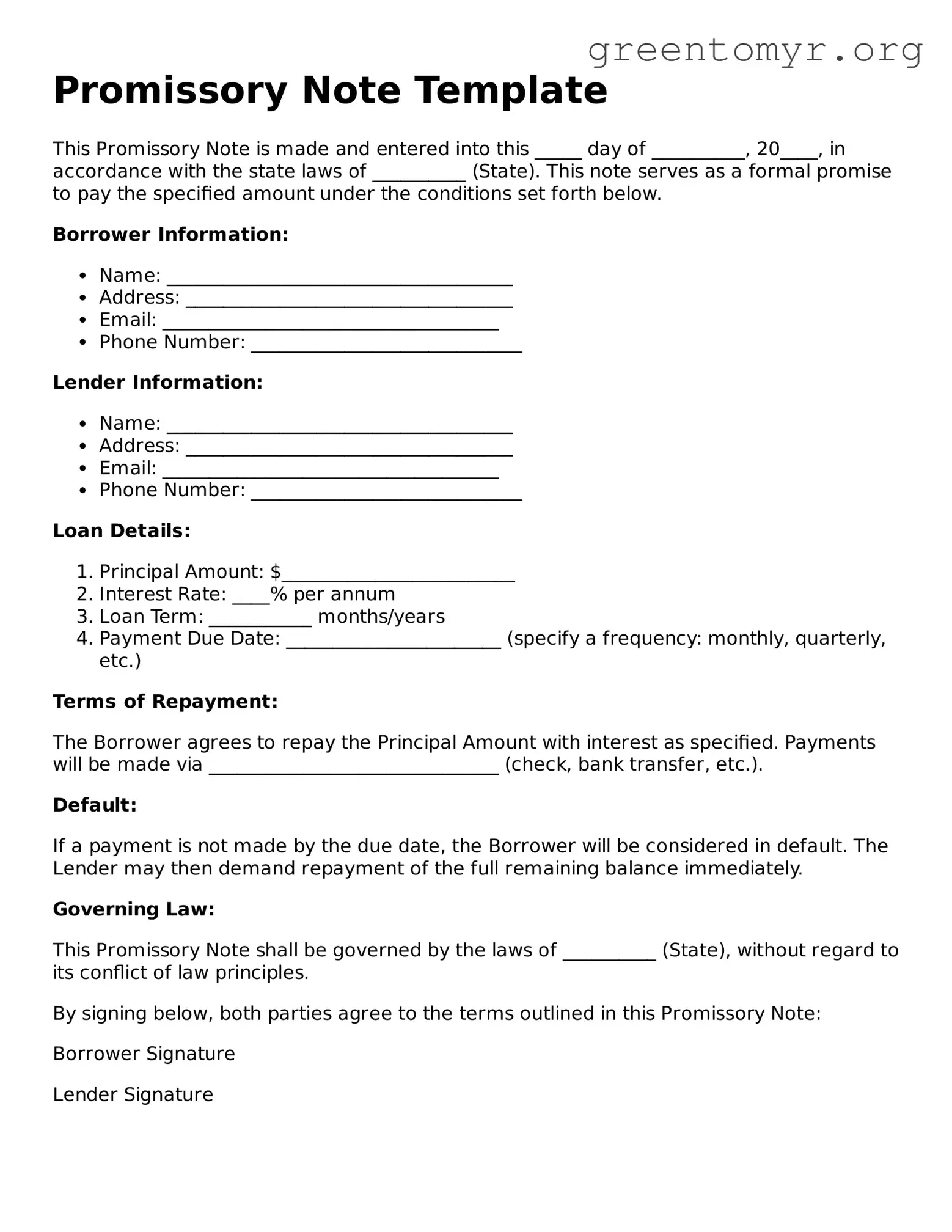

This Promissory Note is made and entered into this _____ day of __________, 20____, in accordance with the state laws of __________ (State). This note serves as a formal promise to pay the specified amount under the conditions set forth below.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

The Borrower agrees to repay the Principal Amount with interest as specified. Payments will be made via _______________________________ (check, bank transfer, etc.).

Default:

If a payment is not made by the due date, the Borrower will be considered in default. The Lender may then demand repayment of the full remaining balance immediately.

Governing Law:

This Promissory Note shall be governed by the laws of __________ (State), without regard to its conflict of law principles.

By signing below, both parties agree to the terms outlined in this Promissory Note:

Borrower Signature

Lender Signature

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a future date or on demand. |

| Parties Involved | The document involves two key parties: the maker, who promises to pay, and the payee, who is entitled to receive the payment. |

| Governing Law | The laws governing promissory notes can vary by state. For example, in California, the Uniform Commercial Code (UCC) provides the framework for these notes. |

| Requirements | To be valid, a promissory note generally requires a clear amount, repayment terms, and signatures from all parties involved. |

| Enforceability | If properly executed, a promissory note is legally binding, making it enforceable in court if the terms are not met. |

Once you obtain a Promissory Note form, filling it out accurately is essential for ensuring clarity in any financial agreement. After completing the form, it will be necessary to retain a copy for your records, and both parties involved should sign the document to make it legally binding.

A promissory note is a financial document in which one party makes a written promise to pay a specified amount of money to another party at a defined future date or on demand. It serves as a formal agreement between a borrower and a lender, outlining the terms of the loan.

A typical promissory note includes the following key information:

Yes, there are several types of promissory notes, including:

A promissory note is primarily a simple document that promises payment, while a loan agreement is a more detailed contract outlining the terms and conditions of the loan. Loan agreements often include additional provisions concerning defaults, remedies, and legal obligations, whereas promissory notes usually focus strictly on repayment terms.

Yes, a promissory note is a legally binding document, provided that it meets certain criteria. Both parties must be over the age of consent, the terms must be clear, and the note must be signed by the borrower. However, enforceability may depend on local laws and specific circumstances surrounding the agreement.

If the borrower fails to repay, the lender has the right to take legal action to recover the owed amount. Options may include suing for breach of contract or seeking to collect through other means, such as putting a lien on the borrower's assets if the note is secured.

Yes, a promissory note can be amended if both parties agree to the changes. Amendments should be put in writing and signed by both the borrower and lender to ensure clarity and legal standing. It’s advisable to document any modifications to avoid confusion later.

Individuals often encounter several common errors when completing a Promissory Note form. First, many fail to provide clear identification of the parties involved. This includes not specifying the full legal names of the borrower and lender. Without proper identification, it becomes difficult to enforce the note if needed.

Another frequent mistake is overlooking the essential details regarding the loan amount. Borrowers may leave the space for the dollar amount blank or miscalculate the desired sum. Such inaccuracies can lead to disputes over the expected loan amount in the future.

Additionally, people sometimes neglect to state the interest rate associated with the loan. Without this detail, expectations surrounding repayment can vary significantly. The absence of a documented interest rate may lead to confusion and potential legal issues later on.

It is also common for individuals to omit the repayment schedule. If the Promissory Note does not specify how and when payments will be made, this can create misunderstandings between parties. Clear terms help both borrowers and lenders act predictably.

Furthermore, a lack of clarity about default conditions represents a significant oversight. Without explicit consequences outlined in the event of default, the enforceability of the note may be compromised. This can lead to lengthy disputes and legal complications.

People frequently make the mistake of not signing the Promissory Note. A signature is a crucial component of the document. Without it, the note lacks validity and can be rendered unenforceable.

Lastly, failing to keep copies of the completed document poses risks. If disputes arise, having access to the original signed Promissory Note is essential for both parties. Proper record-keeping safeguards against any potential disagreements.

A Promissory Note is essential for outlining the agreement between a borrower and a lender regarding a loan. However, several other documents often accompany this form to provide a comprehensive framework for the transaction. Below are some key supplementary documents typically used alongside a Promissory Note.

Understanding these additional documents is crucial for both borrowers and lenders. Each piece serves to clarify responsibilities and protect the interests of the parties involved in the loan agreement.

Loan Agreement: Like a promissory note, a loan agreement outlines the terms of a loan between a lender and a borrower. It specifies the amount borrowed, interest rate, repayment schedule, and consequences of default.

Mortgage: A mortgage is a type of secured promissory note. It involves a loan to purchase real estate, where the property serves as collateral. Both documents establish a repayment obligation but differ in that a mortgage includes real property as a security interest.

Credit Agreement: Similar to a promissory note, a credit agreement governs the terms under which a borrower can use credit. It details the credit limit, repayment terms, and fees associated with the borrowing.

Bonds: Bonds are formal debt instruments issued by corporations or governments where the issuer promises to pay back the borrowed amount plus interest. Both bonds and promissory notes represent a promise to pay, though bonds are typically sold to the public.

IOU (I Owe You): An IOU is a simple acknowledgment of a debt. While it lacks the formalities of a promissory note, it still represents an obligation to pay a specific amount. Both documents serve to outline outstanding debts.

Filling out a Promissory Note can be a straightforward process if you follow some best practices. Below are important guidelines to consider.

By adhering to these guidelines, you can create a clear and effective Promissory Note that serves the interests of all parties involved.

When dealing with financial agreements, particularly in the realm of loans, the Promissory Note often comes up. Many people have misconceptions about this important document. Understanding these misconceptions can prevent confusion and aid in clearer communication between parties involved. Below is a list of ten common misconceptions about the Promissory Note.

By clarifying these misconceptions, individuals can better navigate the requirements and implications of using Promissory Notes in their financial dealings, ensuring that they understand their rights and obligations fully.

Understanding how to effectively fill out and utilize a Promissory Note form is crucial for anyone engaging in lending or borrowing money. Here are some key takeaways to consider:

Taking the time to carefully complete a Promissory Note can protect both the lender and the borrower. Meeting these key points can lay the groundwork for a smooth financial transaction.

How to Get Acord Insurance Certificate - This standardized form simplifies the filing process for workers' compensation claims.

Sba Personal Financial Statement - Applicants should keep detailed records when filling out the SBA 413.