The Tax Power of Attorney (POA) Form 3520-BE plays a crucial role in facilitating communication between taxpayers and the Internal Revenue Service (IRS) when it comes to the management of tax obligations. Designed for individuals who wish to appoint a representative to act on their behalf, this form streamlines the process of dealing with tax matters, ensuring that taxpayers can receive guidance and support without needing to navigate the complexities of tax law alone. The form requires detailed information, including the taxpayer's name, identification number, and the representative's details. It grants specific powers, allowing the appointed individual to handle various tasks such as filing returns, accessing information, and negotiating with the IRS. This delegation of authority not only alleviates the burden on taxpayers but also enhances the efficiency of tax administration by ensuring that knowledgeable representatives can advocate for them effectively. Understanding the nuances of this form is essential for anyone looking to manage their taxes proactively and ensure compliance while benefitting from professional oversight.

STATE OF CALIFORNIA

Franchise Tax Board

Business Entity or Group Nonresident |

■ |

|

CALIFORNIA FORM |

|

|

|

|

Power of Attorney Declaration |

|

|

|

|

Use this legal document to authorize a specific individual(s) to receive confidential information and represent you in all matters before the Franchise Tax Board (FTB).

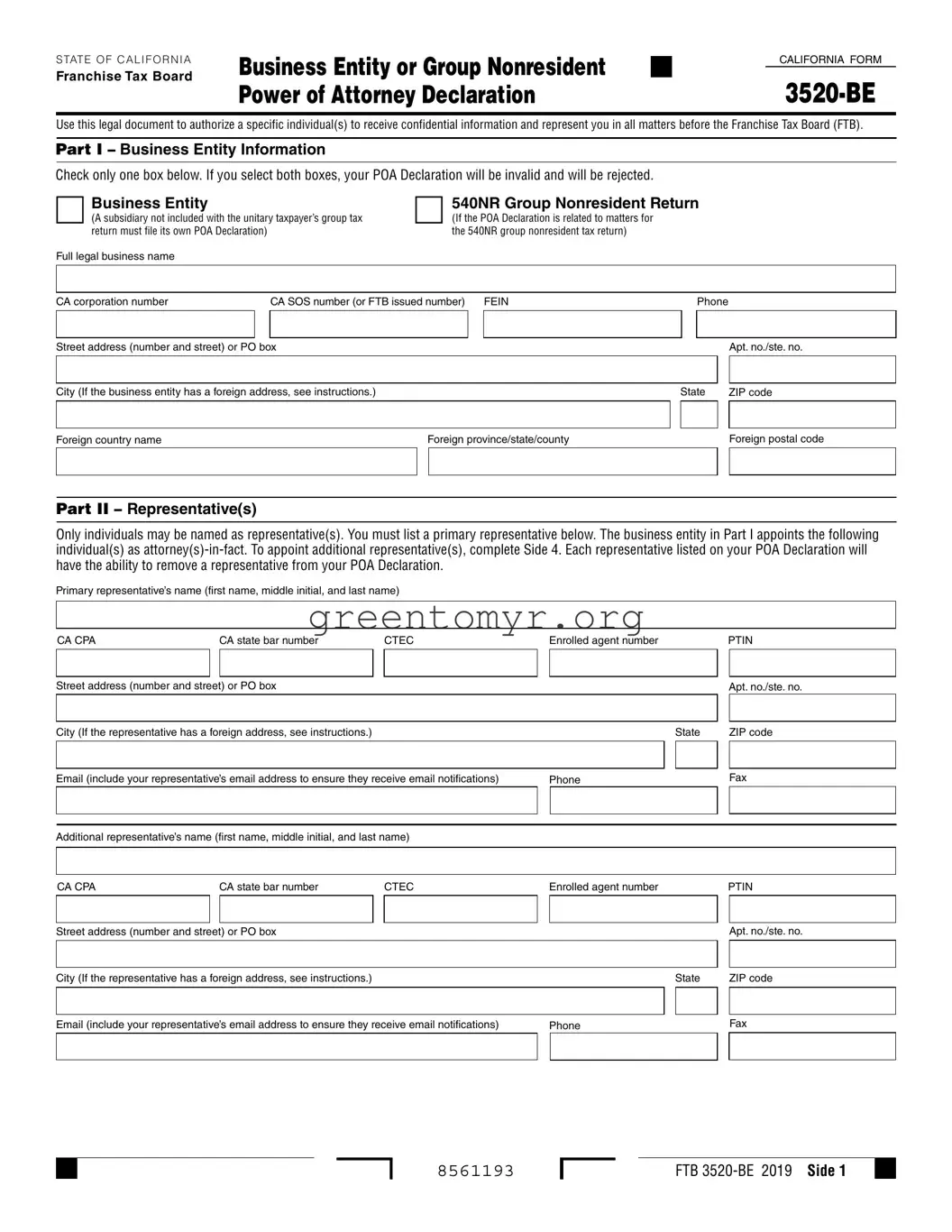

Part I – Business Entity Information

Check only one box below. If you select both boxes, your POA Declaration will be invalid and will be rejected.

Business Entity |

|

|

540NR Group Nonresident Return |

|

|||||||

□ (A subsidiary not included with the unitary taxpayer’s group tax |

□ (If the POA Declaration is related to matters for |

|

|

|

|

|

|||||

return must file its own POA Declaration) |

|

|

the 540NR group nonresident tax return) |

|

|

|

|

|

|||

Full legal business name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

CA corporation number |

CA SOS number (or FTB issued number) FEIN |

|

|

Phone |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street address (number and street) or PO box |

|

|

|

|

|

|

|

|

Apt. no./ste. no. |

||

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

City (If the business entity has a foreign address, see instructions.) |

|

|

|

|

State |

ZIP code |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign country name |

|

Foreign province/state/county |

|

|

|

|

Foreign postal code |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part II – Representative(s)

Only individuals may be named as representative(s). You must list a primary representative below. The business entity in Part I appoints the following individual(s) as

Primary representative’s name (first name, middle initial, and last name)

CA CPA |

CA state bar number |

CTEC |

Enrolled agent number |

|

|

PTIN |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street address (number and street) or PO box |

|

|

|

|

|

|

Apt. no./ste. no. |

|||

|

|

|

|

|

|

|

|

|

|

|

City (If the representative has a foreign address, see instructions.) |

|

|

|

State |

|

ZIP code |

||||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

Email (include your representative’s email address to ensure they receive email notifications) |

Phone |

|

|

|

Fax |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional representative’s name (first name, middle initial, and last name) |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

CA CPA |

CA state bar number |

CTEC |

Enrolled agent number |

|

|

PTIN |

||||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Street address (number and street) or PO box |

|

|

|

|

|

|

Apt. no./ste. no. |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City (If the representative has a foreign address, see instructions.) |

|

|

|

State |

|

ZIP code |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Email (include your representative’s email address to ensure they receive email notifications) |

Phone |

|

|

|

Fax |

|||||

|

|

|

|

|

|

|

|

|

|

|

■

8561193

FTB |

■ |

■

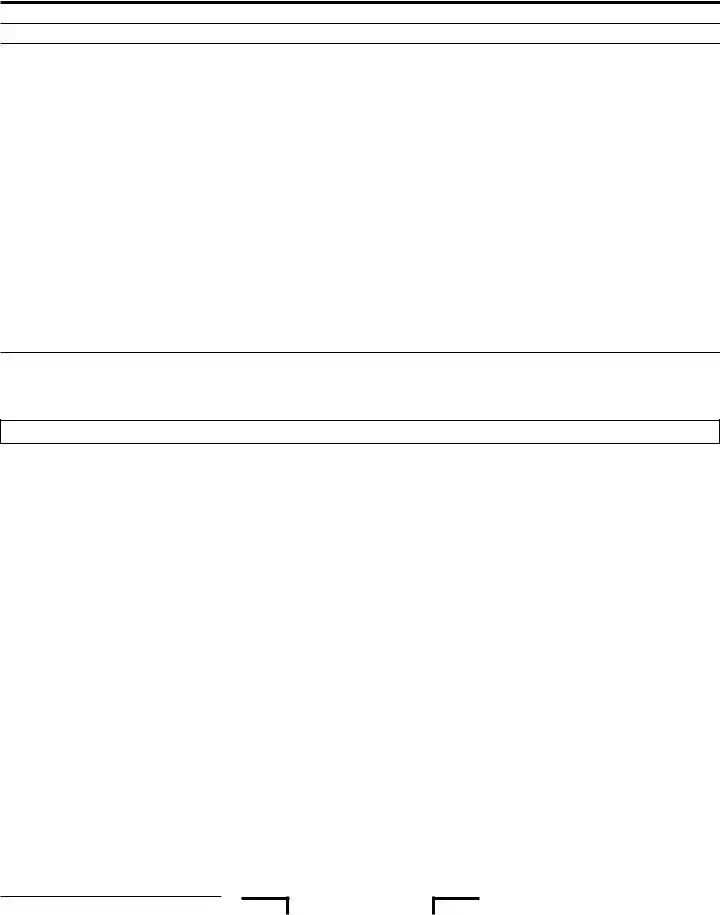

Part III – Authorization for All Years or Specific Income Periods Your POA Declaration Covers

You must check either the “Yes” or “No” box below. Your selection authorizes representatives in Part II and on Side 4 to contact FTB about your account, receive and inspect your confidential information, represent you in all FTB matters, and request information we receive from the Internal Revenue Service (IRS) for either question 1 or 2 indicated below.

If you authorize “all years” and “specific income periods,” the specific income periods privilege prevails. Enter “NA” (not applicable) or strike through any blank year fields in question 2a through 2d. If you do not check either the “Yes” or “No” box or check both the “Yes” and “No” box, we will process the authorization as a “No.” This may cause your POA Declaration to be invalid, and it may be rejected. If you authorized all years, this will include previous, current, and future years up to the expiration date. If you authorized “specific income periods,” you can designate future years or income periods up to fve years from the POA Declaration signature date.

1. |

Authorized All Years |

. . . . . . . . . . . . . . . . . . . . . . . . . . . □Yes |

□No |

|

Or |

. . . . . . . . . . . . . . . . . . . . . . . . . . . □Yes |

□No |

2. |

Authorized Specifc Income Periods* |

||

|

Year Begins: |

Year Ends: |

|

|

(mm/dd/yyyy) |

(mm/dd/yyyy) |

|

|

|

2a. |

|

|

2b. |

* For example, |

|

2c. |

Single Year: |

||

Year Range: |

2d. |

|

Multiple Years: |

–

–

–

–

Part IV – Additional Authorizations

Check either the “Yes” or “No” box below for additional authorizations you would like to grant your representative(s) in addition to those described in Part III. If you do not check either the “Yes” or “No” box or check both the “Yes” and “No” box for any additional authorizations below, we will process the authorization as a “No.” For more information, see instructions.

1. |

Add representative(s) |

□Yes |

□No |

2. |

Receive, but not endorse, refund check(s) |

□Yes |

□No |

3. |

Waive the California statutes of limitations (SOL) |

□Yes |

□No |

4. |

Execute settlement and closing agreements |

□Yes |

□No |

5. |

Other acts (describe on Side 5) |

□Yes |

□No |

Side 2 FTB

J

8562193

7

■

Part V – Request or Retain MyFTB Full Online Account Access for Tax Professional(s)

You must check either the “Yes” or “No” box below. If you check the “Yes” box, you are requesting to authorize or retain full online account access for your tax professional(s), including the ability to view tax returns and take available actions based upon the year(s) designated on this declaration. If you requested full online account access for your tax professional(s) on your POA declaration, a separate notice will be mailed to you with an authorization code and instructions to approve or deny the online account access request. An authorization code will not be sent for tax professional(s) that have existing full online account access.

If you check the “No” box, both the “Yes” and “No” boxes, or do not check any box, we will process the authorization as a “No”, and your tax professional(s) will be granted limited online account access; any existing relationships with full online account access will be changed to limited online account access. Limited online account access includes viewing notices and most correspondence issued by FTB in the last 12 months.

This online account access authorization does not affect their ability to take actions on your behalf or the information your representative can receive by phone, chat, or in person.

If your POA declaration is rejected, this request for online access will not be processed and no updates will be made to online access levels for any existing relationships.

Note: Online access is not available for 540NR Group Nonresident Return accounts.

Authorize MyFTB Full Online Account Access for Tax Professional(s) |

□Yes □No |

Part VI – Signature Authorizing Power of Attorney Declaration

To learn about your privacy rights, how we may use your information, and the consequences for not providing the requested information, go to ftb.ca.gov/forms and search for 1131. To request this notice by mail, call 800.852.5711.

The authority granted to the representative(s) in this POA Declaration will generally expire six years from the date this form is signed, or on the date that a POA declaration is revoked, whichever occurs first.

I declare under penalty of perjury under the laws of the State of California that I am a corporate officer, general partner, authorized managing member, or tax matter partner on behalf of the business entity in Part I, and that I have the authority to sign this form on behalf of the business entity.

I understand that submitting this POA Declaration will not revoke any previously submitted POA Declarations with overlapping privileges.

FTB will reject this POA Declaration if not signed and dated by an authorized individual.

By signing this POA declaration, I understand that FTB will grant limited online account access to my tax professional representative(s) unless full online account access has been requested in Part V. If you do not want your tax professional representative(s) to have any online access, refer to Part V instructions.

Print Name |

|

Title (required for business entities) |

|

|

|

|

|

|

Signature |

|

Date |

x

J

8563193

7

FTB

■

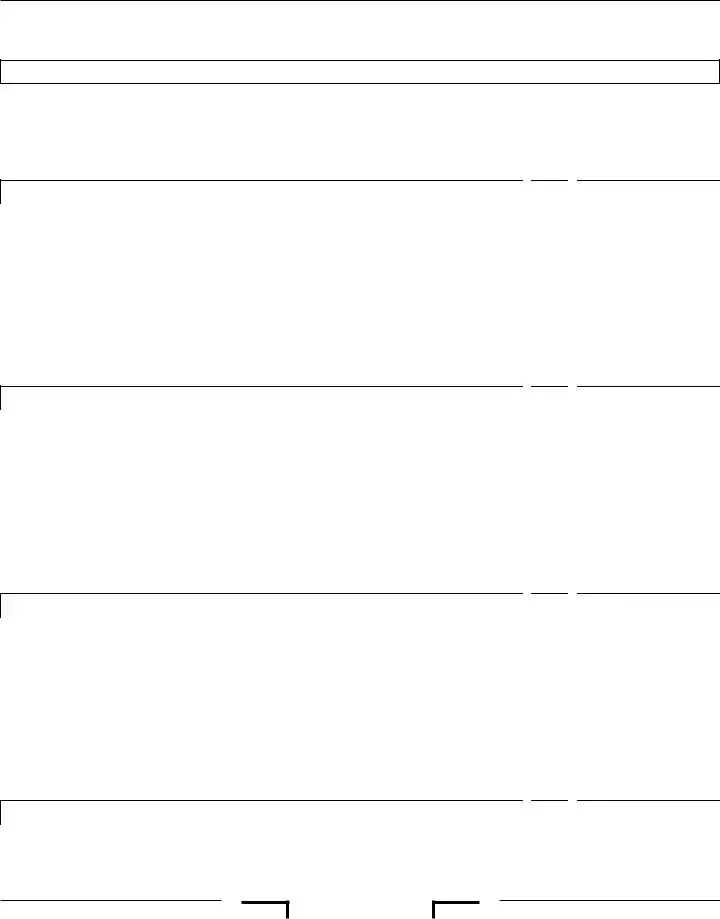

The business entity in Part I appoints the following additional representative(s) as

Additional representative’s name (first name, middle initial, and last name)

CA CPA |

|

CA state bar number |

|

CTEC |

|

Enrolled agent number |

|

PTIN |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street address (number and street) or PO box |

|

|

|

|

|

|

|

|

|

|

Apt. no./ste. no. |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City (If the representative has a foreign address, see instructions.) |

|

|

|

|

|

State |

|

ZIP code |

|

|

||||||

._________________, |

|

|

|

D |

|

|

|

._____ |

____, |

|

||||||

|

|

|

|

|

||||||||||||

Email (include your representative’s email address to ensure they receive email notifications) |

|

Phone |

Fax |

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional representative’s name (first name, middle initial, and last name) |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CA CPA |

|

CA state bar number |

|

CTEC |

|

Enrolled agent number |

|

PTIN |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street address (number and street) or PO box |

|

|

|

|

|

|

|

|

|

|

Apt. no./ste. no. |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City (If the representative has a foreign address, see instructions.) |

|

|

|

|

|

State |

|

ZIP code |

|

|

||||||

._________________, |

|

|

|

D |

|

|

|

._____ |

____, |

|

||||||

|

|

|

|

|

||||||||||||

Email (include your representative’s email address to ensure they receive email notifications) |

|

Phone |

|

|

Fax |

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional representative’s name (first name, middle initial, and last name) |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CA CPA |

|

CA state bar number |

|

CTEC |

|

Enrolled agent number |

PTIN |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street address (number and street) or PO box |

|

|

|

|

|

|

|

|

|

|

Apt. no./ste. no. |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City (If the representative has a foreign address, see instructions.) |

|

|

|

|

|

State |

|

ZIP code |

|

|

||||||

._________________, |

|

|

|

D |

|

|

|

._____ |

____, |

|

||||||

|

|

|

|

|

||||||||||||

Email (include your representative’s email address to ensure they receive email notifications) |

|

Phone |

|

Fax |

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional representative’s name (first name, middle initial, and last name) |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CA CPA |

|

CA state bar number |

|

CTEC |

|

Enrolled agent number |

PTIN |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street address (number and street) or PO box |

|

|

|

|

|

|

|

|

|

|

Apt. no./ste. no. |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City (If the representative has a foreign address, see instructions.) |

|

|

|

|

|

State |

|

ZIP code |

|

|

||||||

._________________, |

|

|

|

D |

|

|

|

._____ |

____, |

|

||||||

|

|

|

|

|

||||||||||||

Email (include your representative’s email address to ensure they receive email notifications) |

|

Phone |

|

Fax |

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

■ Side 4 FTB

8564193

■

■

Other Acts Authorization(s)

Submit this page if you selected Yes to the Other Acts Authorization box from Part IV. If you did not select “Yes,” or selected both “Yes” and “No” within Part IV, we will disregard this page without the listed authorizations being granted. Describe the specific other acts you authorize your representative(s) named in Part II (and on Side 4) to perform before FTB. Authorizations listed in Part III and Part IV prevail over conflicting authorizations listed in this section. Do not return this page if blank.

J

8565193

7

FTB

| Fact Name | Details |

|---|---|

| Form Purpose | The Tax POA form 3520-BE is used for granting authority to an individual to act on your behalf for tax matters. |

| Eligibility | Any taxpayer, including individuals and businesses, can use this form to designate a Power of Attorney. |

| Governing Law | The form is governed under the Internal Revenue Code (IRC) and applicable state laws. |

| Signing Requirement | The form must be signed by the taxpayer granting the Power of Attorney. |

| Duration of Authority | The authority granted to the appointed representative lasts until revoked by the taxpayer. |

| Submission Process | This form can be submitted to the IRS and should be kept on file for your records. |

| State-Specific Forms | Some states may require their own Power of Attorney forms, depending on state laws. |

| Revocation | A taxpayer can revoke the Power of Attorney at any time by submitting a written request to the IRS. |

Once you have your Tax POA form 3520-BE, you're ready to begin the process of filling it out. Understand that this form is important for authorizing someone to act on your behalf regarding tax matters. Take your time, ensure that all information is accurate, and double-check your entries to avoid any potential issues.

The Tax Power of Attorney (POA) form 3520-BE is an official document that allows taxpayers to designate an individual or entity to handle specific tax matters on their behalf. This form grants authority to the appointed representative to receive tax information and correspond with the Internal Revenue Service (IRS) regarding tax issues, ensuring that taxpayers can get professional help when they need it.

This form is ideal for anyone who is unable to manage their tax affairs, whether due to time constraints, lack of knowledge, or other personal circumstances. Common users include:

To successfully fill out form 3520-BE, follow these steps:

No, there is no fee associated with submitting the Tax POA form 3520-BE to the IRS. However, if you work with a tax professional to handle your representation, they may charge a fee for their services.

You can submit form 3520-BE to the IRS in several ways. The most common methods include:

Yes, you can revoke the Power of Attorney at any time by submitting a written notice to the IRS. Ensure you also inform the authorized representative about the revocation to avoid any confusion in the future.

The validity of the form lasts until you revoke it or the appointed representative withdraws from their role. Regularly review your POA arrangement, especially if your tax situation changes or you no longer need representation.

When individuals take the step to appoint someone to handle their tax matters through the Tax Power of Attorney (POA) form 3520-BE, they occasionally encounter pitfalls that can lead to complications. One common mistake is neglecting to provide complete information about both the taxpayer and the designated representative. This information includes names, addresses, and identification numbers. Omitting any of these details can hinder the processing of the POA, delaying the representative's ability to act on behalf of the taxpayer.

Another frequent error occurs when taxpayers sign the form but forget to date it. A signature without a date may lead to questions regarding the validity of the authorization. To prevent confusion, always ensure that the date is clearly written alongside the signature. Similarly, individuals sometimes fail to follow the correct format for their representative's information. For example, not including the appropriate designation, such as "CPA" or "Attorney," can create misunderstandings about the representative's qualifications.

Some people also overlook reviewing the completed form for any typographical errors. Simple mistakes, such as incorrect spelling of names or miswritten identification numbers, can result in significant delays or even rejections. Moreover, another mistake involves indicating the powers granted but not specifying the limitations, if any. It's essential to define the extent of authority clearly, as vague language might lead to misunderstandings regarding the representative's capabilities.

While appointing a representative, taxpayers sometimes neglect to check whether their representative has accepted the role properly. It is crucial for the chosen person to sign the POA form as well; their signature is a confirmation of their willingness to take on this responsibility. Additionally, failing to provide the IRS with the necessary copies or failing to send the form to the right address can complicate matters further.

Another oversight stems from misunderstanding the duration of authority granted. Not specifying whether the POA should remain in effect until revoked or is only temporary can lead to potential complications at tax time. Furthermore, individuals may not utilize the most current version of the form. Using an outdated form can render the submission ineffective, as tax forms are periodically revised.

Lastly, it is essential to remember that the Tax POA form is a legal document. Treating it casually or overlooking its significance can lead to misunderstandings or disputes later. Correctly filling out the form not only facilitates smooth communication between the taxpayer and the IRS but also protects the interests of the individual appointing the representative.

When dealing with the Tax POA form 3520-BE, several additional documents might be necessary to ensure everything is in order. Understanding these forms can help clarify your needs and streamline your tax-related processes.

Being aware of these documents can simplify your interactions with the IRS. Make sure to gather the necessary forms to avoid any hiccups in your tax filings.

When filling out the Tax POA Form 3520-BE, it’s essential to be precise and informed. Here are some essential do's and don'ts to keep in mind:

Using these tips will make the process smoother and help ensure your Tax POA Form 3520-BE is processed without issues.

The Tax POA form 3520-BE is often misunderstood. Below are six common misconceptions about this form along with clarifications.

When dealing with the Tax Power of Attorney (POA) form 3520-BE, there are several important points to keep in mind. Here are some key takeaways:

Filling out the Tax POA form 3520-BE correctly ensures that your designated representative can effectively act on your behalf regarding tax matters.