The Tax Power of Attorney (POA) form is a crucial document that allows individuals to appoint someone else to act on their behalf in matters related to the IRS. This form enables the appointed agent to handle a variety of tax-related tasks, including filing returns, accessing tax information, and communicating with the IRS. It is important to note that the Tax POA can be specific to certain tax years or types of taxes, providing flexibility based on the taxpayer's needs. Understanding the types of authority that can be granted through the form is essential, as it allows for both limited and broad powers depending on the preferences of the taxpayer. Accuracy is key when filling out the form; any errors can lead to delays or complications. Ultimately, the Tax POA form serves as an important tool for taxpayers who wish to ensure their tax matters are managed effectively, while also allowing them to maintain some level of control over their personal financial affairs.

mil OFDEPARTMENTREVENUE

Form REV184b, Business Power of Attorney

Read instructions before completing this form.

To grant authority for an individual or sole proprietor, complete Form REV184i, Individual or Sole Proprietor Power of Attorney.

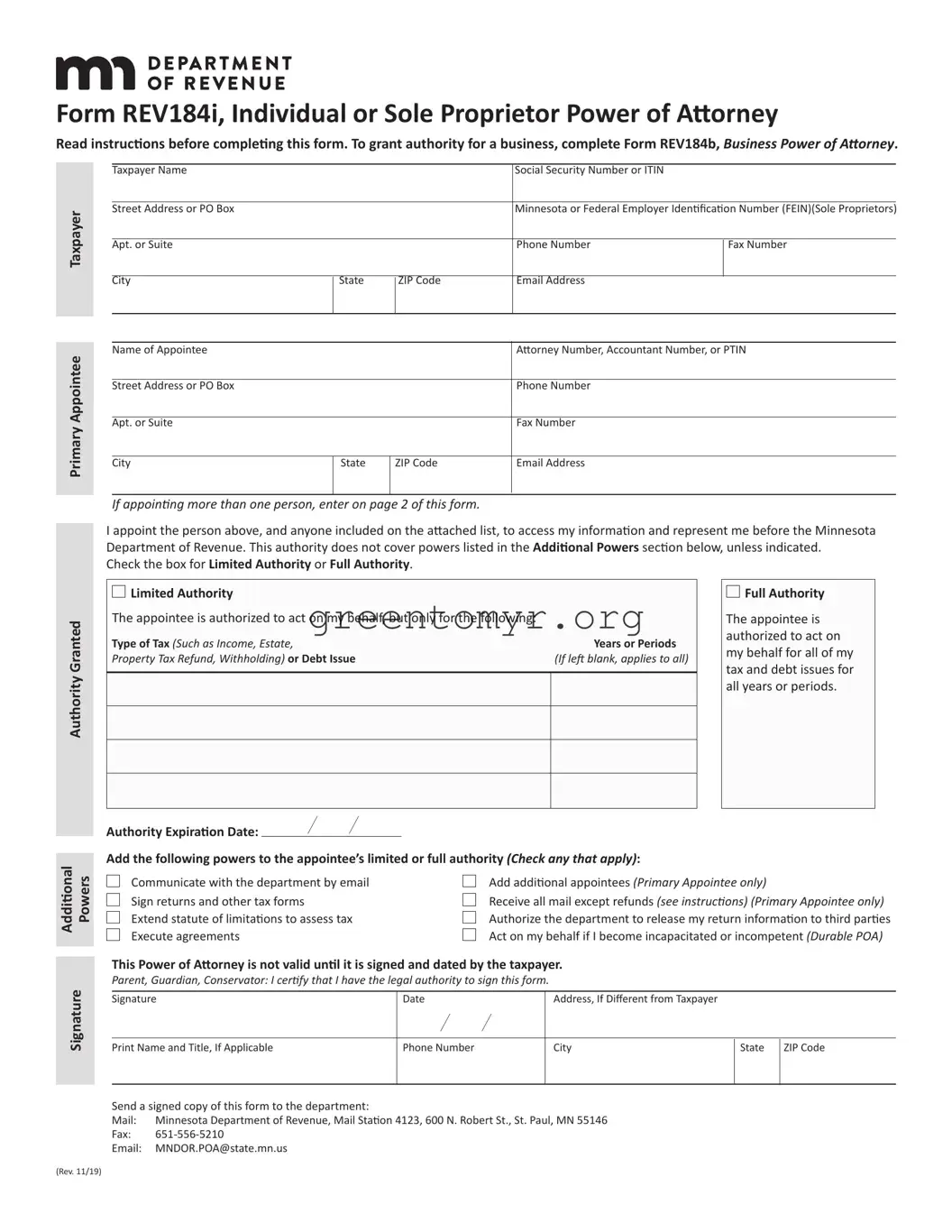

Business Taxpayer

Primary Appointee

Business Taxpayer Name |

|

|

Minnesota or Federal Employer Identification Number (FEIN) |

|

Street Address or PO Box |

|

|

Phone Number |

Fax Number |

Apt. or Suite |

|

|

|

I |

|

|

Combined Business Returns: Filing entity name (if different) |

||

City |

State |

ZIP Code |

Filing Entity FEIN or Taxpayer Identification Number |

|

I |

|

I |

|

|

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

|

Street Address or PO Box |

|

|

Phone Number |

|

Apt. or Suite |

|

|

Fax Number |

|

City |

State |

ZIP Code |

Email Address |

|

I |

|

I |

|

|

If appointing more than one person, enter on page 2 of this form. |

|

|

||

The person named above, and anyone included on the attached list, is appointed to access the taxpayer’s information and represent it be- fore the Minnesota Department of Revenue. Check the box for Limited Authority or Full Authority. (This authority does not cover powers listed in the Additional Powers section below, unless indicated.)

Authority Granted

□

Limited Authority

Limited Authority

The appointee is authorized to act on behalf of the taxpayer, but only for the following:

Type of Tax (Such as Business Income, |

Tax Form Name or Number |

Years or Periods |

Sales, Withholding) or Debt Issue |

(If applicable) |

(If left blank, applies to all) |

□

Full Authority

Full Authority

The appointee is authorized to act on behalf of the taxpayer for all tax and debt issues for all years or periods.

Authority Expiration Date: |

I |

I |

|

|

Signature Powers

Additional

(Rev. 11/19)

Add the following powers to the appointee’s limited or full authority (check any that apply):

□ |

Communicate with the department by email |

□ |

Add additional appointees (Primary Appointee only) |

□ |

Sign returns and other tax forms |

□ |

Receive all mail except refunds (see instructions) (Primary Appointee only) |

□ |

Extend statute of limitations to assess tax |

□ |

Authorize the department to release return information to third parties |

□ |

Execute agreements |

|

|

This Power of Attorney is not valid until it is signed and dated by someone with legal authority to sign agreements on behalf of the business taxpayer.

I certify that I have the legal authority to sign this form.

Signature |

Date |

Address, If Different from Taxpayer |

|

I |

I |

|

|

Print Name and Title |

Phone Number |

City |

State |

ZIP Code |

|

|

|

|

|

Send a signed copy of this form to the department:

Mail: |

Minnesota Department of Revenue, Mail Station 4123, 600 N. Robert St., St. Paul, MN 55146 |

Fax: |

|

Email: |

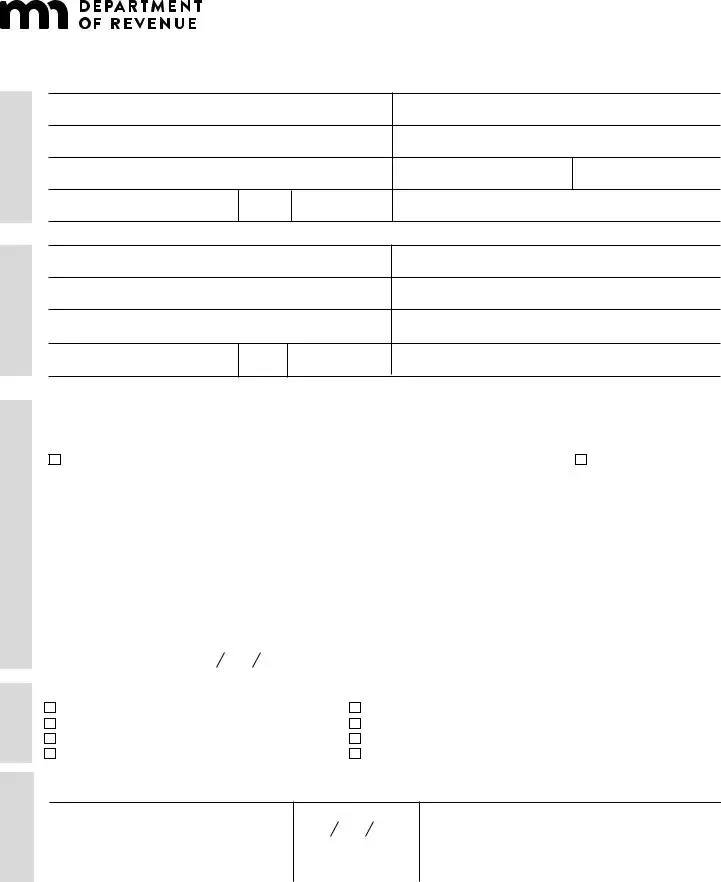

Form REV184b, Page 2 — Additional Appointees

Name of Business Taxpayer

MN ID or FEIN

Include any additional appointees below. Additional appointees only have authority over matters chosen in the Authority Granted and Additional Powers sections on page 1.

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

Street Address or PO Box |

|

|

Phone Number |

Apt. or Suite |

|

|

Fax Number |

City |

State |

ZIP Code |

Email Address |

I |

|

I |

|

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

Street Address or PO Box |

|

|

Phone Number |

Apt. or Suite |

|

|

Fax Number |

City |

State |

ZIP Code |

Email Address |

I |

|

I |

|

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

Street Address or PO Box |

|

|

Phone Number |

Apt. or Suite |

|

|

Fax Number |

City |

State |

ZIP Code |

Email Address |

I |

|

I |

|

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

Street Address or PO Box |

|

|

Phone Number |

Apt. or Suite |

|

|

Fax Number |

City |

State |

ZIP Code |

Email Address |

I |

|

I |

|

Name of Appointee |

|

|

Attorney Number, Accountant Number, or PTIN |

Street Address or PO Box |

|

|

Phone Number |

Apt. or Suite |

|

|

Fax Number |

City |

State |

ZIP Code |

Email Address |

I |

|

I |

|

Attach additional copies of this page, as needed.

Form REV184b Instructions

What is a Power of Attorney (POA)?

A power of attorney (POA) is a legal document that grants an attorney, accountant, agent, tax return preparer, or other person authority to access the business taxpayer’s account information and represent the taxpayer before the Minnesota Department of Revenue.

Use of Information

The information you enter on this form may be private or nonpublic under state law. We use it to allow the appointee to access the taxpay- er’s account and take actions on its behalf. We may share it with other government entities for tax administration if allowed by law. You are not required to provide the information requested; however, we are unable to process the appointment unless the form is complete.

How do I complete this form?

Business Taxpayer

Step 1

Enter the business taxpayer’s name and contact information.

Note: This form does not cover personal tax issues or sole proprietorships. Complete Form REV184i, Individual Power of Attorney.

Step 2

Enter the Federal Employer ID number (FEIN), or Minnesota Tax ID number.

Step 3

For businesses filing combined business returns, enter the name and ID number for the entity responsible for filing returns.

Primary Appointee

Eligibility: The appointee must be eligible to represent the business with the department.

The taxpayer may not appoint:

•A person barred or suspended from practice as an attorney or accountant

•A person barred or suspended from practice before the IRS

•An employee of the department

•A former department employee within one year of leaving the department

For details, go to www.revenue.state.mn.us and enter Preparer Enforcement in the Search box.

Step 4

Enter the appointee’s name and contact information. An appointee is a person selected to represent the taxpayer before the department. The taxpayer may have more than one appointee, but only the primary appointee can be selected to receive mailed correspondence from the department.

For additional appointees, complete page 2 of Form REV184b. Include additional pages, if needed. Note: The taxpayer is responsible for keeping the appointees informed of changes to its account.

Authority Granted

Step 5

Choose whether to grant the appointee full authority or to limit authority to specific issues.

Limited Authority allows the appointee to act on specific tax or debt issues.

•By tax type or issue

•By year or filing period is optional. If no year is provided, authority applies to all periods.

Full Authority allows your appointee to act on your behalf for your tax and debt issues.

Choose an expiration date for the POA if applicable. To have the POA end on a specific date, enter the month, day, and year (enter as MM/ DD/YY). If no date is provided, the POA and additional powers will remain in effect until removed.

Continued

Form REV184b Instructions, cont.

Additional Powers

Step 6

Choose additional powers to give the appointee.

•Communicate by email

Allows the appointee to communicate with the department by email.

Note: Transmit return information at your own risk. Email is not secure. The department is not liable for damages caused by interception of emails.

•Sign returns and other forms

This does not authorize the appointee to endorse or negotiate any checks or other payments issued by the department.

•Add additional appointees

Allows the primary appointee to authorize additional appointees.

Note: The appointee may only grant authority over tax types or issues authorized in the Authority Granted section.

•Execute agreements

Allows the appointee to enter into contracts and other binding agreements on behalf of the taxpayer.

•Authorize disclosure to third parties

Allows the appointee to authorize the department to share return information with people outside the department. Appointees may discuss the taxpayer’s account with people they employ or supervise, even if this box is not checked.

•Receive all mail except refunds

Authorizes the department to mail letters, legal notices, and tax information directly to the primary appointee only. Any refunds or letters relating to refunds will be sent directly to the business.

Note: The business may still receive copies of some mail from the department in certain circumstances.

This power is effective only for the tax types or issues granted to the primary appointee. If the business is only granting authority for spe- cific years or periods, this option is not available. All mail will go directly to the business.

Mail will go to the most recently designated person, replacing designations from a prior POA.

Signature

Step 7

Owners, officers, or authorized agents:

Sign, date, print your name and title, and enter your contact information. This POA is not valid until it is signed and dated by someone with legal authority to sign it

We reserve the right to request additional information as needed to verify identity and authority to sign.

Step 8

Send the form to the department using only one of the following:

•Mail: Minnesota Department of Revenue, Mail Station 4123, 600 N. Robert St., St. Paul, MN 55146

•Fax:

•Email: [email protected]

How do I revoke an appointee?

To revoke an appointee, the taxpayer or the appointee must send the department a signed and dated statement terminating the appointee’s authority or a completed Form REV184r, Revocation of Power of Attorney.

No POA form is necessary to access a taxpayer’s

Questions?

Website: www.revenue.state.mn.us

Email: [email protected]

Phone:

| Fact Name | Description |

|---|---|

| Definition | The Tax Power of Attorney (POA) form allows an individual to authorize someone else to act on their behalf regarding tax matters. |

| Common Use | Individuals often utilize this form to give their tax preparer or attorney the right to communicate with the IRS or state tax agencies. |

| State-Specific Variants | Many states have their own versions of the Tax POA form, and the requirements may differ. |

| Governing Law | In the U.S., the IRS guidelines and state tax regulations govern the use of Tax POA forms. |

| Form Number | The IRS Tax POA form is known as Form 2848. Other states may have different identifying numbers. |

| Expiration | Tax POA forms generally remain valid until the taxpayer revokes it or until an expiration date is specified. |

| Signature Requirement | A valid signature from the taxpayer is mandatory on the form for it to be legally binding. |

| Filing Method | Tax POA forms can usually be submitted by mail or electronically, but methods may vary by state. |

| Limitations | The authority granted through a POA is limited to the specified tax matters and does not extend to unrelated decisions. |

Filling out the Tax Power of Attorney (POA) form is an important step to ensure someone can manage your tax matters legally. After completing the form, submit it to the IRS along with any required documents to finalize the process.

A Tax Power of Attorney (POA) form allows an individual to designate another person to act on their behalf concerning tax matters. This form grants the appointed representative the authority to handle various tax-related issues with the Internal Revenue Service (IRS) or state tax agencies. It can cover actions such as filing tax returns, obtaining tax information, and communicating with tax officials.

Individuals can appoint various representatives. Common choices include:

It’s important to ensure that the representative understands the responsibilities and has the authority to navigate tax situations effectively.

Completing the Tax POA form involves several clear steps:

Accuracy during completion is vital to ensure that the POA is effective.

Upon submission of the Tax POA form, the relevant tax authority will review it. Once accepted, the appointed representative can act on behalf of the taxpayer. The authority may send a confirmation to the taxpayer and the representative. It is advisable to keep records of the submission for future reference.

Yes, a Tax POA can be revoked at any time by the taxpayer. To revoke the authority, the taxpayer should submit a written statement to the tax authority that originally accepted the POA. This statement should include:

Once the tax authority acknowledges the revocation, the representative’s powers will cease immediately.

Filling out a Tax Power of Attorney (POA) form can be a straightforward process, but many people stumble along the way. One common mistake is the failure to provide complete and accurate information. When individuals omit significant details or make spelling errors, they risk delays or even denials. The IRS requires precise data to prevent any confusion regarding who is authorized to act on behalf of the taxpayer.

Another frequent error is neglecting to sign and date the form. Without a signature or the date, the form is considered incomplete. This missing step may lead to the rejection of the request, creating unnecessary complications. Always remember to review the form completely before submission, ensuring every required action is taken.

People often overlook the importance of specifying the correct tax years. A Tax POA should clearly indicate which tax years the authorization applies. Failing to do this can limit the authority granted or confuse the tax representative regarding the scope of their power.

Additionally, some individuals fail to clearly identify the tax representative. A common error involves writing down incomplete names or incorrect identification numbers. Make sure to provide the full name and, when applicable, the preparer's identification number to avoid any uncertainty about who has been authorized.

One significant oversight is not understanding the scope of authority being granted. It's crucial to decide what powers you want to bestow upon your representative. If you grant too much authority, it may lead to unintended consequences. Conversely, granting too little might hinder your representative's ability to provide the necessary help.

Finally, many people do not keep copies of the submission. After sending off the Tax POA, it’s wise to retain a copy for personal records. This way, you can refer back to it if there are any questions or disputes about what powers were granted.

When preparing a Tax Power of Attorney (POA) form, individuals may also need to consider other documents that can facilitate the tax-related matters they are addressing. These accompanying forms help streamline the process and ensure that all necessary legalities are covered. Below is a list of commonly used forms and documents that complement the Tax POA.

Understanding and utilizing these documents alongside the Tax POA can significantly ease the tax preparation and filing process. Each form serves a distinct purpose, ensuring that individuals and their representatives have the necessary support to address any tax issues effectively and efficiently.

Durable Power of Attorney (DPOA): This document allows one person to grant another the authority to make decisions on their behalf, even if they become incapacitated. Like the Tax POA, it empowers an agent to act in the best interest of the principal.

Financial Power of Attorney: Similar to the Tax POA, this document permits the designated agent to manage the principal's financial matters. This includes handling bank accounts, investments, and taxes.

Healthcare Power of Attorney: A Healthcare POA, while focused on medical decisions, shares the essential function of granting authority to act on behalf of another individual. Both forms ensure someone can advocate for a person’s wishes when they are unable to do so themselves.

Living Will: Though primarily a document about medical care preferences, a Living Will can work in conjunction with a Healthcare POA to clarify the individual’s wishes. Both aim to ensure the person’s desires are honored when they cannot communicate them.

Trust Agreement: A Trust allows one person to manage assets for another, which may include tax-related matters. Both documents designate someone to handle specific responsibilities and protect an individual's interests.

Tax Return Authorization: This form is used for authorizing someone to discuss a tax return or tax matter with the IRS. Like the Tax POA, it enables communication between the taxpayer and the IRS without granting broader powers.

Consent to Release Information: This document, similar to the Tax POA, allows individuals to authorize third parties to access specific information, ensuring that important details can be shared when needed.

Employment Authorization: This form is used to grant permission for an employer to manage an employee’s taxrelated withholdings and payments. It parallels the Tax POA in giving others the power to handle tax responsibilities.

When filling out the Tax Power of Attorney (POA) form, it is important to follow certain guidelines. Adhering to these suggestions will help ensure that the process runs smoothly and that all necessary information is provided accurately.

Following these dos and don'ts will help ensure that your Tax POA form is processed efficiently and correctly.

The Tax Power of Attorney (Tax POA) form often comes with a variety of misconceptions. Below are some common misunderstandings about this important legal document.

Understanding the Tax Power of Attorney (POA) form is crucial for effectively handling tax matters. Here are some key takeaways to guide you through the process:

By following these key points, you will better navigate the complexities involved in appointing someone to represent you with the IRS through the Tax POA form.