When it comes to purchasing a vehicle, the financial agreement between buyer and seller is crucial; this is where the Promissory Note for a Car comes into play. This essential document outlines the terms under which the buyer agrees to repay the loan, detailing the amount borrowed, the interest rate, and the payment schedule. Clarity is key, as the form also specifies the consequences of defaulting on payments, ensuring both parties understand their obligations. Additionally, information regarding collateral—typically the vehicle itself—is provided to secure the loan. The inclusion of signatures from both the buyer and lender validates the agreement, creating a legal obligation that protects the interests of all involved. Understanding this form is vital for anyone looking to finance a vehicle, as it sets the stage for a transparent and structured repayment process.

Promissory Note for Car

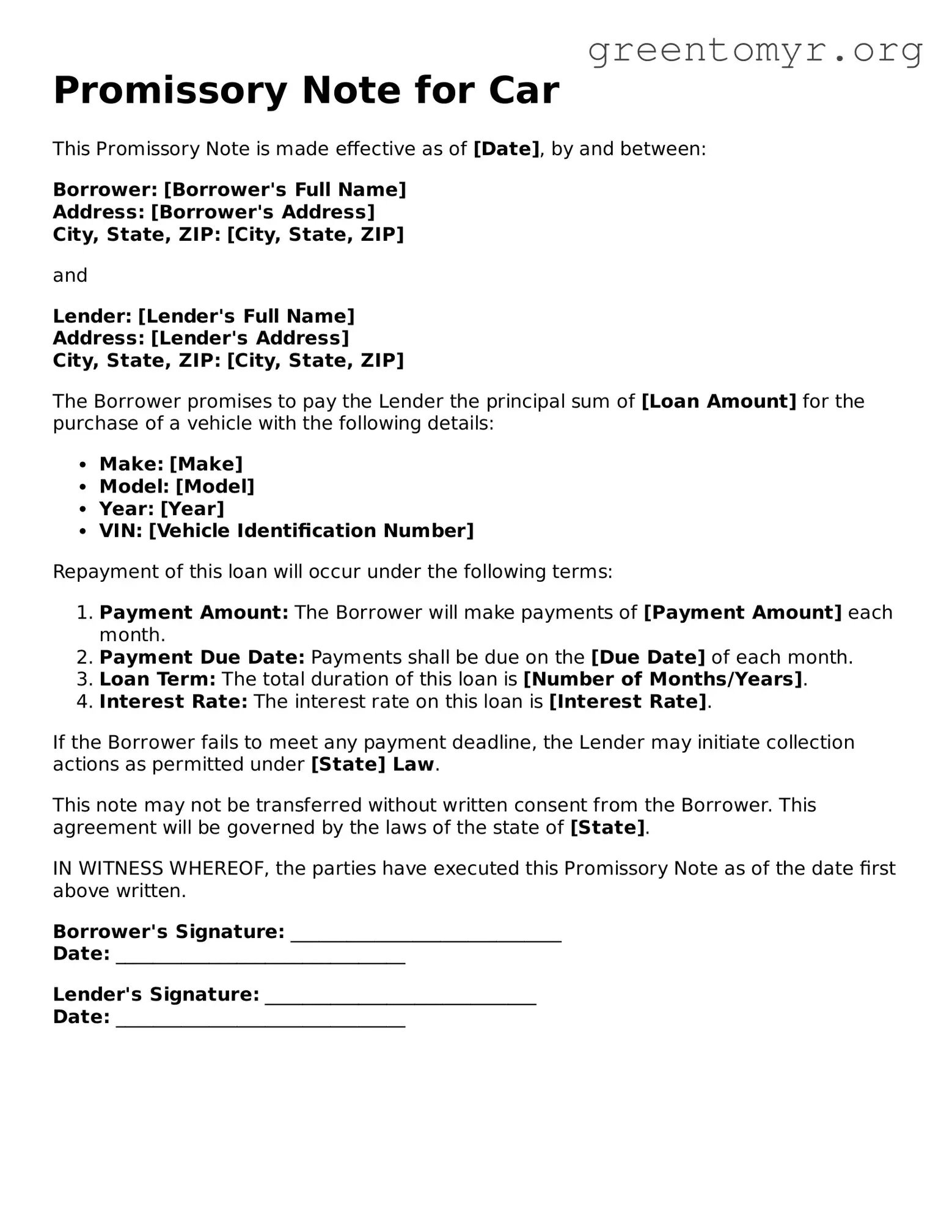

This Promissory Note is made effective as of [Date], by and between:

Borrower: [Borrower's Full Name]

Address: [Borrower's Address]

City, State, ZIP: [City, State, ZIP]

and

Lender: [Lender's Full Name]

Address: [Lender's Address]

City, State, ZIP: [City, State, ZIP]

The Borrower promises to pay the Lender the principal sum of [Loan Amount] for the purchase of a vehicle with the following details:

Repayment of this loan will occur under the following terms:

If the Borrower fails to meet any payment deadline, the Lender may initiate collection actions as permitted under [State] Law.

This note may not be transferred without written consent from the Borrower. This agreement will be governed by the laws of the state of [State].

IN WITNESS WHEREOF, the parties have executed this Promissory Note as of the date first above written.

Borrower's Signature: _____________________________

Date: _______________________________

Lender's Signature: _____________________________

Date: _______________________________

| Fact Name | Description |

|---|---|

| Definition | A promissory note for a car is a written promise to pay a specified amount of money to a lender in exchange for a vehicle. |

| Parties Involved | The note typically involves two parties: the borrower (buyer of the car) and the lender (financial institution or individual). |

| Installment Payments | Payments are usually structured as regular installments over a specified period until the total amount is repaid. |

| Interest Rates | The note may outline interest rates, which can be fixed or variable depending on the agreement. |

| State-Specific Laws | Each state has its own laws regarding promissory notes. For example, in California, the relevant laws can be found in the California Commercial Code. |

| Secured vs. Unsecured | A promissory note for a car is commonly secured by the vehicle itself, meaning the lender can reclaim the car if the borrower defaults. |

| Default Consequences | If the borrower fails to make payments, the lender may take legal action to recover the owed amount or repossess the vehicle. |

| Modification Clause | Some notes include a modification clause, allowing parties to renegotiate terms if necessary. |

| Signature Requirement | Both parties must sign the note to make it legally binding. This signifies their agreement to the terms laid out. |

Filling out the Promissory Note for a Car requires careful attention to detail to ensure accuracy. This form is essential for documenting the agreement between the borrower and lender regarding the terms of the loan. After completing the form, the borrower and lender will need to sign and date it to establish its validity.

A Promissory Note for a Car is a legal document in which one party promises to pay a specific amount to another party for the purchase of a vehicle. This note outlines the loan terms, including the principal amount, interest rate, payment schedule, and any penalties for late payments. It is essential to have this document to establish clear expectations between the buyer and the seller.

A Promissory Note is crucial for several reasons:

A typical Promissory Note for a Car includes the following key information:

To complete a Promissory Note for a Car, follow these steps:

Filling out a Promissory Note for a car is a critical step in the financing process, yet many people make common mistakes. Understanding these pitfalls can help ensure a smoother transaction. First and foremost, one frequent error is failing to include all necessary parties. Sometimes, individuals omit a co-signer or additional stakeholders. This can lead to confusion or disputes in the future.

Another mistake involves providing incomplete or inaccurate information. Whether it's the vehicle identification number (VIN) or the buyer's information, accuracy is essential. An incorrect VIN can throw off the entire transaction and potentially complicate ownership verification later on.

A key detail often overlooked is the repayment terms. Many people forget to specify the interest rate or the payment schedule. Without clear terms, lenders and borrowers might find themselves in disagreement about what’s expected, leading to frustration on both ends.

In some cases, individuals may misunderstand the distinction between secured and unsecured notes. A Promissory Note for a car should typically be secured by the vehicle itself. If this aspect isn’t understood, it may result in unintended legal issues should a default occur.

Additionally, many people neglect to review potential penalties for late payments or defaults. Omitting these terms can lead to misunderstandings if a payment is missed. Clarity on this front helps protect both the lender and borrower.

Moreover, the effective date of the agreement often goes unmentioned. This date marks when the loan terms begin. Failure to include this detail can create confusion over when payments are due.

Another common misstep lies in the signature section. Individuals sometimes forget to include a date next to their signatures or fail to sign altogether. An unsigned document may not hold legal standing, which could jeopardize the agreement.

One should also consider the format of the note. A poorly formatted document can be just as problematic; simplicity and clarity go a long way. When terms are hard to read or understand, it opens the door for potential disputes.

Lastly, assuming that verbal agreements supersede what is written down can lead to trouble. A Promissory Note should be comprehensive, capturing all mutual understandings in writing. This reduces ambiguity and reinforces accountability.

By being mindful of these mistakes while filling out a Promissory Note for a car, individuals can protect themselves and pave the way for a smooth financing experience. Taking the time to double-check each detail might be the difference between a seamless transaction and a complicated situation down the line.

When entering into a financing agreement for a vehicle, a Promissory Note serves as a crucial document outlining the borrower's promise to repay the loan. However, it often works in conjunction with other important forms and documents. Here’s a look at some of the common documents associated with a Promissory Note for a Car.

Understanding each of these documents is integral to the financing process. They ensure that both parties are protected and clarify expectations and obligations, paving the way for a smooth car ownership experience.

Loan Agreement: A loan agreement sets the terms under which one party lends money to another. Like a promissory note, it clearly outlines the repayment obligations but often includes more details about interest rates and default consequences.

Mortgage: A mortgage is a formal agreement where property is used as security for a loan. Both documents obligate the borrower to repay, and both can lead to the loss of the collateral if payments are not made.

Lease Agreement: A lease agreement involves the rental of property for a specified period. Similar to a promissory note, it requires regular payments and outlines the consequences of late payments or defaults.

Installment Contract: An installment contract allows buyers to pay for goods over time. Like a promissory note, it specifies payment schedules and what happens if a payment is missed.

Credit Agreement: A credit agreement details the terms of credit extended by a lender to a borrower. It shares similarities with a promissory note in that both obligate the borrower to repay borrowed funds under specific conditions.

Personal Loan Agreement: This document outlines the specific terms of a personal loan. It is similar to a promissory note as it reflects the borrower's commitment to repay the loan amount.

Retail Installment Sale Contract: This contract is commonly used for purchasing items on credit. It shares the same repayment structure as a promissory note.

Lines of Credit Agreement: A line of credit allows borrowers to access funds as needed. Like a promissory note, it requires repayment but offers more flexibility in accessing funds.

Student Loan Agreement: This document details the terms of a loan taken out to pay for education. It is comparable to a promissory note, highlighting the borrower's responsibility to repay the loan over time.

Debt Consolidation Agreement: A debt consolidation agreement combines multiple debts into a single loan. Similar to a promissory note, it outlines repayment terms and obligations for the borrower.

When filling out the Promissory Note for a Car form, it's essential to keep a few important guidelines in mind. Below is a list of what you should and shouldn't do to ensure a smooth process.

By adhering to these guidelines, you increase the chances of a successful and straightforward transaction.

Misconception 1: A promissory note is only for bank loans.

This is incorrect. A promissory note can be used between individuals as well. For instance, friends or family can use it when one person lends money to another for purchasing a car. The note serves as a written agreement confirming the borrowing terms, irrespective of who the lender is.

Misconception 2: A promissory note guarantees repayment.

While a promissory note is a legal commitment to repay, it does not ensure that the lender will receive the funds. If the borrower encounters financial difficulties, they may default, leaving the lender with limited recourse. Thus, it is crucial to consider the borrower's ability to repay before entering the agreement.

Misconception 3: The terms of a promissory note cannot be modified.

In fact, the terms of a promissory note can be amended by mutual agreement of the parties involved. If both the lender and borrower agree to adjust payment schedules or interest rates, they can create a revised note. Documentation of these changes should be made in writing for clarity and future reference.

Misconception 4: Promissory notes must be notarized to be valid.

This is not true. Notarization can enhance the credibility of a promissory note, but it is not a legal requirement for validity in most jurisdictions. As long as the note adequately outlines the terms and is agreed upon by both parties, it can be considered binding without notary acknowledgment.

Misconception 5: A promissory note is unnecessary if there is an oral agreement.

While oral agreements can be binding, they can lead to misunderstandings or disputes. A written promissory note provides clear evidence of the terms agreed upon, making it easier to resolve potential conflicts. Having a documented agreement considerably reduces the risk of misinterpretation.

When it comes to financing a vehicle through a Promissory Note, understanding the details is crucial. Below are key takeaways to guide you through the process.

Taking these steps will not only protect your interests but also foster trust between parties involved. A well-drafted Promissory Note is vital for a smooth transaction.