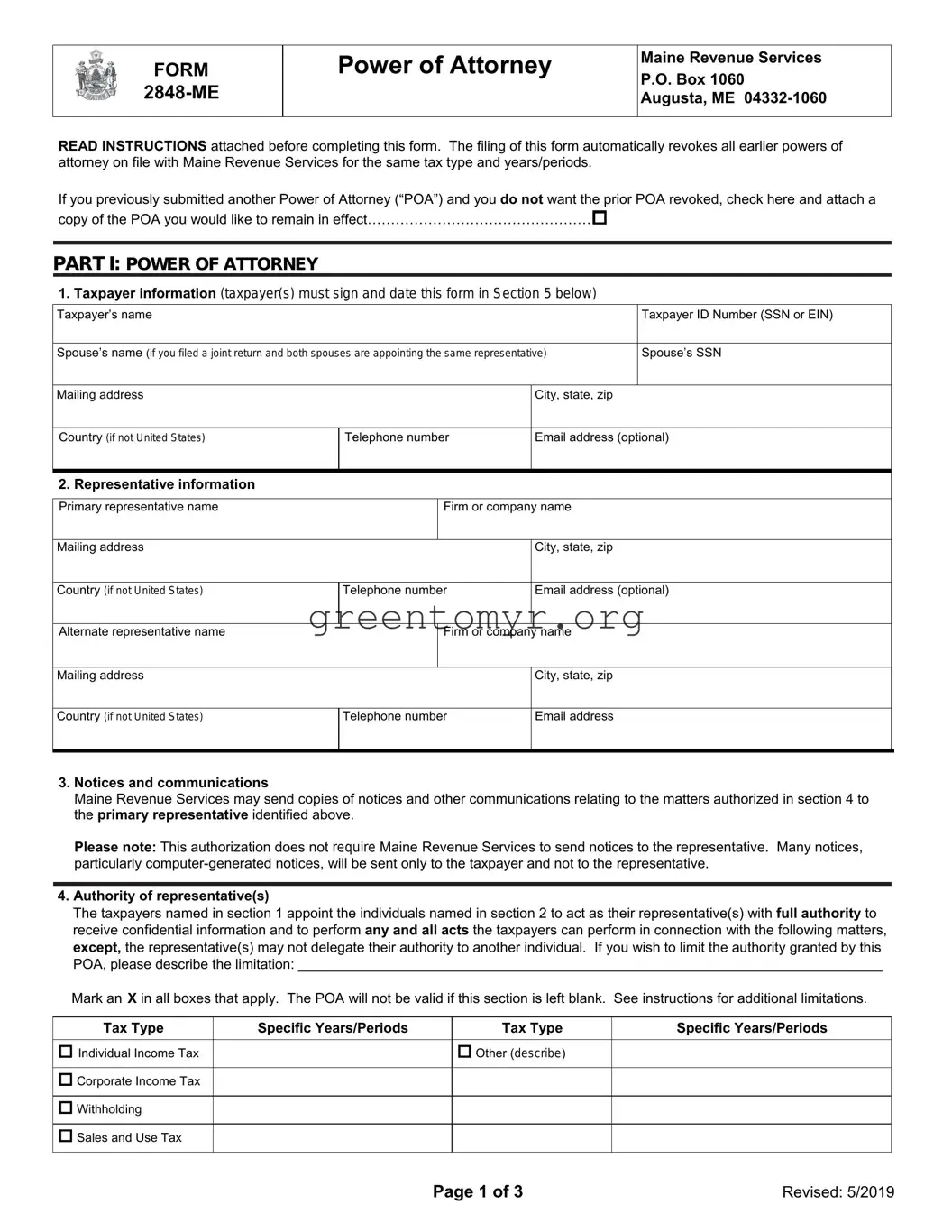

The Tax Power of Attorney form 2848-ME is a crucial document for taxpayers in Maine, enabling individuals to authorize someone else to act on their behalf in tax matters. This form is designed specifically for the state of Maine, catering to the unique tax regulations and requirements that govern the state. It allows taxpayers to appoint a representative who has the authority to handle various tax-related tasks, such as filing returns, discussing tax issues with state tax authorities, and receiving confidential information pertinent to the taxpayer’s account. By completing this form, individuals can delegate their responsibilities while ensuring that their interests are protected during interactions with the Maine Revenue Services. The document requires essential information, including the taxpayer's name, address, and Social Security number, as well as the representative's details. Furthermore, it is important to note that the appointment can be limited to specific tax years or types of tax, granting flexibility to the taxpayer in managing their tax obligations. This practical form not only streamlines communication with tax authorities but also provides peace of mind, allowing taxpayers to engage knowledgeable representatives suited for complex tax situations.

FORM

Power of Attorney

Maine Revenue Services

P.O. Box 1060

Augusta, ME

READ INSTRUCTIONS attached before completing this form. The filing of this form automatically revokes all earlier powers of attorney on file with Maine Revenue Services for the same tax type and years/periods.

If you previously submitted another Power of Attorney (“POA”) and you do not want the prior POA revoked, check here and attach a copy of the POA you would like to remain in effect…………………………………………

PART I: POWER OF ATTORNEY

1.Taxpayer information (taxpayer(s) must sign and date this form in Section 5 below)

Taxpayer’s name |

Taxpayer ID Number (SSN or EIN) |

|

|

Spouse’s name (if you filed a joint return and both spouses are appointing the same representative) |

Spouse’s SSN |

|

|

Mailing address

Country (if not United States) |

Telephone number |

I

2. Representative information

City, state, zip

Email address (optional)

Primary representative name |

Firm or company name |

|

I |

|

City, state, zip |

Mailing address |

|

|

|

|

|

|

Email address (optional) |

Country (if not United States) |

Telephone number |

||

|

I |

|

name |

Alternate representative name |

Firm or company |

|

|

|

I |

|

City, state, zip |

Mailing address |

|

|

|

|

|

|

Email address |

Country (if not United States) |

Telephone number |

||

|

I |

|

|

3.Notices and communications

Maine Revenue Services may send copies of notices and other communications relating to the matters authorized in section 4 to the primary representative identified above.

Please note: This authorization does not require Maine Revenue Services to send notices to the representative. Many notices, particularly

4.Authority of representative(s)

The taxpayers named in section 1 appoint the individuals named in section 2 to act as their representative(s) with full authority to receive confidential information and to perform any and all acts the taxpayers can perform in connection with the following matters, except, the representative(s) may not delegate their authority to another individual. If you wish to limit the authority granted by this POA, please describe the limitation: ___________________________________________________________________________

Mark an X in all boxes that apply. The POA will not be valid if this section is left blank. See instructions for additional limitations.

Tax Type |

Specific Years/Periods |

Tax Type |

Individual Income Tax |

|

Other (describe) |

Corporate Income Tax

Withholding

Sales and Use Tax

Specific Years/Periods

Page 1 of 3 |

Revised: 5/2019 |

5.Taxpayer signature

I certify, under penalty of perjury, that I am the taxpayer identified in section 1 above, or if signing as a corporate officer, that I am a partner, member, manager, or fiduciary acting on behalf of the taxpayer, that I have the authority to execute this POA.

Signature

Print name (and title, if applicable)

Date

Spouse’s signature (required if listed above)

Print name

Date

PART II: DECLARATION OF REPRESENTATIVE

I certify, under penalty of perjury, that I am:

Primary Alternate

A member in good standing of the bar of the highest court of the following jurisdiction: ______________________

Duly qualified to practice as a certified public accountant in the following jurisdiction: _______________________

|

An enrolled agent under U.S. Department of Treasury Circular 230 |

A bona fide officer of the taxpayer’s organization

A

|

A member of the taxpayer’s immediate family |

A fiduciary of the taxpayer

Other (explain): ______________________________________________________________________________

Signature – Primary Representative

Print name (and title, if applicable)

Date

Signature – Alternate Representative

Print name (and title, if applicable)

Date

FORMS NOT SIGNED, DATED, OR OTHERWISE INCOMPLETE WILL NOT BE ACCEPTED.

Page 2 of 3 |

Revised: 5/2019 |

Instructions

General Information

Use Form

Unless you limit the authority (see section 4), your representative will be authorized to perform any and all acts you can perform, including, but not limited to: receiving your confidential information; agreeing to tax adjustments; signing settlement agreements; and making otherwise binding decisions on your behalf with regard to the tax matters covered by the POA.

Limited Power of Attorney Form

If you want your representative to communicate with and receive confidential information from MRS, but you do not want that person to act on your behalf, please fill out Form

Revocation

Filing Form

Example 1:

On 5/1/2017, you authorize Jane Doe to represent you for individual income tax for 2015. On 10/1/2017, you authorize Jim Jones to represent you for individual income tax for 2016. Both POA’s are valid.

Example 2:

On 5/1/2017, you authorize Jane Doe to represent you for individual income tax for 2015. On 10/1/2017, you authorize Jim Jones to represent you for sales and use tax for 2015. Both POA’s will be valid.

Example 3:

On 5/1/2017, you authorize Jane Doe to represent you for individual income tax for 2015. On 10/1/2017, you authorize Jim Jones to represent you for individual income tax for years

If you do not want a prior POA automatically revoked, you must check the box at the top of the form and attach a copy of the prior POA you would like to remain in effect.

Other requests to revoke a POA must be in writing and must be signed by the taxpayer.

Section 2 – Representative information

Form

Section 3 – Notices and communications

MRS may send copies of notices and other communications relating to the tax matters authorized in section 4 only to the primary representative. Many notices, particularly

Section 4 – Authority of representatives

This section allows you to specify which tax matters are covered by the POA and what authority you are granting your representative. By default, your representative will have full authority to receive your confidential information and to perform any and all acts you can perform in connection with the matters described in section 4. However, your authorized representative may not delegate their authority to another individual. If you wish to limit your representative’s authority, please specifically describe the limitation.

For this form to be valid, you must select both the tax type and years/periods covered by the POA. If no tax type is selected, the POA will not be accepted.

You may list current, prior, or future years/periods. You must use specific periods. General references such as “All Years” will not be accepted.

Note: MRS will not accept a POA for future years/period which begin more than three years from the date the POA is received by MRS.

Section 5 – Taxpayer signature

You must sign, print your name, and date the POA for it to be valid. If you filed a joint return and both spouses are appointing the same representative, both spouses must sign. POA forms must be hand- signed.

If you are signing on behalf of the taxpayer, please include your

PART I – Power of Attorney

Section 1 – Taxpayer information

The Taxpayer’s identification number may be a social security number (“SSN”) or employer identification number (“EIN”) depending on the type of taxpayer. Please fill out the taxpayer information section accurately and completely. Note: By providing an email address, you authorize MRS to communicate your confidential information via email to the address provided.

PART II – Declaration of Representatives

Your representative must indicate their relationship to you and sign and date the form. The POA must be signed by the representative to be valid.

Submitting Completed POA Form

Completed POA forms should be mailed to MRS at the address at the top of the form. Completed POA forms may also be faxed or emailed to the MRS division responsible for the tax type covered by the POA. For fax/email contact info for the specific divisions, visit our website at: www.maine.gov/revenue/about/contact.

Page 3 of 3 |

Revised: 5/2019 |

| Fact Name | Details |

|---|---|

| Form Name | Tax Power of Attorney (Form 2848-ME) |

| Purpose | This form allows taxpayers to authorize someone to represent them before the IRS. |

| Eligibility | Any individual or business can appoint a representative using this form. |

| Signatory Requirements | Both the taxpayer and the representative must sign the form to make it valid. |

| Representation Limits | The representative can act on behalf of the taxpayer for specified tax matters only. |

| Submission Method | The completed form can be submitted electronically or via postal mail to the IRS. |

| Expiration | The power of attorney remains in effect until revoked or until the tax matters are resolved. |

| Governing Laws | This form is governed by federal tax laws and regulations. |

| Form Audience | This form is typically used by individual taxpayers, corporations, and accountants. |

| Additional Resources | The IRS website provides guidance and instructions for completing this form. |

Filling out Form 2848 to appoint a representative for tax purposes requires careful attention to detail. Following the steps below will help ensure that the form is completed accurately, allowing for efficient processing by the IRS.

After submission, track the progress of your appointment. The IRS may take some time to process the form, and you may need to follow up if there are any delays or issues related to your representative's authority to act on your behalf.

The Tax POA Form 2848-ME is a Power of Attorney form that allows taxpayers to appoint an individual or organization to represent them before the IRS. This form grants the appointed representative the authority to handle various tax matters on behalf of the taxpayer, including discussions with the IRS, receiving documents, and signing forms as needed.

Taxpayers can appoint any individual, such as a tax professional, attorney, or trusted friend, to represent them. The appointed representative must have a valid Preparer Tax Identification Number (PTIN) or be an enrolled agent, attorney, or certified public accountant.

The form consists of several important sections, including:

The authority granted through Form 2848-ME remains in effect until it is revoked by the taxpayer, the IRS processes a new Form 2848, or the representative is no longer authorized. It is important for taxpayers to maintain a copy of the form and periodically review it to ensure it reflects their current representatives.

Once completed, the form can be submitted to the IRS by mailing it to the appropriate address listed on the IRS website, based on the taxpayer’s location and the type of form being filed. Additionally, the form can also be faxed to the IRS if applicable based on specific IRS guidelines.

Yes, taxpayers can revoke their Power of Attorney at any time. To do this, the taxpayer should submit a written notice to the IRS that includes their name, address, social security number or EIN, and a statement revoking the previous authority. If desired, a new Form 2848 can be filed simultaneously to appoint a different representative.

If tax matters are not specified on Form 2848-ME, the appointed representative may not have the authority to act on your behalf for those unspecified matters. To avoid any potential issues, it is crucial to clearly detail all relevant tax issues within the form.

There is no fee required to file the Form 2848-ME with the IRS. However, if you hire a professional to assist you with completing the form or to represent you, they may charge you a fee for their services. Always clarify any costs with your representative in advance.

When individuals need someone to represent them before the IRS, they often fill out Form 2848, also known as the Power of Attorney (POA) form. However, mistakes can easily occur during this process, complicating matters and delaying representation. Understanding some common errors can help ensure the form is completed correctly.

One frequent mistake is providing incorrect identification information. When entering the tax identification number, such as a Social Security number or Employer Identification Number, it's essential to double-check for accuracy. A small typo can lead to significant delays in processing the form, potentially preventing the designated representative from acting on behalf of the taxpayer.

Another common error occurs when people neglect to sign the form. Without the taxpayer's signature, the IRS will not process the form. Additionally, if the taxpayer is signing on behalf of another individual, it’s crucial to include the appropriate title or indicate the authority under which they are signing. This omission can lead to confusion and rejection of the form.

When filling out the form, individuals sometimes incorrectly select the type of representation being granted. Understanding the different categories of representation is key. Whether it's representation for general matters or for specific tax years or issues affects how the IRS processes the form. Careful consideration and clarity in this section can help prevent disruptions.

The designation of the representative can also be mishandled. Many individuals make the mistake of failing to provide complete information for their representative, such as their address or phone number. The IRS needs all relevant contact details to establish clear communication. Missing information can hinder timely responses and adequate representation.

Sometimes, people leave out important details in the description of matters to be handled. Clarity is vital. Vague or limited details may lead to misunderstandings about the scope of the power granted. It is always best to be as comprehensive as possible to avoid any misinterpretations.

Additionally, individuals often forget to provide a specific timeframe for the representation. While many choose to make the representation effective indefinitely, specifying a start and end date can be crucial in certain situations. This helps to clarify the authority being granted and provides a clear understanding of the relationship between the taxpayer and the representative.

Lastly, keeping a copy of the completed form is a crucial step that many overlook. Without a record, taxpayers may find it challenging to verify what they submitted and may lack important information when following up. Maintaining a copy ensures that both the taxpayer and their representative are on the same page. Taking time to avoid these errors can lead to a smoother process when seeking representation before the IRS.

The Tax Power of Attorney (POA) form 2848-ME is a critical document that allows taxpayers to authorize an individual, typically a tax professional, to act on their behalf regarding tax matters with the IRS. Alongside this form, several other documents may be required to streamline the process. Below is a list of commonly used forms and documents that complement the 2848-ME form.

Familiarity with these documents can help taxpayers navigate the complexities involved in dealing with the IRS. Using the appropriate forms in conjunction with the Tax POA form 2848-ME can ensure that tax matters are handled efficiently and correctly.

When completing the Tax Power of Attorney (POA) Form 2848-ME, it is important to follow specific guidelines to ensure accurate submission. Below is a list of things you should and should not do.

When it comes to the Tax Power of Attorney form 2848-ME, some common misconceptions can lead to confusion. Let’s clarify these myths.

This is false. While many use it to designate accountants or tax preparers, any individual can serve as an agent.

Not true. You can specify the extent of authority given to your agent. You maintain significant control over your tax matters.

This is incorrect. You can submit the form whenever you need someone to represent you for any tax-related issue, regardless of the time of year.

Actually, you can revoke a Power of Attorney at any time by submitting a new form or a written notice to the IRS.

You can limit the authorization to specific tax years or types of taxes. This flexibility allows you to manage your situation effectively.

This is misleading. While it's primarily for federal tax matters, it can also be used for state tax issues, depending on state requirements.

Understanding how to fill out and use the Tax POA form 2848-me can make interactions with the IRS smoother. The following key takeaways can help ensure that the process is clear and effective.

These steps help in ensuring that the process of delegating tax matters is done accurately and effectively.