The Tax Power of Attorney (POA) Form PA-1 is an essential document for individuals and businesses navigating their tax obligations in Pennsylvania. Designed to allow taxpayers to appoint a trusted individual, such as an attorney or tax professional, this form grants them the authority to handle tax matters on their behalf. It is pivotal during times of illness or absence, ensuring that tax filings and communications can continue without disruption. The form encompasses various provisions that address both the broad and specific powers granted, including the ability to represent the taxpayer before the Pennsylvania Department of Revenue. By completing and submitting the PA-1, taxpayers can secure much-needed assistance with tax issues, audits, disputes, and filings. Understanding this form is vital, as it not only streamlines the process but also helps to mitigate the risks associated with tax compliance. Ensuring that the PA-1 form is accurately completed and filed can lead to a smoother, less stressful experience when dealing with state tax authorities.

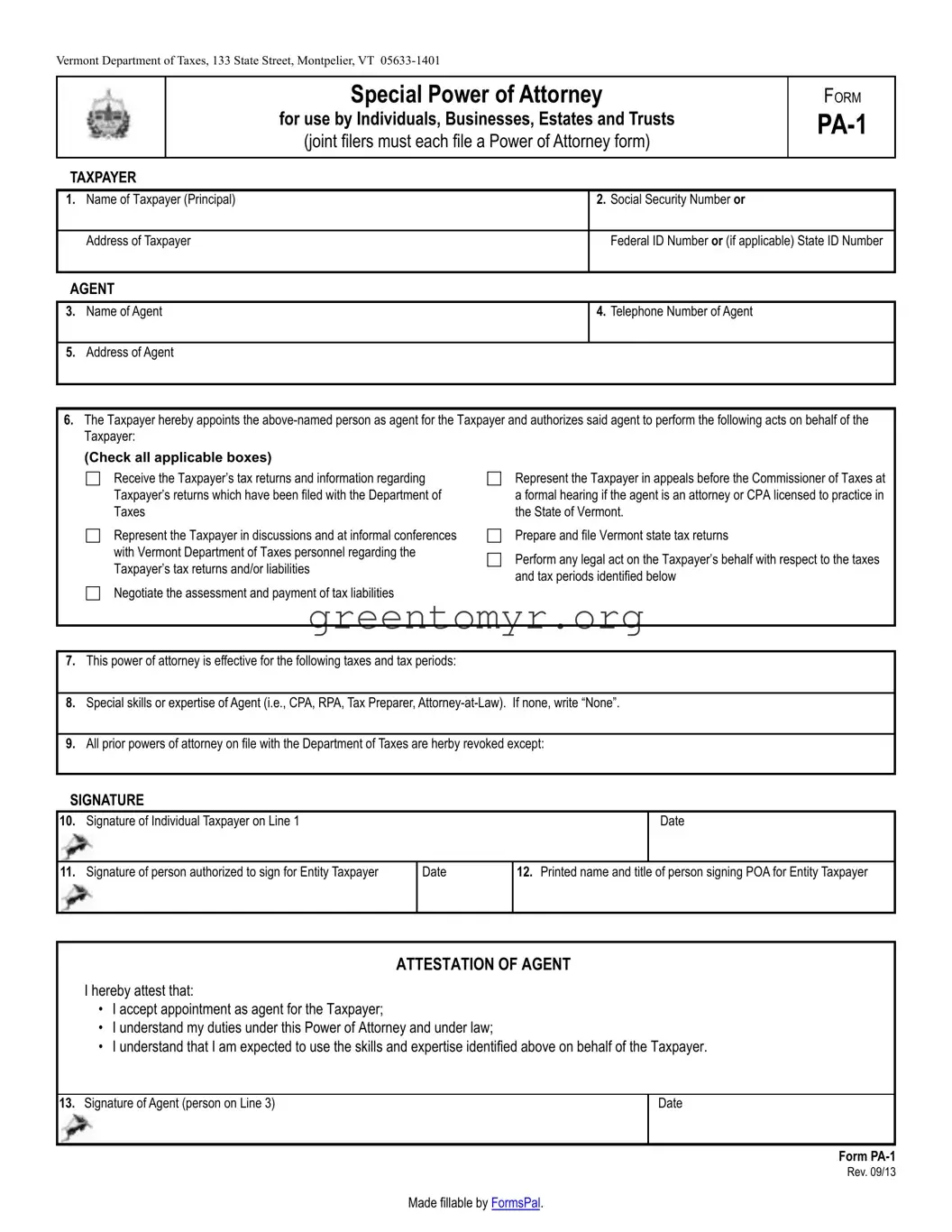

Vermont Department of Taxes, 133 State Street, Montpelier, VT

|

|

|

Special Power of Attorney |

|

FORM |

|

|

|

|

for use by Individuals, Businesses, Estates and Trusts |

|||

|

|

|

(joint filers must each file a Power of Attorney form) |

|

||

TAXPAYER |

|

|

|

|

||

1. |

Name of Taxpayer (Principal) |

|

2. |

Social Security Number or |

|

|

|

|

|

|

|

||

|

Address of Taxpayer |

|

|

Federal ID Number or (if applicable) State ID Number |

||

|

|

|

|

|

||

AGENT |

|

|

|

|

||

|

|

|

|

|

|

|

3. |

Name of Agent |

|

4. |

Telephone Number of Agent |

|

|

|

|

|

|

|

|

|

5. |

Address of Agent |

|

|

|

|

|

|

|

|

|

|

|

|

6. The Taxpayer hereby appoints the

|

Taxpayer: |

|

|

(Check all applicable boxes) |

|

|

Receive the Taxpayer’s tax returns and information regarding |

Represent the Taxpayer in appeals before the Commissioner of Taxes at |

|

Taxpayer’s returns which have been filed with the Department of |

a formal hearing if the agent is an attorney or CPA licensed to practice in |

|

Taxes |

the State of Vermont. |

|

Represent the Taxpayer in discussions and at informal conferences |

Prepare and file Vermont state tax returns |

|

with Vermont Department of Taxes personnel regarding the |

Perform any legal act on the Taxpayer’s behalf with respect to the taxes |

|

Taxpayer’s tax returns and/or liabilities |

|

|

and tax periods identified below |

|

|

Negotiate the assessment and payment of tax liabilities |

|

|

|

|

|

|

|

|

|

|

7. |

This power of attorney is effective for the following taxes and tax periods: |

|

|

|

|

8. |

Special skills or expertise of Agent (i.e., CPA, RPA, Tax Preparer, |

|

|

|

|

9. |

All prior powers of attorney on file with the Department of Taxes are herby revoked except: |

|

|

|

|

SIGNATURE |

|

|

10. |

Signature of Individual Taxpayer on Line 1 |

Date |

? |

|

|

|

|

|

11. |

Signature of person authorized to sign for Entity Taxpayer |

|

Date |

12. Printed name and title of person signing POA for Entity Taxpayer |

|

?- |

|

|

|

|

|

|

|

|

|

||

|

|

ATTESTATION OF AGENT |

|||

|

I hereby attest that: |

|

|

|

|

|

• I accept appointment as agent for the Taxpayer; |

|

|

|

|

|

• I understand my duties under this Power of Attorney and under law; |

|

|

||

|

• I understand that I am expected to use the skills and expertise identified above on behalf of the Taxpayer. |

||||

|

|

|

|

|

|

13. |

Signature of Agent (person on Line 3) |

|

|

|

Date |

|

|

|

|

|

|

Form

Rev. 09/13

Made fillable by FormsPal.

INSTRUCTIONS FOR COMPLETING VERMONT DEPARTMENT OF TAXES

SPECIAL POWER OF ATTORNEY (POA).

•This form may be used by individuals, businesses, estates and trusts. Joint income tax filers must each complete and file a power of attorney form.

•All POA forms submitted to the Department of Taxes must comply with the requirements of chapter 123 of Title 14, except that signatures of a witness and notary are not required.

•POA forms must be signed by the agent. THE DEPARTMENT OF TAXES WILL NOT ACCEPT A POA UNLESS

SIGNED BY THE AGENT.

•By signing, an agent attests that he/she accepts appointment as agent and understands the duties of agent, both under the POA and under the law. In addition, if special skills or expertise of the agent are identifed, the agent must attest that he/ she understands that he/she is expected to use those skills and expertise on behalf of the Taxpayer.

1.Print the name and address of the Taxpayer.

2.Enter the Social Security Number of an individual Taxpayer or Federal ID Number or (if applicable) State ID Number of an entity Taxpayer.

3.Print the name of the Agent.

4.Print the telephone number of the Agent.

5.Print the address of the Agent.

6.Check applicable boxes if you are authorized to prepare and file Vermont state tax returns, the returns must still be signed by the taxpayer.

7.List specific tax types (i.e., “income tax”) and tax periods (i.e., “2002”) for which Agent is authorized to

act on your behalf. If all taxes and tax periods, write “ALL”.

8.Identify any special skills or expertise of Agent which will be exercised by agent on behalf of Taxpayer, such as CPA, RPA, tax preparer,

9.List any prior Powers of Attorney on file with the Department of Taxes which are NOT revoked.

10.Signature of person on Line 1 if an individual Taxpayer.

11.Signature of person signing for an entity Taxpayer.

12.Print the name and title of person signing for an entity taxpayer.

13.Signature of Agent and date agent signed.

| Fact Name | Details |

|---|---|

| Name of Form | Tax Power of Attorney (PA-1) |

| Purpose | This form allows an individual to grant authority to another person to represent them in tax matters. |

| Governing Law | The form is governed by the Pennsylvania Consolidated Statutes Title 72, Section 7202. |

| Who Can Use It | Any taxpayer who wishes to authorize another person to handle their tax affairs can use this form. |

| Required Information | The form requires personal information from both the taxpayer and the representative, including names, addresses, and signatures. |

| Filing Location | The completed form should be sent to the Pennsylvania Department of Revenue. |

| Duration of Authority | The authority granted through this form remains in effect until revoked by the taxpayer. |

| Notarization | Notarization of the form is not required, but signatures must be duly authorized. |

Completing the Tax POA (Power of Attorney) form PA-1 is essential for designating someone to represent you in tax matters. After filling out this form, you will be able to authorize another individual to handle your tax issues on your behalf. Be sure to gather the necessary information before beginning to fill out the form.

The Tax POA PA-1 form is a Power of Attorney document that allows an individual to appoint someone else to represent them in matters related to tax issues. This can include handling tax returns, correspondence, and any audits with the tax authority. It streamlines communication and can ease the burden on the taxpayer by granting authority to a trusted representative.

Any individual can be designated as a Power of Attorney, as long as they are of legal age and competent to handle the responsibilities. This can be a family member, friend, or a tax professional, such as an accountant or attorney. It is important to choose someone who understands tax matters and can represent your interests effectively.

To complete the PA-1 form, follow these steps:

No, the PA-1 form does not require notarization. However, ensure that all signatures are completed as required. It’s always a good practice to keep a copy of the completed form for your records.

Yes, you can revoke a Power of Attorney at any time as long as you are competent to do so. To revoke the authority, you must submit a written revocation to the tax authority, along with a copy of the original PA-1 form. It's advisable to inform your appointed representative about the revocation as well.

Generally, there is no fee required for submitting the PA-1 form to the tax authority. However, check with the specific agency for any potential costs related to processing or other related services that might arise.

The PA-1 form becomes effective once it has been submitted and accepted by the tax authority. The processing time may vary, but typically, you can expect it to be effective within a few weeks. You may want to check with the agency if you have concerns about the timeline.

Yes, you can appoint multiple individuals to serve as Power of Attorney, either jointly or separately. If individuals are named together, they must typically act in unison unless otherwise specified. Clarification on how they can operate is important to avoid confusion in transactions.

If you do not file a Power of Attorney, the tax authority will only communicate directly with you regarding tax matters. This can complicate situations, especially during audits or if you are unable to handle your tax affairs. Granting someone Power of Attorney can ensure that your interests are better managed when dealing with tax complexities.

The PA-1 form is primarily intended for state tax matters. However, you may need to complete separate forms for federal tax representation. Check with the IRS and your state tax authority for specific requirements regarding Power of Attorney forms tailored to their processes.

Filling out the Tax Power of Attorney (POA) form, known as PA-1, is a crucial step for anyone looking to authorize someone else to handle their tax matters. Unfortunately, many people make mistakes during this process, which can lead to significant issues down the line. Here are ten common errors to avoid when completing the PA-1 form.

First and foremost, neglecting to provide accurate personal information can cause delays. Individuals must ensure that their names, addresses, and Social Security numbers are correct and match their official documents. A small typo can lead to complications.

Another mistake often seen is failing to specify the powers granted to the representative. The form allows for a range of designations, from limited to general powers. Clarity on what the representative is authorized to do helps avoid any confusion in the future.

Some individuals mistakenly leave the signature blank or forget to sign at all. Without a valid signature, the form may be rendered invalid, which defeats its purpose. Always double-check that the required signatures are provided.

A frequent oversight involves using outdated forms. Tax forms and regulations can change, so it’s essential to ensure you are using the most current version of the PA-1 form to avoid any unexpected rejections.

Moreover, individuals often neglect to include their representative's information completely. It’s vital to provide detailed information about the person authorized to act on your behalf, including their name, address, and taxpayer identification number. Without this information, the IRS may not recognize them as your representative.

Many people also make the error of not indicating the duration of the POA. Whether it’s a specific timeframe or until revoked, stating this clearly helps the representative know how long their authority lasts.

Another common issue is overlooking the “Revocation” section. If someone decides to cancel their POA, it’s essential to follow the right procedures to revoke it formally. Skipping this step can lead to unauthorized actions being taken after the desired revocation.

In some cases, individuals forget to keep a copy of the completed form. Having a copy for personal records is important for reference and ensures you have proof of who is authorized to manage your tax affairs.

Finally, failing to follow up on the status of the POA can be a mistake. Once the form is submitted, it’s advisable to verify that the IRS has processed the request. Checking confirms that everything is in order and can help address any issues that arise quickly.

Being mindful of these common mistakes can help ensure a smoother experience when completing the PA-1 form. Taking the time to carefully fill out the information can make a significant difference in managing tax matters effectively.

When submitting a Tax Power of Attorney (POA) form PA-1, several additional documents may be required to ensure the process runs smoothly. Each of these forms serves a unique purpose in the tax representation process. Below is a list of commonly used documents associated with the PA-1 form.

These documents can accelerate the communication between the taxpayer and the IRS while also ensuring that all necessary information is available for the representatives involved. It is essential to prepare and submit them accurately to avoid potential delays in processing tax matters.

When filling out the Tax POA Form PA-1, keep these guidelines in mind:

By following these tips, you can simplify the process and avoid common mistakes.

Understanding the Tax POA form PA-1 can be challenging. Here are nine common misconceptions people have about this form, along with clarifications for each misconception.

This is not true. While tax professionals often handle these forms, individuals can also file the form on their own behalf.

Many believe the form is needed solely for tax filings. In reality, it can also be used to authorize someone to address tax-related issues, not just to file returns.

While a Power of Attorney allows your representative to act on your behalf, it doesn’t grant them unlimited authority. You specify the scope of their powers within the form.

This is a misconception. You can revoke the Power of Attorney at any time. Just be sure to notify the IRS and your representative.

Each state has its own guidelines and requirements for POA forms. Verify that you are using the correct version specific to your state.

Once filed, the Power of Attorney remains in effect until revoked or canceled. You do not need to resubmit the form annually.

While the taxpayer is generally involved, someone else can help fill it out, provided they have the necessary information and consent from the taxpayer.

This is a common belief, but it's not the case. Anyone can be appointed as your representative as long as they are not disqualified by the IRS.

It’s essential to keep a copy of the filed form for your records. You may need it for future reference or if disputes arise.

When filling out and using the Tax POA form PA-1, keep these key takeaways in mind: