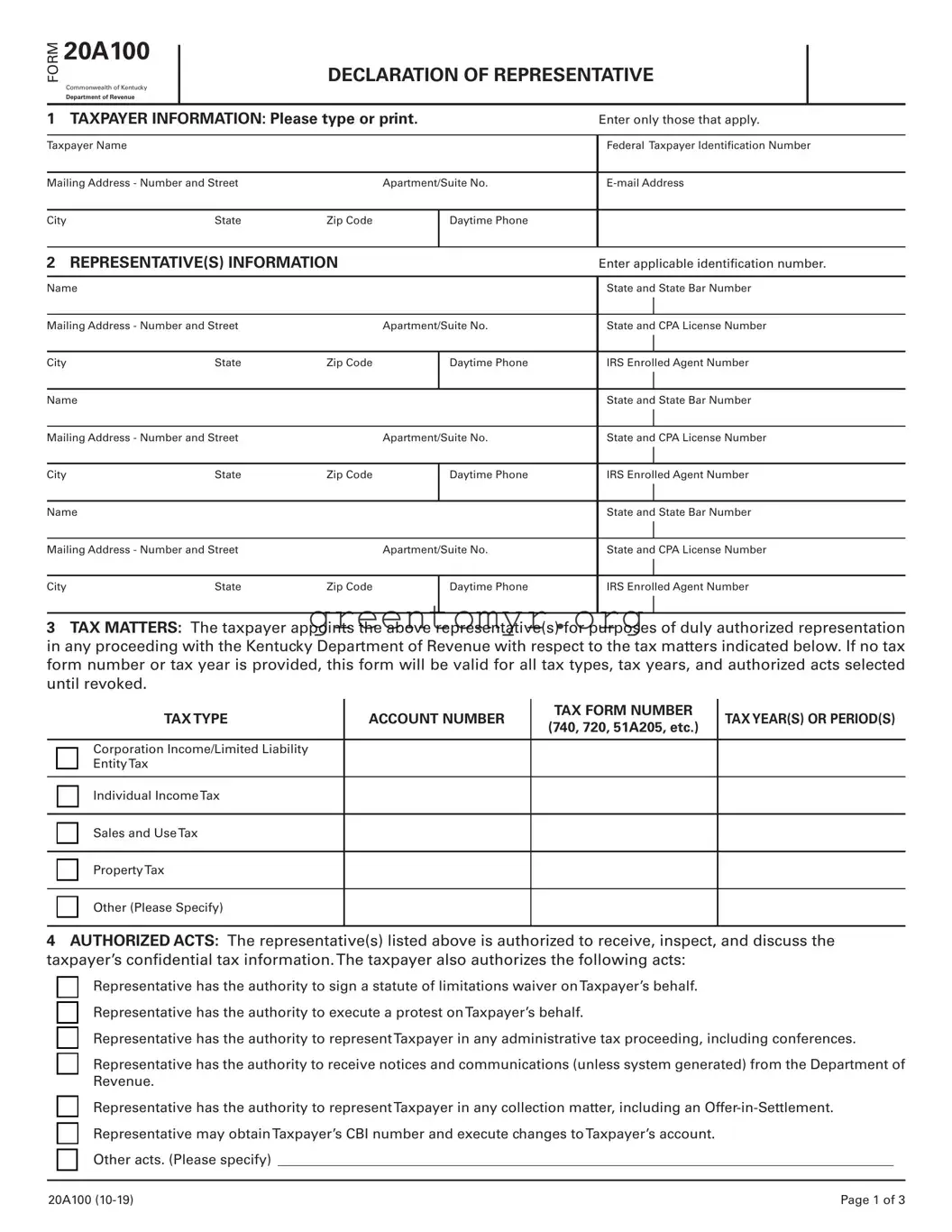

The Tax POA Form 20A100 is an essential document for individuals and businesses looking to authorize an attorney-in-fact or representative to act on their behalf in tax matters with the Department of Revenue. This form streamlines communication between taxpayers and tax authorities, facilitating the resolution of tax issues more efficiently. By completing the Form 20A100, taxpayers provide clear guidance about the extent of authority granted to their representative, allowing them to handle various tax-related tasks, such as filing returns, making payments, and discussing sensitive financial information. It's crucial for taxpayers to understand the specifics of this authorization, including any limitations or conditions they wish to impose. Moreover, the form requires basic personal information, such as the taxpayer’s name, address, and identification numbers, alongside the representative's details. This ensures that the Department of Revenue can easily verify the legitimacy of the authorization. Understanding these aspects can empower taxpayers to manage their tax responsibilities more effectively, while also protecting their interests by choosing qualified representatives.

20A100

DECLARATION OF REPRESENTATIVE

Commonwealth of Kentucky

Department of Revenue

1 TAXPAYER INFORMATION: Please type or print. |

|

Enter only those that apply. |

||||

|

|

|

|

|

|

|

Taxpayer Name |

|

|

|

Federal Taxpayer Identifcation Number |

||

|

|

|

|

|

||

Mailing Address - Number and Street |

|

Apartment/Suite No. |

||||

|

|

|

|

|

|

|

City |

State |

Zip Code |

IDaytime Phone |

|

|

|

2 |

REPRESENTATIVE(S) INFORMATION |

|

|

Enter applicable identifcation number. |

||

|

|

|

|

|

|

|

Name |

|

|

|

State and State Bar Number |

||

|

|

|

|

|

|

I |

Mailing Address - Number and Street |

|

Apartment/Suite No. |

State and CPA License Number |

|||

|

|

|

|

|

|

I |

City |

State |

Zip Code |

I |

Daytime Phone |

I |

|

|

IRS Enrolled Agent Number |

|||||

|

|

|

|

|

|

|

Name |

|

|

|

State and State Bar Number |

||

|

|

|

|

|

|

I |

Mailing Address - Number and Street |

|

Apartment/Suite No. |

State and CPA License Number |

|||

|

|

|

|

|

|

I |

City |

State |

Zip Code |

I |

Daytime Phone |

I |

|

|

IRS Enrolled Agent Number |

|||||

|

|

|

|

|

|

|

Name |

|

|

|

State and State Bar Number |

||

|

|

|

|

|

|

I |

Mailing Address - Number and Street |

|

Apartment/Suite No. |

State and CPA License Number |

|||

|

|

|

|

|

|

I |

City |

State |

Zip Code |

I |

Daytime Phone |

I |

|

|

IRS Enrolled Agent Number |

|||||

|

|

|

|

|

|

|

3TAX MATTERS: The taxpayer appoints the above representative(s) for purposes of duly authorized representation in any proceeding with the Kentucky Department of Revenue with respect to the tax matters indicated below. If no tax form number or tax year is provided, this form will be valid for all tax types, tax years, and authorized acts selected until revoked.

TAX TYPE |

ACCOUNT NUMBER |

TAX FORM NUMBER |

TAX YEAR(S) OR PERIOD(S) |

|

(740, 720, 51A205, etc.) |

||||

|

|

|

Corporation Income/Limited Liability

¨EntityTax

¨Individual IncomeTax

¨Sales and UseTax

¨PropertyTax

¨Other (Please Specify)

4AUTHORIZED ACTS: The representative(s) listed above is authorized to receive, inspect, and discuss the taxpayer’s confdential tax information.The taxpayer also authorizes the following acts:

¨Representative has the authority to sign a statute of limitations waiver onTaxpayer’s behalf.

¨Representative has the authority to execute a protest onTaxpayer’s behalf.

¨Representative has the authority to representTaxpayer in any administrative tax proceeding, including conferences.

¨Representative has the authority to receive notices and communications (unless system generated) from the Department of Revenue.

¨Representative has the authority to representTaxpayer in any collection matter, including an

¨Representative may obtainTaxpayer’s CBI number and execute changes toTaxpayer’s account.

¨Other acts. (Please specify) ________________________________________________________________________________________

20A100 |

Page 1 of 3 |

FORM 20A100

DECLARATION OF REPRESENTATIVE

Page 2 of 3

5CONSOLIDATED OR UNITARY COMBINED RETURN FILERS: If the taxpayer fles a consolidated or unitary combined tax return per KRS 141.200(11) and/or KRS 141.201(3)(a), the authorized acts will be extended to the subsidiaries included in the return. If any subsidiaries are to be excluded from the authorized acts, list below.

NAME

FEDERAL IDENTIFICATION

NUMBER

TAX YEARS

6 RETENTION/REVOCATION OF PRIOR POWER(S) OF ATTORNEY OR REPRESENTATIVE AUTHORIZATION(S)

The fling of this authorization form automatically revokes any prior power(s) of attorney or representative authorization(s) on fle with the Department of Revenue for the same matter(s) and year(s) or period(s) covered by this document. If you do not want to revoke any prior power(s) of attorney or representative authorization(s), you must attach a copy of any power(s) of attorney or

representative authorization(s) you wish to remain in effect for the same matter(s) and year(s) or period(s) covered.

7SIGNATURE OFTAXPAYER. If a tax matter concerns a year in which a joint return was fled, each spouse must fle a separate representative authorization even if they are appointing the same representative(s). If signed by a corporate offcer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the legal authority to execute this form on behalf of the taxpayer.

NOT VALID UNLESS COMPLETED, SIGNED, AND DATED BY THE TAXPAYER.

Signature |

Date Signed |

|

|

|

|

Print Name |

Title (if applicable) |

|

8 SIGNATURE OF REPRESENTATIVE(S)

Under penalties of perjury, by my signature below I declare that:

•I am not currently suspended or disbarred from practice, or ineligible for practice;

•I am subject to regulations contained in Circular 230 (31 CFR, Subtitle A, Part 10) as amended, governing practice before the Internal Revenue Service;

•I am authorized to represent the taxpayer for the matter(s) specifed; and

NOT VALID UNLESS COMPLETED, SIGNED, AND DATED BY THE REPRESENTATIVE(S).

Signature |

Date Signed |

|

|

|

|

Printed Name |

PTIN (if applicable) |

|

|

|

|

Signature |

Date Signed |

|

|

|

|

Printed Name |

PTIN (if applicable) |

|

|

|

|

Signature |

Date Signed |

|

Printed Name |

PTIN (if applicable) |

FORM 20A100

Instructions for Form 20A100

Page 3 of 3

Purpose of Form 20A100

Use the Declaration of Representative (Form 20A100) to authorize the individual(s) to represent you before the Kentucky Department of Revenue. You may grant the individual(s) authorization to act on your behalf with regard to any tax administered by the Kentucky Department of Revenue. Form 20A100 is provided for the taxpayer’s convenience. One form may be submitted to designate all tax types the Department is authorized to communicate with the authorized representative(s). You may revoke this form at any time.

1Taxpayer

Name and

Daytime

Federal Taxpayer Identifcation

2Representative Information

Enter up to three individuals authorized to represent you and act on your behalf before the Department about the tax matters and authorized acts specifed on this form. Provide the name, address, and telephone number of the authorized representative(s). If the authorized representative is an attorney, certifed public accountant (CPA), or enrolled agent, provide the appropriate identifcation number.

3Tax Matters

Select the tax types the authorized representative(s) may act on your behalf with the Department. Provide the account number for all tax types selected. If authorization is being granted for specifc forms and tax periods, list the tax forms and tax periods. If tax forms and tax periods are left blank, this form will be valid for all tax types, tax periods, and authorized acts selected until revoked.

4Authorized Acts

This form allows the authorized representative(s) to communicate and receive confdential tax information. You may also select other acts the authorized representative(s) may perform on your behalf. If an act is not listed, select “Other” and specify.

Note: This form does not allow the authorized representative to sign tax returns or settlement agreements on your behalf.

5Consolidated or Unitary Combined Return Filers

If a consolidated or unitary combined tax return has been fled, list any subsidiary(ies) to be excluded from this authorization. The Department will not discuss or provide confdential tax information to the authorized representative(s) for any subsidiary listed. If no subsidiaries are listed, this form will extend to all corporations in a consolidated or unitary combined tax return.

6Retention/Revocation

Filing this form will automatically revoke any prior power of attorney or authorization letter submitted to the Department for the tax matters included on this form. If you do not want to revoke a prior power of attorney or authorization letter, a copy MUST be attached to this form to remain in effect.

7Signature of Taxpayer

This form must be signed and dated by the taxpayer to be valid. If the taxpayer is a business entity, it must be signed by an individual with the authority to delegate a representative on behalf of the taxpayer. If not signed and dated, the Department will not communicate with or provide confdential tax information to the authorized representative(s) included on this form.

8Signature of the Authorized Representative(s)

This form must be signed and dated by the authorized representative(s) to be valid. If not signed and dated, the Department will not communicate with or provide confdential tax information to the authorized representative(s) included on this form.

Mail this form to the following address:

Kentucky Department of Revenue

P. O. Box 181, Station 56

Frankfort, Kentucky

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA Form 20A100 is used for granting power of attorney to a representative for tax-related matters. |

| Governing Laws | This form operates under the state tax laws, particularly referencing the Illinois Compiled Statutes (ILCS) regarding tax representation. |

| Eligibility | Any individual or business entity can appoint a representative using this form, if they are authorized to act on their behalf for tax purposes. |

| Filing Method | The completed form can be submitted electronically or via paper to the relevant state tax authority. |

| Effective Date | The power of attorney becomes effective upon submission, unless a different date is specified by the taxpayer. |

| Revocation | The authority granted can be revoked at any time by the entity that issued it, through a separate revocation document. |

Filling out the Tax POA form 20a100 is an important step if you wish to designate someone to represent you in matters related to your taxes. After submitting the form, your designated representative will be able to work on your behalf with the tax authorities, allowing for smoother communication and management of your tax issues.

The Tax POA form 20A100 is a Power of Attorney form specifically designed for tax matters. This form allows individuals to authorize another person to act on their behalf regarding tax-related issues. The representative could be a tax professional, attorney, or any individual the taxpayer trusts. This form is essential for facilitating communication and decision-making with tax authorities.

You can designate anyone as your representative as long as they are not under any legal limitations that would keep them from acting in your interests. Common choices include:

It is important to choose someone who is knowledgeable about tax matters and can effectively handle your specific needs.

Completing the 20A100 form is straightforward. Follow these steps:

After completing the form, submit it to the appropriate tax authority. Ensure that your representative receives a copy for their records.

The effectiveness of the Tax POA form 20A100 is typically immediate upon submission, unless otherwise specified. However, processing times may vary depending on the tax authority. It is advisable to confirm with the relevant agency that they have accepted your form. Avoid any delays in communication by submitting the form well in advance of any critical tax deadlines.

Many individuals encounter difficulties when completing the Tax Power of Attorney (POA) form 20A100. Understanding common mistakes can help ensure smoother processing and avoid potential delays. Here are five prevalent errors.

First, one mistake often made is neglecting to provide accurate taxpayer information. This includes the taxpayer's name, Social Security number (SSN), and address. Any discrepancy in these details can lead to confusion and slow down the IRS's processing of the form.

Next, individuals sometimes skip the section for the representative's information. It's essential to fill out this part completely, including the representative's name and ID number, usually an SSN or Employer Identification Number (EIN). Failing to do so may result in the IRS not recognizing the representative’s authority.

Another common error involves not specifying the type of tax and tax years for which the POA is granted. Without clear indications of the applicable taxes—such as income tax or estate tax—and the corresponding years, the IRS may reject the form. Clarity in this area is vital.

People also tend to overlook the signature requirement at the end of the form. This simple but crucial step is often forgotten, rendering the form invalid. Both the taxpayer and the representative must sign to authenticate the authority given.

Lastly, submitting the form without ensuring that it’s current can lead to problems. IRS forms and procedures can change, and using outdated versions may cause delays or rejections. Always verify that the most current version is being used when filing.

The Tax Power of Attorney (POA) form 20A100 allows individuals to appoint someone to handle their tax-related matters. When using this form, several other documents may also be required to ensure everything runs smoothly. Here are some common forms and documents often used alongside the Tax POA form.

Using these documents in conjunction with the Tax POA form 20A100 enables a smoother process for managing tax obligations. Always ensure that each form is filled out correctly to avoid complications.

The Tax Power of Attorney (POA) form 20A100 allows individuals to designate someone to act on their behalf in matters related to their taxes. It shares similarities with several other legal documents that empower individuals to delegate authority. Below is a list of these documents, each highlighting how they are akin to the Tax POA form.

Each of these documents serves to facilitate the management and delegation of important responsibilities, ensuring that individuals can appoint trusted representatives to act in their best interests across various domains.

When you're filling out the Tax POA form 20a100, there are certain things that can help make the process smoother. Here’s a clear list of dos and don’ts to keep in mind:

Understanding the Tax Power of Attorney (POA) Form 20A100 is essential for ensuring proper representation when dealing with tax matters. However, several misconceptions surround this important document. Here are nine common misunderstandings:

Many people believe that the Tax POA form is solely for corporate use. However, individuals can also use this form to authorize someone to act on their behalf regarding tax-related issues.

Submitting the POA form does not mean the IRS will automatically accept all requests made by the designated representative. Each request is evaluated on a case-by-case basis.

This form allows individuals to designate various representatives, not just attorneys. Friends, family members, or tax professionals can be named, providing flexibility.

Many believe they must fill out a new POA form every tax year. In fact, the form remains valid until the taxpayer revokes it or the representative no longer qualifies.

While the form is versatile, it is important to note that it has specific limitations. It doesn't cover issues unrelated to taxation or matters outside the jurisdiction of the IRS.

Some individuals think that the Tax POA form must be notarized to be valid. Notarization is not necessary, though having it notarized can add an extra layer of verification.

Contrary to popular belief, revoking the Power of Attorney is straightforward. By submitting a written statement to the IRS, you can successfully terminate the authorization.

Another misunderstanding is the belief that only one person can be designated. Multiple representatives can be appointed to assist with tax matters, provided you specify them on the form.

While the 20A100 form is commonly associated with federal tax representation, it can also be used for state tax matters. It’s essential to check the specific requirements of your state to ensure compliance.

Addressing these misconceptions can help taxpayers navigate the complexities of tax representation more effectively and confidently.

When navigating the Tax POA form 20a100, there are several crucial aspects to keep in mind. Understanding these points can make the process more straightforward and help ensure you’re fully prepared.

By carefully following these guidelines, you can manage your tax-related matters more efficiently through the proper use of the Tax POA form 20a100.