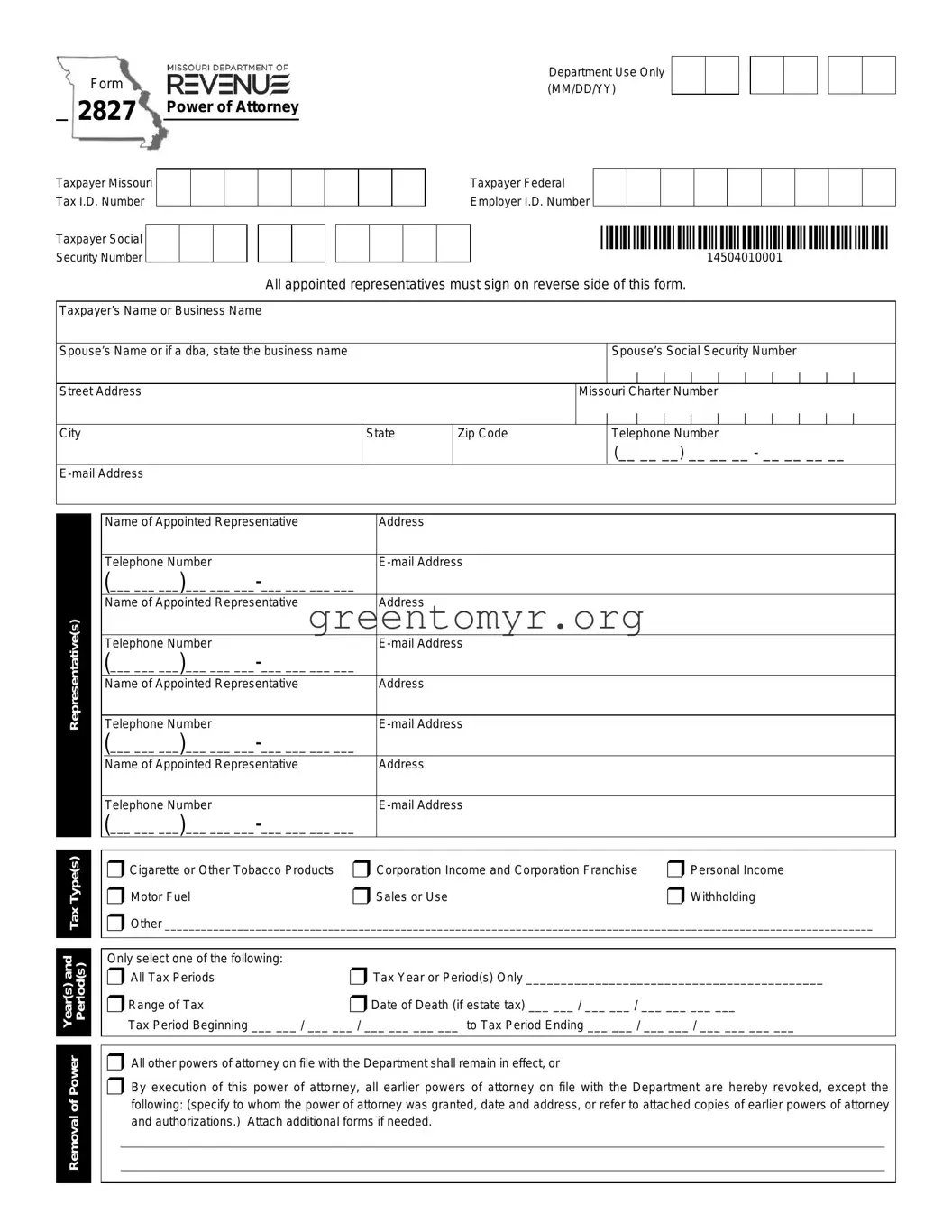

The IRS Tax Power of Attorney (POA) Form 2827 is an essential document that allows individuals to designate someone to represent them in tax matters. This form simplifies the process for taxpayers, creating a formal relationship between the taxpayer and their chosen representative. By completing Form 2827, you grant authority for your representative to handle a range of interactions with the IRS, such as discussing your tax return, negotiating settlements, or obtaining tax information on your behalf. This is particularly beneficial when dealing with complex tax situations or disputes. The form requires specific information, including your details, your representative's contact information, and the scope of the authority granted, ensuring clarity and understanding in the representation agreement. Understanding how to fill out and submit this form correctly can greatly alleviate the burdens of tax compliance and provide peace of mind in managing your tax affairs.

Form |

|

R:V:NUS |

|

|

|

|

(MM/DD/YY) |

[IJ[IJ[IJ |

||

|

|

|

DEPARTMENT OF |

|

|

|

|

Department Use Only |

|

|

2827 |

|

|

|

|

|

|

|

|

||

|

Power of Attorney |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||

Taxpayer Missouri |

I |

I |

I |

I I I |

I |

I |

I |

Taxpayer Federal |

I I I I I I I |

|

Tax I.D. Number |

Employer I.D. Number I I I |

|||||||||

Taxpayer Social |

|

I |

I |

IITJ I |

I |

I |

I |

I |

*14504010001* |

|

Security Number I |

|

|

14504010001 |

|||||||

All appointed representatives must sign on reverse side of this form.

Taxpayer’s Name or Business Name

Spouse’s Name or if a dba, state the business name |

|

|

|

Spouse’s Social Security Number |

|

|

|

|

|

|

I |

| | | | | | |

| |

| |

| |

Street Address |

|

|

Missouri Charter Number |

|

|

|

|

|

|

|

I | |

| | | | | | |

| |

| |

| |

City |

State |

Zip Code |

|

Telephone Number |

|

|

|

|

I |

I |

I(__ __ __) __ __ __ - __ __ __ __ |

|

|||

|

|

|

|

|

|

|

|

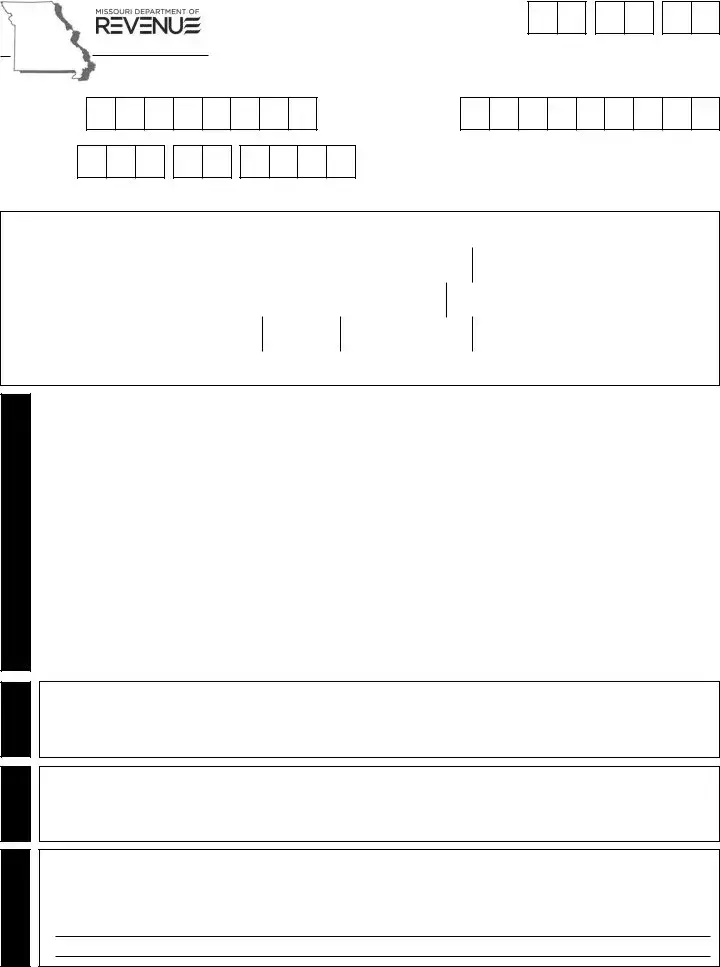

Representative(s)

Year(s) and Removal of Power Period(s) Tax Type(s)

Name of Appointed Representative |

Address |

|

|

Telephone Number |

|

(___ ___ ___)___ ___ |

|

Name of Appointed Representative |

Address |

|

|

Telephone Number |

|

(___ ___ ___)___ ___ |

|

Name of Appointed Representative |

Address |

|

|

Telephone Number |

|

(___ ___ ___)___ ___ |

|

Name of Appointed Representative |

Address |

|

|

Telephone Number |

|

(___ ___ ___)___ ___ |

|

rCigarette or Other Tobacco Products r Corporation Income and Corporation Franchise r Personal Income

r Motor Fuel |

r Sales or Use |

r Withholding |

rOther _____________________________________________________________________________________________________________________

Only select one of the following: |

|

r All Tax Periods |

r Tax Year or Period(s) Only ___________________________________________ |

r Range of Tax |

r Date of Death (if estate tax) ___ ___ / ___ ___ / ___ ___ ___ ___ |

Tax Period Beginning ___ ___ / ___ ___ / ___ ___ ___ ___ to Tax Period Ending ___ ___ / ___ ___ / ___ ___ ___ ___

rAll other powers of attorney on file with the Department shall remain in effect, or

rBy execution of this power of attorney, all earlier powers of attorney on file with the Department are hereby revoked, except the following: (specify to whom the power of attorney was granted, date and address, or refer to attached copies of earlier powers of attorney and authorizations.) Attach additional forms if needed.

Signature

Under penalties of perjury, I (we) hereby certify that I (we) am (are) the taxpayer(s) named herein or that I have the authority to execute this power of attorney on behalf of the taxpayer(s).

Name

Signature |

Date (MM/DD/YYYY) |

Taxpayer Telephone Number |

|

__ __ / __ __ / __ __ __ __ |

I(___ ___ ___)___ ___ |

Name |

Title (if applicable) |

|

|

|

|

Signature |

Date (MM/DD/YYYY) |

Taxpayer Telephone Number |

|

__ __ / __ __ / __ __ __ __ |

I(___ ___ ___)___ ___ |

Declaration of Representative(s)

Please consult Missouri Regulation 12 CSR

I declare that I am aware of Regulation 12 CSR

1. |

a member in good standing of the bar; |

5. |

a fiduciary for the taxpayer; |

2. |

a certified public accountant duly qualified to practice; |

6. |

an enrolled agent; |

3. |

an officer of the taxpayer organization; |

7. |

tax preparer, or |

4. |

a |

8. |

other authorized representative or agent |

Note: All appointed representatives must sign below. No digital signatures allowed.

