The IRS Form 2848, also known as the Power of Attorney and Declaration of Representative, serves a crucial role in tax-related matters between taxpayers and the IRS. This form allows taxpayers to designate an individual, usually a tax professional, to represent them before the IRS regarding specific tax issues. When you complete and submit the 2848, you give your chosen representative the authority to act on your behalf, which may include receiving confidential information, negotiating settlements, and communicating directly with the IRS. It’s essential to specify the types of tax issues and tax years that the authority covers, as this form is not a blanket authorization; rather, it is tailored to particular circumstances. By correctly filling out this document, taxpayers can ensure that they are supported in their dealings with the IRS, ultimately making a potentially stressful process more manageable and organized.

REVENUe ____________________

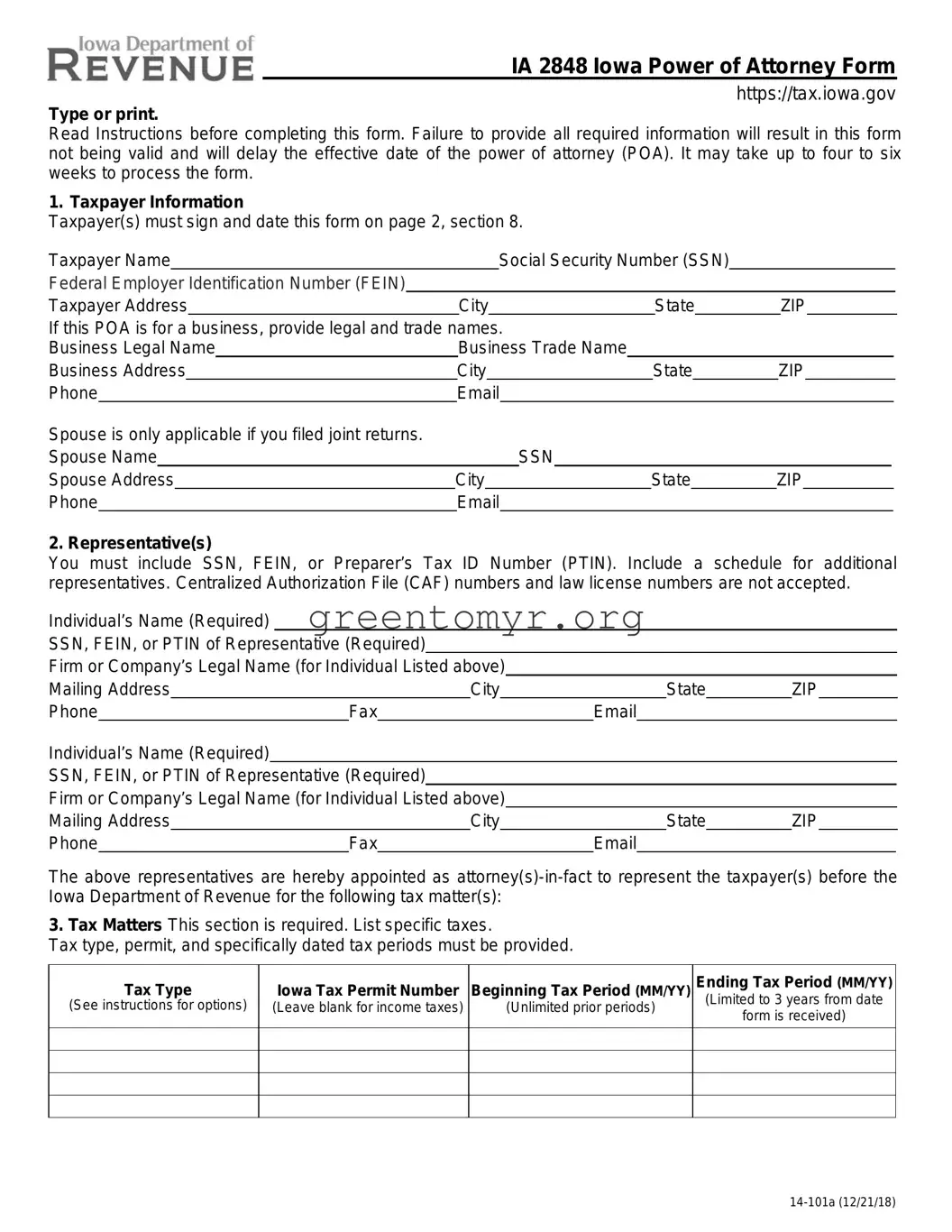

IA 2848 Iowa Power of Attorney Form

https://tax.iowa.gov

Type or print.

Read Instructions before completing this form. Failure to provide all required information will result in this form not being valid and will delay the effective date of the power of attorney (POA). It may take up to four to six weeks to process the form.

1. Taxpayer Information

Taxpayer(s) must sign and date this form on page 2, section 8.

Taxpayer Name |

|

|

Social Security Number (SSN) |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Federal Employer Identification Number (FEIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Taxpayer Address |

City |

State |

|

ZIP |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

If this POA is for a business, provide legal and trade names. |

|

|

|

|

|

|

|||||||||||||

Business Legal Name |

Business Trade Name |

|

|

|

|

|

|

||||||||||||

Business Address |

|

City |

|

State |

|

ZIP |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Phone |

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Spouse is only applicable if you filed joint returns. |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Spouse Name |

|

|

SSN |

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Spouse Address |

City |

State |

|

ZIP |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Phone |

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. Representative(s)

You must include SSN, FEIN, or Preparer’s Tax ID Number (PTIN). Include a schedule for additional representatives. Centralized Authorization File (CAF) numbers and law license numbers are not accepted.

Individual’s Name (Required)

SSN, FEIN, or PTIN of Representative (Required)

Firm or Company’s Legal Name (for Individual Listed above)

Mailing Address |

|

|

|

City |

|

|

State |

ZIP |

||||

Phone |

|

Fax |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Individual’s Name (Required)

SSN, FEIN, or PTIN of Representative (Required)

Firm or Company’s Legal Name (for Individual Listed above)

Mailing Address |

|

|

|

City |

|

|

State |

ZIP |

||||

Phone |

|

Fax |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

The above representatives are hereby appointed as

3.Tax Matters This section is required. List specific taxes.

Tax type, permit, and specifically dated tax periods must be provided.

Tax Type |

Iowa Tax Permit Number |

Beginning Tax Period (MM/YY) |

(See instructions for options) |

(Leave blank for income taxes) |

(Unlimited prior periods) |

|

|

|

Ending Tax Period (MM/YY) (Limited to 3 years from date form is received)

IA 2848 Iowa Power of Attorney Form, page 2

4.Acts Authorized (Do not name additional representatives in this section.)

Representatives are authorized to receive and inspect confidential tax information and to perform any and all acts with respect to the tax matters described in section 3. For example, the representative may negotiate, sign any agreements, consents, or other documents, and represent the taxpayer(s) in any informal and formal proceeding involving the Department. See Instructions for full list of authorized activities. The authority does not include the power to receive refund checks, unless specifically added in section 5 below. List any specific additions or deletions to the acts otherwise authorized in this power of attorney:

Additions:

Deletions:

5. Receipt of Refund Checks

If you want to authorize a representative named in section 2 to receive, but not to endorse or cash, refund

checks, initial here |

|

and list the name of that representative below. |

Name of representative to receive refund check(s)

6. Notices and Communications

Original notices and other written communications will be sent to you and the taxpayer. A copy will be sent to the first representative listed in section 2.

7. Retention or Revocation of Prior Power(s) of Attorney

The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the Iowa Department of Revenue for the same tax matters and tax periods covered by this document.

If you do not want to revoke a prior power of attorney, check here □

You must attach a copy of any power of attorney you want to remain in effect.

8. Signature of Taxpayer(s)

If a tax matter concerns a joint individual income tax return, both spouses are required to sign this form, if represented by the same individual(s).

If signed by a corporate officer, partner, member, guardian, tax matters partner, executor, receiver, administrator, or trustee on behalf of the taxpayer: I certify that I have the authority to execute this form on behalf of the taxpayer.

If the taxpayer is an entity with more than one owner or member, a second signature of a person authorized to legally bind the entity is required.

If this form is not signed and dated, this power of attorney will not be valid. The form will be returned to you.

Signature ______________________________ |

Date |

____________________________________ |

|

Print Name |

____________________________ |

Title _____________________________________ |

|

Signature ______________________________ |

Date |

____________________________________ |

|

Print Name |

____________________________ |

Title _____________________________________ |

|

Mail to:

Registration Services

Iowa Department of Revenue

PO Box 10470

Des Moines IA

Or fax to:

Purpose of form

Taxpayer information is confidential. The Iowa Department of Revenue will discuss confidential tax information only with the taxpayer, unless the taxpayer has a valid power of attorney form on file with the Department.

A power of attorney is required by the Department when the taxpayer wishes to authorize another person to perform one or more of the following on behalf of the taxpayer:

a. To receive copies of notices or documents sent by the Department, its representatives, or its attorneys.

b. To receive (but not to endorse and collect) checks in payment of any refund of Iowa taxes, penalties, or interest.

c. To request waivers (including offers of waivers) of restrictions on assessment or collection of tax deficiencies and waivers of notice of disallowance of a claim for credit or refund.

d. To request extensions of time for assessment or collection of taxes.

e. To fully represent the taxpayer(s) in any formal or informal meeting with the Department, hearing, determination, final or otherwise, or appeal.

f.To enter into any compromise with the Department.

g.To execute any release from liability required by the Department before divulging otherwise confidential information concerning taxpayer(s).

h.Other acts as expressly stipulated in writing by the taxpayer.

3.Tax Matters

Tax type options

Enter tax type in section 3 and include beginning and ending dates for each. Valid tax types are: Individual Income, Partnership, Corporation, Sales, Use, Withholding, Franchise, Inheritance, Fiduciary, or Other (specify).

Tax periods

Specific tax periods must be identified. Each tax period must be separately stated.

Beginning tax period

An unlimited number of prior tax periods is allowed.

Ending tax period

An

7.Retention / Revocation of prior Power(s) of Attorney Canceling a power of attorney

A power of attorney may be revoked by a taxpayer at any time by filing a statement of revocation with the Department. The statement must indicate that the authority of the previous power of attorney is revoked and must be signed and dated by the taxpayer. Also, the name and address of each representative whose authority is revoked must be listed or a copy of the power of attorney must be included. Revocation of the authority to represent the taxpayer before the Department will be effective on the date received by the Department.

IA 2848 Iowa Power of Attorney Instructions

Submitting a new power of attorney

A new power of attorney for a particular tax type(s) and tax period(s) revokes a prior power of attorney for those tax type(s) and tax period(s), unless the taxpayer indicates on the new power of attorney form that a prior power of attorney is to remain in effect. The effective date of a new power of attorney is the date it is received by the Department.

For a

Withdrawing as a representative

A representative may withdraw from representing a taxpayer by filing a statement with the Department. The statement must be signed and dated by the representative and must identify the name and address of the taxpayer(s) and the matter(s) from which the representative is withdrawing.

8.Signature of Taxpayer(s) Who must sign?

Individual taxpayer. A power of attorney form must be signed by the individual.

Joint returns. If a tax matter concerns a joint individual income tax return, both taxpayers must sign and date.

Corporation. An officer of the corporation having authority to legally bind the corporation must sign the power of attorney form. The corporation must certify that the officer has such authority.

Association. An officer of the association having authority to legally bind the association must sign the power of attorney form. The association must certify that the officer has such authority.

Partnership. A power of attorney must be signed by all partners, or if executed in the name of the partnership, by the partner or partners duly authorized to act for the partnership, who must certify that the partner(s) has such authority.

Federal Power of Attorney

The Federal Power of Attorney form or a Military Power of Attorney is accepted by the Iowa Department of Revenue. To be valid, the federal or military form must include a statement that it is applicable for Iowa purposes at the time it is executed. In the case of a previously executed Federal or Military Power of Attorney subsequently revised to apply for Iowa purposes, it must contain a written statement that indicates it is being submitted for use with State of Iowa forms and the statement needs to be initialed by the taxpayer. Iowa allows married taxpayers to file one Iowa Power of Attorney form on behalf of both spouses. The IRS requires separate Power of Attorney forms for each spouse. If the Federal Power of Attorney is being used for Iowa purposes by married taxpayers, both federal forms must be submitted to Iowa.

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 2848, also known as Power of Attorney and Declaration of Representative, allows an individual to appoint a representative to act on their behalf regarding tax matters. |

| Eligibility | Any U.S. citizen or resident alien can use Form 2848 to designate a representative. |

| Designated Representative | The representative must be an individual, a tax professional, or another person with proper authority to act on the taxpayer's behalf. |

| Representatives’ Authority | The appointed representative can receive confidential tax information and represent the taxpayer before the IRS for specified matters. |

| State Forms | Some states have their own Power of Attorney forms, such as California's Form FTB 3520, governed by California Revenue and Taxation Code. |

| Filing Method | Form 2848 must be signed by both the taxpayer and the representative and submitted to the IRS. It can be submitted electronically or by mail. |

| Expiration | Form 2848 remains in effect until revoked by the taxpayer or when the representative cannot continue to represent the taxpayer. |

| Multiple Representatives | Taxpayers can appoint multiple representatives by listing them on the same Form 2848, ensuring clarity on their roles. |

| Limitations | The power granted by Form 2848 is limited to tax matters. It does not authorize representatives for non-tax issues. |

| Revocation Process | Taxpayers can revoke a Power of Attorney by submitting a written statement to the IRS, effectively terminating the authority of the representative. |

Filling out the Tax Power of Attorney (POA) Form 2848 can be a straightforward process. Once completed, this form allows you to designate a representative to handle your tax matters with the IRS. Follow the steps below carefully to ensure you provide all necessary information.

The Tax Power of Attorney (POA) Form 2848 is a document authorized by the Internal Revenue Service (IRS). It allows taxpayers to appoint someone else, often referred to as an agent, to represent them in tax matters. This representation can include interactions with the IRS regarding tax returns, tax liabilities, and audits. By filing Form 2848, taxpayers can grant their chosen representative the authority to receive confidential information, discuss their tax issues, and act on their behalf. This can be particularly useful if a taxpayer requires assistance navigating complex tax situations or simply wants to ensure their rights are protected.

Individuals eligible to act as an agent on Form 2848 include:

It is important to note that the representative must have valid credentials or professional status recognized by the IRS. However, a family member or friend without proper credentials can also be designated, but they may have limited authority and access compared to qualified professionals.

Completing Form 2848 requires careful attention to detail. The process involves several steps:

Once completed, you can submit Form 2848 either by mailing it to the appropriate IRS address or, in certain cases, by faxing it. Always check the current submission guidelines on the IRS website, as they may change over time.

Yes, you can revoke the Power of Attorney at any time. To do so, you must submit a written notice to the IRS, stating your intention to revoke the authority of the designated agent. You may also consider filing a new Form 2848 if you wish to appoint a different representative. It is advisable to notify the former agent about the revocation as a courtesy. The IRS will process your revocation, effectively ending the agent's power to act on your behalf in tax matters.

When filling out the IRS Form 2848, many individuals make common mistakes that can delay processing or lead to complications. Understanding these errors is crucial for effective communication with the IRS.

One frequent mistake is failing to provide specific details about the taxpayer. Ensure that the name, address, and Social Security Number (SSN) are accurate and consistent. Even minor discrepancies can cause delays.

Another common error relates to the signature. Many people neglect to sign the form. Without a signature, the IRS will not process the Power of Attorney, potentially leaving your case unresolved.

Additionally, some individuals overlook the importance of specifying the tax matters for which they are granting authority. Clearly indicate the type of taxes and tax years involved to prevent confusion and ensure that the representative can act effectively.

Missing the designated dates is another area where mistakes occur. Practitioners often forget to include the start and end dates for the authority granted. Unclear date ranges can lead to misunderstandings about the scope of representation.

People sometimes also fail to identify the representative correctly. Ensure that both the name and credentials of the appointed individual are correctly filled out. Errors here can lead to unauthorized representatives, which can complicate your case.

Another mistake is not keeping a copy of the submitted form. Always retain a copy for your records. This will be essential if issues arise or if the IRS has questions regarding your authorization.

Lastly, individuals often do not follow the correct submission method. Whether sending by postal mail or electronically, ensure that you are using the method as specified by the IRS guidelines. This step is necessary to avoid unnecessary delays in processing.

The IRS Form 2848, or Power of Attorney and Declaration of Representative, allows individuals to appoint someone to represent them before the IRS. When filing this form, there are several other documents and forms that may complement the POA. These documents can streamline communication and ensure that all relevant information is available to the representative. Below is a list of frequently used forms and documents that often accompany the Form 2848.

Using these additional documents in conjunction with Form 2848 ensures that the appointed representative has access to all necessary information and the authorizations needed to assist effectively. This collaborative approach helps streamline the taxpayer's experience with the IRS and ensures compliance with all relevant tax obligations.

When completing the Tax Power of Attorney (POA) Form 2848, attention to detail can make a significant difference. Here are five essential dos and don’ts to consider.

The IRS Form 2848, also known as the Power of Attorney (POA), is often misunderstood. Here are six common misconceptions surrounding this important form.

Many individuals believe that only certified tax professionals can complete this form. In reality, anyone can fill it out as long as they understand the information required and the role of the person designated as the representative.

This is not accurate. When you sign Form 2848, you are granting authority to your representative, but you retain the right to revoke this authority at any time and still have the final say in your tax decisions.

Form 2848 does not expire automatically each year. Once it is valid, it remains in effect until revoked, the representative is changed, or the case is completed. However, a new form may be needed if there are changes in your Representative’s authorization, such as a shift in their status or the type of representation.

This is incorrect. You can designate multiple representatives on the same form. Each representative can be assigned a specific role or responsibility regarding your tax matters, allowing for more flexibility.

The IRS does not send a confirmation once they receive the form. It is the taxpayer's responsibility to ensure that it was submitted correctly and to keep a copy for their records.

While Form 2848 is primarily associated with tax matters, it can also authorize your representative to act on your behalf in various IRS-related proceedings, including appeals and audits.

Filling out and using the Tax Power of Attorney form, also known as IRS Form 2848, is a significant step for individuals seeking to authorize someone to represent them before the IRS.