The Tax Power of Attorney (POA) Form A-222 serves as a crucial document for individuals seeking to authorize another person to act on their behalf in matters related to tax filings and communications with the Internal Revenue Service (IRS) or state tax authorities. This form designates a trusted representative to manage tax-related responsibilities, which may include filing returns, negotiating tax debts, and handling audits. Utilizing the A-222 form can streamline complex tax issues, providing taxpayers with peace of mind that their interests are being represented effectively. Additionally, it is essential that the form is filled out accurately to avoid delays or complications. When completing this form, individuals must provide pertinent information about both themselves and their appointed tax representative. Understanding the implications of granting power of attorney is vital, as this designation grants significant authority over personal tax matters. As such, choosing a representative wisely becomes an integral part of the process. The A-222 form ultimately serves as a practical tool for taxpayers, simplifying interactions with tax authorities while ensuring representation is in place for optimal management of their tax obligations.

Wisconsin Department

of Revenue

Power of Attorney

(Please print or type)

Form

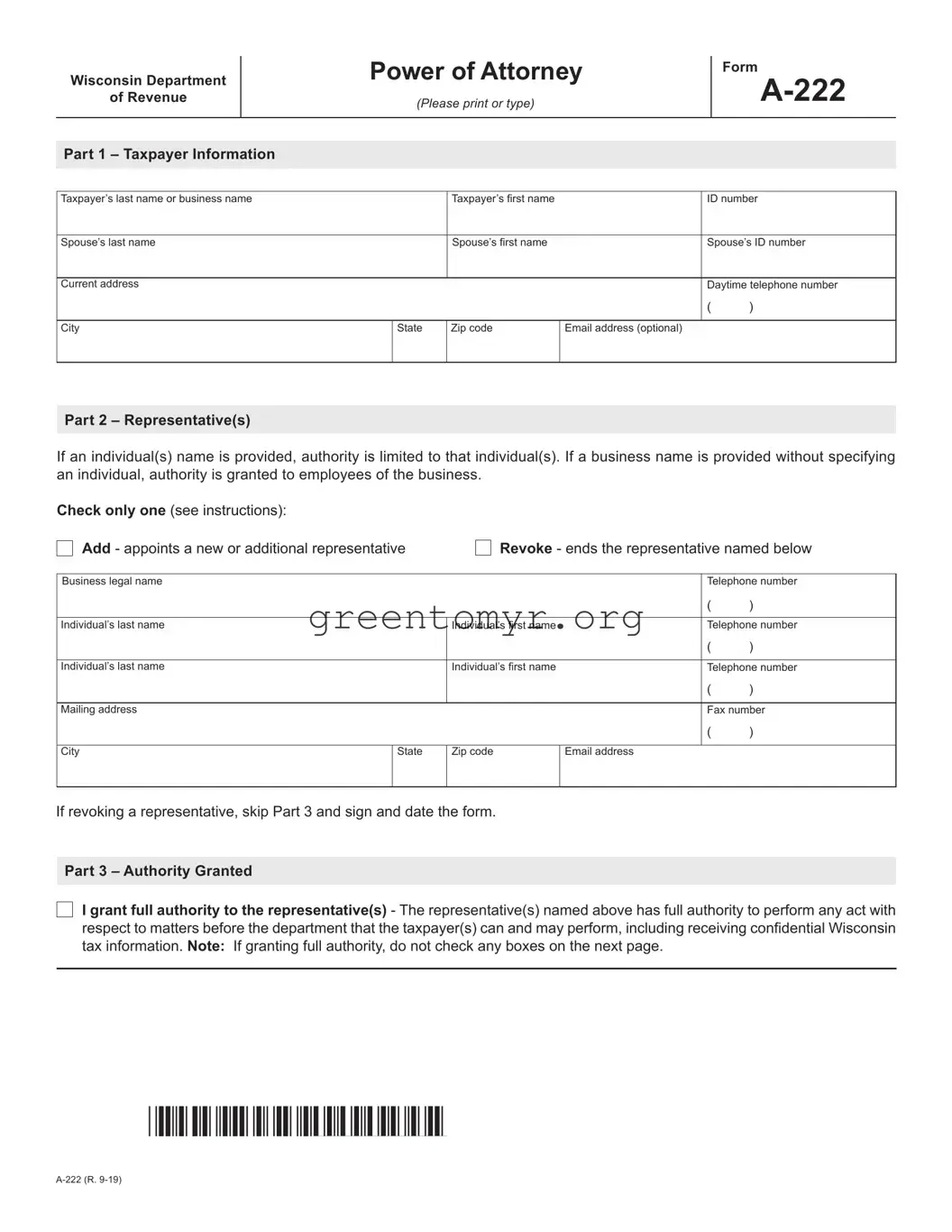

Part 1 – Taxpayer Information

Taxpayer’s last name or business name |

|

Taxpayer’s first name |

|

ID number |

||

|

|

|

|

|

|

|

Spouse’s last name |

|

Spouse’s first name |

|

Spouse’s ID number |

||

|

|

|

|

|

|

|

Current address |

|

|

|

Daytime telephone number |

||

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

City |

|

State |

Zip code |

Email address (optional) |

|

|

|

I |

|

|

I |

|

|

Part 2 – Representative(s)

If an individual(s) name is provided, authority is limited to that individual(s). If a business name is provided without specifying an individual, authority is granted to employees of the business.

