The Tax POA Authorization to Disclose Tax Information form is a critical document for anyone who needs to allow another person to manage their tax matters with the Internal Revenue Service (IRS). This form grants the designated representative, often known as a power of attorney (POA), the authority to receive and discuss tax information on your behalf. It is essential for ensuring that tax-related issues are addressed promptly and efficiently. The form requires specific details, including the taxpayer's name, taxpayer identification number, and the agent's information. Additionally, it covers which tax matters the agent can discuss and for which periods they have the authority. Filling out this form accurately can help prevent delays and complications in handling tax affairs, making it a valuable tool for taxpayers seeking assistance or representation. Understanding this authorization process is vital for anyone looking to streamline their interactions with the IRS and ensure compliance with tax regulations.

CLEAR FORM

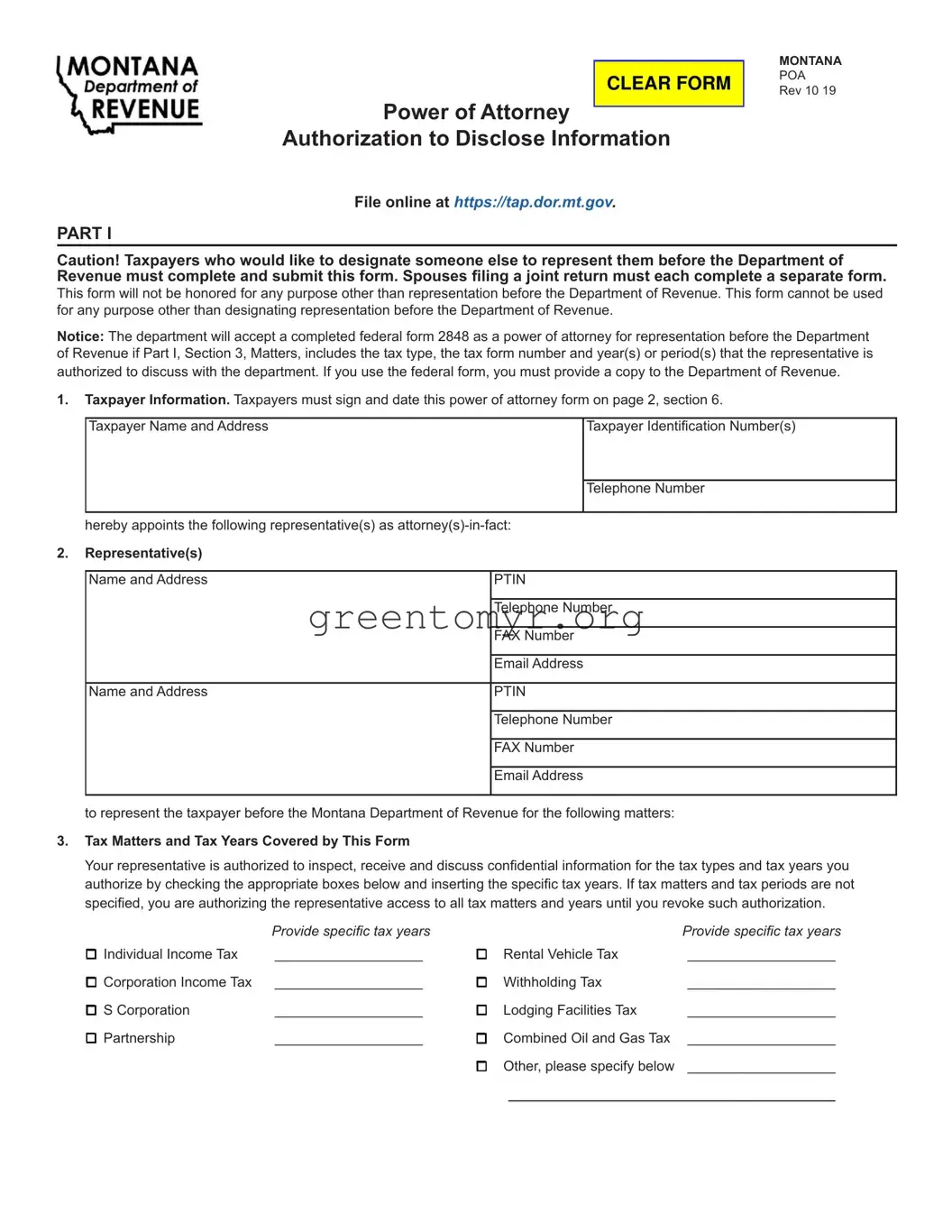

Power of Attorney

Authorization to Disclose Information

File online at https://tap.dor.mt.gov.

PART I

MONTANA POA Rev 10 19

Caution! Taxpayers who would like to designate someone else to represent them before the Department of Revenue must complete and submit this form. Spouses filing a joint return must each complete a separate form.

This form will not be honored for any purpose other than representation before the Department of Revenue. This form cannot be used for any purpose other than designating representation before the Department of Revenue.

Notice: The department will accept a completed federal form 2848 as a power of attorney for representation before the Department of Revenue if Part I, Section 3, Matters, includes the tax type, the tax form number and year(s) or period(s) that the representative is authorized to discuss with the department. If you use the federal form, you must provide a copy to the Department of Revenue.

1.Taxpayer Information. Taxpayers must sign and date this power of attorney form on page 2, section 6.

Taxpayer Name and Address

Taxpayer Identification Number(s)

Telephone Number

hereby appoints the following representative(s) as

2.Representative(s) Name and Address

Name and Address

PTIN

Telephone Number

FAX Number

Email Address

PTIN

Telephone Number

FAX Number

Email Address

to represent the taxpayer before the Montana Department of Revenue for the following matters:

3.Tax Matters and Tax Years Covered by This Form

Your representative is authorized to inspect, receive and discuss confidential information for the tax types and tax years you authorize by checking the appropriate boxes below and inserting the specific tax years. If tax matters and tax periods are not specified, you are authorizing the representative access to all tax matters and years until you revoke such authorization.

|

Provide specific tax years |

|

|

Provide specific tax years |

q Individual Income Tax |

___________________ |

q |

Rental Vehicle Tax |

___________________ |

q Corporation Income Tax |

___________________ |

q |

Withholding Tax |

___________________ |

q S Corporation |

___________________ |

q |

Lodging Facilities Tax |

___________________ |

q Partnership |

___________________ |

q Combined Oil and Gas Tax |

___________________ |

|

|

|

q Other, please specify below |

___________________ |

|

__________________________________________

4.Acts Authorized by This Form

Check the box that best describes what authorization you are delegating to your representative.

q Representation. Department employees can provide confidential information to the representative and discuss the information. q Information sharing. Department employees can provide confidential information to the representative, but cannot discuss

the information.

q

5.Revocation of Prior Power(s) of Attorney

q Check this box if you want all prior POAs revoked.

If you are a representative and want to withdraw an existing POA, write WITHDRAW across the top of the existing form. See instructions on page 3.

6.Signature of taxpayer. If a tax matter concerns a year in which a joint return was filed, the spouses each file a separate power of attorney even if the same representative(s) is(are) appointed. If signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, fiduciary or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form

on behalf of the taxpayer.

If not signed and dated, this power of attorney will not be in effect and the taxpayer will be notified.

_______________________________________ |

____________________ |

__________________________________ |

Signature |

Date |

Title (if applicable) |

_______________________________________ |

|

__________________________________ |

Print Name |

|

Print Taxpayer Name from Line 1 (if other |

|

|

than individual) |

PART II. Declaration of Representative

I declare that:

I am authorized to represent the taxpayer identified in Part I for the matter(s) specified there; and

I am one of the following:

a.Attorney - licensed to practice law in the jurisdiction shown below.

b.Certified Public Accountant - duly qualified to practice as a certified public accountant in the jurisdiction shown below.

c.Enrolled Agent or Licensed Public Accountant, etc.

d.Officer - a bona fide officer of the taxpayer’s organization.

e.Full time employee - a full time employee of the taxpayer.

f.Family member - a member of the taxpayer’s immediate family (for example, spouse, parent, child, grandparent,

g.Other

Representative Signature. See instructions on page 4.

Designation -

Insert Letter from

Above

Relationship to Taxpayer (see instructions for Part II)

Signature

Date

Filing this Form

►File Online on TransAction Portal at https://tap.dor.mt.gov.

►Fax to: (406)

Or, if you are already working with a department employee, fax your completed form to the number provided by that person.

►Mail the completed form to: Montana Department of Revenue 340 N. Last Chance Gulch

PO Box 5805

Helena, MT

2

Instructions for Power of Attorney

Authorization to Disclose Tax Information

Part I

Section 1. Taxpayer Information

Individual. Enter your name, personal address, social

security number (SSN), telephone number, individual taxpayer identification number (ITIN) and/or federal employee identification number (FEIN) if applicable. Do not use your representative’s address or post office box for your own. If you file a tax return that includes

a sole proprietorship business (federal Schedule C) and the matters for which you are authorizing the listed representative(s) to represent you include your individual and business tax matters, including employment tax liabilities, enter both your SSN (or ITIN) and your business

FEIN as your taxpayer identification numbers. If the tax

matter concerns a joint return, a separate power of attorney form is required for each spouse.

C Corporation, S corporations, partnership, limited

liability company or association. Enter the name, business address, federal employer identification number

(FEIN), and telephone number. If this form is being prepared for C corporations filing a combined tax return, a list of subsidiaries is not required. This power of attorney

applies to all members of the combined tax return.

Trust. Enter the name, title, address of the trustee, the name and FEIN of the trust and telephone number.

Estate. Enter the name of the decedent as well as the name, title and address of the decedent’s personal

representative. Enter the estate’s FEIN for the taxpayer identification number or, if the estate does not have an

FEIN, the decedent’s SSN (or ITIN).

Section 2. Authorization of Representative

Enter your representative’s full legal name. Use the identical full name on all submissions and correspondence.

Enter the representative’s telephone number, address or post office box and

If a trust, estate, guardianship or conservatorship wants an

individual other than the personal representative, trustee or other fiduciary to handle tax matters before the Department

of Revenue, the personal representative, trustee or other

fiduciary must complete this form and designate the

other individual with the power of attorney. Otherwise, the personal representative, trustee or other fiduciary has the requisite authority to handle tax matters before the

Department of Revenue and need not complete this form.

Section 3. Tax Matters and Tax Years Covered by the Form

Indicate, by checking the appropriate boxes, what tax types you are authorizing your representative to inspect, receive and discuss with the Department of Revenue.

You may list any tax years or periods that have already ended as of the date you sign the form.

If the matter relates to estate tax, enter the date of the

decedent’s death instead of a tax year.

If the tax matter and tax periods aren’t specified, you are authorizing the representative access to all tax matters and years until you revoke their authorization.

Section 4. Acts Authorized by This Form

If you are providing authorization to another individual, check one of the three boxes depending on what authorization you are providing to your representative. A disclosure authorized by this form may take place by telephone, letter, facsimile, email or a personal visit.

Note: If you check the “yes” box on the individual tax return next to the question “Do you want to allow another person

(third party designee) to discuss this return with us?” you

authorize Department of Revenue employees to discuss the tax return with the third party designee. They cannot

discuss any other issues, such as outstanding tax liabilities, without a completed power of attorney form.

Section 5. Revocation of Prior Power(s) of Attorney

Taxpayer Revocation. Check the box if you want all prior POAs revoked.

Revocation Withdraw by Representative. If you are a representative and want to revoke an existing POA, write REVOKE across the top of the form and submit the form as indicated on page 4.

Section 6. Signature

Individual. You must sign and date the form. If you file a joint return, your spouse must execute his or her own Montana power of attorney to designate a representative.

Corporation or association. An officer having authority to bind the corporation must sign.

Partnership. All partners must sign unless one partner is authorized to act in the name of the partnership. A partner is authorized to act in the name of the partnership if, under Montana law, the partner has authority to bind the partnership. If there is any doubt whether a partner has the authority to bind the partnership, it is best that all partners sign the form.

Limited Liability Company (LLC). If the LLC is member- managed, all members must sign, unless one member is authorized to act in the name of the LLC. If the LLC is

Estate, trust or other fiduciary. As discussed in Section 2, if a trust, estate, guardianship or conservatorship wants an

individual other than the personal representative, trustee or other fiduciary to handle tax matters before the Department

of Revenue, the personal representative, trustee or other

fiduciary must complete this form and designate the other individual with the power of attorney. Thus, the personal representative of an estate must sign. The trustee of a trust must sign. If a guardian or conservator has been appointed

3

for a taxpayer, the guardian or conservator must sign. In all cases, the fiduciary must include the representative capacity in which the fiduciary is signing, such as “John Doe, guardian of Jane Roe.”

Part II. Declaration of Representative

The representative(s) you name may sign and date the Declaration of Representative. Enter the applicable designation (items

a.Attorney – Enter the

b.Certified Public Accountant – Enter the

c.Enrolled Agent, Licensed Public Accountant, etc.

d.Officer – Enter the title of the officer (for example,

President, Vice President, Secretary, etc.).

e.

f.Family Member – Enter the relationship to the taxpayer (for example, spouse, parent, child, brother, sister, etc.).

g.Other – Identify the type of representative and enter a brief description of the representative’s relationship to the taxpayer.

Filing this Form

File Online on TransAction Portal at https://tap.dor.mt.gov.

Fax the completed form to (406)

Mail the completed form to:

Montana Department of Revenue

340 N. Last Chance Gulch

PO Box 5805

Helena, MT

Questions? Please call us at (406)

File online at https://tap.dor.mt.gov.

4

| Fact Name | Description |

|---|---|

| Purpose | This form allows taxpayers to authorize a representative to receive and discuss their tax information with the IRS. |

| Eligibility | Any individual or entity that has a valid interest in a taxpayer’s information can be named as a representative. |

| Form Requirements | The taxpayer must provide personal identification information, including Social Security Number, and specify the type of tax information relevant to the authorization. |

| Governing Law | Federal regulations under the Internal Revenue Code, specifically 26 U.S.C. § 6103, govern the disclosure of tax information. |

| Duration | The authorization remains in effect until the taxpayer revokes it or the specified task is completed. |

| Filing Process | Once completed, this form should be submitted to the IRS, and the taxpayer should retain a copy for their records. |

Completing the Tax POA Authorization to Disclose Tax Information form is an important step toward granting someone the ability to handle your tax matters. Once this form is correctly filled out and submitted to the appropriate tax authority, it allows your designated representative to access your tax information, making communication and resolution more efficient.

After following these steps, you've efficiently authorized your representative to manage your tax information. Be sure to keep track of any communications from the tax authority related to this authorization, as it's crucial to stay informed about your tax matters.

The Tax POA Authorization to Disclose Tax Information form is a document that allows taxpayers to authorize a third party, typically a tax professional, to access their tax information. This form enables the designated individual or organization to communicate directly with the IRS on behalf of the taxpayer, making it easier to manage tax issues or complex returns.

This form is necessary for anyone who wishes to grant permission to another person or entity to handle their tax matters. If you're working with an accountant, tax preparer, or attorney regarding your tax situation, you should fill out this form to ensure they have the authority to act on your behalf.

To complete the form, you must provide:

Ensure all information is accurate to avoid delays in processing your request.

The authorization generally remains in effect until you officially revoke it. You can revoke or modify the authorization at any time by submitting a new form or by informing the IRS directly. Always keep a copy of the revocation for your records.

You can submit the Tax POA Authorization to Disclose Tax Information form by mailing it directly to the IRS at the address specified on the form. Alternatively, many tax professionals will file it electronically on your behalf through their systems to expedite the process.

If you decide to revoke or change the authorization, you must submit a new form or provide written notice to the IRS. The new authorization will invalidate any previous ones. Always keep track of which forms you have submitted to avoid confusion later.

Filling out the Tax Power of Attorney (POA) Authorization to Disclose Tax Information form can be a straightforward process. However, many individuals encounter common pitfalls that can lead to delays or complications. One major mistake is failing to provide accurate information about the taxpayer. The IRS requires precise details, including the full name, Social Security number, and address. Omitting or misspelling this information can result in the rejection of the form, creating unnecessary hurdles for the taxpayer.

Another frequent error is not correctly designating the representative. The Tax POA form allows for one or more representatives to be named, but if the person completing the form incorrectly identifies the representative's information, it can create issues down the line. Mistakes such as providing an outdated address or an incorrect identification number can lead to confusion about who is authorized to discuss tax matters on behalf of the taxpayer.

In addition, many people neglect to sign and date the form. This oversight may seem minor but is actually crucial. The IRS requires the taxpayer’s signature to validate the authorization. Without a signature and the appropriate date, the form will not be processed. This can lead to delays in tax discussions and potential penalties, which can easily be avoided by ensuring this step is completed meticulously.

Lastly, a common mistake involves not providing a clear purpose for the authorization. While it’s often assumed that the representative will understand the needs, the IRS prefers that the taxpayer outlines the specific reasons for granting access. This can include whether the representative is allowed to speak about all tax years or just selected ones. Lack of clarity may lead to limited access for the representative, ultimately defeating the purpose of filling out the form.

The Tax POA Authorization to Disclose Tax Information form allows individuals to authorize a representative to access their tax information. When preparing financial documents or managing tax-related matters, several other forms may be necessary to streamline the process. Here are five other important documents that are commonly used in conjunction with the Tax POA form.

Understanding these additional forms can greatly assist individuals in managing their tax affairs more effectively. Each document serves a specific purpose and facilitates communication with the IRS and related financial institutions.

When filling out the Tax POA Authorization to Disclose Tax Information form, careful attention is needed to ensure compliance and accuracy. Here are some essential dos and don'ts:

There are several misconceptions regarding the Tax POA Authorization to Disclose Tax Information form. Understanding the truth behind these misconceptions can help individuals use the form effectively when designating someone to manage their tax affairs. Here is a list of common misconceptions:

Filling out the Tax POA Authorization to Disclose Tax Information form requires attention to detail. Here are key takeaways to consider: