The Tax Power of Attorney (POA) form 21-002-13 serves as a critical tool for individuals or organizations seeking to authorize another person to represent them in tax matters. This form allows taxpayers to designate an agent who can interact with the Internal Revenue Service (IRS) on their behalf. Key components of the form include the identification of the taxpayer, the agent appointed, and the specific tax matters that the agent is allowed to handle. Additionally, the form outlines the duration of the authority granted, ensuring that the agent's power is limited to a certain timeframe unless otherwise extended. Completing this form is essential for ensuring proper communication with the IRS, facilitating a smoother resolution to tax issues. Homeowners, business owners, and others can all benefit from understanding how to effectively use the Tax POA form, which can prevent misunderstandings and streamline tax processes. Furthermore, knowing the requirements and implications of this authorization is crucial for anyone looking to safeguard their financial interests.

- DEPARTMENT OF - |

POWER OF ATTORNEY |

|

REV EN UE |

AND |

STATE OF M I SS I SSIPPI |

DECLARATION OF REPRESENTATION |

Form

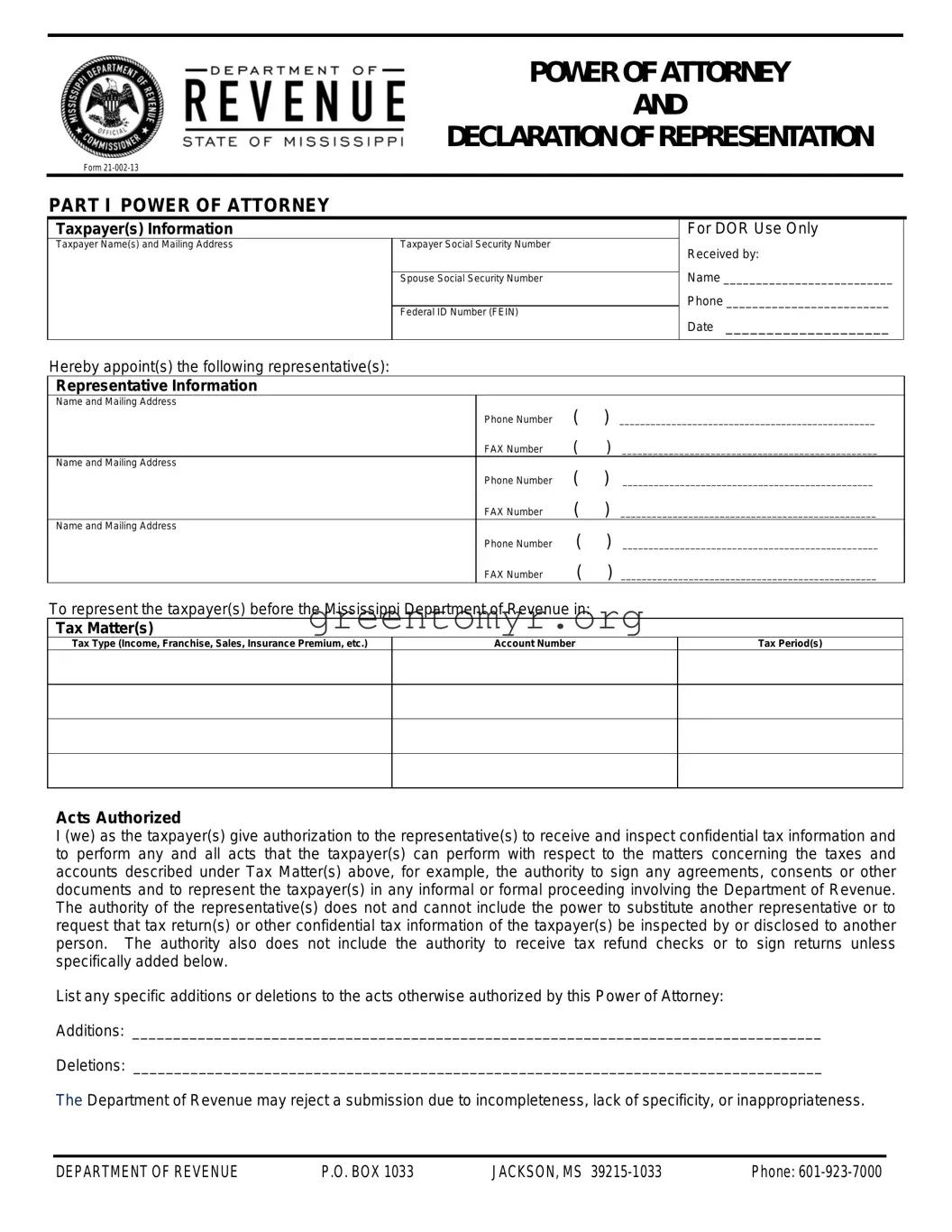

PART I POWER OF ATTORNEY

Taxpayer(s) Information

Taxpayer Name(s) and Mailing Address |

Taxpayer Social Security Number |

|

Spouse Social Security Number |

|

Federal ID Number (FEIN) |

For DOR Use Only

Received by:

Name __________________________

Phone _________________________

Date ____________________

Hereby appoint(s) the following representative(s):

Representative Information

Name and Mailing Address

Phone Number |

( |

) |

_________________________________________________ |

FAX Number |

( |

) |

_________________________________________________ |

Name and Mailing Address |

( |

) |

|

Phone Number |

________________________________________________ |

||

FAX Number |

( |

) |

_________________________________________________ |

Name and Mailing Address |

( |

) |

|

Phone Number |

_________________________________________________ |

||

FAX Number |

( |

) |

_________________________________________________ |

To represent the taxpayer(s) before the Mississippi Department of Revenue in:

Tax Matter(s)

Tax Type (Income, Franchise, Sales, Insurance Premium, etc.)

Account Number

Tax Period(s)

Acts Authorized

I (we) as the taxpayer(s) give authorization to the representative(s) to receive and inspect confidential tax information and to perform any and all acts that the taxpayer(s) can perform with respect to the matters concerning the taxes and accounts described under Tax Matter(s) above, for example, the authority to sign any agreements, consents or other documents and to represent the taxpayer(s) in any informal or formal proceeding involving the Department of Revenue. The authority of the representative(s) does not and cannot include the power to substitute another representative or to request that tax return(s) or other confidential tax information of the taxpayer(s) be inspected by or disclosed to another person. The authority also does not include the authority to receive tax refund checks or to sign returns unless specifically added below.

List any specific additions or deletions to the acts otherwise authorized by this Power of Attorney:

Additions: ____________________________________________________________________________________

Deletions: ____________________________________________________________________________________

The Department of Revenue may reject a submission due to incompleteness, lack of specificity, or inappropriateness.

DEPARTMENT OF REVENUE |

P.O. BOX 1033 |

JACKSON, MS |

Phone: |

DOR Power of Attorney, Form

Retention/Revocation of Prior Power(s) of Attorney

The filing of this Power of Attorney automatically revokes all earlier Power(s) of Attorney on file with the Department of Revenue for the same tax matter(s) covered by this document. If you do not want to revoke a prior Power or Attorney,

check here D

and ATTACH A COPY OF THE POWER(S) OF ATTORNEY YOU WANT TO REMAIN IN EFFECT.

and ATTACH A COPY OF THE POWER(S) OF ATTORNEY YOU WANT TO REMAIN IN EFFECT.

Who Must Sign and What Documentation of Authority Must Be Attached

If a tax matter concerns a joint return, both husband and wife must sign if joint representation is requested. A corporation or subsidiary MUST contain the signatures of a principal officer and the secretary or other officer. A guardian, executor, receiver, administrator, conservator or trustee MUST attach the appropriate documentation granting the authority from the court or taxpayer.

Signing is Certification Under Oath Subject to Penalty of Perjury

The person(s) signing this Power of Attorney and Declaration of Representations certifies under oath that all the information contained in this document is true and correct and that he, she or they have the authority to sign this document as the taxpayer(s) or on behalf of the taxpayer(s) and acknowledge that this Power of Attorney and Declaration of Representation is being signed under the penalty of perjury pursuant to Miss. Code Ann. §

IF NOT SIGNED AND DATED, THIS POWER OF ATTORNEY WILL BE RETURNED.

Signature |

Date |

Title (if applicable) |

Print Name |

Phone Number |

FAX Number |

Signature |

Date |

Title (if applicable) |

Print Name |

Phone Number |

FAX Number |

PART II DECLARATION OF REPRESENTATIVE

Under penalties of perjury and Miss. Code Ann.

1)I am authorized to represent the taxpayer(s) identified in Part I for the tax matter(s) specified there: and

2)I am one of the following:

a.Attorney – a member in good standing of the bar of the highest court of the jurisdiction shown below.

b.Certified Public Accountant – duly authorized to practice as a certified public accountant in the jurisdiction shown.

c.Officer – a bona fide officer of the taxpayer’s organization.

d.

e.Family Member – a member of the taxpayer’s immediate family (i.e., spouse, parent, child, brother, or sister).

f.Enrolled Agent – enrolled as an agent under the requirements of the IRS.

g.Other – Provide explanation ________________________________________________________________

IF NOT SIGNED AND DATED, THIS POWER OF ATTORNEY WILL BE RETURNED.

Designation – Insert |

State Issuing |

State License |

Above letter |

License |

Number |

|

|

|

Signature

Date

DEPARTMENT OF REVENUE |

P.O. BOX 1033 |

JACKSON, MS |

Phone: |

| Fact Name | Details |

|---|---|

| Form Title | Tax Power of Attorney (Form 21-002-13) |

| Purpose | To authorize an individual or organization to represent a taxpayer in dealings with the IRS. |

| Governing Law | This form is governed by Internal Revenue Code Sections 6013(e) and 6103(e). |

| Who Can Use It | Any individual, corporation, or partnership can use this form to appoint a representative. |

| Filing Method | The completed form can be submitted electronically or by mail to the appropriate IRS office. |

| Effective Date | This form takes effect once signed and dated by the taxpayer and the representative. |

After you have gathered the necessary information, you are ready to start filling out the Tax POA form 21-002-13. This form is important for designating someone to represent you in tax matters. Taking careful steps ensures that you provide accurate information, helping to avoid potential delays or issues.

Once the form is submitted, you should allow for some processing time. Your representative can then begin to act on your behalf for the matters specified in the form. It's always a good idea to follow up to ensure that everything has been received and is in order.

The Tax POA form 21-002-13 is a Power of Attorney form that allows an individual to appoint someone else to act on their behalf regarding tax matters. This might include the ability to discuss tax issues with the IRS, file tax returns, or receive tax refunds. It is commonly used when taxpayers are unable to manage their tax affairs themselves, whether due to illness, absence, or other reasons.

You can choose any person to serve as your representative by using the Tax POA form 21-002-13. Common choices include trusted family members, friends, or tax professionals such as accountants or attorneys. Just ensure that the person you appoint is willing to take on this responsibility and understands the complexities of tax matters.

Filling out the form involves several straightforward steps:

The authority granted under the Tax POA form 21-002-13 remains in effect until you formally revoke it or until the representative dies, becomes incapacitated, or is no longer willing to serve. If you wish to end the arrangement, you must submit a written notice of revocation to the IRS and notify your representative.

Yes, you can revoke the Tax POA at any time, as long as you follow the proper procedures. Typically, this involves submitting a revocation form to the IRS and notifying your previously appointed representative. Following these steps ensures that your tax matters are handled according to your current preferences.

Generally, there is no fee to submit the Tax POA form 21-002-13 to the IRS. However, if you choose to work with a tax professional to help prepare and file the form, they may charge a fee for their services. It's always wise to discuss costs upfront if you're working with someone on tax matters.

Once you have completed the Tax POA form 21-002-13, you will need to send it to the address specified by the IRS for your particular situation. This could differ based on where you live and other factors. Always check the IRS instructions for the most accurate mailing address to ensure timely processing.

Filling out the Tax POA form 21-002-13 can be a straightforward process, but mistakes can lead to delays or complications in tax matters. One common mistake is failing to provide accurate personal information. Individuals often overlook the importance of entering precise names, addresses, and taxpayer identification numbers. Incorrect or incomplete information can cause significant issues when the IRS attempts to process the form.

Another frequent error involves omitting signatures. Each individual listed on the form must sign it, and a missing signature renders the document invalid. Some people mistakenly assume a power of attorney is valid without the necessary signatures, but this is not the case. Ensure that all parties involved sign the document before submission.

Additionally, many individuals ignore the specific tax year or years for which the power of attorney is being granted. Clearly indicating the relevant tax years helps establish the scope of representation. Without this detail, the IRS may not recognize the authority granted to the representative.

Some filers misuse or fail to select the appropriate representative designation. The form allows individuals to appoint an attorney, an accountant, or another qualified person. Not selecting the correct designation can lead to complications when the representative attempts to act on behalf of the taxpayer.

People often miss the critical requirement of providing a clear and concise description of the tax matters involved. A vague explanation can lead to misunderstandings between the taxpayer and the representative. It is vital to outline the scope of the representation to ensure both parties are on the same page.

In some cases, taxpayers overlook the importance of checking for updates to the form and instructions. The IRS may revise forms or procedures that affect how the POA is implemented. Staying informed about the latest requirements prevents mistakes stemming from outdated information.

Errors can also arise from submitting the form without a cover letter or accompanying documentation. Including a cover letter can clarify the intent of the submission and provide context for the representative's actions. This practice streamlines communication with the IRS.

A significant mistake involves not keeping copies of the submitted form for personal records. Documenting all communications and submissions is essential in case questions arise later. Without a copy, the taxpayer may face difficulties proving that the form was submitted.

Lastly, individuals sometimes fail to consult with their representatives before submitting the form. Open communication is crucial to ensure that everyone understands their roles and responsibilities. This simple conversation can prevent misunderstandings that may complicate matters down the line.

The Tax Power of Attorney (POA) form 21-002-13 allows a designated individual to act on behalf of another person regarding tax matters. When filing this form, other documents may also be necessary to ensure comprehensive representation. Below is a list of commonly used forms and documents that accompany the Tax POA form.

These documents play significant roles in ensuring that tax matters are handled efficiently. Being organized with the necessary paperwork helps avoid delays and facilitates clear communication with tax authorities.

When completing the Tax POA form 21-002-13, attention to detail is essential. The following guidelines outline important do’s and don’ts that can help ensure a smooth submission process.

Do:

Don’t:

By adhering to these guidelines, individuals can navigate the process of filling out the Tax POA form more confidently and efficiently.

Many people misunderstand the Tax POA form 21-002-13. Here are six common misconceptions, along with clear explanations.

This is false. The Tax POA form is intended for specific authorization situations. Only individuals or entities that meet certain criteria, such as being a qualified representative, can complete and submit this form on behalf of a taxpayer.

This is not accurate. The authority granted through the Tax POA form is limited to the specific matters outlined in the form. The taxpayer can control what powers are given and can revoke them at any time.

This misconception is misleading. Once the Tax POA form is submitted, it remains valid until it is revoked, the purpose is fulfilled, or the representative resigns. There's no annual renewal requirement.

This is incorrect. While many people choose attorneys for this task, the Tax POA form can also be completed by non-attorney representatives, as long as they meet the qualifications outlined by the IRS.

This statement is misleading. Although primarily designed for tax issues, the Tax POA form can also assist with related matters where a taxpayer requires representation before the IRS.

This is untrue. A taxpayer can revoke the Power of Attorney at any time by submitting a revocation form. It is essential to communicate changes to all parties involved.

The Tax POA form 21-002-13 is important for anyone who needs to authorize someone else to handle their tax matters. Here are key takeaways about filling it out and using it effectively:

This form empowers your chosen representative to act on your behalf regarding tax issues, ensuring that you have support when needed.