The Tax Power of Attorney (POA) form RD-1061 plays a crucial role in the realm of tax management, allowing individuals and businesses to designate a representative who can act on their behalf when dealing with tax matters. Whether it's preparing and filing returns, addressing audits, or resolving tax discrepancies, the form ensures that the appointed representative has the authority to interact with tax agencies. By utilizing the RD-1061, taxpayers can streamline their communication with tax authorities, minimizing stress during tax season or when other challenges arise. Moreover, this form outlines the specific powers granted to the representative, which can include signing documents, negotiating on behalf of the taxpayer, and accessing confidential tax information. Understanding the nuances of the RD-1061 is necessary for anyone looking to simplify their tax obligations and ensure compliance while relying on a trusted advisor. This article will explore the key components of the RD-1061, the process of completing the form, and the benefits of designating a representative for tax matters.

Form

CLEAR

Page 1

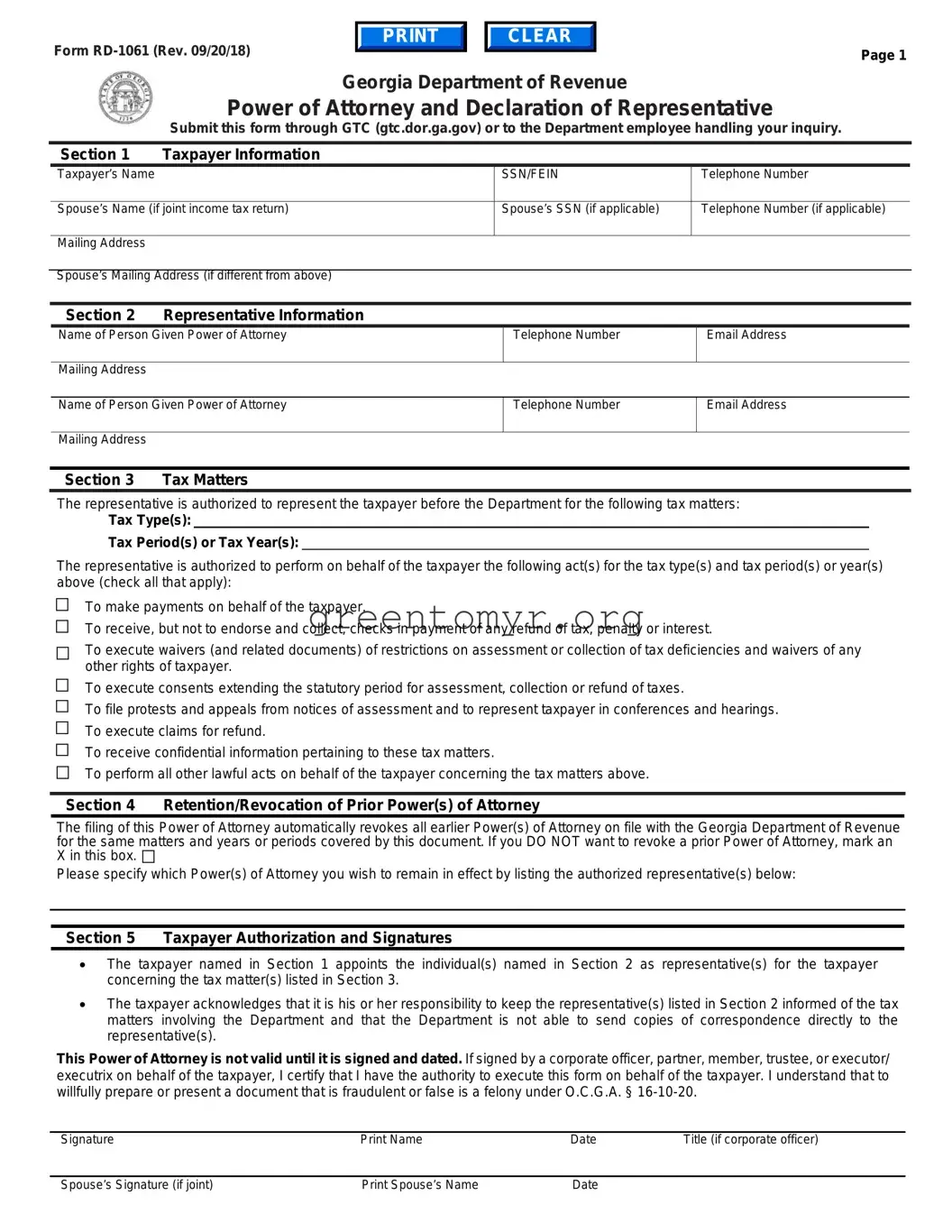

Georgia Department of Revenue

Power of Attorney and Declaration of Representative

Submit this form through GTC (gtc.dor.ga.gov) or to the Department employee handling your inquiry.

Section 1 |

Taxpayer Information |

|

|

|

Taxpayer’s Name |

|

SSN/FEIN |

Telephone Number |

|

|

|

|

|

|

Spouse’s Name (if joint income tax return) |

Spouse’s SSN (if applicable) |

Telephone Number (if applicable) |

||

Mailing Address

Spouse’s Mailing Address (if different from above)

Section 2 Representative Information

Name of Person Given Power of Attorney

Mailing Address

Telephone Number

Email Address

Name of Person Given Power of Attorney

Mailing Address

Telephone Number

Email Address

Section 3 |

Tax Matters |

The representative is authorized to represent the taxpayer before the Department for the following tax matters:

Tax Type(s):

Tax Period(s) or Tax Year(s):

The representative is authorized to perform on behalf of the taxpayer the following act(s) for the tax type(s) and tax period(s) or year(s) above (check all that apply):

To make payments on behalf of the taxpayer.

To receive, but not to endorse and collect, checks in payment of any refund of tax, penalty or interest.

To execute waivers (and related documents) of restrictions on assessment or collection of tax deficiencies and waivers of any other rights of taxpayer.

To execute consents extending the statutory period for assessment, collection or refund of taxes.

To file protests and appeals from notices of assessment and to represent taxpayer in conferences and hearings.

To execute claims for refund.

To receive confidential information pertaining to these tax matters.

To perform all other lawful acts on behalf of the taxpayer concerning the tax matters above.

Section 4 Retention/Revocation of Prior Power(s) of Attorney

The filing of this Power of Attorney automatically revokes all earlier Power(s) of Attorney on file with the Georgia Department of Revenue for the same matters and years or periods covered by this document. If you DO NOT want to revoke a prior Power of Attorney, mark an X in this box.

Please specify which Power(s) of Attorney you wish to remain in effect by listing the authorized representative(s) below:

Section 5 Taxpayer Authorization and Signatures

•The taxpayer named in Section 1 appoints the individual(s) named in Section 2 as representative(s) for the taxpayer concerning the tax matter(s) listed in Section 3.

•The taxpayer acknowledges that it is his or her responsibility to keep the representative(s) listed in Section 2 informed of the tax matters involving the Department and that the Department is not able to send copies of correspondence directly to the representative(s).

This Power of Attorney is not valid until it is signed and dated. If signed by a corporate officer, partner, member, trustee, or executor/ executrix on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer. I understand that to willfully prepare or present a document that is fraudulent or false is a felony under O.C.G.A. §

Signature |

Print Name |

Date |

Title (if corporate officer) |

Spouse’s Signature (if joint) |

Print Spouse’s Name |

Date |

|

Form |

Page 2 |

Section 6 Acknowledgment of the Power of Attorney

This Power of Attorney must be acknowledged by the taxpayer before a notary public, unless the appointed representative(s) is licensed to practice as an

Acknowledgement of Power of Attorney. The person(s) signing as the taxpayer in Section 5 above appeared this day before a notary public and acknowledged this Power of Attorney as a voluntary act and deed.

Sworn and subscribed before me this __________ day of ______________________, 20_______.

Signature of Notary

Notary Seal

Date

Section 7 Declaration of Representative

Under penalties of perjury, I declare that:

• I am authorized to represent the taxpayer identified in Section 1 for the matter(s) specified in Section 3 of this form; and

•I am one of the following (indicate all thatapply):

1.An

2.A certified public accountant duly qualified to practice in the jurisdiction indicated below.

3.Enrolled as an agent to practice before the Internal Revenue Service under the requirements of Circular 230.

4.A registered public accountant.

Designation – use number(s) from above list

(1 - 4)

Licensing jurisdiction (state) or other licensing authority (if applicable)

Bar, license, certification,

registration, or enrollment number

Signature

Date

Form |

Page 3 |

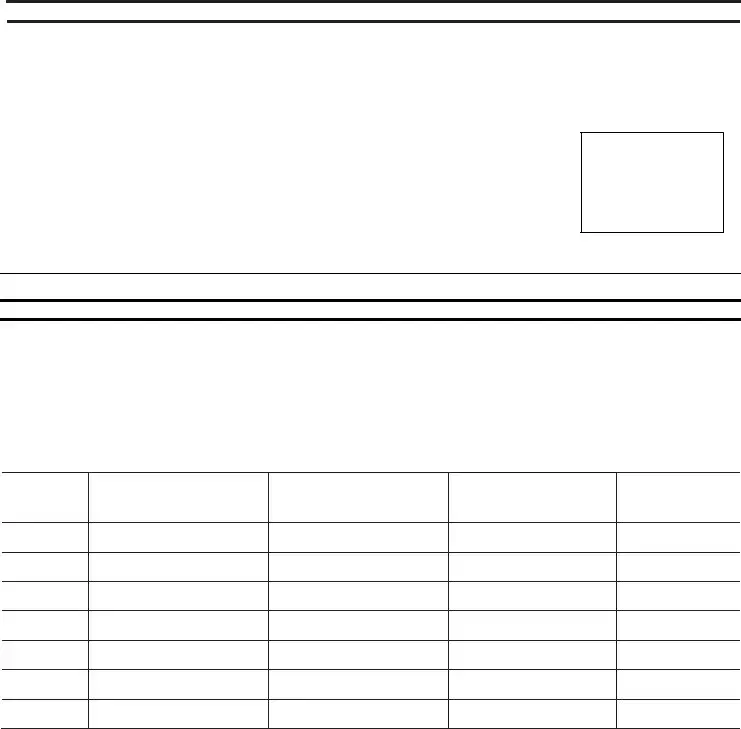

Purpose of Form

A taxpayer may use Form

Filing Instructions

Taxpayers should submit Form

To upload to GTC: (1) Login, (2) Under “I Want To” select “See More Links”, (3) Select “Submit Power of Attorney", and (4) Follow the prompts to upload the Form

Revocation

If you have a valid Form

If the taxpayer or representative merely wants to revoke an existing authorization, upload a copy of the previously executed Form

Specific Instructions

Section 1 – Taxpayer Information

Enter the name, address, and contact information of the taxpayer. If the taxpayer is an individual, enter the full Social Security number (SSN). If the taxpayer is a business entity, enter the Federal Employer Identification Number (FEIN). If the taxpayer is granting access to a joint return, enter the spouse’s name, address, and full SSN.

Section 2 – Representative Information

Enter the representatives’ names, addresses and any applicable contact information. A representative must be an individual, not a business entity. If designating authority to more than two representatives, please attach a schedule similar in form to Section 2 signed by the taxpayer.

Section 3 – Tax Matters

Enter the tax type(s) and specific period(s) or year(s) for which the authorization is being granted. The Department will only discuss and/or disclose taxpayer information for the type(s) and period(s) listed. Notices and communications will be sent to the taxpayer, not the representative. The representative may access copies of taxpayer notices and communications via third party access to the taxpayer’s account through GTC.

Form |

Page 4 |

Section 4 – Retention/Revocation of Prior Power(s) of Attorney

All existing Form

Section 5 – Taxpayer Authorization and Signature

The taxpayer must sign in Section 5 for Form

Taxpayer |

Who Must Sign |

|

|

|

|

Individuals |

The individual/sole proprietor must sign (if granting access to a joint return, |

|

spouse must also sign). |

||

|

||

Corporations |

A corporate officer with authority to sign. |

|

|

|

|

Partnerships |

A partner having authority to act in the name of the partnership must sign. |

|

|

|

|

Limited Liability |

A member having authority to act in the name of the company must sign. |

|

Companies |

||

|

||

Trusts |

A trustee must sign. |

|

|

|

|

Estates |

An executor/executrix or the personal representative of the estate must sign. |

|

|

|

Section 6 – Acknowledgment of the Power of Attorney

This POA must be acknowledged by the taxpayer before a notary public, unless an appointed representative is an

Section 7 – Declaration of Representative

If an appointed representative is licensed to practice as an

| Fact Name | Description |

|---|---|

| Form Name | Tax Power of Attorney (POA) Form RD-1061 |

| Purpose | This form authorizes a designated individual to represent a taxpayer before the Department of Revenue. |

| Governing Law | The form is governed by the state’s taxation laws, particularly under state tax code provisions. |

| Eligibility | Any individual or entity may complete this form to grant representation authority. |

| Submission Method | The completed form can typically be submitted via mail or electronically, depending on state regulations. |

| Revocation | Taxpayers can revoke the power of attorney at any time by submitting a notice in writing. |

| Duration | The power of attorney remains in effect until revoked or the taxpayer passes away. |

| Scope of Authority | The agent can handle various tax matters, including filing returns and communicating with tax authorities. |

| Signatures Required | The form must be signed by the taxpayer and the designated representative, along with date of execution. |

Once you have the Tax POA Form RD-1061 ready, it's time to fill it out correctly. Completing this form allows you to authorize someone to act on your behalf regarding tax matters. Follow the steps below to ensure everything is filled out properly and submit it without any hassle.

After you submit the form, keep an eye out for any confirmation of acceptance from the tax authority. This will ensure your representative can act on your behalf smoothly when the need arises.

The Tax POA form RD-1061 is a Power of Attorney document specifically designed for taxpayers in the United States. This form allows individuals to authorize another person—often referred to as a representative—to handle tax-related matters on their behalf. Through the RD-1061, taxpayers can give permission for their appointed representatives to access their tax information, communicate with tax authorities, and act on their behalf in various tax matters.

Taxpayers have the option to designate a wide range of individuals as their representatives using the RD-1061 form. This can include tax professionals, like Certified Public Accountants (CPAs) or enrolled agents, as well as family members or trusted friends. It's important to choose someone who is knowledgeable about tax matters and can effectively advocate for the taxpayer's interests when dealing with tax authorities.

While the RD-1061 form grants considerable authority to the designated representative, there are limitations to be aware of:

Filling out the RD-1061 form involves several straightforward steps:

After completing the RD-1061 form, it should be submitted to the appropriate tax authority. For federal matters, this typically means filing with the Internal Revenue Service (IRS) or the state department of revenue, depending on the jurisdiction. It is advisable to keep a copy of the form for personal records. If the appointed representative will be dealing with specific tax authorities, they should be instructed to retain copies as well.

Filling out the Tax Power of Attorney (POA) form RD-1061 can be a straightforward process, but many individuals encounter common mistakes that can lead to complications. Understanding these errors can help ensure that the form is completed correctly and submitted without issues. One prevalent mistake is failing to provide all required signatures. In many cases, individuals overlook the necessity of including both the taxpayer's and the representative's signatures. This omission can result in delays and might even lead to rejection of the form.

Another frequent error involves incorrect identification of the representative. It is essential to ensure that the person's name, address, and contact information are entered accurately. Misplacing a letter or providing outdated information can create confusion, making it difficult for the tax authorities to reach your representative when needed. It is critical to double-check these details before submission to maintain clear communication with the IRS.

Individuals often forget to specify the tax matters that the Power of Attorney covers. Leaving this section blank or vaguely defined may lead to limitations on what the representative is authorized to handle. Clearly outlining the specific tax years or types of tax issues can prevent misunderstandings later. Correctly identifying these matters can empower your representative and streamline the resolution of any pending issues with the IRS.

Finally, many people neglect to keep a copy of the completed RD-1061 form for their personal records. Having a copy readily available is vital for tracking what was submitted and for reference during future communications with the tax authorities. Without documentation of submission, individuals may face challenges in proving who was authorized to act on their behalf at a later date. Taking these steps can significantly improve the effectiveness of the Tax POA process.

When handling matters related to tax representation, certain forms and documents are commonly used alongside the Tax POA form RD-1061. These documents help ensure a smooth and efficient process when dealing with tax issues.

Understanding these forms can aid in the navigation of tax-related processes and ensure that representation is by the appropriate individuals for efficient resolution.

The Tax Power of Attorney (POA) form RD-1061 is an important document that allows individuals to authorize someone else to represent them in tax matters. The following documents share similarities with the RD-1061 form in terms of purpose and function:

When filling out the Tax POA (Power of Attorney) form RD-1061, there are important steps to follow to ensure accuracy and compliance. Below are essential dos and don'ts to keep in mind:

The Tax POA form RD-1061 is an important document used by taxpayers to designate someone to represent them before the tax authorities. Unfortunately, several misconceptions about this form can lead to confusion. Here’s a look at eight common misunderstandings:

Awareness of these misconceptions can help taxpayers navigate their tax representation more effectively. It's essential to understand the purpose and implications of the Tax POA form to ensure proper use and avoid pitfalls.