The Tax Power of Attorney (POA) LGL 001 form serves as a vital tool for individuals and businesses alike, enabling them to appoint a representative to handle tax matters on their behalf. This form is particularly useful during tax season when complexities can arise, and assistance becomes invaluable. By designating a representative through this documented agreement, taxpayers ensure that their interests are adequately represented with tax authorities. The form not only outlines the specific powers granted to the appointed representative but also specifies the types of tax matters covered, including filing returns, receiving tax information, and negotiating with the Internal Revenue Service (IRS). Additionally, it includes necessary details such as the taxpayer's information and the representative's credentials, ensuring that all parties involved have a clear understanding of the authority being conferred. Completing the Tax POA LGL 001 form correctly helps streamline communication between the taxpayer and the IRS, thereby reducing potential misunderstandings and enhancing the overall efficiency of tax-related processes.

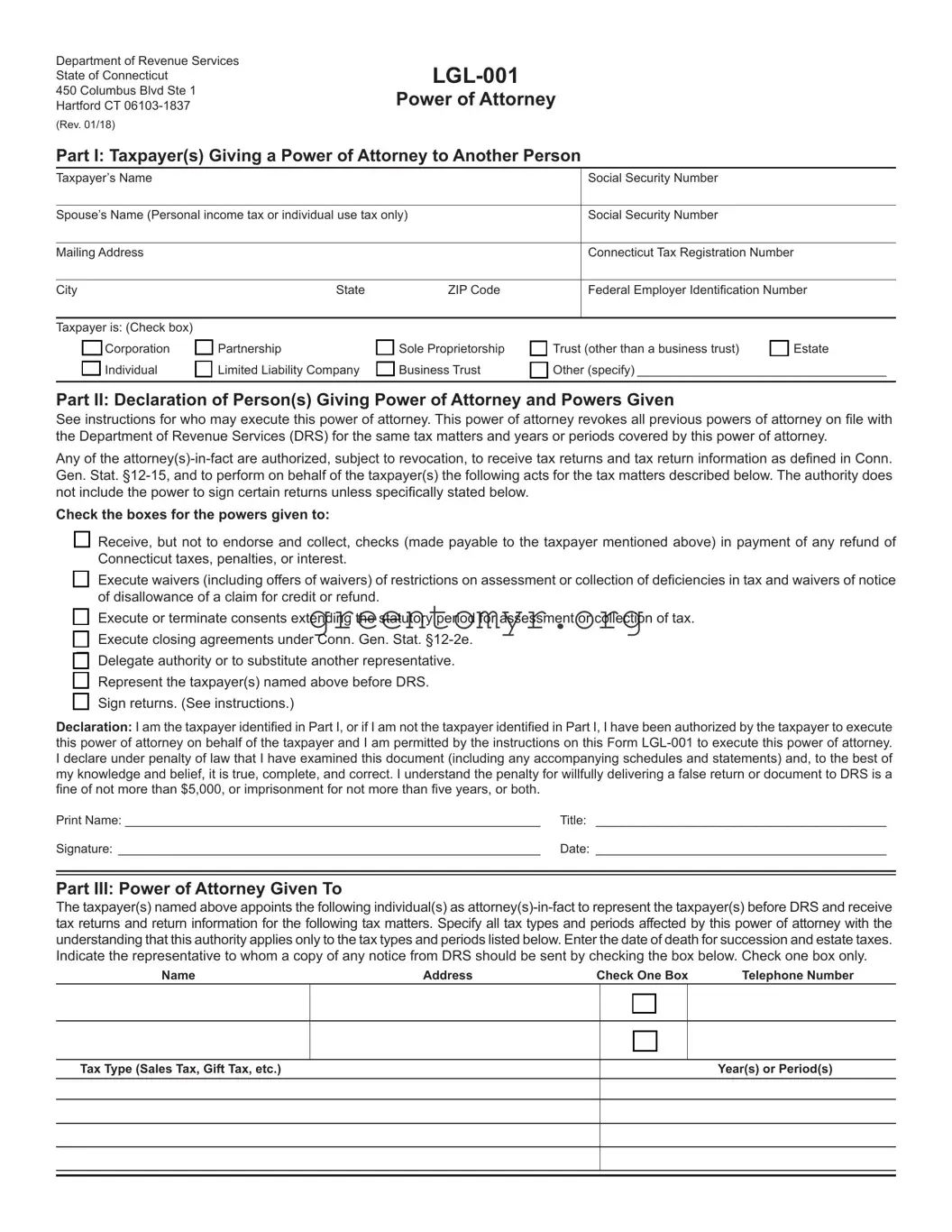

Department of Revenue Services State of Connecticut

450 Columbus Blvd Ste 1 Hartford CT

(Rev. 01/18)

Power of Attorney

Part I: Taxpayer(s) Giving a Power of Attorney to Another Person

Taxpayer’s Name |

|

|

Social Security Number |

|

|

|

|

Spouse’s Name (Personal income tax or individual use tax only) |

|

Social Security Number |

|

|

|

|

|

Mailing Address |

|

|

Connecticut Tax Registration Number |

|

|

|

|

City |

State |

ZIP Code |

Federal Employer Identification Number |

|

|

|

|

Taxpayer is: (Check box) |

|

|

|

|

Corporation |

Partnership |

Sole Proprietorship |

Trust (other than a business trust) |

Estate |

Individual |

Limited Liability Company |

Business Trust |

Other (specify) ____________________________________ |

|

|

|

|

|

|

Part II: Declaration of Person(s) Giving Power of Attorney and Powers Given

See instructions for who may execute this power of attorney. This power of attorney revokes all previous powers of attorney on file with the Department of Revenue Services (DRS) for the same tax matters and years or periods covered by this power of attorney.

Any of the

Check the boxes for the powers given to:

Receive, but not to endorse and collect, checks (made payable to the taxpayer mentioned above) in payment of any refund of Connecticut taxes, penalties, or interest.

Execute waivers (including offers of waivers) of restrictions on assessment or collection of deficiencies in tax and waivers of notice of disallowance of a claim for credit or refund.

Execute or terminate consents extending the statutory period for assessment or collection of tax. Execute closing agreements under Conn. Gen. Stat.

Delegate authority or to substitute another representative. Represent the taxpayer(s) named above before DRS. Sign returns. (See instructions.)

Declaration: I am the taxpayer identified in Part I, or if I am not the taxpayer identified in Part I, I have been authorized by the taxpayer to execute this power of attorney on behalf of the taxpayer and I am permitted by the instructions on this Form

Print Name: ____________________________________________________________ |

Title: __________________________________________ |

Signature: _____________________________________________________________ |

Date: __________________________________________ |

Part III: Power of Attorney Given To

The taxpayer(s) named above appoints the following individual(s) as

Name |

Address |

Check One Box |

|

Telephone Number |

||

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

Tax Type (Sales Tax, Gift Tax, etc.) |

|

|

|

|

|

Year(s) or Period(s) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Instructions

Use

Connecticut law stipulates that all official mailings will be sent to the taxpayer of record at the address on file with DRS. As a matter of policy, DRS also provides taxpayers with the right to have a copy of any notice sent to its counsel or other qualified representative who has properly executed and filed this power of attorney with DRS for the type of tax and tax period that is the subject of the notice. This power of attorney does not change the requirement that DRS send all official mailings directly to the taxpayer.

Part I: Taxpayer(s) Giving a Power of Attorney to Another Person

Provide the taxpayer’s name and address and either your Social Security Number (SSN) or Connecticut Tax Registration Number and Federal Employer Identification Number. If you are a sole proprietor, enter your name and SSN. Do not enter your trade name. Do not use your representative’s address as your own.

Your spouse’s name is not required except for joint personal income tax or individual use tax returns.

If you are filing a joint personal income tax return and you and your spouse have the same representative(s), include your spouse’s name and SSN in the space provided. Otherwise, each spouse must file a separate

Check the box that describes the taxpayer.

Part II: Declaration of the Person Giving Power of Attorney And Powers Given

Any person giving a power of attorney to another person(s) must sign this declaration and must check the box for each act being granted to the

Who may execute this power of attorney?

Any individual if the request is for an income tax return filed by that individual (or filed by that individual and his or her spouse if the request is for a joint income tax return);

Conn. Agencies Regs.

A limited liability company (LLC) member if the taxpayer is an LLC and has no manager or a manager if the taxpayer is an LLC and has managers

The sole proprietor if the taxpayer is a sole proprietorship;

A general partner if the taxpayer is a partnership or a limited partnership;

The administrator or executor if the taxpayer is an estate;

The trustee if the taxpayer is a trust;

If the taxpayer is a corporation, a principal officer or corporate officer (who has legal authority to bind the corporation), any

person who is designated by the board of directors or other governing body of the corporation, any officer or employee of the corporation upon written request signed by a principal officer of the corporation and attested to by the secretary or other officer of the corporation, or any other person who is authorized to receive or inspect the corporation’s return or return information under I.R.C. §6103(e)(1)(D);

The successor, receiver, guarantor, or any assignee of the taxpayer; or

The authorized representative of any of the above.

Part III: Power of Attorney Given To

Provide the name, address, and telephone number of the person(s) designated by you to be your

Enter the tax type and the tax periods or tax years that are the subject of this power of attorney. Be specific about the type of tax at issue (refer to the following examples):

Withholding tax;

Income tax;

Sales and use taxes;

Corporation business tax;

Admissions and dues tax;

Estate tax;

Gift tax;

Motor vehicle fuels tax;

Gross earnings tax (petroleum, gas, hospital, community antenna);

Cigarette tax distributor; and

Individual use tax.

The terms years and periods can indicate various time frames.

A tax year may be a calendar year of 1/1/06 through 12/31/06 or a fiscal year of 7/1/06 through 6/30/07 for corporation tax. A tax period may have one or more monthly or quarterly periods.

Example: A sales and use tax period of 1/1/04 through 12/31/06 may contain 36 monthly or 12 quarterly periods.

Indicate the tax year(s) or tax period(s) to be covered by the power of attorney.

Where to File

Do not send an

Mail, fax, or deliver

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA lgl 001 form is used to grant power of attorney to individuals or entities, allowing them to represent taxpayers before tax authorities. |

| Governing Law | This form is governed by state tax laws, which vary by state. It's essential to check specific regulations applicable to your state. |

| Eligibility | Generally, taxpayers, including individuals and businesses, can complete the Tax POA lgl 001 form to designate a representative. |

| Submission Process | After completing the form, it must be submitted to the appropriate tax authority. Some states may require mail submission, while others allow electronic submission. |

| Revocation | Taxpayers can revoke the power of attorney at any time by filing a revocation form or informing the tax authority directly. |

| Expiration | The authority granted by the Tax POA lgl 001 form typically remains in effect until the taxpayer revokes it or until the matter for which it was filed is resolved. |

To successfully complete the Tax POA lgl 001 form, gather your personal information and ensure you have a clear understanding of who will act on your behalf. After filling out the form, submit it to the appropriate tax authority. Here's how to go about it:

The Tax POA lgl 001 form is a document that allows taxpayers in the United States to authorize someone else to represent them before tax authorities. This could be an accountant, attorney, or any other individual. By completing this form, you designate them as your Power of Attorney (POA) for tax matters.

You might need this form for several reasons:

You can appoint anyone you trust, as long as they are legally able to act on your behalf. This includes:

To complete the form, follow these steps:

Yes, once you have completed the form, you must submit it to the IRS or the relevant state tax agency. You can do this by mailing it directly to the agency or, in some cases, providing it to your representative to submit on your behalf.

Absolutely. You have the right to revoke the Tax POA lgl 001 form at any time. To do this, you will need to notify the representative and submit a formal revocation notice to the IRS or state tax agency. Ensure you follow the proper procedures to ensure the revocation is effective.

When filling out the Tax Power of Attorney (POA) form, individuals often overlook critical details that can lead to complications. One common mistake is failing to provide accurate information about the taxpayer. The name, address, and Social Security number should match exactly with what the IRS has on file. Inaccuracies in this basic information can result in delays or even denials of the authority granted in the form.

Another frequent error involves selecting the wrong representative. The person designated to act on your behalf must be a qualified individual, such as a licensed attorney or an enrolled agent. Those who fail to verify the qualifications of their chosen representative risk invalidating their Power of Attorney, which means important tax matters may remain unresolved.

In addition, individuals may neglect to sign the form. A lack of signature renders the document incomplete and unenforceable. Whether due to oversight or misunderstanding, forgetting to provide this essential authentication can lead to significant delays in tax matters.

Another pitfall arises when individuals do not use the latest version of the form. The IRS occasionally updates its forms, and using an outdated version could result in rejection of the submission. Always check that you are completing the most current form to avoid unnecessary complications.

People might also make errors regarding the scope of authority granted. The form allows taxpayers to specify the type of tax matters their representative can handle. Omitting particular powers or being too vague can lead to misunderstandings about what actions the representative is permitted to take.

A further mistake often occurs when individuals forget to include all necessary documentation. If more than one person is involved, such as in business entities, additional signatures or authorizations may be necessary. Incomplete submissions slow down the process and complicate the representation.

Another common misstep is overlooking the revocation of prior Powers of Attorney. If an individual has previously granted another representative authority, it is crucial to revoke that authorization explicitly on the new form. Failing to do so can lead to confusion, with two representatives potentially acting on conflicting information.

Some filers also misinterpret the duration of the Power of Attorney. It is critical to understand that the authority granted can be either temporary or permanent until explicitly revoked. Misjudgment in this area can lead to unwarranted actions by the representative after the taxpayer no longer intends for them to act on their behalf.

Additionally, when filling out the form, taxpayers may incorrectly assume that a faxed copy or scanned version will suffice. In most cases, the IRS requires a physical copy with original signatures. Submitting a non-compliant version could result in the form being disregarded altogether.

Lastly, a lack of follow-up is a prevalent mistake. After submitting the Tax POA form, it is wise to verify with the IRS that the request has been processed. Not doing so might lead to misunderstandings about whether the representative has been granted the authority they need to act, creating additional burdens for the taxpayer at a later date.

When dealing with tax matters, various forms and documents often accompany the Tax POA LGL 001 form. These documents help clarify authority, verify identity, and ensure proper representation. Below is a list of commonly used forms that may be necessary in conjunction with the Tax POA LGL 001 form.

These forms serve distinct purposes, yet they collectively contribute to effective communication with tax authorities. Being prepared with the appropriate documentation can streamline the process and provide clarity when managing tax-related issues.

When filling out the Tax POA lgl 001 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Below are five important steps to take and avoid:

The Tax POA lgl 001 form often raises questions and misconceptions. Understanding the truths behind these misconceptions can help you navigate the process more effectively. Here are five common misunderstandings:

Many believe that only certified professionals can use this form. In reality, any taxpayer can fill out the Tax POA lgl 001 form to authorize someone to represent them before the IRS.

Some think that by signing the form, they give their representative full control over all tax matters. The form can specify the exact scope of authority, limiting what the representative can do on your behalf.

There's a belief that submitting this form will increase your tax liability. The form does not alter your tax obligations; it simply allows someone else to manage your tax matters.

Many assume that after filing, the authorization is permanent. However, you can revoke the POA at any time by submitting a new form or a written notice to the IRS.

It is a common belief that you can only have one authorized representative. In fact, you can designate multiple representatives, allowing for flexibility in who can handle your tax issues.

When considering the Tax POA lgl 001 form, here are some key takeaways to keep in mind: