When navigating the complexities of tax responsibilities, the Tax Power of Attorney (POA) Form 33 emerges as an essential tool for individuals and businesses alike. This form allows taxpayers to authorize a designated representative to act on their behalf, ensuring that critical tax matters are managed effectively. By completing the form, taxpayers grant their chosen representatives the power to handle a variety of tax-related issues, from filing returns to conducting discussions with the IRS or state tax agencies. Importantly, this form emphasizes transparency, requiring taxpayers to provide specific details about the extent of the authority granted and the duration of that authority. Moreover, it safeguards taxpayer rights, as representatives must adhere to the regulations and guidelines set forth by the IRS. For those seeking guidance, the form also outlines clear instructions on how to complete and submit it, making the process accessible and straightforward. Ultimately, understanding the nuances and applications of Form 33 is crucial for anyone looking to streamline their tax interactions while ensuring compliance with federal and state regulations.

|

b)_EBRASl<A- |

|

|

Power of Attorney |

|

FORM |

||||||

|

Good Life. Great Service. |

|

|

|

||||||||

|

|

|

|

|

|

33 |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DEPARTMENT OF REVENUE |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||

I |

|

|

|

|

Taxpayer’s Name and Address |

|

|

I |

||||

|

|

|

Name of Taxpayer |

|

|

Business Name |

|

|

|

|

||

|

|

C: |

|

|

|

|

|

|

|

|

|

|

~- |

|

|

|

|

|

|

|

|||||

Address (Street or Other Mailing Address) |

|

|

Business Address (Street or Other Mailing Address) |

|

|

|

||||||

0 |

|

|

|

|

|

|

|

|

|

|

||

|

|

Q) |

|

|

|

|

|

|

|

|

|

|

|

~a. |

|

|

|

|

|

|

|

||||

City |

State |

Zip Code |

City |

State |

Zip Code |

|

|

|||||

|

|

..Q) |

|

|

|

|

|

|

|

|

|

|

|

|

Q) |

|

|

|

|

|

|

|

|

|

|

1/1 |

|

|

|

|

|

|

|

|

|

|

||

|

ii: |

Nebraska ID or Social Security Number |

|

|

Federal ID or Social Security Number |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

I

(If more than two, see Designation of

I

Name |

|

|

Name |

|

|

|

|

|

|

|

|

Title or Firm Name |

|

|

Title or Firm Name |

|

|

|

|

|

|

|

|

Address (Street or Other Mailing Address) |

|

|

Address (Street or Other Mailing Address) |

|

|

|

|

|

|

|

|

City |

State |

Zip Code |

City |

State |

Zip Code |

|

|

|

|

||

Email Address (See Email in the instructions) |

Phone Number |

Email Address (See Email in the instructions) |

Phone Number |

||

|

|

I |

|

|

I |

The taxpayer appoints the above

Tax Category

Tax Matter of Representation

Tax Period

The

•Fully represent the taxpayer in any hearing, determination, or appeal.

•Enter into any compromise with DOR.

•Execute waivers, including offers of waivers, of restrictions on assessment or collection of tax deficiencies.

•Execute waivers of notice of disallowance of a claim for credit or refund.

•Execute consents extending the statutory period for issuing a notice of deficiency determination.

•Receive, but not endorse or collect, checks in payment of any refund of taxes, penalties, or interest.

•Receive all notices and other written communications with respect to the taxpayer. If more than one

•Perform other acts, specifically:

|

|

|

|

Revocation of Prior Powers of Attorney |

|

|

|

||||

A. □ |

|

I choose to revoke all prior powers of attorney on file with DOR with respect to the same tax matters, and tax periods listed above, |

|||||||||

|

|

except the following: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

B. □ |

|

I choose to revoke all powers of attorney on file with DOR. |

|

|

|

||||||

|

|

If signed by a corporate officer, partner, member, LLC manager, or fiduciary on behalf of the taxpayer, I hereby certify that I have the authority to execute |

|||||||||

sign |

|

this Power of Attorney on behalf of the taxpayer. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

here |

|

|

|

|

|

|

|

|

|||

|

Signature |

|

|

|

|

|

Date |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Print Name |

|

|

|

Email Address |

Title, If Applicable |

|

|||

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|||

|

|

Signature |

|

|

|

|

|

Date |

|

||

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Print Name |

|

|

|

Email Address |

Title, If Applicable |

||||

|

|

|

|

|

|

|

|||||

You may fax this form to

Mail this form to: Nebraska Department of Revenue, PO Box 94818, Lincoln, NE

Supersedes

Instructions

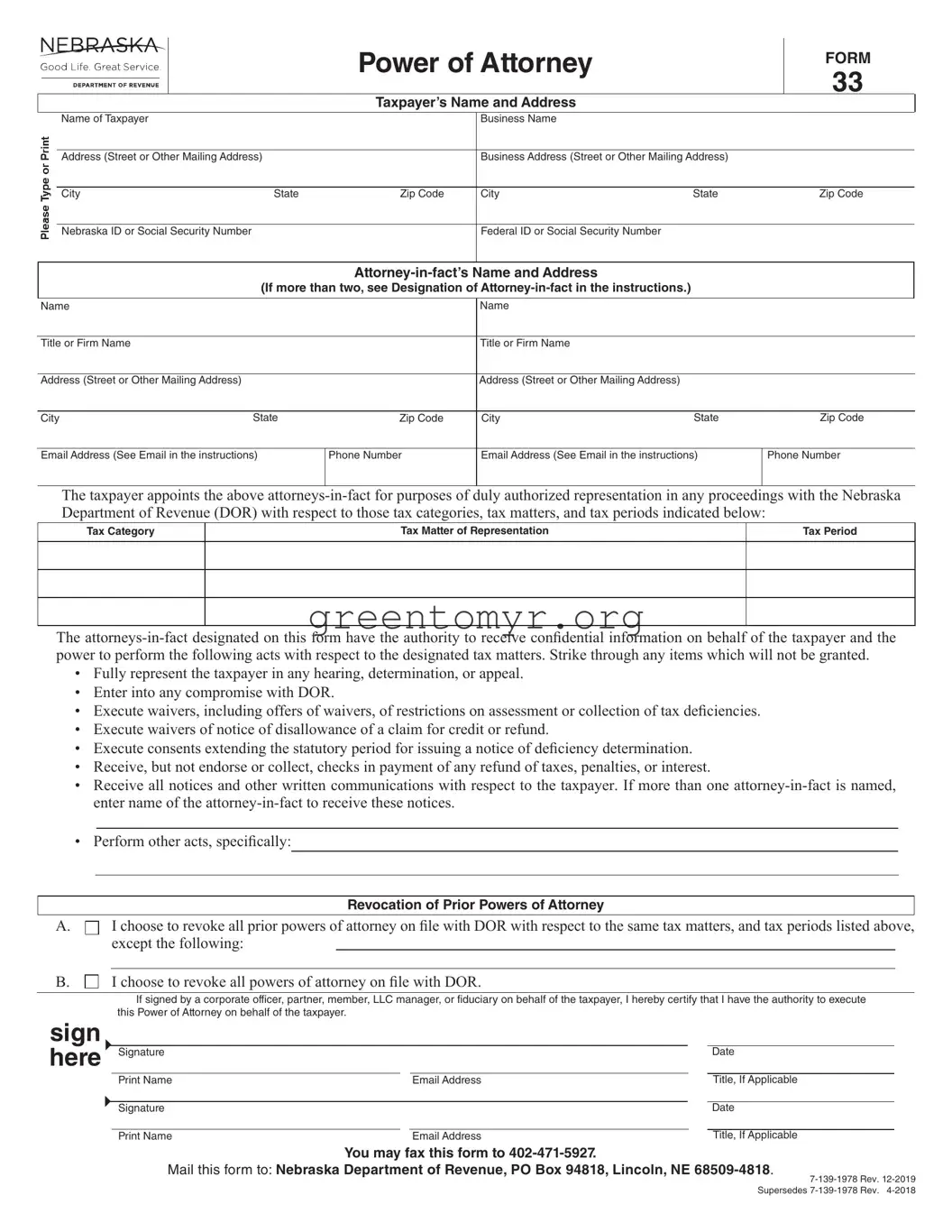

Who Must File. Any taxpayer who wishes to secure representation by another party in matters before the Nebraska Department of Revenue (DOR) with regard to any tax imposed by the tax laws of the State of Nebraska, must fle a Power of Attorney (POA), Form 33, or other appropriate POA. A POA authorizes that party to receive confdential tax information regarding the taxpayer. The Form 33 is provided for the taxpayer’s convenience in designating a POA, but it is not the sole form which may be used. DOR will honor all other properly completed and signed POA authorizations.

When and Where to File. The completed Form 33 may be fled any time. This form, or another properly completed and signed POA, must be fled with DOR before any person designated can represent the taxpayer in matters involving disclosure of confdential tax information.

This form, or other appropriate POA, may be faxed or mailed to DOR:

•Fax to

•Mail to the Nebraska Department of Revenue, PO Box 94818, Lincoln, NE

Taxpayer’s Name and Address. If the taxpayer is an individual, a Social Security number must be listed. If a married, fling jointly return was fled, enter both spouses’ Social Security numbers in the spaces provided.

If the taxpayer is a corporation, partnership, or association, enter the name, state and federal ID numbers (if applicable), and the business address. If the Form 33 will be used in a tax matter in the case of a partnership for which the names, addresses, and Social Security numbers or ID numbers have not already been furnished to DOR, these items should be listed on an attached sheet.

If the taxpayer is an estate or trust, enter the name, title, and address of the fduciary, as well as the name and ID number or Social Security number of the taxpayer. If this space is used to list other information, clearly label the change.

Designation of

Email. By entering an email address, the taxpayer acknowledges that DOR may contact the taxpayer by email. The taxpayer accepts any risk to confdentiality associated with this method of communication. DOR will send all confdential information by secure email or the State of Nebraska’s fle share system. If you do not wish to be contacted by email, write “Opt Out” on the line labeled “email address.”

Tax Category, Tax Matter, and Tax Period. Form 33 is designed to clearly express the scope of the authority granted by the taxpayer to any

“Tax Category” requires a list of the type of tax, such as “income” or “sales and use.” “Tax Matter of Representation” requires a brief summary of the subjects for which the attorney-

Authorized Acts. The Form 33 lists several acts which can be performed by the

If the taxpayer wishes to authorize an act which is not listed, a concise and specifc statement about the additional authorization must be made in the space provided, or a separate signed statement may be attached to the Form 33.

Revocation of Prior Powers of Attorney. To revoke any POAs previously fled with DOR, choose Box A or B.

Box A. Checking this box allows the taxpayer the option of revoking all POAs on fle with DOR with the exception of those listed on the lines provided (or on a list attached to the Form 33). Check box A and list the names, addresses, and zip codes of the

Box B. Checking this box revokes all POAs previously fled with DOR. Check Box B, and sign the form.

If no boxes are checked, all prior POAs will remain in force.

Signature. The taxpayer must sign and date the form. If spouses fle a married, fling jointly income tax return, which both have signed, then both spouses must sign the Form 33. If only one spouse in a married couple signs Form 33, then a separate Form 33 must be signed by the other spouse. If there is only one spousal signature or a second POA is not signed, then only the person designated by the POA would be authorized to perform the acts authorized by the POA. The nonsigning spouse who has fled a joint return with his or her spouse may still obtain information about, and may discuss issues regarding, the couple’s joint return. However, a person may not authorize another party, or themselves, to receive confdential tax information regarding separate returns fled by the person’s spouse.

Only certain people may represent a taxpayer in a contested case once a hearing offcer is appointed: (1) the taxpayer;

(2)a Nebraska attorney; or (3) a

If the taxpayer is a partnership, all partners must sign, unless one is duly authorized to act in the name of the partnership. Nebraska has adopted the Uniform Partnership Act of 1998 (Neb. Rev. Stat. §§

If the taxpayer is a corporation or an association, an offcer having authority to bind the entity must sign. The offcer must indicate his or her offcial title on the line provided.

If the taxpayer is a Nebraska limited liability company (LLC), then the Form 33 must be signed by a member of the LLC. The validity of the authorizations made by a foreign LLC will be determined governed by the laws of the state in which the LLC was organized.

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA form 33 is used to grant an individual or entity the authority to represent a taxpayer before the state tax agency. |

| Governing Laws | This form is governed by the laws of the specific state in which it is filed, including tax code provisions and regulations. |

| Eligibility | Any individual or business entity can act as a representative on behalf of the taxpayer, provided they have the proper authority from the taxpayer. |

| Filing Process | The completed form must be submitted to the state tax agency, either by mail or electronically, depending on the state's guidelines. |

When it comes to managing your tax matters, having the right forms filled out correctly is essential. Completing the Tax POA form 33 is a straightforward process that allows you to designate someone to represent you with the IRS. Take your time filling out the form to ensure accuracy. Here are the steps to guide you through the process.

Once you've submitted the form, the IRS will process your application. Keep a copy of the completed form for your records. This helps ensure you have everything you need in case any questions arise in the future.

The Tax POA Form 33 is a document that allows individuals or organizations to designate an authorized representative to act on their behalf regarding tax matters. This form is commonly used when taxpayers want to grant someone—their accountant, attorney, or tax preparer—the authority to interact with the IRS and other tax authorities.

Any individual or entity that needs assistance with tax issues can use the Tax POA Form 33. This includes individuals filing personal tax returns, businesses handling corporate tax matters, and any organizations managing tax-related concerns.

The Tax POA Form 33 requires various pieces of information, including:

The Tax POA Form 33 can be submitted in a couple of ways. You may mail it to the appropriate address provided by the IRS, or you can submit it electronically through certain tax software programs if they support form submission.

Yes, you can revoke the authority at any time. To do this, you must submit a revocation form to the same authorities you initially submitted the Tax POA Form 33. Ensure that the revocation includes your name, the representative’s name, and any specific details regarding the original form.

After filing the Tax POA Form 33, the IRS will process your request. Once approved, your authorized representative will receive a copy of the form confirming their authorization. Both you and the representative will be notified regarding the status of the submission.

Typically, there are no fees directly associated with submitting the Tax POA Form 33 to the IRS. However, if you are working with a tax professional or attorney, they may charge a fee for their services. It’s important to clarify any potential costs with your representative beforehand.

The authorization granted in the Tax POA Form 33 lasts until you revoke it or until the specified time period expires, whichever comes first. Make sure to review and renew the authorization if you anticipate needing your representative’s assistance beyond the original time frame.

Filling out the Tax Power of Attorney (POA) Form 33 can be a straightforward process, but many individuals make common mistakes that can delay their tax matters. Understanding these pitfalls is essential to ensure that the form is completed accurately and promptly.

One frequent mistake is failing to provide complete taxpayer information. Users often overlook the requirement to include their full name, address, and Social Security number. This information is critical, as it helps the IRS verify your identity. Incomplete details can lead to processing delays or even rejection of the form.

Another common error involves inaccurately designating the authorized representative. It is vital to ensure that the individual you are appointing holds the right qualifications. If your chosen representative does not meet the IRS requirements, your submission may not be processed, leaving you without the assistance you need.

Omitting the specific tax matters that the Power of Attorney covers is another mistake people often make. Be as detailed as possible when describing the types of taxes involved, whether they are income taxes, estate taxes, or others. This clarity ensures that your representative has the authority to act on your behalf in all necessary areas.

Some individuals also fail to sign and date the form properly. A signature without a date could lead to complications or questions about when the authority was granted. Always double-check that both the signature and date fields are complete before submitting the form.

In addition, neglecting to review the form for errors is a common oversight. Simple mistakes in spelling, numbers, or other details can mislead the IRS and cause unnecessary delays in processing your request. Taking a moment to review the form can save you time and prevent frustration.

Another mistake often made involves not keeping a copy of the submitted form. This is crucial for your records and future reference. If any issues arise, having a copy of your submission can help expedite communication with the IRS.

Lastly, not following the proper submission methods can lead to confusion. Ensure you understand whether to mail the form to a specific address or submit it electronically. Misunderstanding these details can result in your POA being lost or not received by the IRS.

The Tax Power of Attorney (POA) form 33 allows individuals to designate someone to act on their behalf in tax matters. When dealing with the IRS or state revenue agencies, several other documents may accompany this form to ensure all necessary information is conveyed. Below is a list of related forms and documents that are commonly used alongside the Tax POA form 33.

Each of these forms serves a unique purpose and can help facilitate the smooth management of your tax affairs when working with your authorized representative. Ensuring you gather the necessary documents will streamline communication with tax authorities and improve your filing experience.

The Tax Power of Attorney (POA) Form 33 allows individuals to authorize someone else to handle their tax matters with the IRS. This document shares similarities with several other legal forms that empower individuals to delegate authority or manage responsibilities. Below are four such documents:

Understanding these documents can help individuals make informed decisions when it comes to delegating authority in various aspects of their lives.

When filling out the Tax Power of Attorney (POA) form 33, there are some important dos and don'ts to keep in mind. Adhering to these guidelines can ensure a smoother process and can prevent potential issues. Here’s a helpful list:

Many people have misunderstandings about the Tax Power of Attorney (POA) Form 33. Clear information can help demystify its purpose and uses. Here are some common misconceptions about this important document:

This form is often thought to be strictly for tax matters. In reality, it can also be used for representing a taxpayer in various transactions related to tax, not limited solely to filing or disputes.

While a verbal agreement may seem convenient, it is not legally binding. The Tax POA Form 33 formalizes the representation and protects both parties involved.

This is not true. Anyone can be appointed to represent you—friends, family members, or professionals, as long as they meet the requirements set out by the IRS.

Many individuals believe that submitting this form is a one-time event. In reality, you can revoke it or file a new one if your situation changes or if you wish to designate a different representative.

Many fear losing control by signing the POA. However, the form allows you to specify the extent of the authority granted, so you maintain a level of control over what actions your representative can take.

This form is often seen as something only needed during an audit process. Actually, it can be useful for many situations, such as negotiating payments or clarifying tax liabilities.

When dealing with the Tax Power of Attorney (POA) Form 33, understanding how to fill it out and use it properly leads to smoother interactions with the IRS. Here are six key takeaways:

Filling out and understanding the Tax POA Form 33 can significantly streamline your tax-related issues. Being informed empowers you and your representative to navigate the tax system more effectively.