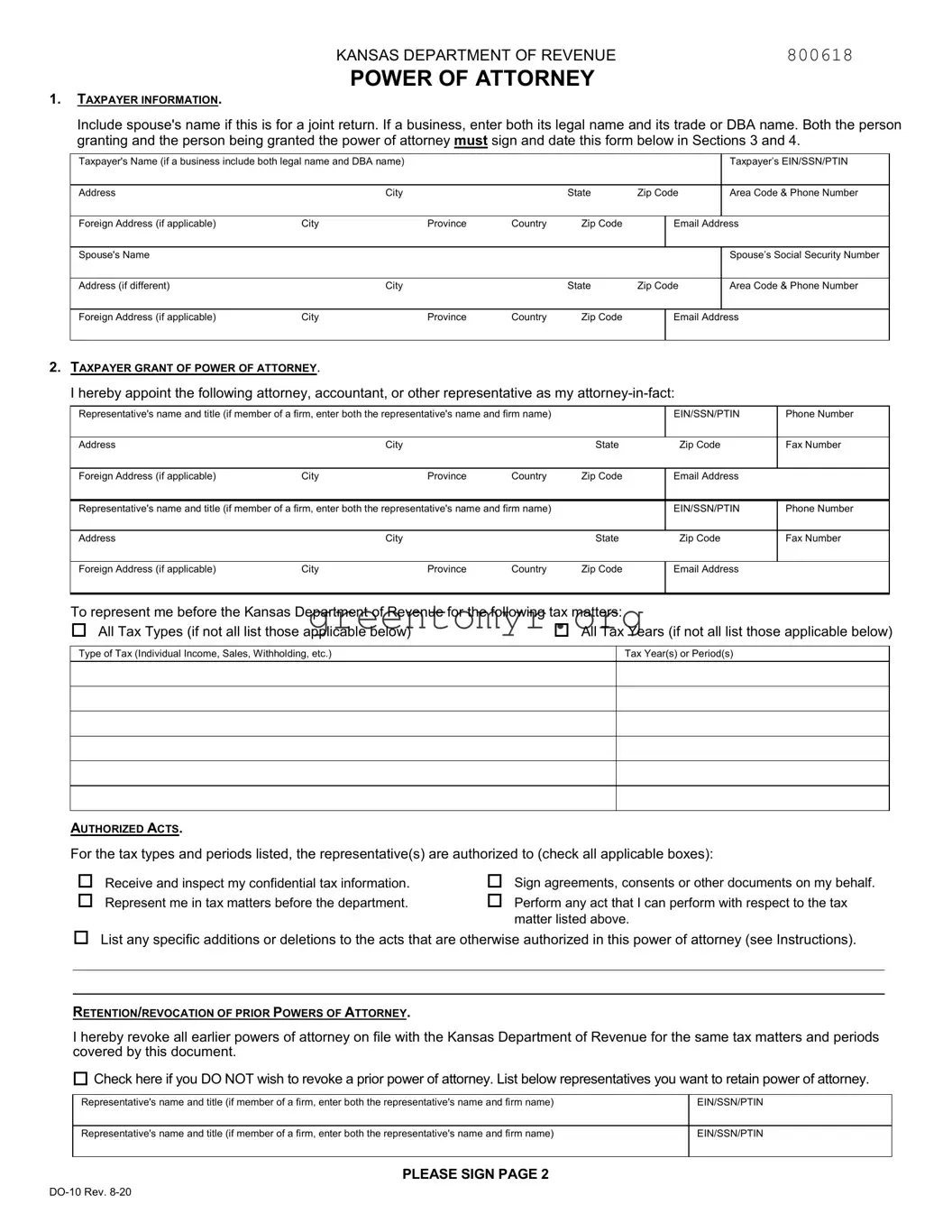

The Tax POA DO-10 form is an important document for taxpayers who wish to grant someone else the authority to handle their tax matters. This form allows individuals to appoint an authorized representative, typically a tax professional or attorney, to act on their behalf before the taxing authorities. By completing the Tax POA DO-10, taxpayers enable their representatives to discuss their tax affairs, submit documents, and even negotiate with the IRS or state tax agencies. It is crucial to understand the various sections of the form, including the personal information of both the taxpayer and the representative. Furthermore, the POA must be signed by the taxpayer to validate it. This form is not just a simple paperwork formality; it plays a vital role in ensuring that communications about tax liabilities, obligations, and rights are efficiently managed. Knowing how to effectively use the Tax POA DO-10 can ease the burden of tax compliance and improve communication with tax authorities.

KANSAS DEPARTMENT OF REVENUE |

800618 |

POWER OF ATTORNEY

1.TAXPAYER INFORMATION.

Include spouse's name if this is for a joint return. If a business, enter both its legal name and its trade or DBA name. Both the person granting and the person being granted the power of attorney must sign and date this form below in Sections 3 and 4.

Taxpayer's Name (if a business include both legal name and DBA name) |

|

|

|

|

|

Taxpayer’s EIN/SSN/PTIN |

|

|

|

|

|

|

|

|

|

Address |

City |

|

|

State |

Zip Code |

Area Code & Phone Number |

|

|

|

|

|

|

|

|

|

Foreign Address (if applicable) |

City |

Province |

Country |

Zip Code |

|

IEmail Address |

|

Spouse's Name |

|

|

|

|

|

|

Spouse’s Social Security Number |

|

|

|

|

|

|

|

|

Address (if different) |

City |

|

|

State |

Zip Code |

Area Code & Phone Number |

|

|

|

|

|

|

|

|

|

Foreign Address (if applicable) |

City |

Province |

Country |

Zip Code |

|

IEmail Address |

|

2.TAXPAYER GRANT OF POWER OF ATTORNEY.

I hereby appoint the following attorney, accountant, or other representative as my

Representative's name and title (if member of a firm, enter both the representative's name and firm name) |

|

EIN/SSN/PTIN |

Phone Number |

|

|||

|

|

|

|

|

|

|

|

Address |

|

City |

|

State |

Zip Code |

Fax Number |

|

|

|

|

|

|

|

|

|

Foreign Address (if applicable) |

City |

Province |

Country |

Zip Code |

Email Address |

|

|

|

|

|

|

|

|||

Representative's name and title (if member of a firm, enter both the representative's name and firm name) |

|

EIN/SSN/PTIN |

Phone Number |

|

|||

|

|

|

|

|

|

|

|

Address |

|

City |

|

State |

Zip Code |

Fax Number |

|

|

|

|

|

|

|

|

|

Foreign Address (if applicable) |

City |

Province |

Country |

Zip Code |

Email Address |

|

|

|

|

|

|

||||

To represent me before the Kansas Department of Revenue for the following tax matters: |

|

|

|

||||

All Tax Types (if not all list those applicable below) |

|

All Tax Years (if not all list those applicable below) |

|||||

Type of Tax (Individual Income, Sales, Withholding, etc.)

Tax Year(s) or Period(s)

AUTHORIZED ACTS.

For the tax types and periods listed, the representative(s) are authorized to (check all applicable boxes):

Receive and inspect my confidential tax information.

Represent me in tax matters before the department.

Sign agreements, consents or other documents on my behalf.

Perform any act that I can perform with respect to the tax matter listed above.

List any specific additions or deletions to the acts that are otherwise authorized in this power of attorney (see Instructions).

RETENTION/REVOCATION OF PRIOR POWERS OF ATTORNEY.

I hereby revoke all earlier powers of attorney on file with the Kansas Department of Revenue for the same tax matters and periods covered by this document.

Check here if you DO NOT wish to revoke a prior power of attorney. List below representatives you want to retain power of attorney.

Representative's name and title (if member of a firm, enter both the representative's name and firm name) |

EIN/SSN/PTIN |

|

|

Representative's name and title (if member of a firm, enter both the representative's name and firm name) |

EIN/SSN/PTIN |

|

|

PLEASE SIGN PAGE 2

3.SIGNATURE OF TAXPAYER(S). If a tax matter concerns a joint return, both husband and wife must sign when joint representation is requested. When a corporate officer, partner, guardian, executor, receiver, administrator, or trustee signs this section on behalf of a taxpayer, the signatory also certifies that the signatory is authorized to execute this form on behalf of the taxpayer.

(Signature) |

(Printed Name) |

(Date) |

(Signature) |

(Printed Name) |

(Date) |

4.SIGNATURE OF REPRESENTATIVE(S).

(Signature) |

(Printed Name) |

(Date) |

(Signature) |

(Printed Name) |

(Date) |

INSTRUCTIONS FOR POWER OF ATTORNEY AUTHORIZATION

A power of attorney is a legal document authorizing someone to act as your representative. You, the taxpayer, must complete, sign, and return this form if you wish to grant a power of attorney (POA) to an attorney, accountant, agent, tax return preparer, family member, or anyone else to act on your behalf with the Kansas Department of Revenue (KDOR). You may use this form for any matter affecting any tax administered by the department, including audit and collection matters. This POA will remain in effect until the expiration date, if included under Section 2, or until you revoke it, whichever is earlier. KDOR will accept copies of this form, including fax copies.

SECTION 1. TAXPAYER INFORMATION.

Individuals. In the block provided, enter your name, SSN, address, telephone number, and email address in the spaces provided. If this POA is for a joint return and your spouse is designating the same representative or representatives, enter your spouse’s name, address (if different from your own), Social Security number, and your spouse’s email address.

Businesses. Enter both the legal name and the DBA or trade name, if different. For example, if the business is an individual proprietorship, enter the proprietor's name and the name under which business is transacted. (e.g., Joe Smith dba Joe's Diner). Also enter the EIN (federal employer identification number), telephone number, business address, and email address.

Estates. Enter the name, title, address, and email address of the decedent’s executor/personal representative in the taxpayer section. Use the spouse’s section to enter the decedent’s name, date of death, and SSN.

SECTION 2. TAXPAYER GRANT OF POWER OF ATTORNEY.

Representative's name. Complete all the requested information for each representative. If the representative is a member of a firm, enter the firm’s name too. If you are designating more than two representatives, please complete another form and attach it to this form. Mark the second form “additional representatives.”

Type of tax. If you wish the power of attorney to apply to all periods and all tax types administered by KDOR, please check the box(es) for "All tax types" and "All tax periods". If for a specific tax type and/or tax year enter the type of tax and the tax years or reporting periods for each tax type. If the matter relates to estate, inheritance, or succession tax, please enter the date of the decedent’s death.

Authorized acts. Check all boxes that apply. Use the additional lines to limit, clarify, or otherwise define the acts authorized by this POA. For example, if you wish to limit the POA to a specific time period or to establish an expiration date, enter that information and the dates (month, day, and year) on these lines.

Retention/revocation of prior powers of attorney. Unless otherwise specified, this POA replaces and revokes all previous POAs on file with the department. If there is an existing POA that you do NOT want to revoke, check the box in this section and enter the representative’s name and EIN/SSN/PTIN in the space provided.

If you wish to revoke an existing POA without naming a new representative, attach a copy of the previously executed POA. On the copy of the previously executed POA, write “REVOKE” across the top of the form, and initial and date it again under your signature or signatures already in Section 3.

SECTION 3. SIGNATURE OF TAXPAYER(S).

You must sign and date the POA. If a joint return is being filed and both husband and wife intend to authorize the same person to represent them, both spouses must sign the POA unless one spouse has authorized the other in writing to sign for both. You must attach a copy of your spouse's written authorization to this POA.

SECTION 4. SIGNATURE OF REPRESENTATIVE(S).

Each representative that you name must sign and date this form.

TAXPAYER ASSISTANCE

If you have questions about this form, please visit or call our office.

Taxpayer Assistance Center

Scott State Office Building

120 SE 10th St.

PO Box 3506

Topeka, KS

Phone:

The Department of Revenue office hours are 8 a.m. to 4:45 p.m., Monday through Friday.

Additional copies of this form are available from our website at: ksrevenue.org

2

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA DO-10 form is used to authorize an individual to represent a taxpayer before the IRS or state tax authority. |

| Governing Law | This form is governed by the Internal Revenue Code and applicable state tax laws. |

| Required Information | Taxpayers must provide their name, address, and taxpayer identification number on the form. |

| Representative Details | The form requires the name, address, phone number, and representative's offical ID number. |

| Validity | Once submitted, the form remains valid until revoked or until the specific tax matter is resolved. |

| Submission Method | The form can be submitted electronically or via mail, depending on the tax authority’s regulations. |

| Signatures | Both the taxpayer and the representative must sign the form to validate it. |

| Revocation Process | A taxpayer can revoke the authority granted by submitting a written notice to the tax authority. |

| Limitations | The representative's powers may be limited to specific tax periods or types of tax matters. |

| State Variations | Different states may have their own versions of POA forms with specific requirements. |

Completing the Tax POA DO-10 form is an important step in granting someone the authority to act on your behalf regarding tax matters. After filling out the form, be sure to double-check all information for accuracy before submitting it to the appropriate tax authority.

The Tax POA DO-10 form is a Power of Attorney form specifically used for tax-related matters. It allows an individual or business to designate someone else to handle their tax affairs with the Department of Revenue. This can include filing returns, discussing tax matters, and representing the taxpayer in audits or appeals.

Anyone who needs assistance with their taxes may want to use the Tax POA DO-10 form. This includes:

By using this form, taxpayers can ensure that their interests are represented and protected.

Completing the Tax POA DO-10 form involves several straightforward steps:

Make sure all information is accurate to avoid any delays in processing.

Once you have completed the form, send it to the appropriate office of the Department of Revenue. The specific mailing address may vary depending on your location or the type of tax issue involved. Check the Department of Revenue's official website for the most accurate address and any additional submission instructions.

The processing time for the Tax POA DO-10 form can vary. Generally, it may take anywhere from a few days to a couple of weeks. Once processed, you and your designated representative will receive confirmation. During busy seasons, such as tax filing periods, processing may take longer. It’s a good idea to submit the form well in advance of any important tax deadlines to ensure enough time for processing.

The Tax POA DO-10 form, or the Power of Attorney for tax matters, is an essential document used in the United States to allow someone else to handle your tax affairs. Filling it out may seem straightforward, but individuals often make common mistakes that can lead to confusion and delays. Recognizing these mistakes can help ensure that your form is completed correctly, allowing your authorized representative to assist you effectively.

One frequent error is failing to provide the correct personal information. When completing the form, it is vital to double-check that your name, address, and Social Security number (or Employer Identification Number) are accurate. An oversight in these details can result in the form being rejected or, worse, unauthorized representation.

Another mistake occurs when individuals neglect to specify the tax matters that the Power of Attorney covers. The form provides sections where you can define what types of taxes you're authorizing someone to manage. If this part is left blank, the IRS may interpret it as a lack of authority, preventing your representative from acting on your behalf.

Alongside this, people often overlook signing and dating the form. Omitting your signature means the document is invalid, rendering all the information inputted ineffective. Remember, after filling it out, you must also date it. The date is crucial as it shows when you granted the power.

People sometimes forget to include the representative's exact information. While it might be tempting to fill in a name and contact number, providing incomplete information can lead to complications. Ensuring that the appointed representative’s details, including their address and phone number, are accurate is essential for seamless communication with the IRS.

In addition, some individuals mistakenly assume that simply having a Power of Attorney means the person can automatically deal with tax issues. Depending on the specifics outlined in the form, such as which taxes are covered, there may be limitations. It's essential to be clear about the scope of authority you are granting.

Another common pitfall occurs when the form is not filed with the correct tax authority. Many people believe submitting the form wherever it may seem convenient would suffice. However, direct submission to the IRS or relevant state tax office is required. It’s wise to double-check the guidelines for where to send your completed form.

Additionally, individuals may fail to retain a copy of the signed form for their records. This might not seem crucial, but having a copy can be invaluable if questions arise about your designated representative’s authority in the future. Keep this document safe and accessible.

Some people also neglect to check if their representative is indeed authorized to act in specific tax matters. Not every tax professional is equipped to handle all tax situations; some may lack the credentials for representation in particular contexts. Confirming their qualifications is prudent before granting them power.

Finally, one of the biggest mistakes is not reviewing the form thoroughly before submission. Errors in the information can often go unnoticed, causing delays or complications down the line. Taking a moment to review everything carefully ensures the accuracy of the filing and avoids unnecessary backtracking later.

By understanding these pitfalls, individuals can take proactive steps to ensure that their Tax POA DO-10 form is correctly filled out, enabling their chosen representative to assist with their tax matters confidently.

The Tax Power of Attorney (POA) DO-10 form is a vital document that allows an individual to appoint someone to act on their behalf in tax matters before the IRS or state taxation authorities. Understanding additional forms and documents that accompany this form can streamline the process and ensure that all necessary information is submitted accurately. Below are some essential forms and documents related to the Tax POA DO-10.

It is important to ensure that all relevant documents are completed accurately and submitted on time. Gathering this paperwork will create a smooth process for managing tax responsibilities effectively. Each document plays a role in helping the appointed representative effectively serve the individual's tax interests.

When filling out the Tax POA DO-10 form, there are several important tips to keep in mind to ensure your application is processed smoothly. Following these will save you time and potential errors.

The Tax POA DO-10 form is an important document but often surrounded by misconceptions. Here is a list of five common misunderstandings:

Many people believe that this form is exclusively for individuals with outstanding tax liabilities. In reality, the Tax POA DO-10 can be used by anyone who needs to appoint someone to manage their tax matters, regardless of whether they owe taxes or not.

While many choose to appoint tax professionals, such as accountants or attorneys, anyone can serve as an agent. This could be a family member or a friend, as long as the form is filled out correctly and signed by the individual.

The form grants authority specifically related to tax matters. It does not extend to general financial or legal decision-making. The scope of authority is limited to tax-related issues as defined in the document.

Some believe that the authority granted is permanent. However, the Tax POA DO-10 can be revoked by the individual at any time. Additionally, it may also have a specified duration if noted on the form.

This document serves a formal purpose and provides legal protection for both the taxpayer and the appointed agent. Verbal consent does not provide the same level of accountability or authority, making the completion of the Tax POA DO-10 advisable.

Filling out and using the Tax POA DO-10 form can simplify the process of managing your tax matters. Here are some key takeaways to keep in mind: