The Tax Power of Attorney (POA) Form DP-2848 serves as an essential tool for taxpayers who wish to appoint someone to act on their behalf in matters related to the Internal Revenue Service (IRS). This form allows individuals to designate an attorney, accountant, or another representative to handle their tax issues, ensuring that communication with the IRS is seamless and efficient. By using this form, taxpayers grant their representatives the authority to request and receive information, negotiate, and make decisions regarding their tax obligations and rights. With specific sections detailing the powers granted, including the ability to sign tax returns and represent the taxpayer in various proceedings, the DP-2848 accommodates a range of circumstances. Moreover, this form must be completed accurately and submitted in a timely fashion to avoid any lapses in representation. Understanding the nuances of the DP-2848 is crucial for individuals who seek assistance in navigating their tax responsibilities, as it ultimately enhances their ability to manage fiscal matters with confidence.

DO NOT STAPLE

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

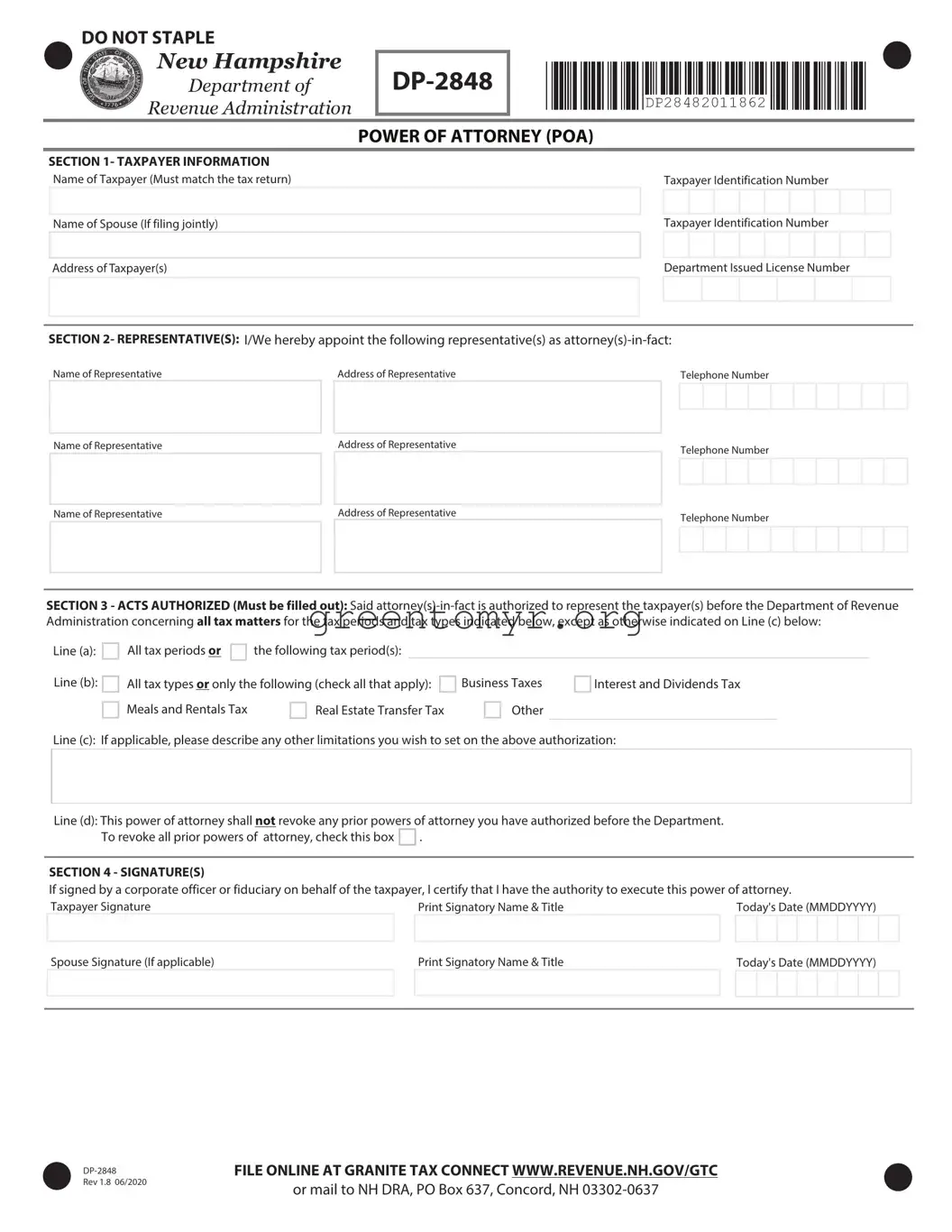

POWER OF ATTORNEY (POA) |

|

|

|

||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

SECTION 1- TAXPAYER INFORMATION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Name of Taxpayer (Mustmatchthe |

tax |

return) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer Identification Number |

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Name of Spouse (If filing jointly) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxpayer Identification Number |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of Taxpayer(s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Department Issued License Number |

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SECTION 2- REPRESENTATIVE(S): I/We hereby appoint the following representative(s) as

|

Name of Representative |

|

Address of Representative |

Telephone Number |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Representative |

|

Address of Representative |

Telephone Number |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Representative |

|

Address of Representative |

Telephone Number |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SECTION 3 - ACTS AUTHORIZED (Must be filled out): Said

Line (a):

Line (b):

All tax periods or |

|

the following tax period(s): |

All tax types or only the following (check all that apply):

Meals and Rentals Tax |

|

Real Estate Transfer Tax |

Business Taxes

Other

Interest and Dividends Tax

Line (c): If applicable, please describe any other limitations you wish to set on the above authorization:

Line (d): This power of attorney shall not revoke any prior powers of attorney you have authorized before the Department.

To revoke all prior powers of attorney, check this box |

. |

SECTION 4 - SIGNATURE(S)

If signed by a corporate officer or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power of attorney.

Taxpayer Signature |

Print Signatory Name & Title |

Today's Date (MMDDYYYY) |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse Signature (If applicable) |

Print Signatory Name & Title |

Today's Date (MMDDYYYY) |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rev 1.8 06/2020

FILE ONLINE AT GRANITE TAX CONNECT WWW.REVENUE.NH.GOV/GTC

or mail to NH DRA, PO Box 637, Concord, NH

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

POWER OF ATTORNEY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

INSTRUCTIONS |

(POA) |

||||||||||||||

|

|

|

|

|

|

|||||||||||

WHEN TO FILE

A Power Of Attorney (POA) is required prior to the Department of Revenue Administration communicating with anyone other than the taxpayer regarding any issue relating to the taxpayer.

WHERE TO FILE

File online at Granite Tax Connect www.revenue.nh.gov/gtc or mail to NH DRA, Taxpayer Services Division, PO Box 637, Concord NH

PLEASE NOTE

All applicable items must be filled in to properly complete Form

SECTION 1 - TAXPAYER INFORMATION

Enter the taxpayer's name (must match the tax return), current mailing address including zip code, and taxpayer identification number (and Department issued license number if applicable). If joint returns are involved and you and your spouse are designating the same representative(s), also enter your spouse's name and taxpayer identification number (and Department issued license number if applicable). If you need to list additional taxpayers, an additional page may be attached with each taxpayer's name and taxpayer identification number.

SECTION 2 - REPRESENTATIVE(S)

Enter the name of the representative(s). This can be an individual(s) or the name of a firm. What you enter in the Name of Representative box determines who the Department will have authority to correspond with as your authorized representative. If you list only an individual(s) name from a firm, then only the individual(s) will have authority to represent you. If you put the firm name in the Name of Representative box then ANYONE with the firm will have the authority to represent you.

Enter the current mailing address including zip code of the representative in the Address of Representative box beside the Name of Representative box. Only the person(s) or firm named in the Name of Representative box has authorization to represent you with the Department. A firm name that is part of an individual's address does not mean that the employees of the firm can represent the taxpayer.

Provide the representative's phone number in the space provided. If more than one name is listed, provide the phone number of the first person listed.

This section allows for three representatives. If you have more than three, please attach an additional sheet and note "see attached" in one of the Name of Representative boxes.

SECTION 3 - ACTS AUTHORIZED (MUST BE FILLED OUT)

On Line (a), either check the "all" box to indicate that the representative applies to all tax periods, or limit the representation to a particular tax period(s) and provide the date range or period(s). If you enter only a year(s) (e.g. 2018) the representation will include any period (including any Meals and Rooms or Tobacco Tax periods, if authorized on Line (b)) that fall within that year. If you limit the representation to a date range, please be aware that your representative will not be permitted to discuss any other date range with the Department. Note: If you check both the "all" box and provide a date range, the representation will not be limited to the date range, but will apply to all dates and tax periods.

On Line (b), check the boxes for the tax types that apply to your representation. If the representation applies to all taxes, check the "all" box. To limit the representation to one or more taxes, check all the appropriate boxes and for any taxes not shown, check the "other" box and identify the taxes on the line (for example MET or UPT). Note: If you check both the "all" box and the boxes for specific taxes, the representation will not be limited to a specific tax, but will apply to all tax types.

On Line (c), describe any other limitations you wish to place on your representation. For example, if you wish to only authorize your representative to receive information, note this limitation on Line (c). Otherwise, your representative will not only be authorized to receive your confidential information but also full power to perform all acts necessary related to the subject matter of the indicated tax types and periods.

If the box on Line (d) is not checked, the filing of this form will not revoke or otherwise invalidate any prior powers on file with the Department. If you check the box provided on Line (d), you will revoke all prior powers of attorney, unless the representatives are identified again in Section 2 of this form.

If you are a representative that wishes to withdraw representation of a taxpayer, please forward a signed and dated letter with a copy of the POA you are withdrawing to the Department.

Rev 1.8 06/2020

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

POWER OF ATTORNEY

(POA)

INSTRUCTIONS Continued

SECTION 4 - SIGNATURE(S)

The taxpayer is required to sign and date the POA. The completed and signed form

NEED HELP?

Questions not covered here may be answered in our "Frequently Asked Questions" available on our website at www.revenue.nh.gov or by calling Taxpayer Services at (603)

Rev 1.8 06/2020

| Fact Name | Detail |

|---|---|

| Purpose | The DP-2848 form serves as a Power of Attorney for tax matters, allowing a designated representative to act on behalf of a taxpayer. |

| Who Can Use It | This form can be used by both individuals and businesses who need assistance with their tax matters. |

| Governing Laws | The DP-2848 is governed by state-specific tax laws, which can differ by jurisdiction. It’s important to check local regulations. |

| Validity | The Power of Attorney remains valid until revoked by the taxpayer or the specific authority has been completed. |

| Signature Requirement | The form must be signed by the taxpayer to validate the authorization for the representative. |

| Submission Process | The DP-2848 form must be submitted to the appropriate tax authority, either through mail or electronically, depending on state guidelines. |

After you have completed the Tax POA form DP-2848, you will submit it to the relevant tax authority. Doing this allows the specified representative to handle certain tax matters on your behalf. Ensure that you review all information for accuracy before sending it in.

Finally, submit the completed DP-2848 form to the appropriate IRS office. You may also choose to fax it, depending on the situation. Always check the instructions for the preferred submission method.

The Tax POA form DP-2848 is a Power of Attorney form that allows you to authorize someone to represent you before the IRS or other tax authorities. This individual can manage your tax matters on your behalf, including handling communications and filing documents related to your tax obligations.

You can authorize a wide range of individuals, including tax professionals, attorneys, or family members, to act on your behalf. The person you choose must be trustworthy and capable of managing your tax affairs competently. Make sure they meet the requirements outlined by the IRS and can represent you effectively.

Completing the DP-2848 form involves the following steps:

Ensure all details are accurate before submission to avoid delays in processing.

The DP-2848 form remains valid until you revoke it or the specific tax matters it covers have been resolved. You may revoke the authorization at any time by submitting a written notice to the IRS, which establishes that you no longer want the designated person to represent you.

The completed DP-2848 form should be sent to the appropriate address indicated in the instructions provided with the form. This could be the location of the specific IRS office handling your tax matters or a designated address for processing such forms. Check the latest IRS guidelines to ensure accurate submission and timely processing.

Filling out the Tax Power of Attorney (POA) Form 2848 can be a daunting task for many individuals, often leading to mistakes that could affect tax representation. One common error is failing to provide complete and accurate personal information. This includes not using the full legal name, neglecting to fill in the correct address, or omitting identification numbers. Such omissions can create delays or even invalidate the POA, hindering the process of tax representation.

Another frequent mistake occurs when individuals overlook signing the form where required. Proper execution is crucial. Incomplete signatures may result in the IRS returning the form or refusing to process it. Always double-check for signatures from all relevant parties. Each signatory must ensure their name is appropriately printed alongside their signature to avoid any confusion regarding representation.

People often mistakenly assume that the IRS will automatically understand their intentions. A lack of specificity in designating the powers granted to the representative can lead to significant misunderstandings. It is essential to clearly outline the scope of authority being granted. Whether it’s for specific tax years or general representation, clarity can prevent complications later on.

Lastly, failing to use the most current version of the form can be a significant pitfall. Tax forms are subject to updates and changes. Using an outdated version of Form 2848 may result in the IRS rejecting the request for representation. Before submission, it is prudent to verify that the latest form is being used to ensure compliance with current regulations.

The Tax Power of Attorney (POA) form, also known as Form 2848, allows individuals to designate someone to represent them regarding their tax matters. When using this form, several other documents may be helpful in ensuring a smooth process. Here are some commonly used forms and documents that often accompany the Tax POA:

Using these forms alongside the Tax POA form can streamline communication and ensure that the designated representative has the necessary authorization to act on behalf of the taxpayer in various situations. Each document has its specific purpose and is instrumental in managing tax-related matters effectively.

When completing the Tax Power of Attorney (POA) Form DP-2848, it’s important to keep a few guidelines in mind. Here are seven things you should and shouldn't do:

The IRS Power of Attorney (POA) form, known as DP-2848, is a vital tool for anyone needing to appoint someone to handle their tax matters. Unfortunately, many misunderstandings about this form persist. Below are some common misconceptions:

Understanding these misconceptions can help taxpayers better navigate their rights and responsibilities regarding representation with the IRS. Utilizing the DP-2848 effectively ensures that individuals empower trusted representatives to manage their tax affairs.

Filling out and using the Tax POA form, known as Form 2848, is a crucial step for individuals seeking to authorize someone to represent them before the IRS. Here are some key takeaways regarding its use:

Understanding these key aspects will streamline the process and ensure that your representation is effective and compliant with IRS regulations.