The Tax Power of Attorney (POA) Form 49357, commonly referred to as POA-1, is a critical document for taxpayers seeking to authorize someone to manage their tax-related issues with state or federal agencies. This form allows individuals to designate an attorney, accountant, or other trusted representatives to handle matters such as filing returns, negotiating with tax authorities, and responding to audits on their behalf. The POA-1 outlines the specific powers granted to the designated representative, ensuring clarity on what they can and cannot do. Key sections of the form require the taxpayer's information, the representative's details, and descriptions of the tax matters involved. Validity is an essential aspect; it is important to ensure that the form is properly signed and submitted to avoid any complications. The POA-1 not only streamlines communication with tax authorities but also provides a safeguard for taxpayers who may not be able to actively manage their tax affairs due to various reasons, such as illness or geographical constraints.

|

|

|

|

POA - 1 |

|

|

|

|

Indiana Department of Revenue |

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

State Form 49357 |

|

|

|

|

POWER OF ATTORNEY |

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

(R7 / |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

1. Taxpayer Information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

Taxpayer(s) Name(s) |

|

|

|

|

|

|

|

|

DBA Name(s) (if applicable) |

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

☐ New Address? |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

City |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

|

Zip Code |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

I |

|

|||

|

Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

2. Identification Numbers |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

Indiana Taxpayer Identification Number (10 digits) |

or |

Employer Identification Number |

|

||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

I |

I |

I |

|

|

I |

I |

I |

I |

I |

|

I |

I |

I |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

Social Security Number |

|

|

|

|

|

Spouse’s Social Security Number |

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

~l |

|

□ |

~I~ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

Hereby appoint(s) the following: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

3. Representative Information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

Individual Representative Name |

|

|

|

|

|

|

|

|

Additional Individual Representative Name |

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

City |

|

|

|

|

|

|

|

|

|

|

State |

|

Zip Code |

City |

|

State |

Zip Code |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

Telephone Number |

|

|

|

Telephone Number |

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

Additional Individual Representative Name |

|

|

Additional Individual Representative Name |

|

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

City |

|

|

|

|

|

|

|

|

|

|

State |

|

Zip Code |

City |

|

State |

Zip Code |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I |

|

Telephone Number |

|

|

|

Telephone Number |

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

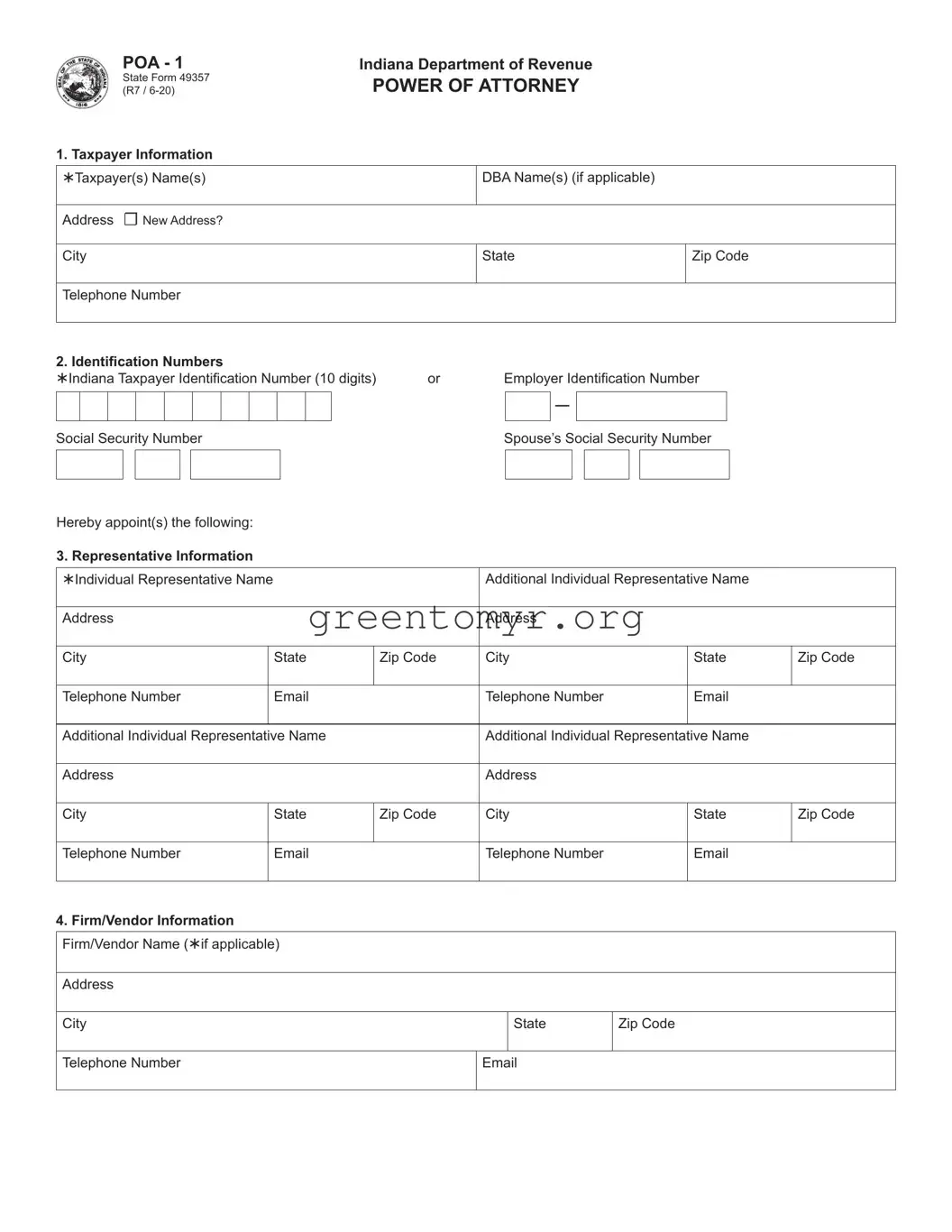

4.Firm/Vendor Information Firm/Vendor Name (if applicable)

Address

City |

|

State |

Zip Code |

|

|

I |

I |

Telephone Number |

|

||

|

I |

|

|

If firm or vendor, list representative(s) name, telephone number and email.

Representative(s) Name

Telephone Number

5. General Authorization

☐I authorize the listed representative(s), in addition to anything otherwise authorized on this form, to represent me regarding any matters with the Indiana Department of Revenue regardless of tax years or income periods. I understand that this authority will expire 5 years from the date this POA is signed or a written and signed notice is filed revoking this authorization.

6.Tax Type(s) (Not applicable if box is checked in question 5 above)

Type of Tax |

Year(s)/Period(s) |

(Income, Withholding, Sales, etc.) |

☐ Current Year ☐ Specify |

_______________________________________ |

___________________________________ |

_______________________________________ |

___________________________________ |

_______________________________________ |

___________________________________ |

I acknowledge that the designated representative has the authority to receive confidential information and full power to perform on behalf of the taxpayer in tax matters related to this Power of Attorney. This authority does not include the power to receive refund checks.

I acknowledge that actions taken by the designated representative are binding, even if the representative is not an attorney. Proceedings cannot later be declared legally defective because the representative was not an attorney.

If I am a corporate officer, partner, or fiduciary acting on behalf of the taxpayer, I certify that I have authority to execute this Power of Attorney on behalf of the taxpayer.

7. Authorizing Signature |

|

Signature _______________________________________________ |

Date _______________________________ |

Printed Name ____________________________________________ |

Title _______________________________ |

Telephone Number ________________________________________ |

Email ______________________________ |

Required fields - if not complete, this form will be returned to sender.

Instructions for Indiana Form

Casual conversations with a taxpayer’s representative who does not have a Power of Attorney on file are permitted. However, the Indi- ana Department of Revenue will not disclose tax return information or

Pursuant to 45 IAC

1.The taxpayer’s name, DBA name (if applicable), address (Please check the box if this is a new address), and telephone number.

2.The Indiana taxpayer’s identification

3.The name, address, and telephone number of your individual representative(s). Only individuals can be named as representatives. If you want to add one individual representative, enter one in the spaces provided. If you want to add more representatives, enter them in the spaces provided.

4.If your representative works for a consulting firm or vendor, enter the company’s name, address, telephone number, and email address. Enter the individual representative name(s) employed by the firm or vendor you have designated. If you want to add more than four individual representatives for a firm or vendor, you can provide the names of those representatives in a separate list, to be attached to this Power of Attorney form.

If you wish for your firm to be represented generally by a company such as a payroll processor, enter the company’s name,

address, telephone number, and email address. If the company is not listed, you must provide the names of one or more individual |

|

representatives. |

|

|

|

5.Check this box if you want to authorize your representative to represent you regarding all tax matters, regardless of the tax year or income period involved.

6.The Power of Attorney form can contain the specific type of tax, or the option ALL. By choosing the option ALL, you will be allowed access to ALL tax types appropriate to the taxpayer. The tax years must be specific.

7.The taxpayer’s signature or the signature of an individual authorized to execute the Power of Attorney on the taxpayer’s behalf.

NOTE: Include as an enclosure any restrictions or limitations the taxpayer has placed on the representative while acting as the tax- payer’s representative.

After the taxpayer executes a Power of Attorney, the department will communicate primarily with the taxpayer’s representative.

The department accepts faxed copies of original Power of Attorney forms. If a copy is provided, the person forwarding the copy certifies, under penalties for perjury, that the copy is a true, accurate, and complete copy of the original document.

Do not send

The department will not accept a Power of Attorney form that has been altered unless it has the initials of the taxpayer (or an individual authorized to execute the Power of Attorney on the taxpayer’s behalf) beside the alteration(s).

This Power of Attorney is effective for 5 years from the date the form is signed. After the expiration of 5 years, a new Power of Attorney form must be completed if the taxpayer wishes to permit the department to communicate with the taxpayer’s representative.

This Power of Attorney can be revoked prior to expiration only by written and signed notice. A subsequent Power of Attorney alone will NOT revoke a prior Power of Attorney.

Required fields – if not complete, this form will be returned to sender.

Submit the form using these methods:

•Fax: (317)

•Mail: Indiana Department of Revenue PO Box 7230

Indianapolis, IN

| Fact Name | Fact Description |

|---|---|

| Form Purpose | The Tax POA form 49357, also known as POA-1, is designed to authorize an individual to represent a taxpayer in matters related to their taxes. |

| Governing Law | This form operates under the laws governing powers of attorney in the respective state, consistent with state tax authorities’ regulations. |

| Who Can Use It | Individuals, businesses, or organizations looking to appoint someone to manage their tax affairs may complete this form. |

| Signature Requirement | The form must be signed by the taxpayer to be valid, indicating consent for representation. |

| Representation Scope | The authorized representative can handle various tax-related matters, such as filing returns and communicating with tax authorities. |

| Duration of Authority | The authority granted by this form remains effective until the taxpayer revokes it or the tax authorities cancel it. |

| Filing Process | Once completed, the form should be submitted to the relevant tax authority, often alongside other tax documents as necessary. |

| Revocation Form | A separate form or written communication is needed to revoke the power of attorney once it is no longer desired. |

After completing the Tax POA form 49357 (POA-1), please review the information for accuracy. You will then submit the form to allow your designated representative to handle matters on your behalf regarding tax issues.

The Tax POA form 49357, also known as the Power of Attorney (POA-1) form, allows an individual to designate another person to represent them before the IRS. This person could be a tax professional, family member, or friend. By completing this form, you give them the authority to discuss your tax matters, respond to IRS correspondence, and negotiate on your behalf. It is an essential tool for anyone who needs assistance managing their tax affairs, ensuring your representative has the appropriate permissions to act on your behalf.

You can choose anyone to be your representative, provided they are willing to assist you. However, the most common choices include:

It's important to ensure that the person you choose is knowledgeable about tax matters and understands your specific needs. Remember, this individual will have access to your sensitive financial information, so trust is crucial.

Completing the Tax POA form 49357 is a straightforward process. Follow these steps:

Once completed, submit the form to the IRS to authorize your representative officially. Keep a copy for your records.

Generally, the POA-1 form remains in effect until you revoke it or your representative withdraws. You may choose to revoke it if you change representatives or decide you no longer need someone to act on your behalf. All you need to do is submit a written notice to the IRS indicating that you are revoking the previously submitted POA-1 form.

In addition, you can always fill out a new form to appoint another representative. This flexibility allows you to manage your tax representation based on your evolving needs.

Filling out the Tax POA form 49357 (POA-1) can be a straightforward task, yet many individuals make common mistakes that can lead to complications. One frequent error occurs when the designated representative's information is incorrectly entered. This can include misspelled names or incorrect addresses, which may result in delays or miscommunication.

Another mistake involves failing to provide a specific authorization. The form requires that taxpayers clearly indicate the types of tax matters the representative will handle. Without this detailed specification, the IRS may not recognize the authority granted, leading to frustration for both the taxpayer and their representative.

Many applicants overlook the necessity of signing the form. Without a signature from the taxpayer, the form is considered incomplete. While it may seem simple, this omission can cause significant delays in gaining representation before the IRS.

Additionally, not dating the form is a common oversight. The date is essential for the validity of the Power of Attorney authorization. Forms submitted without a date may be returned, delaying the process further.

Some individuals also fail to include multiple representatives when needed. If a taxpayer wishes to authorize more than one person, it is crucial to list each representative's information on the form. Neglecting this step can leave a taxpayer without adequate support during their dealings with the IRS.

Taxpayers sometimes submit your form to the wrong IRS address. Each region might have a designated location for processing the POA forms. Sending it to the wrong address can significantly slow down authorization.

Another common issue arises when individuals do not keep a copy of the submitted form. It's important for taxpayers to retain a record for their own reference. This can be critical if questions or issues arise in the future regarding the status of representation.

Using outdated versions of the form is also a frequent error. Taxpayers should ensure they are using the most current version available. Using an older version can lead to rejection by the IRS, forcing taxpayers to redo the process.

Some taxpayers fail to check for any additional requirements that may apply in their state. Occasionally, local laws or regulations may impose extra obligations that must be met for the form to be valid.

Finally, many people rush through the completion of the Tax POA form. Taking the time to review each entry for accuracy and completeness can save significant hassle later. Careful attention to detail is crucial for ensuring that the form is correctly processed.

The Tax Power of Attorney (POA) form 49357 (POA-1) is an essential document that allows an individual to appoint someone else to represent them before the Internal Revenue Service (IRS). When engaging with tax matters, several other forms and documents may also be required or helpful. Below is a list of such documents commonly used in conjunction with the Tax POA form.

Each of these documents serves a unique purpose in the tax process, complementing the Tax POA form 49357. It is advisable to understand the specific use cases of each form to ensure that tax representation and reporting obligations are fulfilled accurately.

The Tax Power of Attorney form 49357 (POA-1) has several similarities with other legal documents that grant someone the authority to act on behalf of another person. Below are six documents that share characteristics with the Tax POA form:

Here are some important guidelines to follow when filling out the Tax POA form 49357 (POA-1):

There are also things to avoid during this process:

Here are ten common misconceptions about the Tax POA form 49357 (POA-1) that people often have:

Understanding these misconceptions can help you navigate the process more effectively. It’s always a good idea to consult with a professional if you have questions about your specific situation.

Filling out and utilizing the Tax POA form 49357 (POA-1) requires attention to detail. Here are some key takeaways to consider: