The Tax Power of Attorney (POA) Form R-7006 is a crucial document that grants an individual the authority to act on behalf of another person in tax matters. This form is especially important for those needing assistance with federal and state tax obligations, whether due to personal circumstances or complexities involved in tax law. By completing and submitting the R-7006 form, a taxpayer explicitly allows their designated representative—such as an attorney, accountant, or any trusted individual—to communicate with tax authorities, obtain tax information, and make decisions regarding their tax filings. It streamlines the often-complicated process of managing tax affairs, ensuring that the chosen representative can operate effectively on behalf of the taxpayer. Furthermore, by using this form, individuals can specify the scope of authority granted, such as whether it includes all tax matters or is limited to specific issues. It’s essential to complete the form accurately and to keep it updated, as a change in circumstances or representation may necessitate a new POA to avoid any potential complications with tax liabilities. As taxpayers navigate their obligations, understanding the role and functionality of Form R-7006 can significantly ease the burden of compliance and facilitate a smoother interaction with the taxing authorities.

LOUISIANA

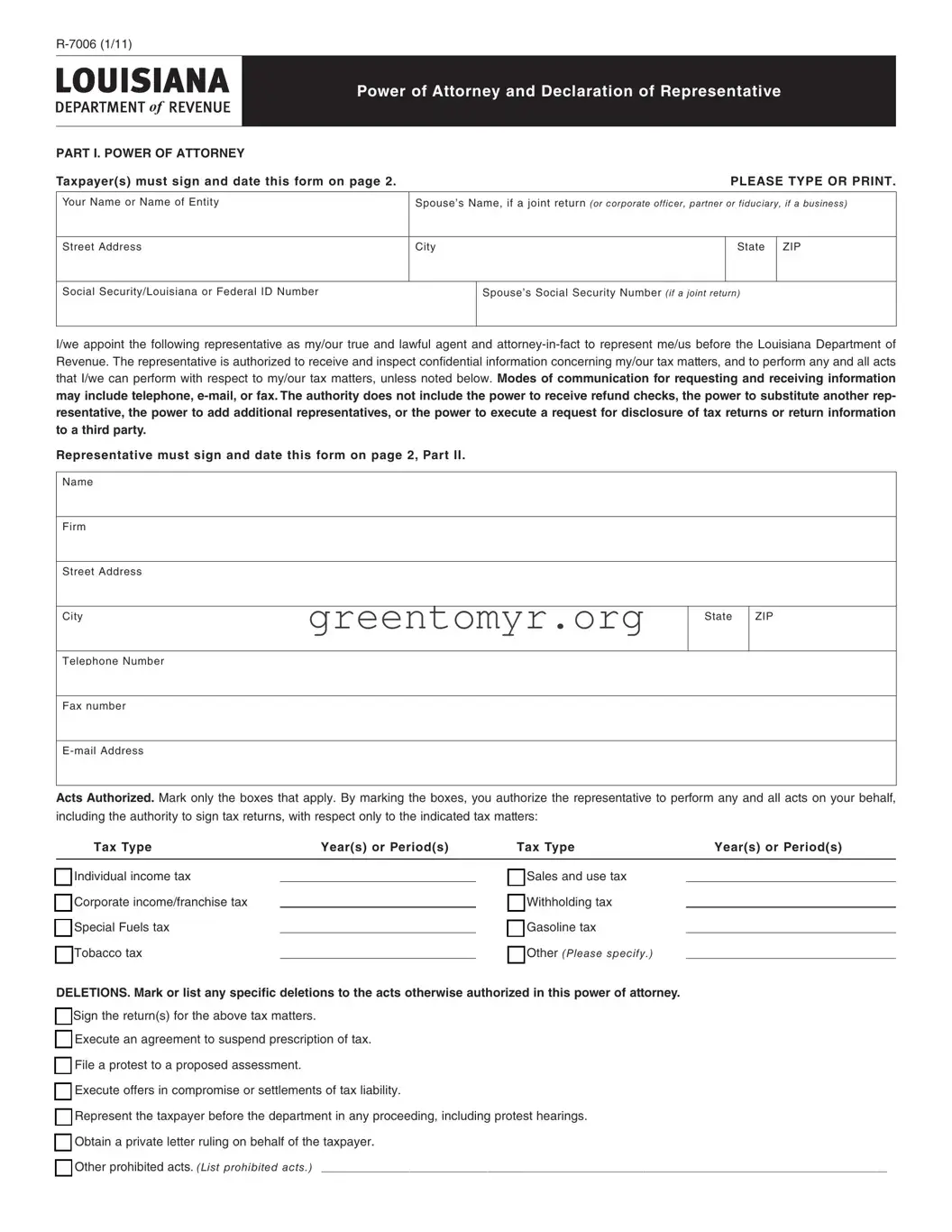

Power of Attorney and Declaration of Representative

DEPARTMENT of REVENUE

PART I. POWER OF ATTORNEY |

|

|

|

|

Taxpayer(s) must sign and date this form on page 2. |

|

|

PLEASE TYPE OR PRINT. |

|

|

|

|

|

|

Your Name or Name of Entity |

Spouse’s Name, if a joint return (or corporate officer, partner or fiduciary, if a business) |

|||

|

|

|

|

|

Street Address |

City |

|

State |

ZIP |

|

|

I |

|

I |

Social Security/Louisiana or Federal ID Number |

Spouse’s Social Security Number (if a joint return) |

|||

I

I/we appoint the following representative as my/our true and lawful agent and

Representative must sign and date this form on page 2, Part II.

Name

Firm

Street Address

City |

State |

ZIP |

|

I |

I |

Telephone Number |

|

|

( |

) |

|

|

|

|

Fax number |

|

|

( |

) |

|

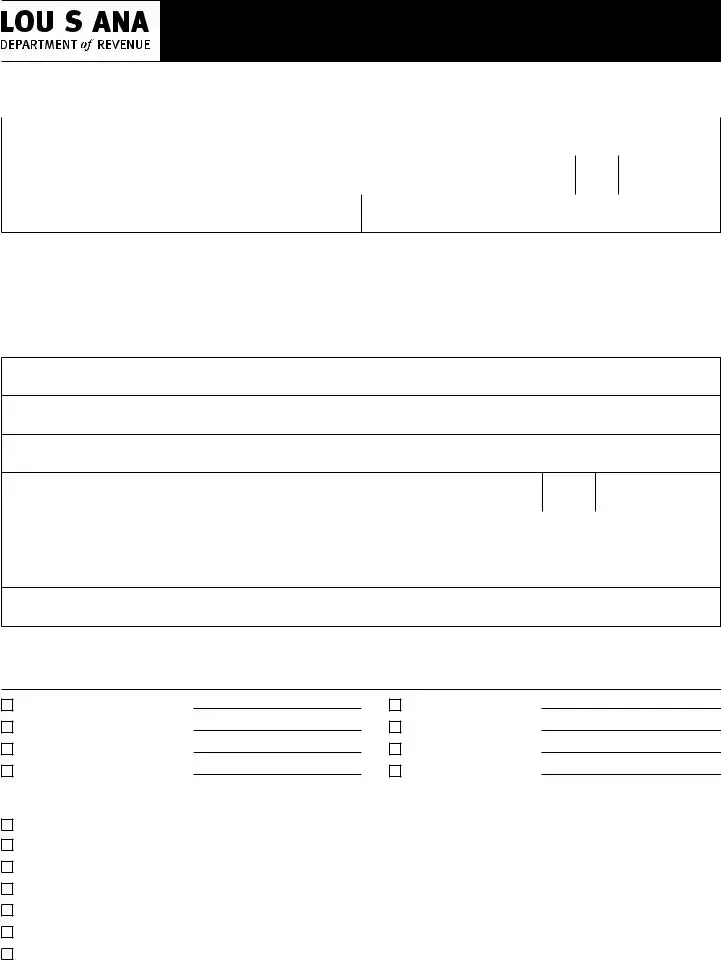

Acts Authorized. Mark only the boxes that apply. By marking the boxes, you authorize the representative to perform any and all acts on your behalf, including the authority to sign tax returns, with respect only to the indicated tax matters:

Tax Type |

Year(s) or Period(s) |

Tax Type |

Year(s) or Period(s) |

■ Individual income tax |

|

■ Sales and use tax |

|

□ |

|

□ |

|

■ Corporate income/franchise tax |

|

■ Withholding tax |

|

□ |

|

□ |

|

■ Special Fuels tax |

|

■ Gasoline tax |

|

□ |

|

□ |

|

■ Tobacco tax |

|

■ Other (Please specify.) |

|

□ |

|

□ |

|

DELETIONS. Mark or list any specifc deletions to the acts otherwise authorized in this power of attorney.

□■ Sign the return(s) for the above tax matters.

□■ Execute an agreement to suspend prescription of tax. □■ File a protest to a proposed assessment.

□■ Execute offers in compromise or settlements of tax liability.

□■ Represent the taxpayer before the department in any proceeding, including protest hearings. □■ Obtain a private letter ruling on behalf of the taxpayer.

□■ Other prohibited acts. (List prohibited acts.) _____________________________________________________________________________________________________________

Page 2 |

NOTICES AND COMMUNICATIONS. Original notices and other written communications will be sent only to you, the taxpayer. Your representative may request and receive information by telephone,

REVOCATION OF PRIOR POWER(S) OF ATTORNEY. Except for Power(s) of Attorney and Declaration of Representative(s) fled on Form

Signature of Taxpayer(s). If a tax matter concerns a joint return, both husband and wife must sign if joint representation is requested. If signed by a corporate officer, partner, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer.

IF THIS POWER OF ATTORNEY IS NOT SIGNED AND DATED, IT WILL BE RETURNED.

_______________________________________________________________________________________________________________________________________ |

______________________________ |

|

Taxpayer signature |

|

Date (mm/dd/yyyy) |

____________________________________________________________________________________________________________________________________________ |

_________________________________ |

|

Spouse signature |

|

Date (mm/dd/yyyy) |

_________________________________________________________________________________ |

_______________________________________________________ |

_________________________________ |

Signature of duly authorized representative, if the taxpayer |

Title |

Date (mm/dd/yyyy) |

is a corporation, partnership, executor or administrator |

|

|

Part II. DECLARATION OF REPRESENTATIVE

Under penalties of perjury, I declare that:

•I am not currently under suspension or disbarment from practice before the Internal Revenue Service.

•I am authorized to represent the taxpayer(s) identified in Part I for the tax matters specified there; and

•I am one of the following: (insert applicable letter in table below)

a.

b.Certified Public

c.Enrolled

d.

e.

f.Family

g.Other (state the relationship, i.e., bookkeeper or friend)

h.Former Louisiana Department of Revenue Employee. As a representative, I cannot accept representation in a matter with which I had direct involvement while I was a public employee.

IF THIS DECLARATION OF REPRESENTATIVE IS NOT SIGNED AND DATED, THE POWER OF ATTORNEY WILL BE RETURNED.

State Issuing

License

State License Number

Signature

Date

(mm/dd/yyyy)

I |

I |

I |

I |

I |

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 7006 allows taxpayers to designate a power of attorney to represent them before the IRS. |

| Eligibility | Individuals and entities, including corporations and partnerships, can use this form to appoint an attorney or other authorized representative. |

| Filing Requirement | Taxpayers must submit Form 7006 to the IRS to allow their appointed representative access to tax information. |

| Revocation | Taxpayers can revoke the power of attorney by submitting a new Form 7006 or a written statement that clearly states the revocation. |

| State-Specific Forms | Many states have their own power of attorney forms that govern tax matters, such as the California Power of Attorney (Form FTB 3520) under the California Revenue and Taxation Code. |

| Timeframe | Once submitted, the IRS typically processes the Form 7006 within a few weeks, but processing times may vary based on workload. |

| Signature Requirement | The taxpayer must sign the form, and if the representative is an entity, an authorized individual must also sign to validate the appointment. |

Completing the Tax POA Form R-7006 is essential for granting someone the authority to act on your behalf concerning tax matters. To ensure a smooth process, follow these steps carefully to fill out the form correctly.

The Tax POA Form R-7006 is a Power of Attorney document used in the United States for tax purposes. It allows one person, referred to as the agent, to represent another individual or entity, known as the principal, in matters related to federal or state taxes. This form ensures that the agent has the authority to discuss and resolve tax issues on behalf of the principal.

This form is ideal for individuals or businesses that require assistance from a tax professional or attorney. If you are unable to handle your tax matters due to time constraints or lack of expertise, consider appointing an agent to act on your behalf using the R-7006 form.

To complete the R-7006 form:

After filling out the form, submit it to the appropriate tax authority, either at the federal or state level. Make sure to keep a copy for your records. You may need to also provide additional documents, depending on the specific requirements of the tax authority you are dealing with.

The Tax POA Form R-7006 remains valid until you revoke it or until the specific assignment is completed. You can revoke the authorization at any time, but be aware that the revocation must be communicated to both the agent and the relevant tax authority.

Yes, you can revoke the R-7006 form at any time. To do so, you must complete a revocation document and notify your agent as well as the tax authority. Be sure to follow any specific guidelines provided by the tax authority for revocation to ensure proper processing.

If you do not authorize a Tax POA, you will need to handle all tax matters yourself. This includes filing returns, responding to notices, and addressing any disputes with the tax authorities, which can be time-consuming and complex without professional assistance.

The form allows for the appointment of one primary agent. However, you can specify alternate agents if needed. It is essential to clearly outline their roles and responsibilities in the form to avoid any confusion regarding authority.

When completing the Tax Power of Attorney (POA) Form R-7006, individuals often encounter a range of common mistakes that can complicate the process. Awareness of these pitfalls can help ensure a smoother experience.

One frequent error is failing to include the correct taxpayer identification number. Providing either an incorrect number or omitting it altogether can lead to delays or rejection of the form. It’s crucial to double-check this information before submission.

Another mistake is neglecting to sign the form. A signature is not just a formality; it validates the document. Without it, the form may not be accepted. Always remember to sign and date where indicated.

Many people also overlook the importance of specifying the scope of the authority granted. The form allows for varied levels of authorization, and not clearly defining this can cause misunderstandings later on. Take the time to specify what the representative is allowed to do on your behalf.

Incomplete or incorrect contact information for the representative is another common issue. Make sure to provide accurate details for the individual who will act on your behalf. This includes their name, address, and phone number, as well as any applicable credentials.

Some individuals forget to indicate whether the authority is to be effective immediately or whether it should begin at a later date. Clarity on this point is essential; otherwise, it may lead to confusion or unwanted complications.

Additionally, confusion often arises around the duration of the Tax POA. Individuals sometimes leave this section blank or do not specify an end date. It’s beneficial to clarify how long the authorization is intended to last to prevent any issues down the line.

Failing to keep a copy of the submitted form is a mistake worth avoiding. Retaining a copy ensures that you have a record of what was submitted and serves as helpful documentation if questions arise later.

Another common error involves misunderstanding the needs of the IRS. Individuals may mistakenly believe they need a POA for all matters when it may only apply to specific tax issues. Understanding the requirements can reduce the likelihood of submitting unnecessary forms.

Lastly, some individuals mistakenly assume that the form does not require any additional documentation. However, certain situations may require you to include supplementary information. Being thorough in your submission can help avoid complications.

The Tax Power of Attorney (POA) form R-7006 allows individuals to grant someone else the authority to handle their tax matters. In conjunction with the R-7006 form, various other documents may also be required or useful. Below is a list of common forms and documents often used alongside the R-7006. Each item is described to provide clarity on its purpose.

Ensuring all necessary documents are prepared and submitted alongside the Tax POA form R-7006 is crucial for effective tax representation. Carefully review each document's purpose and use them as needed to simplify interactions with tax authorities.

Here are some important do's and don'ts when filling out the Tax POA Form R-7006:

The Tax Power of Attorney form, better known as the IRS Form 7006, often encounters misunderstandings. Here are five common misconceptions about this important document:

Understanding these misconceptions is crucial for effective tax representation. Clear information empowers individuals and businesses to navigate their tax obligations confidently.

When considering the use of the Tax POA Form R-7006, it is essential to understand its purpose and significance. This form allows you to grant authority to another individual to represent you before the tax authorities. Below are key takeaways that can help simplify the process.

Understanding these key points can facilitate a smoother experience when filling out and using the Tax POA Form R-7006, ultimately benefiting both you and your designated representative.