Check only one (see instructions): |

|

|

|

|

|

□ Add - appoints a new or additional representative |

□ Revoke - ends the representative named below |

||||

Business legal name |

|

|

|

Telephone number |

|

|

|

|

|

( |

) |

|

|

|

|

|

|

Individual’s last name |

|

Individual’s first name |

|

Telephone number |

|

|

|

|

|

( |

) |

|

|

|

|

|

|

Individual’s last name |

|

Individual’s first name |

|

Telephone number |

|

|

|

|

|

( |

) |

|

|

|

|

|

|

Mailing address |

|

|

|

Fax number |

|

|

|

|

|

( |

) |

|

|

|

|

|

|

City |

State |

Zip code |

Email address |

|

|

|

I |

|

I |

|

|

If revoking a representative, skip Part 3 and sign and date the form.

Part 3 – Authority Granted

□

I grant full authority to the representative(s) - The representative(s) named above has full authority to perform any act with respect to matters before the department that the taxpayer(s) can and may perform, including receiving confidential Wisconsin tax information. Note: If granting full authority, do not check any boxes on the next page.

I grant full authority to the representative(s) - The representative(s) named above has full authority to perform any act with respect to matters before the department that the taxpayer(s) can and may perform, including receiving confidential Wisconsin tax information. Note: If granting full authority, do not check any boxes on the next page.

Illlllll llll 111111111111111 111111111111111 IIIII IIII IIII

Form

Taxpayer Name

Page 2 of 2

ID Number

Part 3 – Authority Granted (continued)

□

I grant limited authority to the representative(s) - (check only items below for which you are granting authority.) The representative(s) named above has authority to perform any act, with respect to the items checked below, that the taxpayer(s) can and may perform, including the authority to receive confidential Wisconsin tax information.

I grant limited authority to the representative(s) - (check only items below for which you are granting authority.) The representative(s) named above has authority to perform any act, with respect to the items checked below, that the taxpayer(s) can and may perform, including the authority to receive confidential Wisconsin tax information.

Limited Authority |

Period(s) (optional) |

Limited Authority |

Period(s) (optional) |

□

Income or Franchise Taxes □

Income or Franchise Taxes □

Sales and Use Taxes

Sales and Use Taxes

□

Excise Taxes

Excise Taxes

□

Property Taxes

Property Taxes

□

Employer Withholding Taxes

Employer Withholding Taxes

□

□

Nontax Debt

Nontax Debt

□

Other (describe below)

Other (describe below)

Part 4 – Signature of Taxpayer(s)

I understand that the execution of this Power of Attorney does not relieve me of personal responsibility for correctly and timely reporting and paying taxes, or from the penalties, fees, or interest for failure to do so, all as provided for under Wisconsin tax law. I understand a photocopy, faxed copy, and/or electronic copy of this form has the same authority as the signed original.

If signed by a corporate officer, general partner, managing member, or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this Power of Attorney on behalf of the taxpayer.

Signature |

Title |

Date |

Signature |

Title |

Date |

Note: All notices that are automatically generated by the department’s computer system will be sent only to the taxpayer. If the representative needs copies of these notices, the representative must request a copy each time a notice is issued if it cannot be accessed in My Tax Account as an approved third party.

Illlllll llll 111111111111111 111111111111111 IIIII IIII IIII

Made fillable by FormsPal.

| Fact Name | Detail |

|---|---|

| Purpose | The Tax POA form A-222 is used to authorize someone to represent you before the state tax agency. |

| Governing Law | This form is governed by state tax regulations applicable in your jurisdiction. |

| Eligibility | Any individual or entity can appoint an authorized representative using this form. |

| Signature Requirement | The taxpayer must sign the form to validate the authorization. |

| Expiration | Authorization remains in effect until revoked or until the particular tax matter is resolved. |

| Submission Method | The completed form can typically be submitted online or via mail, depending on state guidelines. |

| Information Needed | Taxpayer's name, address, and identification number must be provided on the form. |

| Limits of Authority | The representative can discuss tax matters but cannot make payments unless explicitly allowed. |

| Renewal Process | There is no automatic renewal; a new form must be filed for continued representation. |

Once you have the Tax POA form A-222 ready, it’s time to fill it out with the necessary information. Make sure to provide accurate details to ensure a smooth process. Follow these steps carefully to complete the form correctly.

After filling out the form, you’ll need to submit it to the relevant tax authority. Keep track of any deadlines and requirements for submission to prevent any delays in processing your request.

The Tax POA Form A-222 is a Power of Attorney form that allows taxpayers to authorize someone else to represent them before the IRS regarding their tax matters. This form is crucial for individuals who want to appoint someone to handle their tax-related issues, ensuring that their representative can communicate with the IRS on their behalf.

Any individual, including a tax professional such as a CPA or an attorney, can be appointed as a representative by using the Form A-222. However, it's important to select someone you trust to manage your tax affairs since they will have the authority to receive information and act on your behalf.

Form A-222 covers various tax matters, including but not limited to:

Essentially, any tax-related communication with the IRS can be conducted by your appointed representative once the form is filed.

Filling out the Form A-222 involves several straightforward steps:

Ensure that the details are accurate to avoid any issues with the submission.

After completing the Form A-222, you need to submit it to the appropriate IRS office. The specific address may depend on your location and the nature of your tax situation. Check the IRS website for guidance on where to send your form, or consult your representative for clarity.

No, there is no fee to file the Form A-222. However, if you choose to hire a professional to assist you with the form, they may charge for their services. Always clarify fees in advance when working with a tax professional.

Once submitted, the IRS processes the form, typically taking several weeks. After processing, your representative will be able to access your tax information and communicate with the IRS on your behalf. You should receive a confirmation from the IRS when the form is accepted.

Yes, you can revoke your Power of Attorney at any time. To do this, complete a new Form A-222 and select the option to cancel the previous authorization. Additionally, inform your representative of your decision to revoke the authority. This will help avoid any confusion moving forward.

The validity of Form A-222 can extend until you revoke it or until the matter is resolved. If you have a specific duration in mind or particular actions that you want your representative to handle, be sure to specify those in the form when you submit it.

When individuals or businesses consider designating someone to handle their tax matters, they often turn to the Tax Power of Attorney (POA) Form A-222. While this form is quite straightforward, several common mistakes can lead to complications and delays. Understanding these errors is crucial for ensuring a smooth process.

One prevalent mistake occurs when individuals fail to complete all required fields. Omitting essential information, such as the taxpayer's Social Security number or the representative's details, can stall the processing of the form. Authorities may require additional steps to obtain missing information, extending the time it takes to grant the POA. Always double-check that every section is filled correctly and thoroughly.

Another significant error involves signing the form in the wrong section or forgetting to sign it altogether. This seemingly simple oversight can invalidate the entire request. It's important for taxpayers to carefully review the signature requirements and ensure that they are in compliance. Proper signatures by all required parties confirm the intent and maintain the validity of their authorization.

Additionally, individuals sometimes choose an unqualified representative. It’s essential that the appointed person has the authority to act on the taxpayer's behalf. Failure to appoint someone who is authorized, such as a licensed tax professional or attorney, can lead to significant issues. The IRS needs to be confident that the representative can adequately navigate the complexities of tax matters.

Finally, some individuals neglect to keep a copy of the submitted form. Documenting the submission is vital for future reference and for confirming that the IRS has received the request. In instances where disputes arise or further clarification is needed, having a record can simplify communication and resolution. Maintaining diligent documentation helps ensure that individuals can effectively manage their tax responsibilities.

The Tax Power of Attorney (POA) Form A-222 is a crucial document allowing individuals to designate a representative to handle their tax matters. It is often accompanied by several other forms and documents that serve various purposes in the tax process. Below is a list of related forms that individuals may also need to complete.

Understanding these forms is essential for managing tax responsibilities effectively. Each document plays a specific role in ensuring compliance and facilitating communication with the IRS and other financial entities.

Filling out the Tax Power of Attorney (POA) Form A-222 requires careful attention to detail. Here are some important do's and don'ts to ensure a smooth process:

Approaching the Tax POA Form A-222 with diligence can help facilitate your tax-related needs effectively. Prompt and precise actions lead to smoother interactions with the tax authorities.

When dealing with tax matters, the Power of Attorney (POA) form A-222 can often be misunderstood. Clearing up these misconceptions can help individuals and businesses navigate tax representation more effectively.

This form is not limited to individuals. Businesses and organizations can also appoint someone to act on their behalf regarding tax matters.

Filing the A-222 does not mean giving up control. The principal still retains the right to handle their tax matters, and the representative acts only as authorized.

The A-222 form is not exclusively for audits. It can be beneficial in various situations, such as resolving issues with tax returns or communicating with the IRS.

The authority granted through the A-222 can be revoked at any time. A new form can be submitted to designate another representative or to cancel the existing authorization.

The A-222 may apply to both federal and state tax matters. Individuals should ensure they understand the jurisdictional implications of the Power of Attorney.

Filling out the Tax POA (Power of Attorney) Form A-222 is an important step for anyone needing to allow someone else to handle their tax matters. Here are some key takeaways to keep in mind:

Being proactive is crucial when it comes to tax matters. Understanding the nuances of the Tax POA Form A-222 will help ensure a smoother process for you and your designated agent.