The Tax POA 774 form is a crucial document for individuals seeking to authorize another person to represent them before the Internal Revenue Service (IRS). This form facilitates effective communication between tax professionals or family members and the IRS, ensuring that the necessary tax matters can be addressed efficiently. By completing the Tax POA 774, taxpayers grant authority for the designated representative to handle a range of issues, such as signing tax returns, responding to IRS inquiries, and negotiating settlements. The use of this form streamlines interactions, allowing representatives to advocate on behalf of the taxpayer in various situations. Completing the form requires careful attention to detail, including providing accurate personal information and outlining the specific authority granted. There are also particular rules regarding its validity, so it is essential to stay informed about any changes in IRS regulations that may affect the use of the form. Overall, the Tax POA 774 plays a vital role in simplifying the tax process, making it a valuable tool for those seeking assistance with their tax obligations.

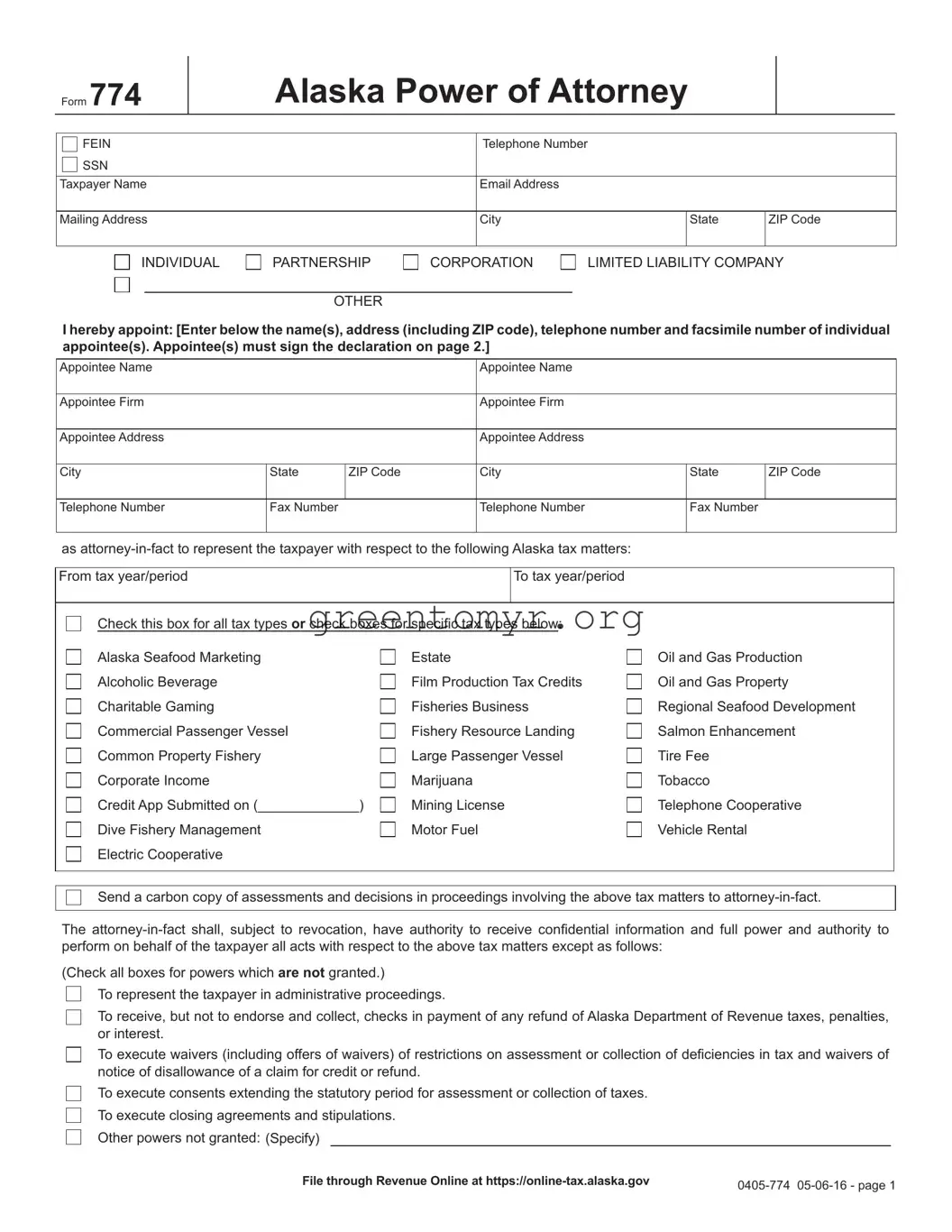

Form 774

Alaska Power of Attorney

FEIN |

Telephone Number |

|

|

SSN |

|

|

|

|

|

|

|

Taxpayer Name |

Email Address |

|

|

|

|

|

|

Mailing Address |

City |

State |

ZIP Code |

|

|

|

|

INDIVIDUAL

PARTNERSHIP

OTHER

CORPORATION

LIMITED LIABILITY COMPANY

I hereby appoint: [Enter below the name(s), address (including ZIP code), telephone number and facsimile number of individual appointee(s). Appointee(s) must sign the declaration on page 2.]

Appointee Name |

|

|

Appointee Name |

|

|

Appointee Firm |

|

|

Appointee Firm |

|

|

Appointee Address |

|

|

Appointee Address |

|

|

City |

State |

ZIP Code |

City |

State |

ZIP Code |

Telephone Number |

Fax Number |

|

Telephone Number |

Fax Number |

|

as

From tax year/period |

|

To tax year/period |

|

|

|

|

|

Check this box for all tax types or check boxes for specific tax types below: |

|

||

Alaska Seafood Marketing |

Estate |

Oil and Gas Production |

|

Alcoholic Beverage |

Film Production Tax Credits |

Oil and Gas Property |

|

Charitable Gaming |

Fisheries Business |

Regional Seafood Development |

|

Commercial Passenger Vessel |

Fishery Resource Landing |

Salmon Enhancement |

|

Common Property Fishery |

Large Passenger Vessel |

Tire Fee |

|

Corporate Income |

Marijuana |

Tobacco |

|

Credit App Submitted on (_____________) |

Mining License |

Telephone Cooperative |

|

Dive Fishery Management |

Motor Fuel |

Vehicle Rental |

|

Electric Cooperative |

|

|

|

|

|

|

|

Send a carbon copy of assessments and decisions in proceedings involving the above tax matters to

The

(Check all boxes for powers which are not granted.)

To represent the taxpayer in administrative proceedings.

To receive, but not to endorse and collect, checks in payment of any refund of Alaska Department of Revenue taxes, penalties, or interest.

To execute waivers (including offers of waivers) of restrictions on assessment or collection of deficiencies in tax and waivers of notice of disallowance of a claim for credit or refund.

To execute consents extending the statutory period for assessment or collection of taxes.

To execute closing agreements and stipulations.

Other powers not granted: (Specify)

File through Revenue Online at |

Form 774

Alaska Power of Attorney

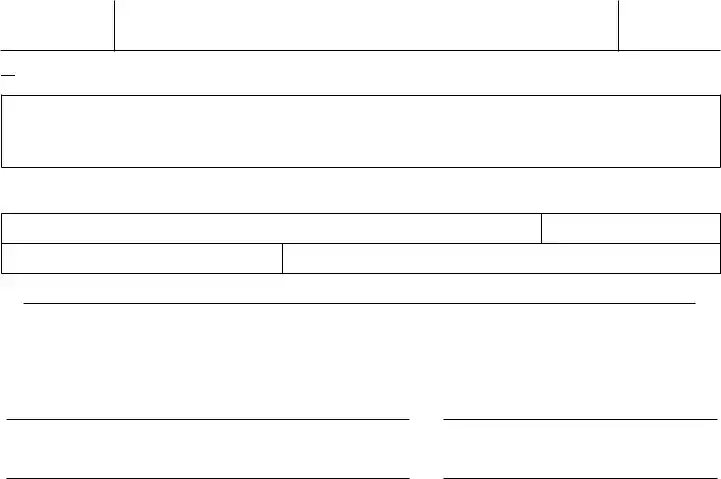

This power of attorney revokes all prior powers of attorney filed with respect to the same matters and years or periods covered by this instrument, except the following: (Specify and attach copies of the powers of attorney)

This power of attorney revokes all prior powers of attorney filed with respect to the same matters and years or periods covered by this instrument, except the following: (Specify and attach copies of the powers of attorney)

Signature of Taxpayer – If signed by a corporate officer, partner, or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power of attorney on behalf of the taxpayer.

Signature |

Date |

Printed Name |

Printed Title |

DECLARATION OF REPRESENTATIVE

The undersigned representative hereby declares under the penalty of unsworn falsification that he/she is an individual authorized to represent a taxpayer before the Department of Revenue and that he/she is authorized to represent the named taxpayer in this matter.

Signature |

Date |

Signature |

Date |

POWER OF ATTORNEY INFORMATION

USE THIS FORM TO GRANT AUTHORITY TO AN INDIVIDUAL TO REPRESENT YOU BEFORE THE DEPARTMENT AND TO RECEIVE TAX INFORMATION.

An individual who is not the taxpayer must be a recognized representative before the individual may represent a taxpayer before the Department of Revenue. A recognized representative is an individual who is appointed as an

A power of attorney is a document signed by the taxpayer by which another individual is given the authority to appear before the department and act for the taxpayer. An

Generally, the power of attorney encompasses all matters relating to a taxpayer’s rights, privileges, or liabilities under laws and regulations administered by the department. This includes, for example, such things as the preparation and filing of necessary documents, receipt of otherwise confidential tax particulars, correspondence and communication with department personnel, and representation of a taxpayer at audits, conferences, hearing, and other meetings.

Forms filed through Revenue Online are considered original forms and do not need to be mailed in. The original of this form, if not filed through Revenue Online, must be mailed to the department.

| Fact Name | Details |

|---|---|

| Form Title | Tax Power of Attorney (POA) Form 774 |

| Purpose | This form allows an individual or entity to designate a representative to handle tax matters with the state. |

| Governing Law | The use of the Tax POA 774 form is governed by the laws of the state in which it is filed. |

| Filing Requirement | This form must be submitted to authorize someone to represent you before the state’s tax agency. |

| Signature Requirement | The individual granting power of attorney must sign the form to validate it. |

| Effective Date | The powers granted become effective upon the signature date unless otherwise specified. |

| Revocation | The authority granted can be revoked at any time by the person who granted it, typically in writing. |

| Limitations | While powerful, the Tax POA 774 does not allow the representative to perform all actions, such as altering tax returns without consent. |

| State-Specific Versions | Some states may have variations of this form, so it’s important to check local requirements. |

| Submission Method | The completed form can often be submitted directly to the tax agency or included with your tax return, depending on state guidelines. |

After completing the Tax POA 774 form, you will need to submit it to the appropriate tax authority. This grants your designated representative the authority to act on your behalf regarding tax matters.

The Tax POA 774 form, formally known as the Power of Attorney for Tax Representation, allows individuals to designate someone else to represent them before the tax authorities, such as the IRS or state tax agencies. This form grants authority to the designated representative to receive information, make inquiries, and represent the taxpayer's interests in various tax matters.

Taxpayers can appoint a wide range of individuals as their representatives. Common choices include tax professionals such as accountants, CPAs, or attorneys. Friends or family members may also serve in this role, but it is essential that the designated person is trustworthy and knowledgeable about tax matters.

To complete the form, an individual must provide personal information, including their name, address, and taxpayer identification number. The form also requires details about the designated representative, such as their name and contact information. Clarity is crucial; ensure that the authority granted is specified clearly, allowing for the representative to act in specific areas related to taxation.

No, the Tax POA 774 form does not require notarization. However, both the taxpayer and the representative must sign the document. Their signatures signify an understanding and agreement to the terms outlined in the form.

The completed Tax POA 774 form can typically be submitted through various methods, depending on the tax agency involved. Common submission methods include mailing the form to the appropriate tax office or, in the case of some states and the IRS, submitting it electronically via their online systems. Check the relevant agency’s guidelines for specific instructions.

Yes, taxpayers have the right to revoke the Tax POA 774 form at any time. To do so, a written revocation should be drafted and sent to the appropriate tax authority. It is also courteous to inform the designated representative of the decision to revoke the power of attorney, so that they are aware of the change in representation.

Should a representative act outside the authority specified in the Tax POA 774 form, the taxpayer may not be liable for any actions taken by the representative that do not comply with the granted Powers. This emphasizes the importance of clearly outlining the areas of authority on the form.

Most tax agencies do not charge a fee for submitting the Tax POA 774 form. However, it is important to verify this with the specific agency, as policies may vary and additional fees could apply if further services are needed from a tax professional or advisor.

When individuals decide to fill out the Tax Power of Attorney (POA) Form 774, they sometimes encounter pitfalls that can lead to delays or complications. One common mistake is not properly identifying the representative. It’s essential for taxpayers to accurately fill in the name and address of the person they are designating. Failing to include complete information or misspelling the representative's name can create significant issues down the line.

Another frequent error is neglecting to specify the tax matters for which the representative has authority. Tax Form 774 requires taxpayers to clearly indicate the specific powers granted. This could range from handling income tax returns to negotiating tax debts. If these details are vague or incomplete, the representative may not have the necessary authority to act on the taxpayer’s behalf.

Additionally, many individuals mistakenly overlook the signature requirement. Each form submitted must be signed by the taxpayer; otherwise, it may be rejected. Taxpayers often assume that a simple oversight won't matter, but without a signature, the authorization is invalid, leaving both the taxpayer and the representative without the necessary legal backing.

Timing can also be an issue. Submitting the form late or at the wrong time can lead to complications. Taxpayers should ensure that the POA is submitted well ahead of deadlines for tax submissions or relevant negotiations. Waiting until the last minute can result in unnecessary stress and possible financial repercussions.

Often, people forget to keep a copy of the submitted form. Retaining a copy is crucial for future reference. It helps in tracking communications and ensures that both the taxpayer and the representative are on the same page regarding the powers granted. Without a duplicate, misunderstandings can arise, leading to complications in their dealings with the tax authorities.

Lastly, one significant oversight is failing to follow up after submission. Taxpayers may assume that everything is in order once the form is sent, but it’s wise to confirm that the IRS has received and processed the POA. Not doing so can lead to situations where the representative is unable to act due to the form not being on file. Proactive communication can prevent future headaches and ensure representation goes smoothly.

The Tax Power of Attorney (POA) 774 form is a crucial document that allows someone to represent you in matters related to taxes. Often, this form is accompanied by other documents that facilitate effective communication and representation with tax authorities. Below is a list of commonly used forms and documents that may be needed alongside the Tax POA 774 form:

Understanding these forms and documents can simplify the tax process and ensure compliance with IRS regulations. Each plays a unique role in representing a taxpayer’s interests effectively.

IRS Form 2848 - Power of Attorney and Declaration of Representative: This form allows a taxpayer to appoint someone to represent them before the IRS. Like the Tax POA 774, it grants authority to act on behalf of the taxpayer, but it is more commonly used for broader tax representations, including audits and appeals.

IRS Form 8821 - Tax Information Authorization: This document allows a designated representative to receive confidential tax information. Although it doesn’t confer authority to represent a taxpayer like the Tax POA 774, it is essential for sharing tax details with third parties.

State Power of Attorney Forms: Similar to the Tax POA 774, state-specific power of attorney forms authorize an agent to handle the taxpayer’s state tax matters. These vary by state but often function in a comparable manner regarding tax representation and authority.

Form 4506 - Request for Copy of Tax Return: While this form serves to obtain copies of tax returns from the IRS, it involves authorization, as the taxpayer must provide consent for a third party to access these documents. This connects to the purpose of the Tax POA 774, which deals with consent and representation.

Form 56 - Notice Concerning Fiduciary Relationship: This document notifies the IRS of a fiduciary relationship and can affect how tax matters are handled for estates and trusts. Its purpose parallels that of the Tax POA 774 in representing the interests of specific taxpayers or beneficiaries.

Filling out the Tax POA 774 form requires careful attention to detail. Here are some valuable tips on what to do and what to avoid:

The Tax POA 774 form, also known as the Power of Attorney, comes with several misconceptions that can lead to confusion. Below are ten common misunderstandings about this important document.

Filling out and using the Tax POA 774 form effectively can be crucial for managing your tax affairs. Here are some key takeaways to keep in mind:

By following these guidelines, you can use the Tax POA 774 form to your advantage and ensure that your tax matters are handled smoothly.