Printed Name of Representative |

Signature of Representative |

Date (MM/DD/YYYY) |

||||||

|

|

|

|

|

|

|

|

___ ___ / ___ ___ / ___ ___ ___ ___ |

Designation (Please select number from list above) |

|

|

Title (if applicable) |

|

||||

r 1 |

r 2 |

r 3 |

r 4 |

r 5 r 6 r 7 |

r 8 |

|

|

|

|

|

|

|

|||||

Printed Name of Representative |

Signature of Representative |

Date (MM/DD/YYYY) |

||||||

|

|

|

|

|

|

|

|

___ ___ / ___ ___ / ___ ___ ___ ___ |

Designation (Please select number from list above) |

|

|

Title (if applicable) |

|

||||

r 1 |

r 2 |

r 3 |

r 4 |

r 5 r 6 r 7 |

r 8 |

|

|

|

|

|

|

|

|||||

Printed Name of Representative |

Signature of Representative |

Date (MM/DD/YYYY) |

||||||

|

|

|

|

|

|

|

|

___ ___ / ___ ___ / ___ ___ ___ ___ |

|

|

|

|

|

||||

Designation (Please select number from list above) |

|

|

Title (if applicable) |

|

||||

r 1 |

r 2 |

r 3 |

r 4 |

r 5 r 6 r 7 |

r 8 |

|

|

|

|

|

|

|

|||||

Printed Name of Representative |

Signature of Representative |

Date (MM/DD/YYYY) |

||||||

|

|

|

|

|

|

|

|

___ ___ / ___ ___ / ___ ___ ___ ___ |

|

|

|

|

|

||||

Designation (Please select number from list above) |

|

|

Title (if applicable) |

|

||||

r 1 |

r 2 |

r 3 |

r 4 |

r 5 r 6 r 7 |

r 8 |

|

|

|

|

|

|

|

|

|

|

|

|

Mail to: |

|

|

Form 2827 (Revised |

|

|

|

|

(Business Tax) |

(Personal Tax) |

(Motor Fuel Tax) |

(Cigarette or Other Tobacco Products Tax) |

Taxation Division |

Taxation Division |

Taxation Division |

Taxation Division |

P.O. Box 357 |

P.O. Box 2200 |

P.O. Box 300 |

P.O. Box 811 |

Jefferson City, MO |

Jefferson City, MO |

Jefferson City, MO |

Jefferson City, MO |

Phone: (573) |

Phone: (573) |

Phone: (573) |

Phone: (573) |

Fax: (573) |

Fax: (573) |

Fax: (573) |

Fax: (573) |

If this is being submitted in response to an audit, please fax to (573)

Visit http://dor.mo.gov/ for additional information.

*14504020001*

14504020001

| Fact Name | Fact Description |

|---|---|

| Purpose | The Tax Power of Attorney (POA) Form 2827 allows individuals to appoint a representative to act on their behalf in matters related to taxes. |

| Eligibility | Any individual who wishes to grant authority for tax-related matters can use Form 2827. |

| Signature Requirement | To be valid, the form must be signed by the taxpayer granting the power of attorney. |

| Governing Law | In the United States, this form is governed by federal tax law, specifically under the Internal Revenue Code. |

| Designated Representative | The individual appointed can be a tax professional, attorney, or any trusted friend or family member. |

| Scope of Authority | The form allows the representative to perform various tasks, such as receiving tax documents and communicating with the IRS. |

| Submission Method | Form 2827 can be submitted via mail or fax to the appropriate IRS office depending on the taxpayer's location. |

| Duration of Authority | The power granted remains in effect until revoked by the taxpayer or the represented individual no longer meets the qualifications. |

| Revocation Process | Taxpayers can revoke the power of attorney by submitting a written notice to the IRS. |

| State-Specific Requirements | Some states might have additional forms or requirements for tax powers of attorney; researching state laws is essential. |

Once you have the Tax POA form 2827 ready, you will need to fill it out accurately before submission to the appropriate IRS office. This process will ensure that the appointed representative has the authority to act on your behalf regarding tax matters.

Once submitted, the IRS will process your form, allowing your representative to act for you in matters specified. Ensure you keep track of any communications regarding your tax matters moving forward.

The Tax POA Form 2827, also known as the Power of Attorney form, allows taxpayers to authorize another individual, including tax professionals, to act on their behalf before the IRS. This form grants the designated representative the authority to receive and handle tax-related communications and issues, streamlining interactions with the IRS for taxpayers.

Any taxpayer, whether an individual or a business entity, can use the Tax POA Form 2827. This includes:

It is important that the person designated as the representative has a valid relationship with the taxpayer and is capable of handling the specific tax issues at hand.

To complete the Tax POA Form 2827, follow these steps:

After completing the form, mail it to the appropriate IRS office address as indicated in the form’s instructions. You may also consult your tax professional for assistance in submission.

Yes, the authorization granted through the Tax POA Form 2827 generally remains in effect until the taxpayer revokes it in writing, the IRS terminates it, or the designated representative becomes deceased. It is advisable to periodically review the authorization to ensure it fits current needs.

If you need to revoke the authorization, submit a written statement to the IRS that clearly indicates your intention. This statement should include:

Mail this revocation statement to the same IRS office where you submitted the original Form 2827. Doing so will notify the IRS that the representative no longer has authority to act on your behalf.

Filling out the Tax Power of Attorney (POA) form 2848 can feel overwhelming, but avoiding common mistakes can make the process much smoother. One of the most frequent errors people make is not providing all the necessary information. When you leave out critical details, such as the taxpayer’s Social Security Number or Taxpayer Identification Number, it can cause delays. Always double-check to ensure that all required fields are filled correctly and thoroughly.

Another common mistake involves improperly designating the representative. It’s important to ensure that the person you are granting power of attorney to is qualified and listed correctly. Some individuals try to name multiple representatives without clearly indicating who is the primary contact. Keeping it clear and concise is crucial to avoid confusion.

Many people also overlook the importance of signing the form. A missing signature can lead to rejection by the IRS. Make sure that the person granting the power of attorney—and not just the representative—signs the form. Remember, both parties must sign for the document to be valid.

Inadequate explanations regarding the powers granted can result in misunderstandings. The form includes sections where you can specify what authority you are granting. Be precise. If you leave it too vague, the representative may not be able to act on your behalf in the way you intended. Clarity is essential.

Not keeping a copy of the completed form is another typical oversight. After filing, it’s wise to retain a copy for your own records. This can be a useful reference in case of any future disputes or questions regarding the powers you’ve designated. Simple oversight can create unnecessary complications down the road.

Many individuals also underestimate the timelines involved in processing the form. Submitting it close to a deadline can lead to stress and potentially missed opportunities for tax relief or negotiation. Plan ahead and file the form well in advance to avoid last-minute issues.

Another mistake people often make is neglecting to inform the representative about the extent of their authority. Ensure that the person you designate understands their responsibilities and the limits of their power. This way, there’s no room for misunderstandings about what actions they can take on your behalf.

Finally, consider the communication with the IRS. Failing to inform the IRS about changes or the revocation of a POA can create confusion. If a situation arises where you need to terminate the power of attorney, be sure to communicate this effectively to avoid any complications. Always follow up to ensure that the IRS has processed the revocation if necessary.

The Tax Power of Attorney (POA) Form 2848 is essential for taxpayers who wish to appoint an individual to act on their behalf before the Internal Revenue Service (IRS). This form is commonly used alongside several other documents that facilitate tax-related processes. Below is a list of frequently associated forms and documents that assist taxpayers in managing their legal and financial affairs.

Understanding these forms and their purposes can help taxpayers navigate the complexities of tax management. Utilizing the correct forms efficiently can streamline processes and reduce potential misunderstandings with tax authorities.

When filling out the Tax POA Form 2827, it’s important to keep a few key do's and don'ts in mind. Here’s a straightforward list to help you navigate the process effectively:

By following these guidelines, you can help ensure a smoother process when handling your Tax POA Form 2827.

It is common for individuals to hold misconceptions about the IRS Form 2848, Power of Attorney and Declaration of Representative, often referred to as the Tax POA form. This form allows taxpayers to appoint someone to represent them before the IRS. Below is a list of nine prevalent misconceptions regarding this form.

This is incorrect. While the form is primarily used for tax matters, it can also be applied in other areas where representation is required before the IRS.

This is not true. A taxpayer can appoint multiple representatives by filing separate forms or including multiple representatives on the same form.

This is a misconception. While attorneys are eligible, taxpayers can also appoint certified public accountants, enrolled agents, or other qualified individuals to represent them.

The Tax POA form is straightforward. It requires basic information, such as the taxpayer's details and signatures. Most individuals can complete it without difficulty.

This is a misunderstanding. The form remains in effect until it is revoked, a new form is submitted, or the individual’s authority is discontinued.

In reality, the authority granted by the form is limited to specific matters outlined by the taxpayer. The representative's access is not unlimited.

This is misleading. The taxpayer retains the right to revoke the representation at any time by submitting a revocation form to the IRS.

This is not the case. There is no fee associated with filing the Tax POA form with the IRS.

In fact, the form can also be submitted electronically through some IRS e-file services, making it more accessible for taxpayers.

Clarifying these misconceptions can alleviate concerns and help individuals better understand the process of appointing a representative for tax matters.

Here are some essential points to consider when filling out and using the Tax Power of Attorney (POA) Form 2827: