The Tax Power of Attorney (POA) 2848a form plays a crucial role in the realm of U.S. tax management. This form allows taxpayers to authorize an individual to represent them before the Internal Revenue Service (IRS) in various matters, including tax returns, audits, and appeals. By designating a representative through this form, taxpayers can ensure their interests are effectively communicated and managed, especially when they are unable to handle tax-related concerns personally. Key aspects of the POA 2848a include specifying the tax matters in which the representative can act, ensuring the confidential information is shared appropriately, and allowing the designated individual access to taxpayer records. Furthermore, the form is valid only for a specific period and can be revoked or modified at any time, providing flexibility for taxpayers. Understanding how to complete and submit this form is essential for anyone looking to simplify their interactions with the IRS, especially during complex situations. By outlining the necessary steps and requirements, this article aims to demystify the Tax POA 2848a form, empowering taxpayers to make informed decisions regarding their tax representation.

|

FORM |

ALABAMA DEPARTMENT OF REVENUE |

|

|

|

2848A |

Power of Attorney |

|

|

||

and Declaration of Representative |

|

|

|||

|

(REV. 2/17) |

|

|

|

|

|

NOTE: If you have questions concerning the completion of this form, please refer to the instructions for Federal |

||||

|

Form 2848 (revised March 2012). Alabama Form 2848A is very similar to the federal form. |

|

|||

|

|

CAUTION: A separate Form 2848A should be completed for each taxpayer. |

|

|

|

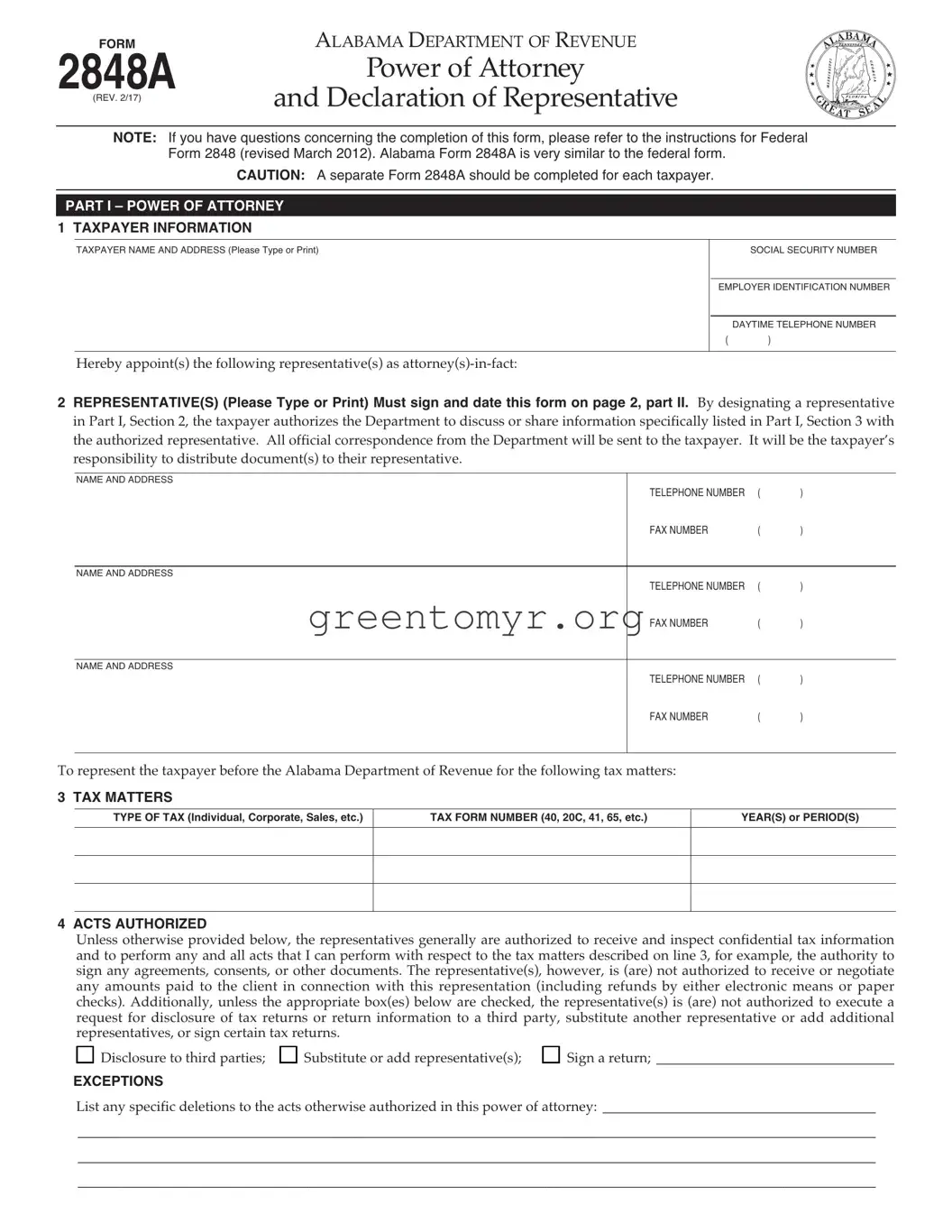

1 TAXPAYER INFORMATION |

|

|

|||

|

TAXPAYER NAME AND ADDRESS (Please Type or Print) |

|

|

SOCIAL SECURITY NUMBER |

|

|

|

|

|

EMPLOYER IDENTIFICATION NUMBER |

|

|

Hereby appoint(s) the following representative(s) as |

|

|

DAYTIME TELEPHONE NUMBER |

|

|

|

( |

) |

||

|

|

|

|

||

|

|

|

|

|

|

2 REPRESENTATIVE(S) (Please Type or Print) Must sign and date this form on page 2, part II. By designating a representative |

||

in Part I, Section 2, the taxpayer authorizes the Department to discuss or share information specifically listed in Part I, Section 3 with |

||

the authorized representative. All official correspondence from the Department will be sent to the taxpayer. It will be the taxpayer’s |

||

responsibility to distribute document(s) to their representative. |

|

|

NAME AND ADDRESS |

|

|

TELEPHONE NUMBER |

( |

) |

FAX NUMBER |

( |

) |

NAME AND ADDRESS |

|

|

TELEPHONE NUMBER |

( |

) |

FAX NUMBER |

( |

) |

NAME AND ADDRESS |

|

|

TELEPHONE NUMBER |

( |

) |

FAX NUMBER |

( |

) |

To represent the taxpayer before the Alabama Department of Revenue for the following tax matters: |

|

|

3 TAX MATTERS |

TAX FORM NUMBER (40, 20C, 41, 65, etc.) |

YEAR(S) or PERIOD(S) |

TYPE OF TAX (Individual, Corporate, Sales, etc.) |

||

4 ACTS AUTHORIZED |

|

Unless otherwise provided below, the representatives generally are authorized to receive and inspect confidential tax information |

|

and to perform any and all acts that I can perform with respect to the tax matters described on line 3, for example, the authority to |

|

sign any agreements, consents, or other documents. The representative(s), however, is (are) not authorized to receive or negotiate |

|

any amounts paid to the client in connection with this representation (including refunds by either electronic means or paper |

|

checks). Additionally, unless the appropriate box(es) below are checked, the representative(s) is (are) not authorized to execute a |

|

request for disclosure of tax returns or return information to a third party, substitute another representative or add additional |

|

representatives, or sign certain tax returns. |

|

Disclosure to third parties; |

Substitute or add representative(s); Sign a return; __________________________________ |

EXCEPTIONS |

|

List any specific deletions to the acts otherwise authorized in this power of attorney: _______________________________________

__________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________

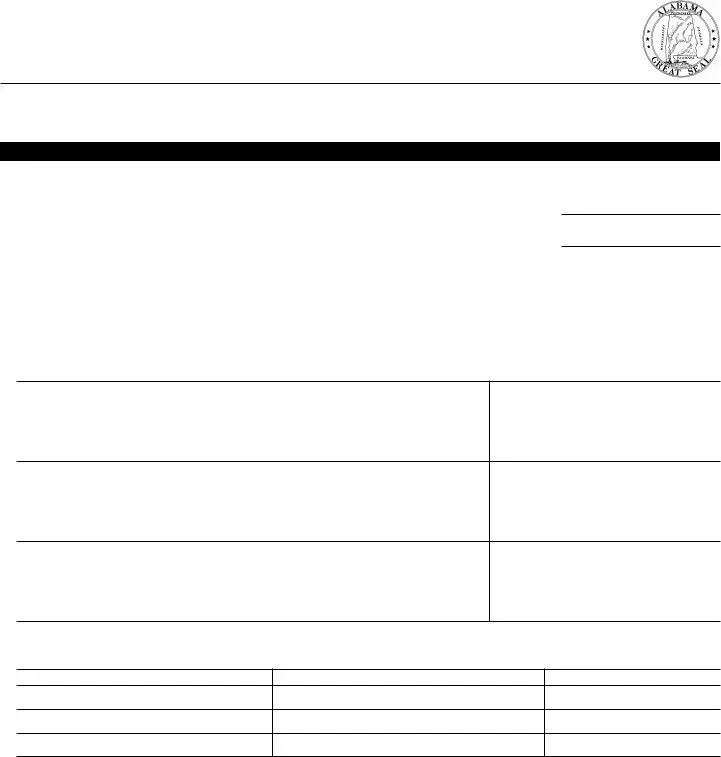

FORM 2848A (REV. 2/17) |

PAGE 2 |

5 RETENTION / REVOCATION OF PRIOR POWER(S) OF ATTORNEY |

|

The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the Alabama |

|

Department of Revenue for the same tax matters and years or periods covered by this document. If you do not want |

|

to revoke a prior power of attorney, check here |

6 SIGNATURE OF TAXPAYEou MuStR AttAch A copY oF ANY power oF AttorNeY You wANt to reMAIN IN eFFect.

If a tax matter concerns a year in which a joint return was filed, the husband and wife must each file a separate power of attorney even if the same representative(s) is (are) being appointed. If signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer.

If this power of attorney is not signed and dated, it will be returned to the taxpayer.

SIGNATURE |

DATE |

TITLE (If Applicable) |

|

|

|

PRINT NAME |

|

|

Under penalties of perjury, I declare that:

• I am not currently under suspension or disbarment from practice before the Internal Revenue Service;

• I am aware of regulations contained in Treasury Department Circular No. 230 (31 CFR, Part 10), as amended, concerning the practice of attorneys, certified public accountants, enrolled agents, enrolled actuaries, and others;

• I am authorized to represent the taxpayer identified in Part I for the tax matter(s) specified there; and

• I am one of the following:

Attorney – a member in good standing of the bar of the highest court of the jurisdiction shown below.

a. Certified Public Accountant – duly qualified to practice as a certified public accountant in the jurisdiction shown below. b. Enrolled Agent – enrolled as an agent under the requirements of Treasury Department Circular No. 230.

c. Officer – a bona fide officer of the taxpayer’s organization. d.

e. Family Member – a member of the taxpayer’s immediate family (i.e., spouse, parent, child, brother, or sister).

f. Enrolled Actuary – enrolled as an actuary by the Joint Board for the Enrollment of Actuaries under 29 U.S.C. 1242 (the g. authority to practice before the Service is limited by section 10.3(d)(1) of Treasury Department Circular No. 230).

Unenrolled Return Preparer – an unenrolled return preparer under section 10.7(c)(1)(viii) of Treasury Department Circular h. No. 230.

Registered Tax Return Preparer – registered as a tax return preparer under the requirements of section 10.4 of Circular 230.

i. Your authority to practice before the Internal Revenue Service is limited. You must have been eligible to sign the return under examination and have signed the return. See Notice

StudentunenrolledAttorneyand returnor CPApreparers– receivesin permissionthe in tructitopracticens. before the IRS by virtue of his/her status as a law, business, or j. accounting student working in LITC or STCP under section 10.7(d) of Circular 230. See instructions for Part II for additional

information and requirements.

Enrolled Retirement Plan Agent – enrolled as a retirement plan agent under the requirements of Circular 230 (the authority to k. practice before the Internal Revenue Service is limited by section 10.3(e)).

If this declaration of representative is not signed and dated, the power of attorney will be returned.

Note: For designations

DESIGNATION – INSERT

ABOVE LETTER

JURISDICTION (State) or

ENROLLMENT CARD NO.

SIGNATURE

DATE

Made fillable by FormsPal.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 2848 is used to authorize an individual to act on your behalf regarding tax matters. |

| Authorized Representative | This form allows you to designate someone, like an attorney or accountant, to represent you before the IRS. |

| Revocation | You can revoke a previously submitted Form 2848 by submitting a new form or a statement to the IRS. |

| Filing Method | The completed form can be submitted by mail or fax to the IRS, depending on the situation. |

| Expiration | The authorization will typically remain in effect unless you revoke it or a specific expiration date is provided. |

| State Specifics | Some states have their own power of attorney forms for tax matters, which must comply with state laws. |

| Signature Requirement | Both you and the representative must sign the form for it to be valid. |

| Information Needed | When filling out the form, you will need to provide your personal details, as well as those of your representative. |

Filling out the Tax POA 2848a form can feel daunting, but with careful attention to detail, it's manageable. After completing the form, you will submit it to the appropriate tax authority for processing. This process allows your designated representative to assist you with tax matters.

The Tax POA 2848a form is a document used to designate a person to represent you before the IRS. This power of attorney form allows your representative to handle tax matters on your behalf, including interacting with the IRS regarding your tax returns, payments, and tax liabilities.

Any individual can be named as your representative on the Tax POA 2848a form. This includes:

Ensure that the person you choose is willing and able to handle your tax matters effectively.

To complete the Tax POA 2848a, you need to provide the following information:

Completing this information accurately is essential for valid representation.

You can submit the completed Tax POA 2848a form to the IRS by mailing it to the address specified in the instructions associated with the form. In some cases, you can also fax it to the appropriate number provided by the IRS, depending on the type of tax matters.

There is no fee for submitting the Tax POA 2848a form to the IRS. However, if you choose to hire a representative, they may charge for their services. Discuss any potential costs with your representative beforehand to avoid surprises.

Filling out the IRS Form 2848, Power of Attorney and Declaration of Representative, can be daunting for many individuals. One common mistake is failing to specify the correct tax matters. The form provides space to designate the type of tax and the years or periods that the power of attorney applies to. Leaving this section blank or providing vague information can lead to confusion and delay in processing.

Another frequent error involves mistakes in the representative's information. It is essential to ensure that the individual granting power of attorney includes the precise name, address, and credentials of the designated representative. A miscommunication here could prevent the representative from properly assisting in tax matters.

Some filers overlook the importance of their own signatures. Both the taxpayer and their spouse, if filing jointly, must sign the form. Neglecting to do so, or using an outdated signature, can result in the IRS rejecting the Power of Attorney entirely, leaving the taxpayer without necessary assistance.

Additionally, incorrect Social Security numbers (SSNs) or Employer Identification Numbers (EINs) can create significant issues. The IRS relies on these numbers to verify identities and link documents to the correct accounts. Any discrepancies can lead to processing delays or complications in communication.

People often forget to check the list of restrictions that can be placed on the powers granted. For those who wish to limit the scope of their representative’s authority, failing to specify these restrictions can give the representative broader powers than intended. This might lead to actions taken that do not align with the taxpayer’s wishes.

Another misstep involves not keeping a copy of the completed form for personal records. Once submitted, taxpayers should have a record of what was filed. This can be crucial for future reference, especially if questions arise or if there are discrepancies with the IRS.

Lastly, timing can be an issue. Submitting the Form 2848 too close to tax deadlines may hinder the representative's ability to act effectively. It’s wise to allow ample time for processing, particularly in busy tax seasons. Recognizing these common pitfalls can help taxpayers navigate the process more smoothly and ensure their interests are effectively represented.

When handling tax matters, especially when dealing with the IRS, it’s important to have the right documents in place. The Tax Power of Attorney form, known as Form 2848, is often accompanied by several other forms that can facilitate a smooth process. Here’s a list of commonly used forms and documents that might accompany the Tax POA 2848 form, providing clarity on their purposes.

Understanding these documents can make your tax preparation process much smoother. Each form serves a unique purpose and ensures you are accurate and compliant with tax laws. Collecting the necessary forms ahead of time can alleviate stress and confusion, especially during tax season.

The Tax Power of Attorney (POA) Form 2848a is a crucial document for taxpayers who wish to authorize someone else to act on their behalf in tax matters. Several other documents serve similar purposes in various legal and financial contexts. Below is a list of seven documents that share similarities with Form 2848a:

Understanding these similar documents is vital for anyone looking to navigate the complexities of legal representation in tax and financial matters. Each plays a unique role but operates under the common theme of delegation and authority.

When filling out the Tax Power of Attorney (POA) Form 2848, there are several important considerations to keep in mind to ensure the process goes smoothly.

The IRS Form 2848, commonly referred to as a Power of Attorney (POA) form, is often misunderstood. Here are six prevalent misconceptions about this important document along with clarifications to enhance understanding.

In reality, the POA only authorizes the agent to represent you for tax matters with the IRS. Their powers are limited to the specific actions you grant them, such as filing returns or discussing your tax situation.

Actually, you can designate multiple individuals as your agents, as long as you clearly outline each person's responsibilities. However, having too many agents may complicate communication and action.

The process is fairly straightforward. You simply need to fill out the form and submit it to the IRS. Include all required signatures and information to ensure prompt processing.

You can revoke the POA at any time by submitting a revocation form to the IRS. Take charge of your financial representation based on your changing needs and preferences.

The authority granted through the POA is specific to tax matters. Your agent can access tax records and handle relevant issues, but not personal financial information outside of tax-related contexts.

In fact, any taxpayer can benefit from designating a representative, regardless of their financial situation. It streamlines communication with the IRS, ensuring that your interests are effectively represented.

Understanding the nuances of the IRS Form 2848 can significantly empower individuals when dealing with tax matters. It helps create an informed taxpayer who can better navigate the complexities of the tax system.

The following are key takeaways regarding the Tax Power of Attorney (POA) 2848a form: