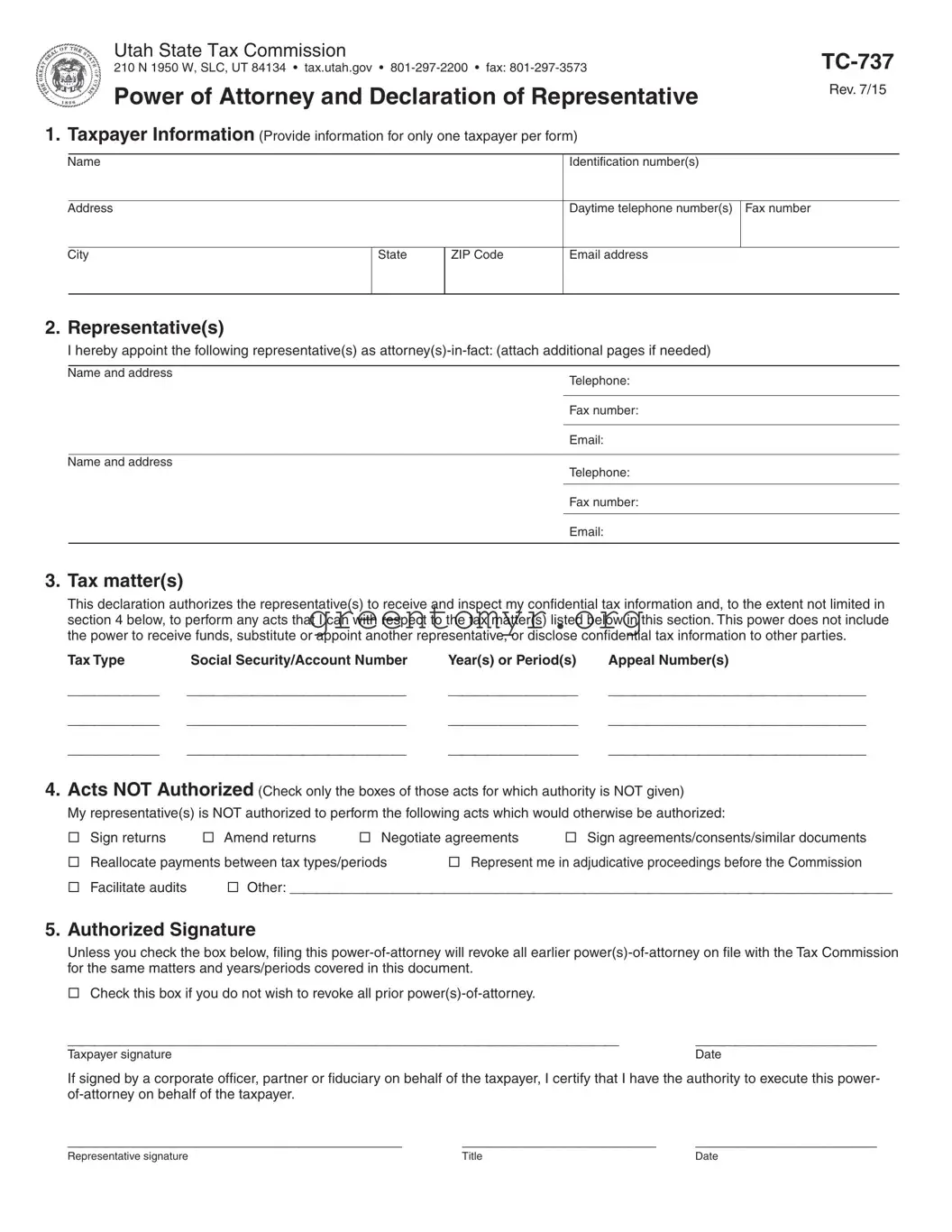

When it comes to managing tax-related matters, understanding the Tax Power of Attorney (POA) form TC-737 can simplify the process for both individuals and their authorized representatives. This form allows a taxpayer to designate someone, such as a family member or a professional tax preparer, to act on their behalf in communications with the tax authorities. The TC-737 enables this appointed agent to receive confidential tax information, file returns, and make representations regarding tax liabilities and disputes. Importantly, it provides a way for taxpayers to retain control over their tax matters while leveraging the expertise of someone trusted. It's crucial to complete the form accurately, as it outlines the extent of the agent's authority and ensures compliance with tax regulations. By understanding the purpose and implications of the TC-737, people can navigate their tax responsibilities more effectively and with greater peace of mind.

Utah State Tax Commission |

|

210 N 1950 W, SLC, UT 84134 tax.utah.gov |

|

Power of Attorney and Declaration of Representative |

Rev. 7/15 |

|

|

1. Taxpayer Information (Provide information for only one taxpayer per form) |

|

Name

Identification number(s)

Address

Daytime telephone number(s) Fax number

City

State

ZIP Code

Email address

2. Representative(s)

I hereby appoint the following representative(s) as

Name and address

Name and address

Telephone:

Fax number:

Email:

Telephone:

Fax number:

Email:

3. Tax matter(s)

This declaration authorizes the representative(s) to receive and inspect my confidential tax information and, to the extent not limited in section 4 below, to perform any acts that I can with respect to the tax matter(s) listed below in this section. This power does not include the power to receive funds, substitute or appoint another representative, or disclose confidential tax information to other parties.

Tax Type |

Social Security/Account Number |

Year(s) or Period(s) |

Appeal Number(s) |

_______ |

_________________ |

__________ |

____________________ |

_______ |

_________________ |

__________ |

____________________ |

_______ |

_________________ |

__________ |

____________________ |

4.Acts NOT Authorized (Check only the boxes of those acts for which authority is NOT given)

My representative(s) is NOT authorized to perform the following acts which would otherwise be authorized:

|

Sign returns |

Amend returns |

Negotiate agreements |

Sign agreements/consents/similar documents |

|

|

Reallocate payments between tax types/periods |

Represent me in adjudicative proceedings before the Commission |

|||

Facilitate audits Other: _______________________________________________

5.Authorized Signature

Unless you check the box below, filing this

Check this box if you do not wish to revoke all prior

___________________________________________ |

______________ |

Taxpayer signature |

Date |

If signed by a corporate officer, partner or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power-

__________________________ _______________ ______________

Representative signature |

Title |

Date |

| Fact Name | Details |

|---|---|

| Purpose | The Tax POA Form TC-737 allows individuals to grant power of attorney to someone else to handle tax-related matters on their behalf in the state of Utah. |

| Governing Law | This form is governed by the Utah State Tax Commission rules and regulations. |

| Who Can Act | Any adult individual, attorney, or tax professional can be designated to act on behalf of the taxpayer as stated in the form. |

| Signing Requirements | The taxpayer must sign the form, indicating their consent for the representative to act on their behalf. |

| Revocation | Authority granted by the TC-737 can be revoked at any time by submitting a written notice to the Tax Commission. |

| Submission Method | The completed form must be submitted to the Utah State Tax Commission, either by mail or electronically, depending on specific guidelines. |

When filling out the Tax POA form TC-737, it's essential to address each section accurately to ensure that your tax matters are handled correctly. After completing the form, you will need to submit it to the appropriate tax authority, ensuring that you follow any additional requirements that may apply to your specific situation.

The Tax Power of Attorney Form TC-737 is a legal document that allows an individual to authorize another person to represent them in matters involving tax issues with the IRS or state tax agencies. This form enables the designated representative to receive and inspect confidential tax information, submit documents and manage tax obligations on behalf of the signatory.

You can designate anyone as your representative on the TC-737 form, provided they are competent to act on your behalf. This may include tax professionals, family members, or friends. Importantly, the person you choose must agree to accept the responsibilities involved in managing your tax matters. It is wise to select someone who is knowledgeable about tax laws and the intricacies of forms and procedures.

Filling out the TC-737 form involves several key steps:

After completing the TC-737 form, you should submit it to the appropriate tax authority. This can vary depending on whether it's for federal or state purposes. For federal representation, send it directly to the IRS at the address indicated in the form instructions. For state representation, refer to your state’s tax agency website for the correct submission guidelines.

Yes, you can revoke the authority granted to a representative at any time. To do this, you must complete a revocation form or simply notify the tax authority in writing that you no longer wish for the designated person to act on your behalf. It is recommended to provide clear details and ensure that your revocation is acknowledged by the relevant tax authority to prevent any unauthorized actions.

When individuals fill out the Tax Power of Attorney (POA) form TC-737, they may encounter several common pitfalls that can lead to complications in the future. Understanding these mistakes can enhance the efficiency of the process and help avoid unnecessary delays or issues with the tax authorities.

One prevalent mistake is neglecting to provide the necessary personal information. Taxpayers must ensure that both their details and those of the person they are designating as their representative are accurately filled in. This includes full names, addresses, and social security numbers. Omitting even a single digit or letter can cause issues with identification.

Additionally, selecting the wrong type of authority is another frequent error. The TC-737 form allows taxpayers to grant various types of powers. It’s vital that individuals clearly indicate whether they want to grant full power or limited authority. Choosing the incorrect option can prevent the designated representative from performing certain necessary tasks.

Another common mistake occurs when individuals forget to sign and date the form. A signature is a critical component that validates the document. Without it, the form is considered incomplete and may not be accepted by tax authorities. Moreover, failing to date the form can create confusion about its timeliness, which is important for any legal processes involved.

Inaccurate or incomplete information about the tax year can also lead to complications. The TC-737 form requires specific reference to the tax years or periods for which the power is granted. Omitting this information, or mistakenly including incorrect years, can limit the representative's effectiveness in managing tax matters for the taxpayer.

People might also overlook the necessity of checking for conflicts of interest. For instance, if a designated representative has a personal relationship with the taxpayer that might bias their representation, it should be reconsidered. Ensuring transparency and trust is essential for all parties involved.

Failing to understand the consequences of the powers granted can create challenges as well. Taxpayers should be fully aware that they are giving their representative the authority to act on their behalf, which can include making significant decisions. This understanding ensures that all parties are on the same page and reduces the risk of future disputes.

Lastly, individuals often do not keep a copy of the completed TC-737 form for their records. Retaining a copy is crucial, as it serves as verification of the powers granted and supports any inquiries or disputes that may arise in the future. Having this documentation can be invaluable, especially if questions about authority come up later.

When managing tax matters, particularly when using the Tax Power of Attorney (POA) form TC-737, several other forms and documents often accompany it. Understanding these documents can help streamline communication with tax authorities and ensure compliance. Here is a list of commonly used forms alongside the TC-737:

Using the correct forms and understanding their purposes can facilitate tax filing and ensure optimal compliance with the IRS. Each document plays a unique role in managing tax obligations and can be critical in specific situations. Always consider consulting a tax professional when navigating these forms for personalized advice and guidance.

When filling out the Tax POA form TC-737, it is essential to follow certain guidelines. This will help ensure your submission is accurate and accepted promptly. Here are four things you should and shouldn't do:

The Tax Power of Attorney (POA) form TC-737 can be misunderstood in several ways. Here are nine common misconceptions, along with clear explanations:

Understanding these misconceptions helps ensure that taxpayers make informed decisions regarding the Tax POA form TC-737 and their tax representation.

Understanding the Tax POA form tc-737 is essential for effectively managing tax matters. This form allows taxpayers to designate a representative to act on their behalf before the tax authorities. Here are some key takeaways for filling out and using this form:

Using the Tax POA form tc-737 correctly can facilitate smoother communication with tax authorities and ensure that your interests are protected.