The Tax POA 151 form plays a vital role in the relationship between taxpayers and their representatives, facilitating smooth communication and legal representation when dealing with the Internal Revenue Service (IRS). Through this form, individuals can authorize another person, typically an accountant or tax professional, to act on their behalf in tax matters. This delegation of authority is not only a matter of convenience; it also ensures that experts can navigate the complexities of tax obligations effectively. The form includes essential sections where taxpayers provide their personal information, designate the representative, outline the specifics of the authority granted, and indicate the duration of this authorization. By completing the Tax POA 151, taxpayers empower their representatives to handle discussions with the IRS, receive confidential information, and even negotiate settlements—a process that can often feel daunting when approached alone. Understanding this form is crucial for anyone looking to simplify their tax interactions while ensuring compliance with tax laws.

Michigan Department of Treasury |

Issued under authority of Public Act 122 of 1941. |

151 (Rev. |

|

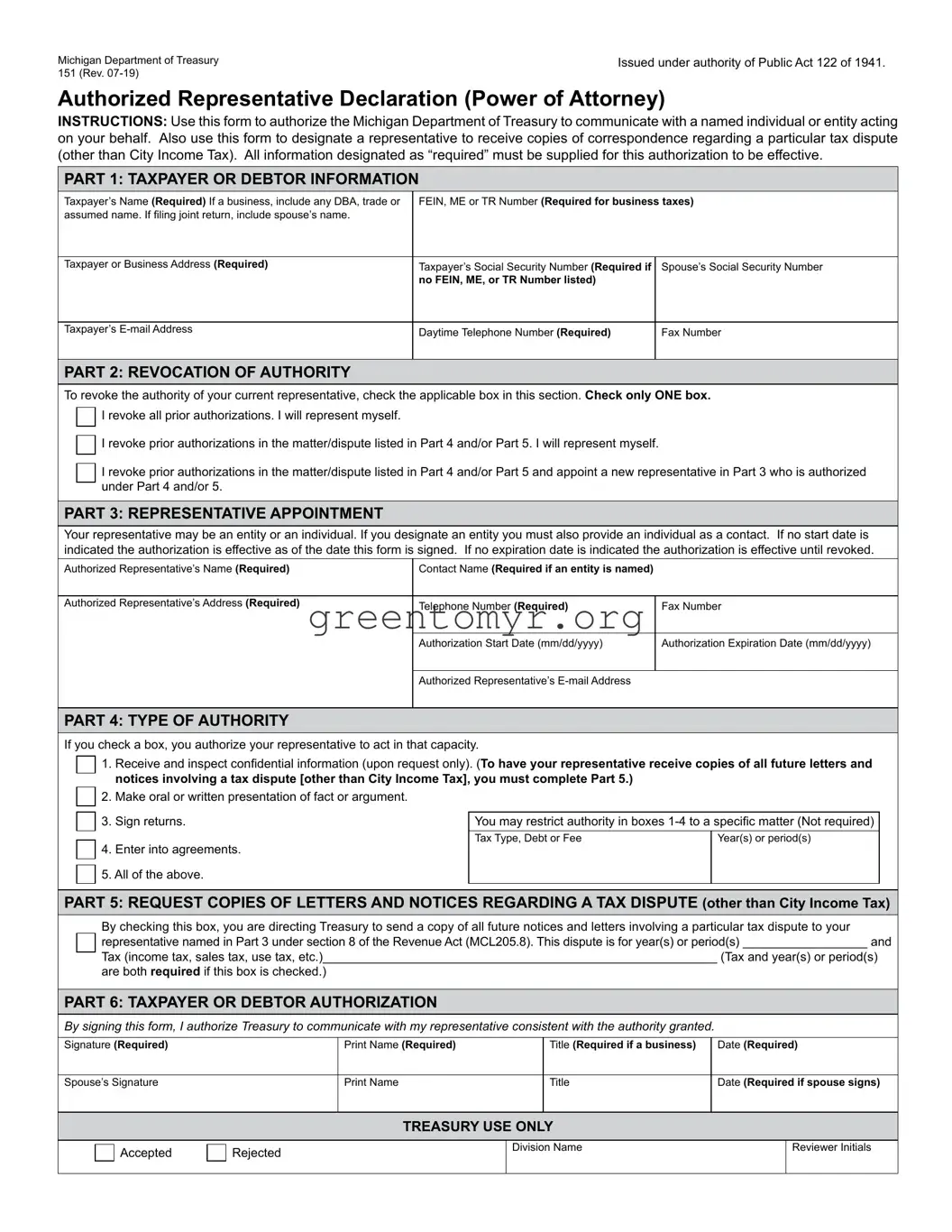

Authorized Representative Declaration (Power of Attorney)

INSTRUCTIONS: Use this form to authorize the Michigan Department of Treasury to communicate with a named individual or entity acting on your behalf. Also use this form to designate a representative to receive copies of correspondence regarding a particular tax dispute (other than City Income Tax). All information designated as “required” must be supplied for this authorization to be effective.

PART 1: TAXPAYER OR DEBTOR INFORMATION

Taxpayer’s Name (Required) If a business, include any DBA, trade or |

FEIN, ME or TR Number (Required for business taxes) |

|

assumed name. If filing joint return, include spouse’s name. |

|

|

|

|

|

Taxpayer or Business Address (Required) |

Taxpayer’s Social Security Number (Required if |

Spouse’s Social Security Number |

|

no FEIN, ME, or TR Number listed) |

|

|

|

|

Taxpayer’s |

Daytime Telephone Number (Required) |

Fax Number |

|

|

|

PART 2: REVOCATION OF AUTHORITY

To revoke the authority of your current representative, check the applicable box in this section. Check only ONE box. □

I revoke all prior authorizations. I will represent myself.

I revoke all prior authorizations. I will represent myself.

□

I revoke prior authorizations in the matter/dispute listed in Part 4 and/or Part 5. I will represent myself.

I revoke prior authorizations in the matter/dispute listed in Part 4 and/or Part 5. I will represent myself.

□ I revoke prior authorizations in the matter/dispute listed in Part 4 and/or Part 5 and appoint a new representative in Part 3 who is authorized under Part 4 and/or 5.

PART 3: REPRESENTATIVE APPOINTMENT

Your representative may be an entity or an individual. If you designate an entity you must also provide an individual as a contact. If no start date is indicated the authorization is effective as of the date this form is signed. If no expiration date is indicated the authorization is effective until revoked.

Authorized Representative’s Name (Required) |

Contact Name (Required if an entity is named) |

|

|

|

|

Authorized Representative’s Address (Required) |

Telephone Number (Required) |

Fax Number |

|

|

|

|

Authorization Start Date (mm/dd/yyyy) |

Authorization Expiration Date (mm/dd/yyyy) |

|

|

|

|

Authorized Representative’s |

|

|

|

|

PART 4: TYPE OF AUTHORITY

If you check a box, you authorize your representative to act in that capacity. |

|

|

|||||

|

|

|

1. |

Receive and inspect confidential information (upon request only). (To have your representative receive copies of all future letters and |

|

||

|

□ |

|

|

||||

|

|

|

notices involving a tax dispute [other than City Income Tax], you must complete Part 5.) |

|

|

||

|

□ |

|

2. |

Make oral or written presentation of fact or argument. |

|

|

|

|

|

|

|

|

|

|

|

|

□ |

|

3. |

Sign returns. |

You may restrict authority in boxes |

|

|

|

|

|

|

Tax Type, Debt or Fee |

Year(s) or period(s) |

|

|

|

□ |

|

4. |

Enter into agreements. |

|

|

|

|

|

5. All of the above. |

|

|

|

||

|

□ |

|

I |

I |

I |

||

|

|

|

|

|

|

|

|

PART 5: REQUEST COPIES OF LETTERS AND NOTICES REGARDING A TAX DISPUTE (other than City Income Tax)

By checking this box, you are directing Treasury to send a copy of all future notices and letters involving a particular tax dispute to your

□ representative named in Part 3 under section 8 of the Revenue Act (MCL205.8). This dispute is for year(s) or period(s) __________________ and

Tax (income tax, sales tax, use tax, etc.)_________________________________________________________ (Tax and year(s) or period(s)

are both required if this box is checked.)

PART 6: TAXPAYER OR DEBTOR AUTHORIZATION

By signing this form, I authorize Treasury to communicate with my representative consistent with the authority granted.

Signature (Required) |

Print Name (Required) |

Title (Required if a business) |

Date (Required) |

Spouse’s Signature |

Print Name |

Title |

Date (Required if spouse signs) |

TREASURY USE ONLY

□ Accepted |

□ Rejected |

Division Name |

Reviewer Initials |

I |

I |

Form 151, Page 2

Purpose

Use the Authorized Representative Declaration (Power of Attorney) (Form 151) to authorize the Michigan Department of Treasury (Treasury) to communicate with a named individual or entity acting on your behalf. This form may also be used to revoke your representative’s authority or to designate a representative to receive letters and notices regarding a particular tax dispute.

Required information. If a box includes the word “Required,” you must provide the information. If a box does not contain the required information, the form is invalid and you will be notified by letter.

Part 2: Revoking the authority of a representative. Complete Part 2 if you want to revoke your representative’s authority in whole or in part or all prior authorizations. After you revoke your representative’s authority, you may represent yourself, or you may appoint a new representative.

Part 3: Appointing an entity as your representative. If you appoint an entity as your representative, then any individual within that entity is authorized to act on your behalf. For example, if you appoint the XYZ Law Firm as your representative, any attorney or paralegal from that firm is authorized to act on your behalf. The “Contact Name” is only to ensure that information sent to the entity is directed to the individual overseeing your representation. The contact name is NOT your sole authorized representative. To appoint an entity, write in the Name and Address box (for example):

XYZ Law Firm 1234 Street

City, State, ZIP Code

Appointing an individual as your representative. If you appoint a specific individual as your representative, then only that individual is authorized to act on your behalf. Treasury will only discuss with or disclose information to that individual. For example, if a specific attorney at the XYZ Law Firm is named as your representative, Treasury will not discuss with or disclose information to any other attorney or paralegal at the same firm. To appoint an individual, write in the Name and Address box (for example):

Lynn Lee XYZ Law Firm 1234 Street

City, State, ZIP Code

Part 4: Type of authority: General or limited. You may grant your representative general or limited authority to act on your behalf. The actions that your representative may take will depend on the boxes that you check in Part 4. Confidential information (box 1) will only be provided upon request; Treasury will not automatically send confidential information to your representative. If you check box 5 in Part 4, you are granting your representative general authority to act on your behalf regarding any tax return and any debt. However, granting your representative general authority does not give the representative the right to receive future copies of letters and notices unless Part 5 is also completed.

Part 5: Requesting copies of letters and notices with respect to a tax dispute.

NOTE: This part does not apply to City Income Tax.

If you complete Part 5, you must identify on the line in Part 5 a single tax matter that is in dispute. The dispute may cover more than one tax period or year. If you have more than one dispute with Treasury and want your representative to receive copies of future notices and letters with respect to those additional disputes, you must fill out a separate form for each dispute. Part 5 does not give a representative authority to act on your behalf. You must give your representative authority to act on your behalf by checking one or more boxes in Part 4 if you want your representative to do more than just receive future notices and letters. Only one representative can be authorized to receive future letters and notices regarding a specific tax dispute under Part 5. Treasury will only send future letters and notices to the person identified on the most recent form. If you appoint an entity as your representative, future letters and notices will be sent to the attention of the first “Contact Name.”

Deceased taxpayer. Do not use this form for a deceased taxpayer. File a Claim for Refund Due a Deceased Taxpayer

MAILING OR FAXING INSTRUCTIONS

Individual taxpayers:

Michigan Department of Treasury

Customer Contact Center

Individual Correspondence Section

P.O. Box 30058

Lansing, Ml 48909

Fax:

When Treasury Collections asks for this form and any attachments:

Michigan Department of Treasury — Coll

P.O. Box 30149

Lansing, Ml 48909

Fax:

When a Treasury field office representative asks for this form, send it as directed by that office.

For all others:

Michigan Department of Treasury

Customer Contact Center

Registration Section

P.O. Box 30778

Lansing, Ml 48909

| Fact Name | Details |

|---|---|

| Form Purpose | The Tax POA 151 form is used to authorize a representative to act on behalf of a taxpayer in matters related to tax return filings and communications with the tax authorities. |

| Governing Law | This form is governed by the Internal Revenue Code (IRC) for federal tax purposes, and by specific state laws for state tax purposes. |

| Eligibility | Any individual taxpayer, whether an individual, business, or organization, can use this form to designate a representative. |

| Notarization | In some states, notarization may be required for the form to be valid. Be sure to check the specific requirements for your state. |

| Submission Method | The completed Tax POA 151 form can typically be submitted via mail, fax, or electronically, depending on jurisdictional regulations. |

| Duration of Authority | The authority granted through the POA is generally effective until revoked by the taxpayer or until the assigned task is completed. |

| Revocation Process | Taxpayers may revoke the POA at any time by submitting a written notice to the tax authority and the designated representative. |

| Applicable States | Many states, including California and New York, have their own versions of the POA form. Check the state’s tax authority for specific guidelines. |

After obtaining the Tax POA 151 form, it's important to carefully fill it out. Each section must be completed accurately to ensure proper authorization for tax representation. Following these steps will guide you through the process.

Once you complete these steps, your form will be sent to the tax authority, allowing your designated representative to act on your behalf. Keep a copy for your records just in case you need to reference it later.

The Tax POA 151 form is an official document that grants someone the authority to act on your behalf in tax matters. This power of attorney is specifically intended for use with the Internal Revenue Service (IRS) and allows an appointed individual to receive your tax information and represent you regarding your tax liability.

You can appoint any individual as your representative using the Tax POA 151 form. This could be a family member, friend, tax professional, or attorney. However, it is important to choose someone you trust, as they will have access to your sensitive tax information and can make decisions on your behalf.

You will need to provide several key pieces of information, including:

To submit the Tax POA 151 form, you must send it to the IRS address indicated in the instructions accompanying the form. It can typically be submitted by mail or, in some cases, electronically. Make sure to follow the specific submission guidelines provided by the IRS to ensure it is processed correctly.

The Tax POA 151 form does not have a specific expiration date. However, it may become invalid if you revoke it or if the designated representative is no longer able to serve due to reasons such as death or withdrawal. It’s advisable to periodically review any powers of attorney you have in place and update them as necessary.

Yes, you can revoke the Tax POA 151 form at any time. To do this, you must provide written notice to the IRS and your representative. Additionally, you may need to fill out and submit a specific revocation form, which the IRS provides. Make sure to keep a copy of both the revocation notice and any related documents for your records.

While the Tax POA 151 form grants considerable authority to your representative, it comes with some limitations. The designated individual cannot perform certain actions, such as changing the ownership of your assets or transferring money from your accounts. The authority is specifically limited to matters related to your tax situations, including filing returns and resolving issues with the IRS.

There is no fee for filing the Tax POA 151 form with the IRS. However, if you choose to hire a tax professional or attorney to assist you with the process or represent you, they may charge fees for their services. It’s important to clarify any potential costs with your chosen representative beforehand.

The processing time for the Tax POA 151 form can vary. Typically, it may take several weeks for the IRS to process your submission. You should allow sufficient time and check your IRS account or contact them if you have concerns about the processing status.

The Tax POA 151 form can be found on the IRS website. You can download it directly in PDF format. Ensure you have the most recent version of the form to avoid issues with processing. Additionally, you may find copies of the form at many tax preparation offices or through professional tax representatives.

Filling out the Tax POA 151 form can be a straightforward process, but many people make common mistakes that can delay their tax matters. One frequent error is failing to provide complete information. It’s essential to fill in all the required fields, including the taxpayer's name, Social Security number, and the tax year in question. Omitting any necessary details may lead to the form being rejected or processed incorrectly.

Another mistake is not signing the form. A signature is required to authorize the representative to act on your behalf. Without it, the IRS cannot accept the Power of Attorney. Ensure that you or your representative signs and dates the form before submitting it. Skipping this step is often an oversight but can lead to complications in the authorization process.

Additionally, people sometimes select the wrong type of representation on the form. Understanding who you wish to designate as your representative is crucial. Selecting the appropriate box for the type of representative ensures that the right person has the authority to act on your behalf. This mistake can lead to confusion and delays in handling tax issues.

Finally, failing to keep a copy of the submitted Tax POA 151 can create issues down the line. After filing the form, it's a good practice to retain a copy for your records. This way, if there are any questions or problems about representation later, you'll have the necessary information to address them. Not keeping a copy can make resolving future issues more complex and time-consuming.

When you are dealing with tax matters, the Tax POA 151 form is commonly accompanied by several other documents. Each of these forms plays a specific role in ensuring that your tax affairs are handled smoothly. Below is a list of forms and documents frequently utilized alongside the Tax POA 151.

Understanding these forms and documents is crucial for effective communication with tax professionals and agencies. Having them organized can lead to a smoother process in managing your tax responsibilities.

IRS Form 2848: This form, also known as the Power of Attorney and Declaration of Representative, allows individuals to authorize someone to represent them before the IRS, similar to how the Tax POA 151 is used for state tax matters.

IRS Form 4506: The Request for Copy of Tax Return form allows taxpayers to request copies of their past tax returns, which may be necessary for representation, similar to the documentation requested in a Tax POA.

IRS Form 8821: This form, the Tax Information Authorization, allows individuals to designate someone to receive confidential tax information from the IRS, akin to the permissions granted in the Tax POA 151.

State Tax POA: Each state has its own version of a Power of Attorney form tailored for state tax matters, serving purposes similar to the Tax POA 151 for local tax representation.

Form 1065: The U.S. Return of Partnership Income must be filed by partnerships and includes provisions for authorized representatives, much like the authority outlined in Tax POA documents.

Form 1120: This is the U.S. Corporation Income Tax Return where designated representatives can file on behalf of corporations, reflecting similar delegation seen in the Tax POA 151.

Form 990: Nonprofit organizations use this form to report their financial activities, and designated individuals can act on behalf of the organization, similar to the function of the Tax POA.

Income Tax Return Extensions: Forms filed to request an extension for submitting income tax returns allow representatives to act, paralleling the authority granted in a Tax POA.

Form 843: This form is used for requesting abatement or refund of taxes and can be filed by an authorized representative, similar to the usage of the Tax POA.

Form 8862: This form is for claiming the Earned Income Credit after disallowance and may require representation, reflecting the needs addressed in the Tax POA 151.

When filling out the Tax POA 151 form, following certain guidelines can help ensure accuracy and compliance.

Here are some key things you should do:

Conversely, here are some things to avoid:

The Tax Power of Attorney (POA) 151 form is an essential tool for managing tax matters with the IRS. However, several misconceptions surround its use and importance. Here are eight common misunderstandings about this form:

Understanding these misconceptions can help individuals better navigate their tax situations and empower them to make informed decisions regarding their financial affairs.

Filling out and using the Tax POA 151 form is an important step for taxpayers who wish to authorize someone to represent them before the tax authorities. Here are key takeaways to consider: