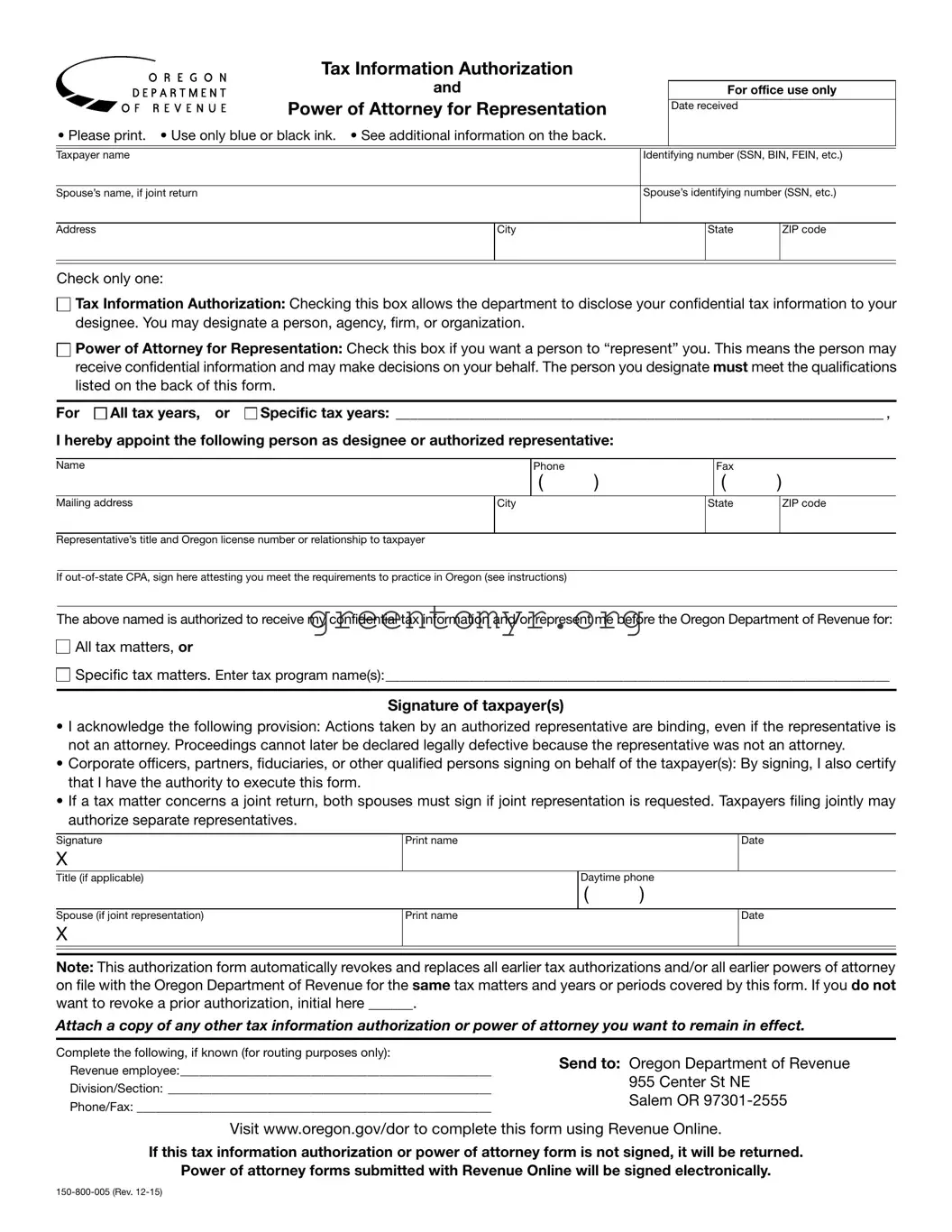

The Tax POA 150-800-005 form plays a crucial role for taxpayers looking to streamline their tax-related communications. This form allows individuals to designate a representative, often a tax professional or attorney, to act on their behalf in dealing with tax matters. By submitting this form, taxpayers grant authority to their chosen representative to receive confidential tax information, respond to tax inquiries, and represent them during audits. Its significance extends beyond mere delegation; it provides peace of mind by ensuring that knowledgeable professionals are handling complex tax situations. The form encompasses essential details, including the taxpayer’s information, representative's information, and the specific powers granted. Without this form, navigating the tax landscape can be daunting, especially when facing the IRS or state tax authorities. Understanding the use and requirements of the Tax POA 150-800-005 is vital for any taxpayer seeking a more manageable approach to tax compliance.

~AEGON |

Tax Information Authorization |

|

|

|

|

||

|

|

|

|

|

|

||

~~ |

DE~ARTMENT |

and |

|

|

For office use only |

||

~~ 0 F R EV E N U E |

Power of Attorney for Representation |

|

|

|

|

||

|

|

|

|

|

Date received |

|

|

• Please print. • Use only blue or black ink. • See additional information on the back. |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer name |

|

|

|

Identifying number (SSN, BIN, FEIN, etc.) |

|||

|

|

|

|

|

|

||

Spouse’s name, if joint return |

|

|

Spouse’s identifying number (SSN, etc.) |

||||

|

|

|

|

|

|

|

|

Address |

|

|

City |

|

|

State |

ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Check only one:

□

Tax Information Authorization: Checking this box allows the department to disclose your confidential tax information to your designee. You may designate a person, agency, firm, or organization.

Tax Information Authorization: Checking this box allows the department to disclose your confidential tax information to your designee. You may designate a person, agency, firm, or organization.

□

Power of Attorney for Representation: Check this box if you want a person to “represent” you. This means the person may receive confidential information and may make decisions on your behalf. The person you designate must meet the qualifications listed on the back of this form.

Power of Attorney for Representation: Check this box if you want a person to “represent” you. This means the person may receive confidential information and may make decisions on your behalf. The person you designate must meet the qualifications listed on the back of this form.

For □

All tax years, or □

All tax years, or □

Specific tax years: __________________________________________________________________ ,

Specific tax years: __________________________________________________________________ ,

I hereby appoint the following person as designee or authorized representative:

Name |

|

Phone |

|

|

Fax |

|

|

|

|

( |

) |

|

( |

) |

|

|

|

|

|

|

|

|

|

Mailing address |

City |

|

State |

|

ZIP code |

||

|

|

|

|

|

|

|

|

Representative’s title and Oregon license number or relationship to taxpayer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If |

|

|

|

|

|

||

The above named is authorized to receive my confidential tax information and/or represent me before the Oregon Department of Revenue for:

□

All tax matters, or

All tax matters, or

□

Specific tax matters. Enter tax program name(s):________________________________________________________________________

Specific tax matters. Enter tax program name(s):________________________________________________________________________

Signature of taxpayer(s)

•I acknowledge the following provision: Actions taken by an authorized representative are binding, even if the representative is not an attorney. Proceedings cannot later be declared legally defective because the representative was not an attorney.

•Corporate officers, partners, fiduciaries, or other qualified persons signing on behalf of the taxpayer(s): By signing, I also certify that I have the authority to execute this form.

•If a tax matter concerns a joint return, both spouses must sign if joint representation is requested. Taxpayers filing jointly may authorize separate representatives.

Signature |

Print name |

|

Date |

|

X |

|

|

|

|

Title (if applicable) |

|

Daytime phone |

||

|

|

( |

) |

|

|

|

|

|

|

Spouse (if joint representation) |

Print name |

|

Date |

|

X |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: This authorization form automatically revokes and replaces all earlier tax authorizations and/or all earlier powers of attorney on file with the Oregon Department of Revenue for the same tax matters and years or periods covered by this form. If you do not want to revoke a prior authorization, initial here ______.

Attach a copy of any other tax information authorization or power of attorney you want to remain in effect.

Complete the following, if known (for routing purposes only):

Revenue employee:__________________________________________________

Division/Section: ____________________________________________________

Phone/Fax: _________________________________________________________

Send to: Oregon Department of Revenue 955 Center St NE

Salem OR

Visit www.oregon.gov/dor to complete this form using Revenue Online.

If this tax information authorization or power of attorney form is not signed, it will be returned.

Power of attorney forms submitted with Revenue Online will be signed electronically.

Additional information

This form is used for two purposes:

•Tax information disclosure authorization. You authorize the department to disclose your confidential tax infor- mation to another person. This person will not receive original notices we send to you.

•Power of attorney for representation. You authorize another person to represent you and act on your behalf. The person must meet the qualifications below. Unless you specify differently, this person will have full power to do all things you might do, with as much binding effect, including, but not limited to: providing information; pre- paring, signing, executing, filing, and inspecting returns and reports; and executing statute of limitation extensions and closing agreements.

This form is effective on the date signed. Authorization termi- nates when the department receives written revocation notice or a new form is executed (unless the space provided on the front is initialed indicating that prior forms are still valid).

Unless the appointed representative has a fiduciary relation- ship to the taxpayer (such as personal representative, trustee, guardian, conservator), original Notices of Deficiency or Assessment will be mailed to the taxpayer as required by law. A copy will be provided to the appointed representative when requested.

For corporations, “taxpayer” as used on this form, must be the corporation that is subject to Oregon tax. List fiscal years by year end date.

Qualifications to represent taxpayer(s) before Department of Revenue

Under Oregon Revised Statute (ORS) 305.230 and Oregon Administrative Rule (OAR)

1.For all tax programs:

a.An adult immediate family member (spouse, parent, child, or sibling).

b.An attorney qualified to practice law in Oregon.

c.A certified public accountant (CPA) or public accoun- tant (PA) qualified to practice public accountancy in Oregon, and their employees.

d.An IRS enrolled agent (EA) qualified to prepare tax returns in Oregon.

e.A designated employee of the taxpayer.

f.An officer or

g.A

h.An individual outside the United States if representa- tion takes place outside the United States.

2.For income tax issues:

a.All those listed in (1); plus

b.A licensed tax consultant (LTC) or licensed tax pre- parer (LTP) licensed by the Oregon State Board of Tax Practitioners.

3.For ad valorem property tax issues:

a.All those listed in (1); plus

b.An Oregon licensed real estate broker or a principal real estate broker; or

c.An Oregon certified, licensed, or registered appraiser; or

d.An authorized agent for designated utilities and com- panies assessed by the department under ORS 308.505 through 308.665 and ORS 308.805 through 308.820.

4.For forestland and timber tax issues:

a.All those listed in (1), (2), and (3)(b) and (c); plus

b.A consulting forester.

An individual who prepares and either signs your tax return or who is not required to sign your tax return (by the instruc- tions or by rule), may represent you during an audit of that return. That individual may not represent you for any other purpose unless they meet one of the qualifications listed above.

Generally, declarations for representation in cases appealed beyond the Department of Revenue must be in writing to the Tax Court Magistrate. A person recognized by a Tax Court Magistrate will be recognized as your representative by the department.

Tax matters partners and S corporation shareholders. See OARs

Attorneys may contact the Oregon State Bar for information on practicing in Oregon. If your

CPAs may practice in Oregon if they meet the following substantial equivalency requirements of ORS 673.010:

1.Licensed in another state;

2.Have an accredited baccalaureate degree with at least 150 semester hours of college education;

3.Passed the Uniform CPA exam; and

4.Have a minimum of one year experience.

Have questions? Need help?

General tax information |

www.oregon.gov/dor |

|

Salem |

(503) |

|

1 (800) |

||

Asistencia en español: |

|

|

En Salem o fuera de Oregon |

(503) |

|

Gratis de prefijo de Oregon |

1 (800) |

|

TTY (hearing or speech impaired; machine only): |

|

|

Salem area or outside Oregon |

(503) |

|

1 (800) |

||

Americans with Disabilities Act (ADA): Call one of the help numbers above for information in alternative formats.

| Fact Name | Detail |

|---|---|

| Purpose | The Tax POA 150-800-005 form is used to appoint a representative for tax matters in Oregon. |

| Governing Law | This form complies with Oregon Revised Statutes, specifically ORS 305.230. |

| Eligibility | Any individual, business, or entity can designate a representative using this form. |

| Submission Method | The completed form can be submitted by mail or fax to the Oregon Department of Revenue. |

Filling out the Tax POA 150-800-005 form is a straightforward process. Once completed, you can submit it to authorize your chosen representative to handle your tax matters. Follow these steps to ensure accurate completion of the form.

After filling out the form, review it for accuracy before submitting. Keep a copy for your records.

The Tax POA 150-800-005 form is a Power of Attorney document used in tax matters. This form allows you to authorize another individual—often a tax professional—to act on your behalf in dealings with tax authorities, such as the IRS or state revenue agencies. It typically applies during situations like tax audits, appeals, or when you need assistance with tax return preparation.

You can appoint any competent individual as your representative using this form. This includes certified public accountants, enrolled agents, or any trusted person, such as a family member or friend. The person you choose must be willing and capable of handling your tax matters responsibly.

Filling out the form involves several key steps:

Yes, you can revoke the Power of Attorney at any time. To do this, you should submit a written statement of revocation to the tax agency and provide a copy to your authorized representative. It is important to ensure that all parties understand the revocation to avoid any potential misunderstandings.

The Power of Attorney generally remains in effect until you revoke it, the designated representative withdraws, or until the purpose of the authorization has been completed. In cases where you specify a limited time frame on the form, it will remain effective only for that duration.

Yes, your completed Tax POA 150-800-005 form must be submitted to the appropriate tax authority. Depending on the state or situation, some agencies may require a copy to process your authorization officially.

Typically, there is no fee associated with filing a Power of Attorney form like the Tax POA 150-800-005. However, if you are seeking the assistance of a tax professional to complete or submit the form, they may charge a fee for their services.

If your authorized representative is unable to act, you may appoint another person by completing a new Tax POA 150-800-005 form. Ensure that the previous authorization is revoked to prevent any confusion about who has the authority to represent you.

The Tax POA 150-800-005 form can usually be obtained directly from the website of your state revenue agency or the IRS. Physical copies may also be available by contacting the office directly or visiting in person.

When filling out the Tax Power of Attorney (POA) 150-800-005 form, it's essential to pay attention to detail. Many individuals make common mistakes that can be easily avoided. Understanding these pitfalls can help ensure the form is completed correctly.

One common mistake is leaving out important personal information. The form requires details such as your name, address, and taxpayer identification number. Omitting any of these can lead to processing delays or even rejection of the form. Always double-check that all fields are filled in correctly.

Another issue arises when signatories fail to sign or date the form. A signature is a crucial component, as it validates the document. Without it, the form lacks legal standing. Make sure to sign at the designated space and include the date of signing. A quick review can save time and headaches later.

Using incorrect or outdated information can lead to complications. Some people may use an old address or an incorrect version of the form. Always ensure that you have the latest version of the 150-800-005 form, and that all provided information is current and accurate.

Incomplete authorization is another frequent error. The form allows you to specify the extent of the authority granted. Many individuals leave this section blank or fail to indicate specific powers. This can create confusion about what the authorized person can or cannot do. Clearly state the powers you are granting.

Failure to provide proper identification for the representative can also lead to problems. If you are granting power of attorney to someone else, their identification must be included. Without it, tax authorities may not recognize the representative when they attempt to act on your behalf.

It's also a mistake to assume that the form does not need to be filed with the IRS. Some people think submitting it only to state tax authorities is sufficient. This is not the case, and not filing with the IRS can lead to complications down the road. Understand where to submit the form to avoid issues.

Lastly, some overlook the importance of keeping copies of the submitted form. After filling it out, keep a copy for your records. This can prove invaluable if questions or disputes arise later. A simple precaution can provide peace of mind.

By being mindful of these common mistakes while completing the Tax POA 150-800-005 form, you can help ensure it is processed without unnecessary delays or issues. Always take your time, review your submissions, and seek clarification if needed.

The Tax Power of Attorney (POA) 150-800-005 form is a key document that allows an individual to designate another person to handle their tax matters with the state. There are several other forms and documents that are commonly used in conjunction with this form to ensure a smooth tax process. Below is a brief description of these documents.

Understanding these documents can greatly facilitate tax management for individuals. Each serves a unique purpose, yet they work together to provide clear authority and ensure all tax matters are appropriately handled.

When filling out the Tax POA 150-800-005 form, here are some helpful dos and don'ts to keep in mind:

The Tax POA 150-800-005 form is an important tool for taxpayers who wish to authorize someone else to act on their behalf regarding tax matters. However, misinformation regarding this form is common. Here are ten misconceptions, clarified for better understanding:

Understanding the facts about the Tax POA 150-800-005 form can empower taxpayers to make informed decisions. Clear representation can alleviate many tax-related stressors.

When preparing to fill out and use the Tax POA 150-800-005 form, it's essential to keep certain points in mind. This will ensure that the process is smooth and efficient.

By adhering to these key takeaways, you can ensure that the process of using the Tax POA 150-800-005 form will be clear and effective.