The Tax Power of Attorney form, known as D-2848, serves as a critical instrument that empowers an individual or organization to represent a taxpayer before the Internal Revenue Service (IRS) or relevant state tax authorities. By completing and submitting this form, a taxpayer grants an appointed agent the authority to handle essential tax matters on their behalf—including filing returns, negotiating on tax liabilities, and accessing confidential tax information. This form does not merely facilitate communication; it also establishes a legal channel through which the designated agent can perform specific actions that the taxpayer would otherwise need to undertake personally. It is important for taxpayers to understand the roles and limitations associated with this form, as it clearly outlines the scope of authority granted and can be customized for varying levels of representation. While commonly used for annual tax filings, the D-2848 can also be beneficial in dealing with audits, disputes, and other tax-related issues. The proper completion and submission of the Tax POA D-2848 form are essential steps in ensuring seamless representation and effective resolution of tax matters.

This is a

- |

Government of the |

OFFICIAL USE ONLY |

|

*** District of Columbia |

Declaration of Representation |

|

|

|

|

||

▲

▲

▲

▲

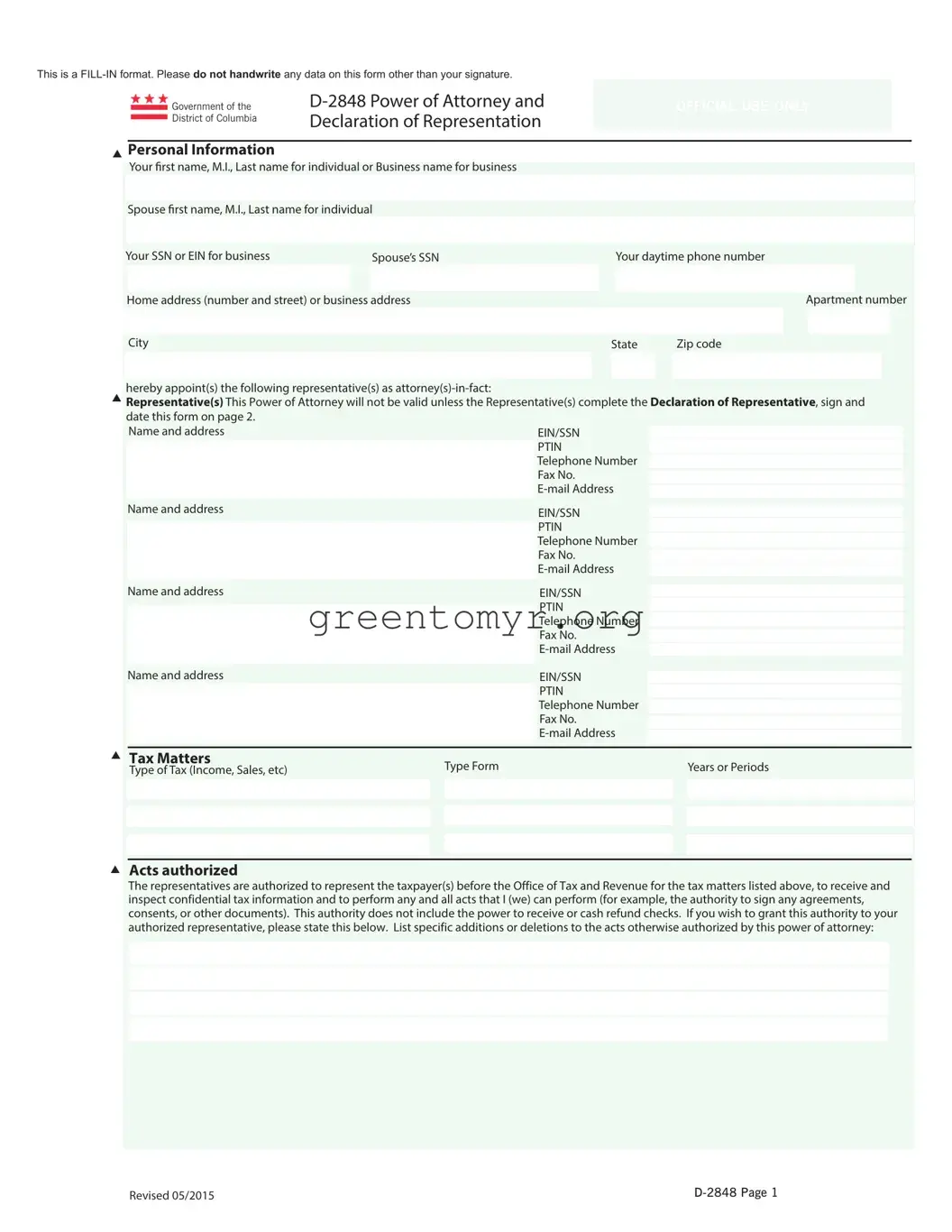

Personal Information

Your frst name, M.I., Last name for individual or Business name for business

Spouse frst name, M.I., Last name for individual

|

Your SSN or EIN for business |

|

Spouse’s SSN |

|

|

|

Your daytime phone number |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Home address (number and street) or business address |

|

|

|

|

|

|

Apartment number |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

Zip code |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

hereby appoint(s) the following representative(s) as

Representative(s) This Power of Attorney will not be valid unless the Representative(s) complete the Declaration of Representative, sign and date this form on page 2.

Name and addressEIN/SSN

PTIN Telephone Number

Fax No.

Name and address |

|

|

|

|

|

|

|

|

|||

|

|

EIN/SSN |

|

|

|

|

|

|

|||

|

|

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

Fax No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Name and address |

|

|

EIN/SSN |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||

|

|

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

Fax No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

Name and address |

|

|

EIN/SSN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

Fax No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tax Matters |

Type Form |

|

|

|

|

|

Years or Periods |

|

|

|

|

Type of Tax (Income, Sales, etc) |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Acts authorized

The representatives are authorized to represent the taxpayer(s) before the Office of Tax and Revenue for the tax matters listed above, to receive and inspect confidential tax information and to perform any and all acts that I (we) can perform (for example, the authority to sign any agreements, consents, or other documents). This authority does not include the power to receive or cash refund checks. If you wish to grant this authority to your authorized representative, please state this below. List specific additions or deletions to the acts otherwise authorized by this power of attorney:

Revised 05/2015 |

▲

▲

▲

▲

▲

Taxpayer's SSN or FEIN |

|

Taxpayer's Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Retention/revocation of prior power(s) of attorney By filing this power of attorney form, you automatically revoke all earlier power(s) of attorney on file with the Office of Tax Revenue for the same tax matters and years or periods covered by this document.

If you do not want to revoke a prior power of attorney, check here:

You must attach a copy of any Power of Attorney you want to remain in effect.

Signatures

Signature of taxpayer(s) If a tax matter concerns a joint return, both husband and wife must sign if joint representation is requested. If signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer. If other than the taxpayer, print the name here and sign below.

Your Signature |

|

Date |

|

Title if other than individual |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse's signature if filing jointly |

|

Date |

|

|

|

|

|||

|

|

Telephone number if other than the taxpayer |

|||||||

|

|

|

|

|

|

|

|

|

|

If not signed and dated, this power of attorney will be returned

Declaration of Representative Representative(s) must complete this section and sign below.

Under penalties of perjury, I declare that:

As the authorized representative of the taxpayer(s) identified for the tax matter(s) specified herein; I am one of the following:

a.A member in good standing of the bar of the highest court of the jurisdiction shown below.

b.A Certified Public Accountant duly qualified to practice in the jurisdiction shown below.

c.An Enrolled Agent under the requirements of Treasury Department Circular # 230.

d.A bona fide officer of the taxpayer’s organization.

e.A

f.A member of the taxpayer’s immediate family (i.e., spouse, parent, child, brother, or sister).

g.A general partner of a partnership.

h.Student Attorney or CPA- receives permission to represent taxpayers before the IRS by virtue of his/her status as a law, business, or accounting student working in an Low Income Taxpayer Clinic or Student Tax Clinic Program.

i.Other

Designation- |

|

Licensing jurisdiction (state) |

Bar, license, certification, |

|

|

|

|

|

||

|

Insert above |

|

or other licensing authority |

registration, or enrollment number |

|

Signature |

|

Date |

|

|

|

letter |

|

(if applicable) |

(if applicable) |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If you have any questions regarding the Power of Attorney, contact the Office of Tax and Revenue, Customer Service Administration, 1101 4th Street, SW, Washington, DC 20024; or call (202)

Mail the original Power of Attorney to:

Office of Tax and Revenue, Customer Service Administration, PO Box 470, Washington, DC

If this declaration is not signed and dated, this power of attorney will be returned

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 2848 serves as a Power of Attorney, allowing one individual to represent another before the IRS. |

| Form Number | The official form number is D-2848, which is necessary for tax-related authority. |

| Eligibility | Any individual or business entity can appoint someone as their representative using this form. |

| State-Specific Forms | Some states have their own power of attorney forms for tax matters; for example, California uses the FTB 3520 form. |

| Governing Laws | Federal regulations governing Form 2848 are found under Title 26 of the U.S. Code. State-specific forms follow their respective state laws. |

| Filing Requirements | The completed form must be signed by both the taxpayer and the appointed representative before submission to the IRS. |

Filling out the Tax POA D-2848 form is a straightforward process that enables you to authorize someone to represent you before the IRS. After completing the form, ensure that it is accurately submitted according to IRS guidelines to facilitate your representative’s ability to act on your behalf.

After submitting the form, monitor the process to ensure that your representative has received authorization. This is essential for smooth communication and tax representation with the IRS.

The Tax POA D-2848 form is a Power of Attorney document specifically designed for taxpayers in the United States. This form allows you to appoint an individual or organization to represent you in dealing with the IRS regarding your tax matters. When you sign this form, you give that representative the authority to receive confidential tax information and communicate with the IRS on your behalf.

You can appoint anyone as your representative, as long as they are qualified to practice before the IRS. Typically, this includes attorneys, certified public accountants (CPAs), and enrolled agents. It is vital to choose someone who is trustworthy and knowledgeable about tax law, as they will handle sensitive financial information and communicate on your behalf.

Completing the D-2848 form is straightforward. Follow these steps:

Make sure all information is accurate to prevent processing delays. If necessary, your representative can help guide you through this process.

Once you submit the D-2848 form to the IRS, your representative will be able to act on your behalf for matters specified in the form. The IRS typically processes the form quickly, allowing your representative to access your tax information and communicate with the IRS. It is advisable to keep a copy of the form for your records.

Yes, you can revoke the Power of Attorney at any time. To do so, you must complete a revocation form or simply notify the IRS in writing, stating your intention to revoke the D-2848. Make sure to provide your information, your representative's information, and any relevant details to ensure the revocation is processed properly. Once the IRS receives your revocation, your representative will no longer have the authority to act on your behalf.

When preparing and submitting the Tax POA D-2848 form, many individuals unknowingly make critical errors that can delay processing and jeopardize their tax matters. Understanding these common mistakes can help ensure that your form is completed accurately and efficiently.

One frequent mistake is failing to sign the form. Without the necessary signatures, the form is incomplete and cannot be processed. It is essential for the taxpayer and the representative to both sign the D-2848. Make sure that you have provided all required signatures before submission.

Another issue arises when filling out the form is the inadequate description of the tax matters. In Box 3, taxpayers must specify which tax matters they are granting power of attorney for. Vague or unclear descriptions can lead to confusion or a denial of your request, so it is crucial to be as specific as possible.

Omitting the correct representative information can also be detrimental. Ensure that all contact details for the designated representative are accurate. Any errors in names, addresses, or identification numbers can cause delays in communication and potential issues with your tax matters.

Often, taxpayers will forget to indicate the tax year(s) involved in the representation. Failing to include this information can create problems, as it becomes unclear which years the power of attorney covers. Be thorough in specifying years to avoid complications.

In some cases, individuals might assign power of attorney to more than one representative without following proper guidelines. It’s important to ensure that the form reflects whether you intend to grant authority to multiple representatives and that their details are clearly listed to avoid confusion.

Another mistake involves not keeping a copy of the completed form. Always retain a copy of the submitted D-2848 form for your records. This can serve as a reference in future communications with the IRS or your representative and can be useful in case any discrepancies arise.

Lastly, a common oversight occurs when individuals fail to submit the form to the correct IRS office. Each form must be sent to the appropriate location based on the taxpayer’s circumstances. Carefully check the submission guidelines and ensure that the form goes to the right place for processing.

By being aware of these common mistakes, you can take proactive steps to ensure that your Tax POA D-2848 is completed successfully. Careful attention during the preparation can help avoid setbacks and ensure that your tax matters are handled smoothly.

The Tax Power of Attorney (POA) D-2848 form is essential when you need someone to handle your tax matters. Along with this form, several other documents may also be required or beneficial. Below is a list of commonly used forms and their brief descriptions.

Having these forms prepared can help facilitate your tax process and ensure everything is in order. Always review your specific needs based on your tax situation to determine which documents you will require.

The IRS Form D-2848, also known as the Power of Attorney and Declaration of Representative, allows individuals to designate a representative to act on their behalf in tax matters. It is pivotal for navigating the complexities of tax obligations. Several other documents share similarities with Form D-2848, primarily in granting authority to representatives and ensuring proper management of legal or financial matters. Below are five key documents that reflect aspects comparable to D-2848:

Understanding these documents can enhance your ability to delegate authority effectively across different aspects of life, whether related to taxes or beyond. Each serves a unique purpose but shares the fundamental principle of empowering another person to act on your behalf.

When filling out the Tax POA D-2848 form, it’s important to pay attention to details. Here’s a list of what you should and shouldn’t do to ensure your form is filled out correctly.

The Tax POA D-2848 form, also known as the Power of Attorney form for tax purposes, often comes with several misconceptions. Understanding the facts can help individuals navigate their tax situations more effectively.

Understanding these misconceptions can help taxpayers make informed choices regarding their tax representations and dealings.

Filling out and using the Tax POA D-2848 form can be straightforward if you understand the key points. Here are some essential takeaways:

Understanding these points will help navigate the process of using the D-2848 form effectively. Properly filling out this form can make handling your tax issues much smoother.