The IRS Form 2848, also known as the Power of Attorney and Declaration of Representative, is an essential document for individuals seeking representation in tax matters. This form allows taxpayers to authorize an attorney, certified public accountant, or enrolled agent to act on their behalf before the IRS. When completing the form, it’s crucial to include specific information such as the taxpayer’s details, the type of tax involved, and the years or periods for which representation is granted. Additionally, the authorized representative must provide their own information and declaration, affirming their qualifications to represent the taxpayer. Understanding this process alleviates potential confusion and ensures that your tax issues are handled efficiently. Anyone facing IRS challenges should consider utilizing this important tool to secure knowledgeable assistance in navigating complex tax matters.

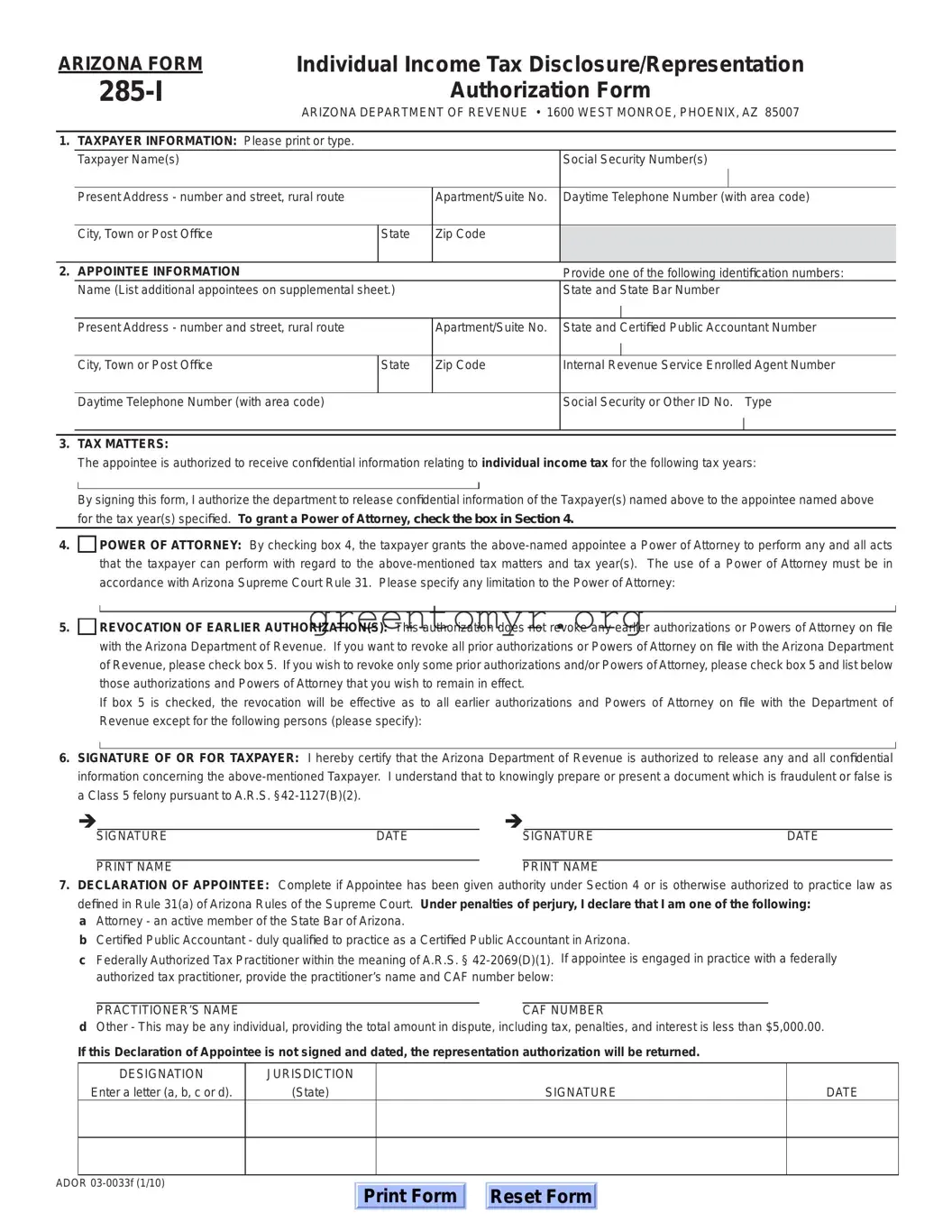

ARIZONA FORM |

Individual Income Tax Disclosure/Representation |

|

|

Authorization Form |

|

|

|

ARIZONA DEPARTMENT OF REVENUE • 1600 WEST MONROE, PHOENIX, AZ 85007 |

|

|

|

1. TAXPAYER INFORMATION: Please print or type. |

||

|

Taxpayer Name(s) |

Social Security Number(s) |

Present Address - number and street, rural route

Apartment/Suite No.

Daytime Telephone Number (with area code)

City, Town or Post Office

State

Zip Code

2. APPOINTEE INFORMATION |

|

|

Provide one of the following identification numbers: |

|

|

Name (List additional appointees on supplemental sheet.) |

|

State and State Bar Number |

|

|

|

|

|

| |

|

Present Address - number and street, rural route |

|

Apartment/Suite No. |

State and Certified Public Accountant Number |

|

|

|

|

| |

|

City, Town or Post Office |

State |

Zip Code |

Internal Revenue Service Enrolled Agent Number |

|

|

|

|

|

|

Daytime Telephone Number (with area code) |

|

|

Social Security or Other ID No. Type |

|

|

|

|

| |

|

|

|

|

|

3.TAX MATTERS:

The appointee is authorized to receive confidential information relating to individual income tax for the following tax years:

By signing this form, I authorize the department to release confidential information of the Taxpayer(s) named above to the appointee named above for the tax year(s) specified. To grant a Power of Attorney, check the box in Section 4.

4.

POWER OF ATTORNEY: By checking box 4, the taxpayer grants the

5.

REVOCATION OF EARLIER AUTHORIZATION(S): This authorization does not revoke any earlier authorizations or Powers of Attorney on file with the Arizona Department of Revenue. If you want to revoke all prior authorizations or Powers of Attorney on file with the Arizona Department of Revenue, please check box 5. If you wish to revoke only some prior authorizations and/or Powers of Attorney, please check box 5 and list below those authorizations and Powers of Attorney that you wish to remain in effect.

If box 5 is checked, the revocation will be effective as to all earlier authorizations and Powers of Attorney on file with the Department of Revenue except for the following persons (please specify):

6.SIGNATURE OF OR FOR TAXPAYER: I hereby certify that the Arizona Department of Revenue is authorized to release any and all confidential information concerning the

Î |

|

|

Î |

|

|

||

|

|

SIGNATURE |

DATE |

|

|

SIGNATURE |

DATE |

|

|

|

|

|

|

||

|

PRINT NAME |

|

PRINT NAME |

|

|||

7.DECLARATION OF APPOINTEE: Complete if Appointee has been given authority under Section 4 or is otherwise authorized to practice law as defined in Rule 31(a) of Arizona Rules of the Supreme Court. Under penalties of perjury, I declare that I am one of the following:

a Attorney - an active member of the State Bar of Arizona.

b Certified Public Accountant - duly qualified to practice as a Certified Public Accountant in Arizona.

c Federally Authorized Tax Practitioner within the meaning of A.R.S. §

PRACTITIONER’S NAME |

CAF NUMBER |

dOther - This may be any individual, providing the total amount in dispute, including tax, penalties, and interest is less than $5,000.00.

If this Declaration of Appointee is not signed and dated, the representation authorization will be returned.

DESIGNATION

Enter a letter (a, b, c or d).

JURISDICTION

(State)

SIGNATURE

DATE

ADOR

Print Form

Reset Form

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA 285-I form is used to establish a Power of Attorney for individuals or businesses to designate someone to act on their behalf regarding tax matters. |

| Who Can Use It | Any taxpayer, whether an individual or entity, can use this form to appoint a representative for tax-related issues. |

| Governing Law | This form is governed by the Internal Revenue Code and applicable state tax laws where the taxpayer resides or operates. |

| Filing Requirement | The form must be completed and submitted to the relevant tax authority to be valid. This may include both federal and state submissions. |

| Duration | The authority granted by the form remains in effect until revoked by the taxpayer or until a specified expiration date is reached. |

| Information Needed | Taxpayer information, representative details, and the specifics of the powers granted must all be clearly outlined on the form. |

| Revocation | The taxpayer can revoke the Power of Attorney at any time by submitting a written notice to the appropriate tax authority. |

| Signature Requirement | Both the taxpayer and the appointed representative must sign the form for it to be legally binding. |

| Submission Format | The form can typically be submitted electronically for federal tax purposes, but state-specific submission methods may vary. |

Filling out the Tax POA 285-I form is a straightforward process that ensures you're prepared to authorize someone to act on your behalf regarding tax matters. After you've completed the form, you'll need to submit it following the specific instructions provided by the tax agency. It’s important to ensure that all information is accurate to avoid any delays in processing.

The Tax POA 285-I form is a Power of Attorney form that allows individuals to designate someone else to represent them concerning tax matters before the IRS. This form authorizes the appointed individual to handle specific tax-related tasks on behalf of the taxpayer.

You can designate any individual as your representative. This can include tax professionals such as CPAs, attorneys, or enrolled agents. It is important to choose someone you trust who is knowledgeable about tax matters.

Yes, the POA 285-I form requires you to specify the tax matters your representative is authorized to handle. This could include income tax, employment tax, or other specific issues. Clearly outlining these matters helps ensure that your representative understands their authority.

No, there is no fee for filing the Tax POA 285-I form with the IRS. However, if you choose a paid representative, they may charge you for their services.

You may submit the POA 285-I form by mailing it to the appropriate IRS office, or you can submit it electronically if your representative has authorization. Check the IRS website or contact the agency for details on submission methods.

Yes, you can revoke the Power of Attorney at any time. To do so, you must submit a written statement to the IRS informing them of the revocation. It is also a good practice to notify your representative if you decide to revoke their authority.

If you feel that your representative is not acting in your best interest, you have the right to revoke their Power of Attorney using the proper procedures. You can also contact the IRS to report any misconduct.

The POA 285-I form remains valid until you revoke it or until your representative can no longer act on your behalf (e.g., due to disability or death). It is advisable to review and update your Power of Attorney regularly.

Yes, you can authorize multiple representatives by completing the form for each individual. However, ensure that each representative has a designated role to avoid confusion regarding authority.

You can find the Tax POA 285-I form on the IRS official website. It is available for download in PDF format, and you can print it out for completion.

Filling out the IRS Form 2848, often referred to as the Power of Attorney (POA) form, might seem straightforward, but many people trip over common pitfalls. One crucial mistake individuals often make is forgetting to include the correct **authorization code**. Without this code, the IRS may reject the form, leaving the individual without representation. Ensuring this code is present is vital for the authority to be recognized.

Another frequent blunder is neglecting to sign the form. It's easy to overlook, but without a valid signature, the form can’t be processed. If multiple individuals are involved, each must provide their signature. Rushing through the process often leads to missing this essential step.

Additionally, using vague or incomplete information for the taxpayer's details can cause complications down the line. This includes missing or incorrect social security numbers, names, or addresses. Accurate information ensures that the IRS can correctly identify the taxpayer, which prevents issues in the future.

The selection of the proper tax matters can also be a point of confusion. People might select broad categories instead of specifically outlining the years or types of returns they are granting access to. Clarity here is key! The IRS needs detailed information to understand what powers are being granted.

Mixing up the types of representation is another common misstep. It’s essential to clearly indicate whether the representation is for a specific issue or for all tax matters. This delineation helps avoid misunderstandings between the taxpayer and the authorized representative.

Failing to provide a valid date can result in additional headaches as well. Each form must be current, and outdated forms can lead to automatic rejections. It's best to double-check the date to ensure all is in order.

Lastly, not keeping a copy of the submitted form is a mistake often made in the rush to submit. Keeping a copy provides a reference for both the taxpayer and the representative and can be crucial should any questions arise later. A simple habit, like saving a copy, saves a lot of trouble in the long run.

The Tax POA 285-I form is commonly used for granting Power of Attorney in tax matters. It allows an individual or business to authorize someone else to represent them before the IRS. Several other forms and documents often accompany this form to ensure completeness and clarity in tax representation. Below is a list of important documents that are frequently associated with the Tax POA 285-I form.

In summary, each of these forms and documents plays a vital role when dealing with tax representation. They help create a clear framework for authorization and ensure that all parties involved can effectively communicate with the IRS.

When filling out the Tax Power of Attorney (POA) 285-I form, it is essential to adhere to specific guidelines to ensure the process goes smoothly. Here's a handy list of things you should and shouldn't do:

Following these guidelines can make the process of authorizing someone to act on your behalf with the IRS much smoother. Being thorough and careful with your information can save you time and stress down the road.

Here are nine common misconceptions about the Tax POA 285-I form along with clarifications to help you better understand its purpose and function.

Understanding these misconceptions can help ensure that taxpayers use the Tax POA 285-I effectively and appropriately.

When filling out and using the Tax POA 285-I form, consider the following key points: