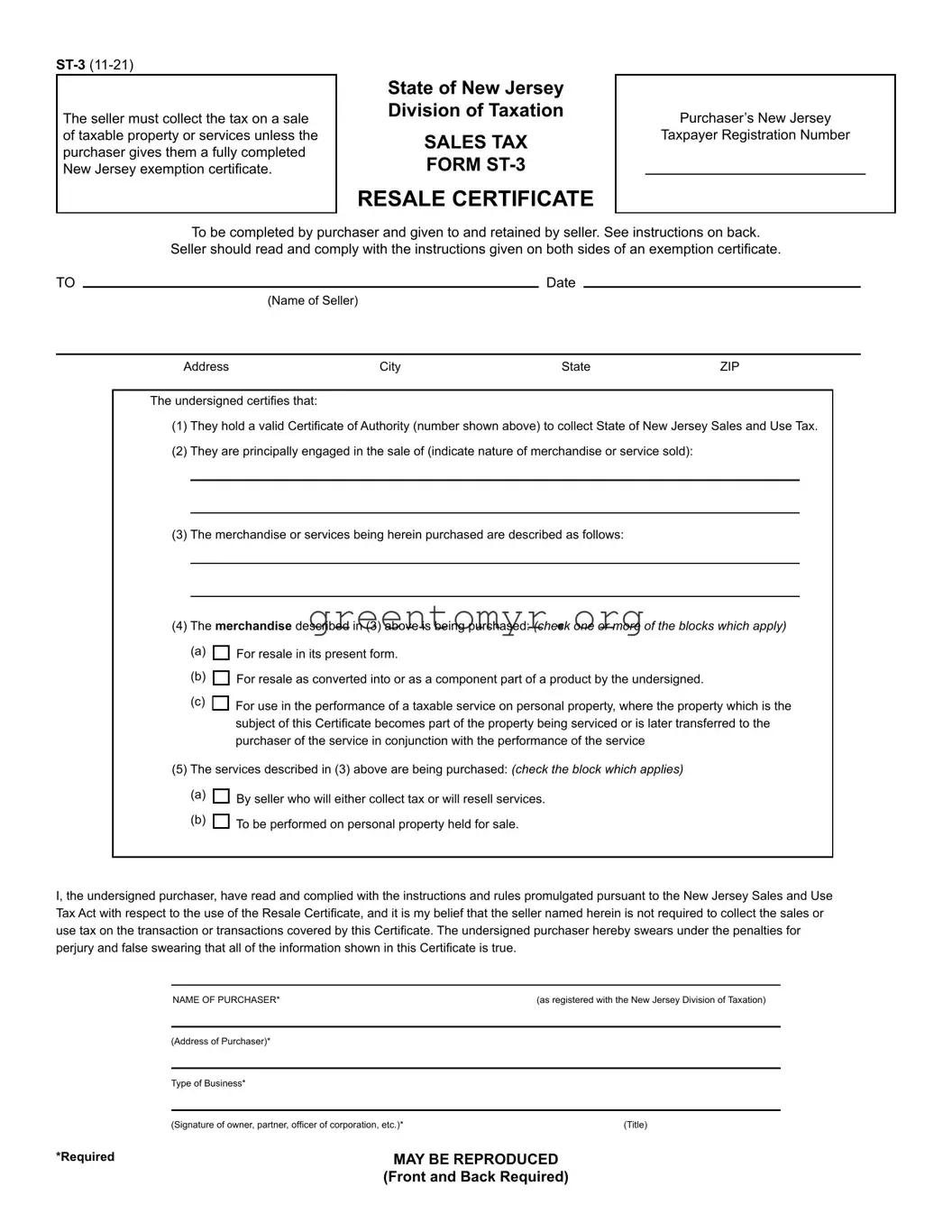

The ST-3 New Jersey form, also known as the Resale Certificate, plays a crucial role in the state's sales tax collection system. This form enables businesses to purchase taxable items without paying sales tax upfront, provided they are intended for resale. Sellers must collect sales tax unless they receive a fully completed exemption certificate from the purchaser. This ensures that transactions align with New Jersey’s Sales and Use Tax Act. The form requires essential information from the purchaser, such as their New Jersey Taxpayer Registration Number, type of business, and details about the items being bought. It also clarifies the specific purposes for which the items are being purchased, whether for resale in their current form or as parts of a different product. Additionally, the ST-3 form has strict guidelines regarding its proper use and retention, ensuring sellers remain compliant during audits. This certification process reduces the burden of sales tax on businesses and fosters a smoother operation for those involved in the resale of goods and services. Failure to comply correctly can lead to liability for unpaid taxes, making it vital for both purchasers and sellers to understand and use the form aptly.

The seller must collect the tax on a sale of taxable property or services unless the purchaser gives them a fully completed New Jersey exemption certificate.

State of New Jersey

Division of Taxation

SALES TAX

FORM

RESALE CERTIFICATE

Purchaser’s New Jersey

Taxpayer Registration Number

To be completed by purchaser and given to and retained by seller. See instructions on back.

Seller should read and comply with the instructions given on both sides of an exemption certificate.

TO |

|

|

Date |

|

|

|

|

(Name of Seller) |

|

|

|

|

|

|

|

|

|

|

Address |

City |

State |

ZIP |

|

The undersigned certifies that:

(1)They hold a valid Certificate of Authority (number shown above) to collect State of New Jersey Sales and Use Tax.

(2)They are principally engaged in the sale of (indicate nature of merchandise or service sold):

(3)The merchandise or services being herein purchased are described as follows:

(4)The merchandise described in (3) above is being purchased: (check one or more of the blocks which apply)

(a)

(b)

(c)

For resale in its present form.

For resale as converted into or as a component part of a product by the undersigned.

For use in the performance of a taxable service on personal property, where the property which is the subject of this Certificate becomes part of the property being serviced or is later transferred to the purchaser of the service in conjunction with the performance of the service

(5) The services described in (3) above are being purchased: (check the block which applies)

(a)

(b)

By seller who will either collect tax or will resell services.

To be performed on personal property held for sale.

I, the undersigned purchaser, have read and complied with the instructions and rules promulgated pursuant to the New Jersey Sales and Use Tax Act with respect to the use of the Resale Certificate, and it is my belief that the seller named herein is not required to collect the sales or use tax on the transaction or transactions covered by this Certificate. The undersigned purchaser hereby swears under the penalties for perjury and false swearing that all of the information shown in this Certificate is true.

NAME OF PURCHASER* |

(as registered with the New Jersey Division of Taxation) |

(Address of Purchaser)*

Type of Business*

(Signature of owner, partner, officer of corporation, etc.)* |

(Title) |

*Required |

MAY BE REPRODUCED |

|

(Front and Back Required) |

INSTRUCTIONS FOR USE OF RESALE CERTIFICATES –

1.Registered sellers who accept fully completed exemption certificates within 90 days subsequent to the date of sale are relieved of liability for the collection and payment of sales tax on the transactions covered by the exemption certificate. The following information must be obtained from a purchaser in order for the exemption certificate to be fully completed:

•Purchaser’s name and address;

•Type of business;

•Reason(s) for exemption;

•Purchaser’s New Jersey tax identification number or, for a purchaser that is not registered in New Jersey, the

Federal employer identification number or

•If a paper exemption certificate is used (including fax), the signature of the purchaser.

The seller’s name and address are not required and are not considered when determining if an exemption certificate is fully completed. A seller that enters data elements from paper into an electronic format is not required to retain the paper exemption certificate.

The seller may, therefore, accept this certificate as a basis for exempting sales to the signatory purchaser and is relieved of liability even if it is determined that the purchaser improperly claimed the exemption. If it is determined that the purchaser improperly claimed an exemption, the purchaser will be held liable for the nonpayment of the tax.

2.Retention of Certificates - Certificates must be retained by the seller for a period of not less than four years from the date of the last sale covered by the certificate. Certificates must be in the physical possession of the seller and available for inspection.

3.Acceptance of an exemption certificate in an audit situation - On and after October 31, 2011, if the seller either has not obtained an exemption certificate or the seller has obtained an incomplete exemption certificate, the seller has at least 120 days after the Division’s request for substantiation of the claimed exemption to either:

1.Obtain a fully completed exemption certificate from the purchaser, taken in good faith, which, in an audit situation, means that the seller obtain a certificate claiming an exemption that:

(a)was statutorily available on the date of the transactions, and

(b)could be applicable to the item being purchased, and

(c)is reasonable for the purchaser’s type of business; OR

2.Obtain other information establishing that the transaction was not subject to the tax.

If the seller obtains this information, the seller is relieved of any liability for the tax on the transaction unless it is discovered through the audit process that the seller had knowledge or had reason to know at the time such information was provided that the information relating to the exemption claimed was materially false or the seller otherwise knowingly participated in activity intended to purposefully evade the tax that is properly due on the transaction. The burden is on the Division to establish that the seller had knowledge or had reason to know at the time the information was provided that the information was materially false.

4.Additional Purchases by Same Purchaser - This certificate will serve to cover additional purchases by the same purchaser of the same general type of property. However, each subsequent sales slip or purchase invoice based on this Certificate must show the purchaser’s name, address and New Jersey, Federal, or out of state registration number for your purpose of verification.

5.Retention of Certificates - Certificates must be retained by the seller for a period of not less than four years from the date of the last sale covered by the certificate. Certificates must be in the physical possession of the seller and available for inspection on or before the 90th day following the date of the transaction to which the certificate relates.

EXAMPLES OF PROPER USE OF RESALE CERTIFICATE

a. A retail household appliance store owner issues a Resale Certificate when purchasing household appliances from a supplier for resale. b. A furniture manufacturer issues a Resale Certificate to cover the purchase of lumber to be used in manufacturing furniture for sale.

c. An automobile service station operator issues a Resale Certificate to cover the purchase of auto parts to be used in repairing customers cars.

EXAMPLES OF IMPROPER USE OF RESALE CERTIFICATE

In the examples below, the seller should not accept Resale Certificates, but should insist upon payment of the sales tax. a. A lumber dealer can not accept a Resale Certificate from a tire dealer who is purchasing lumber for use in altering their premises.

b. A distributor may not issue a Resale Certificate on purchases of cleaning supplies and other materials for their own office maintenance, even though they are in the business of distributing such supplies.

c. A retailer may not issue a Resale certificate on purchases of office equipment for their own use, even though they are in the business of selling office equipment.

d. A supplier can not accept a Resale Certificate from a service station owner who purchases tools and testing equipment for use in their business.

REPRODUCTION OF RESALE CERTIFICATE FORMS: Private reproduction of both sides of Resale Certificates may be made without the prior permission of the Division of Taxation.

FOR MORE INFORMATION: Read publication

https://www.state.nj.us/treasury/pdf/pubs/sales/su6.pdf

DO NOT MAIL THIS FORM TO THE DIVISION OF TAXATION

This form is to be completed by purchaser and given to and retained by seller.

| Fact Title | Description |

|---|---|

| Purpose | The ST-3 form is used as a Resale Certificate in New Jersey for ensuring tax exemption on the purchase of taxable items or services meant for resale. |

| Tax Collection Responsibility | The seller is required to collect sales tax unless the purchaser presents a fully completed New Jersey exemption certificate. |

| Certificate of Authority | Purchasers must have a valid Certificate of Authority to collect State of New Jersey Sales and Use Tax to complete the form. |

| Governing Law | This form falls under the New Jersey Sales and Use Tax Act. |

| Information Requirements | To be valid, the ST-3 form must include details such as the purchaser's name, address, tax identification number, and reasons for exemption. |

| Retention Policy | Sellers must retain the completed forms for at least four years from the date of the last sale covered by the certificate. |

| Usage Examples | Examples include a retail store purchasing products for resale or a manufacturer buying materials for items intended for sale. |

| Improper Use | Examples of improper use include a tire dealer using the certificate for lumber not intended for resale or office supplies for personal use. |

Filling out the ST-3 form in New Jersey involves providing specific information to certify that the purchase of goods or services qualifies for a resale exemption. This information must be completed accurately to ensure compliance with the state's tax regulations. Follow the steps outlined below to correctly fill out the ST-3 Resale Certificate.

After completing the form, it should be given to the seller and kept on file for a minimum of four years. Ensure that the certification is truthful, as there are legal penalties for false statements. The form should not be sent to the Division of Taxation but retained for potential audits or inspections.

The ST-3 form, known as the Resale Certificate, is used in New Jersey to exempt certain transactions from sales tax. This form allows a purchaser who is a registered seller to buy tangible personal property or services without paying sales tax. By providing this certificate to the seller, the purchaser certifies that the items or services being bought are intended for resale or other applicable purposes as outlined in the document.

The ST-3 form should be completed by purchasers who are registered sellers in New Jersey and intend to buy goods or services for resale. This includes retail businesses and service providers that use products in a way that qualifies for exemption from sales tax. Individuals and companies that do not plan to resell goods or services would not need to complete this form.

To ensure that the ST-3 form is valid, several pieces of information must be included:

Sellers are required to keep the ST-3 form for a minimum of four years from the date of the last sale covered by the certificate. The seller must ensure that the form is readily accessible and available for inspection by tax authorities if necessary. Maintaining proper records helps sellers avoid potential liability for uncollected sales tax.

If a seller accepts an incomplete ST-3 form, they may be held responsible for collecting and remitting the sales tax on the transaction. However, if they obtain the correct and complete certificate within a specified timeframe, they may avoid this liability. It’s crucial for sellers to ensure that they have fully executed forms on file to protect themselves during an audit.

Yes, the ST-3 form can cover additional purchases made by the same purchaser of similar types of property. However, for each subsequent transaction, a sales slip or invoice must still include the purchaser’s identifying information to validate the exemption. This practice helps ensure that the resale certificate continues to be applicable and valid.

Examples of proper use of the ST-3 form include a retail store owner purchasing inventory for resale or a manufacturer sourcing raw materials needed to create products for sale. In contrast, improper uses would involve a business purchasing supplies or tools for its own use, rather than for resale. Following these guidelines can help prevent misuse and ensure compliance with tax regulations.

Filling out the ST-3 New Jersey form can seem straightforward, but many people make common mistakes that can lead to complications. One frequent error is failing to provide a valid New Jersey Taxpayer Registration Number. Sellers need this number to ensure they are following the state’s tax regulations properly. Without it, the resale certificate may be deemed incomplete.

Another mistake is neglecting to describe the nature of the business accurately. Purchasers should clearly indicate what type of products or services they offer. Ambiguity in this section can raise red flags and potentially cause issues during audits.

A lot of people forget to check the appropriate box for how the merchandise is being purchased. The form has specific checkboxes, and selecting the correct one is crucial. Misrepresenting how the items will be used can lead to liability for unpaid taxes.

People also often overlook the signature requirement. Each form must be signed by an authorized individual, such as the owner or an officer. Failing to include a signature invalidates the certificate, making it unusable.

In addition, some purchasers do not read the instructions on the back of the form. These instructions provide essential guidance on how to fill out and submit the form correctly. Ignoring them can lead to errors that could have easily been avoided.

Furthermore, many forget that certificates must be retained for at least four years. Sellers need to keep these forms on file for potential inspections. Not retaining them could result in penalties or difficulties in proving tax compliance.

Many purchasers also incorrectly think that once the resale certificate is completed, it covers all future transactions. This is not the case. Each new purchase should have its invoice or sales slip reflecting the purchaser's details for verification purposes.

Lastly, some individuals fail to recognize that certain purchases are ineligible for the resale certificate. For example, purchasing office equipment for personal use while being in the business of selling such items is not allowed. Understanding the limitations and rules surrounding acceptable uses of the resale certificate is critical.

The ST-3 New Jersey form is a resale certificate that allows purchasers to buy items tax-free with the intent to resell. When filling out this form, several related documents may also be utilized to ensure compliance with New Jersey sales tax regulations. Below is a list of common forms and documents often used alongside the ST-3 form.

Using these forms in conjunction with the ST-3 New Jersey resale certificate helps businesses navigate tax obligations and maintain compliance with state regulations. Proper documentation minimizes the risk of misunderstandings with tax authorities. It is essential for buyers and sellers to understand the requirements and ensure all forms are filled out completely and accurately.

The ST-3 form in New Jersey serves as a resale certificate that allows purchasers to buy taxable goods or services without incurring sales tax, provided they fill out the form correctly. There are several other documents similar to the ST-3 form in their function of exempting certain transactions from taxation. Here are eight such documents:

Each of these documents function similarly to the ST-3 form by validating a purchaser's claim to an exemption from sales tax, thus ensuring compliance with New Jersey's tax regulations and aiding in the proper collection of sales taxes where applicable.

When filling out the St 3 New Jersey form, it’s essential to follow certain guidelines to ensure accuracy and compliance. Here are eight recommendations that can help you successfully complete the form:

By adhering to these guidelines, you can navigate the process of filling out the St 3 form with greater ease and confidence.

Understanding the ST-3 New Jersey Resale Certificate is crucial for both buyers and sellers involved in taxable transactions. However, several misconceptions often arise regarding this form. Here are four common misunderstandings and clarifications on each:

Clarifying these misconceptions can help both sellers and purchasers navigate the nuances of New Jersey’s sales tax system effectively. Understanding the rules ensures compliance and minimizes risks associated with tax liabilities.

Key Takeaways on Filling Out and Using the ST-3 New Jersey Form: