The Tax Power of Attorney (POA) form BT-129 serves as a vital tool for individuals and businesses seeking to authorize another person to handle their tax matters on their behalf. This form simplifies communication with tax authorities, allowing the appointed representative to receive confidential tax information, sign tax returns, and engage in discussions related to specific tax issues. It is essential to note that the BT-129 can be tailored to grant varying degrees of authority, depending on the individual’s needs. One of the major advantages of utilizing this form is the streamlining of tax processes, enabling efficient resolution of tax concerns. Furthermore, submitting the BT-129 ensures that taxpayers maintain control over who represents them, thereby protecting their rights while navigating complex tax regulations. The clarity afforded by this legal document can lead to improved interaction with the IRS or state tax agencies, resulting in timely resolutions and fewer misunderstandings.

Form |

OKLAHOMA TAX COMMISSION • 2501 NORTH LINCOLN BOULEVARD |

Revised |

OKLAHOMA CITY, OKLAHOMA 73194 |

|

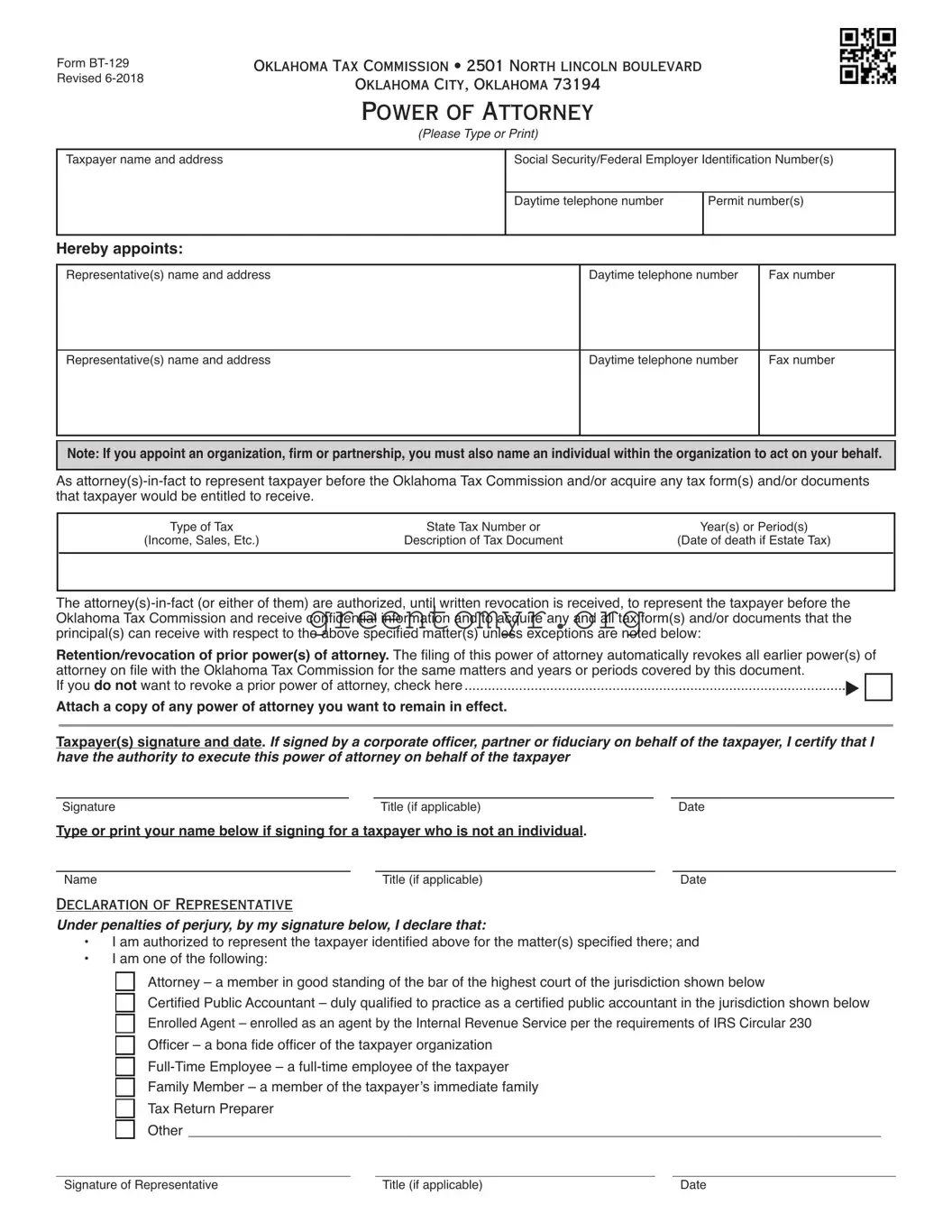

POWER OF ATTORNEY

(Please Type or Print)

Taxpayer name and address |

Social Security/Federal Employer Identification Number(s) |

|

|

|

|

|

Daytime telephone number |

Permit number(s) |

|

|

|

Hereby appoints:

Representative(s) name and address |

Daytime telephone number |

Fax number |

|

|

|

Representative(s) name and address |

Daytime telephone number |

Fax number |

|

|

|

Note: If you appoint an organization, firm or partnership, you must also name an individual within the organization to act on your behalf.

As

Type of Tax |

State Tax Number or |

Year(s) or Period(s) |

(Income, Sales, Etc.) |

Description of Tax Document |

(Date of death if Estate Tax) |

|

|

|

The

Retention/revocation of prior power(s) of attorney. The filing of this power of attorney automatically revokes all earlier power(s) of |

|||

attorney on file with the Oklahoma Tax Commission for the same matters and years or periods covered by this document. |

|

|

|

▼ |

□ |

|

|

If you do not want to revoke a prior power of attorney, check here |

|

||

Attach a copy of any power of attorney you want to remain in effect. |

|

|

|

|

|

||

Taxpayer(s) signature and date. If signed by a corporate officer, partner or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power of attorney on behalf of the taxpayer

Signature |

Title (if applicable) |

Date |

Type or print your name below if signing for a taxpayer who is not an individual.

Name |

Title (if applicable) |

Date |

DECLARATION OF REPRESENTATIVE

Under penalties of perjury, by my signature below, I declare that:

•I am authorized to represent the taxpayer identified above for the matter(s) specified there; and

•I am one of the following:

□

□

□

□

□

□

□

□

Attorney – a member in good standing of the bar of the highest court of the jurisdiction shown below

Certified Public Accountant – duly qualified to practice as a certified public accountant in the jurisdiction shown below

Enrolled Agent – enrolled as an agent by the Internal Revenue Service per the requirements of IRS Circular 230

Officer – a bona fide officer of the taxpayer organization

Family Member – a member of the taxpayer’s immediate family

Tax Return Preparer

Other _________________________________________________________________________________________

Signature of Representative |

Title (if applicable) |

Date |

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA Form BT-129 allows individuals to designate a representative to handle tax-related matters on their behalf. |

| Governing Law | This form is governed by the tax laws of the respective state where it is filed, ensuring compliance with local regulations. |

| Eligibility | Any individual or entity can be appointed as a representative, provided they meet the state's qualifications for representation. |

| Submission | The completed BT-129 form must be submitted to the state's tax authority to be effective and grant the designated representative tax authority. |

Filling out the Tax POA form BT-129 is a straightforward process. Once you've completed this form, you can submit it to authorize someone to represent you in tax matters. This step ensures that the person you designate has the legal authority to act on your behalf regarding tax issues.

Once you’ve carefully filled out the form, it’s important to keep a copy for your records. You can then submit the completed form to the relevant tax authority, ensuring that your representative can act on your behalf without delay.

The Tax Power of Attorney (POA) Form BT-129 is a legal document that allows one individual, referred to as the "principal," to designate another person, known as the "agent," to represent them in tax matters before the state tax authority. This form is essential for individuals who may not have the time, expertise, or ability to handle their tax affairs personally.

The agent can be anyone trustworthy and qualified, including family members, friends, or tax professionals such as accountants and lawyers. However, it’s best to choose someone familiar with tax issues to ensure effective representation.

The agent has the power to perform various actions on behalf of the principal, including:

This flexibility allows the agent to manage complex tax situations effectively.

Filling out the BT-129 form involves a few steps. First, download the form from the relevant tax authority’s website. Then complete the following sections:

Make sure to check the form for clarity and accuracy before submission.

No, a notary is not required to validate the BT-129 form. However, it’s important to ensure that all signatures are completed correctly to avoid any delays in processing.

You should submit the completed form to the appropriate tax authority. The specific submission process may vary based on your location. Typically, it can be mailed or sometimes submitted electronically through a secure portal provided by the tax authority.

The authority granted by the BT-129 form remains in effect until you revoke it. It’s advisable to review your needs periodically. If you no longer require the agent's services or if your circumstances change, you can revoke the POA by submitting a revocation form to the tax authority.

Yes, you can revoke the authority at any time. To do this, you should submit a formal revocation of power of attorney to the tax authority. It’s important to communicate this change to your agent as well, so they are aware that their authority has ended.

If the agent is not performing their duties appropriately, the principal can revoke the POA. It is essential to monitor the activities of the agent, especially if your tax situation is complex or time-sensitive. Open communication with your agent can often help address issues before they escalate.

The BT-129 form can be used to authorize an agent for specific tax years, but it only covers the periods indicated on the form. If you need representation for different years, you should specify this in your authorization or submit separate forms as needed.

Completing the Tax Power of Attorney (POA) form BT-129 can feel overwhelming, and many individuals make common mistakes that can lead to issues down the line. One frequent error involves failing to provide the correct taxpayer identification number. This number is essential as it links the form to the right individual or entity. Without it, the tax authorities may reject the form, causing delays and confusion.

Another mistake often seen is incomplete signatures. Taxpayers must ensure that all required signatures are present. In many cases, individuals overlook the need for both their signature and the signature of the designated representative. This omission can render the document invalid, complicating matters when it comes time to handle tax issues.

Many individuals also neglect to specify the scope of the authority granted to their representative. This aspect of the BT-129 form is critical. If the authority is not clearly defined, the representative may face limitations that hinder their ability to act effectively on behalf of the taxpayer. Be precise and explicit about what you allow your representative to do.

Another common pitfall is failing to date the form correctly. A missing date or an incorrect date can lead to confusion about the form's validity. Ensure that you date the form at the time of signing to prevent issues later on. The date serves as a critical reference point for the authority granted.

People sometimes overlook the need to keep a copy of the completed form. It’s vital to retain a personal copy for future reference. Without it, one may struggle to recall the specifics of the permissions granted or face difficulties in case of disputes. Keeping documentation can simplify communication with your tax representative and streamline the process.

Lastly, many individuals forget to review the form thoroughly before submission. A quick glance may not reveal all the mistakes, including typographical errors or misplaced information. Taking the time to carefully check the form can save significant hassle in the tax management process. Simple errors can lead to significant consequences.

When dealing with tax matters, individuals and businesses may need to use a variety of forms and documents in addition to the Tax Power of Attorney (POA) form BT-129. Understanding these documents can help ensure that you are prepared for any tax-related situation. Here’s a list of some commonly used forms that may accompany the BT-129.

Having these documents ready can help streamline your dealings with tax authorities. Each form serves a specific purpose and may be crucial in various situations, so being informed and organized is always beneficial.

The Tax POA form BT-129 allows a taxpayer to appoint an individual to represent them before the IRS. This form shares similarities with several other legal documents used for different purposes. Here’s a list of nine documents with similar functions or traits:

When filling out the Tax POA form BT-129, certain guidelines can help ensure that the process goes smoothly. Here are four do's and don'ts to consider.

The Tax Power of Attorney (POA) form BT-129 is often surrounded by misunderstandings that can lead to confusion about its use and implications. Here are six common misconceptions, clarified for you.

Understanding these misconceptions about the BT-129 form can help taxpayers make informed decisions about their tax representation. When clarity is achieved, managing tax-related issues becomes much more manageable.

When filling out and using the Tax Power of Attorney (POA) Form BT-129, here are some essential points to keep in mind:

Each of these points can help facilitate a smooth process when dealing with your taxes and ensure that your representative has the authority necessary to assist effectively.