The Tax Power of Attorney (POA) Form 2848 serves as a vital tool for taxpayers who wish to authorize another individual, typically a tax professional or family member, to act on their behalf in tax matters. This form allows for a designated representative to receive confidential tax information, communicate with the IRS, and represent the taxpayer during audits or appeals. By completing this form, taxpayers can grant permission for a specific timeframe and for specific tax matters, ensuring clarity and focus on their intended actions. The form requires essential information about both the taxpayer and the appointed representative, including their respective identification details. Not only does it streamline communication with the IRS, but it also offers a way for individuals to manage their tax obligations more efficiently. Understanding the nuances of Form 2848 is crucial for anyone looking to delegate their tax responsibilities effectively and securely.

Form

Power of Attorney and

Declaration of Representative

Rev. 7/14

Massachusetts

Department of

Revenue

See separate instructions. Please print or type.

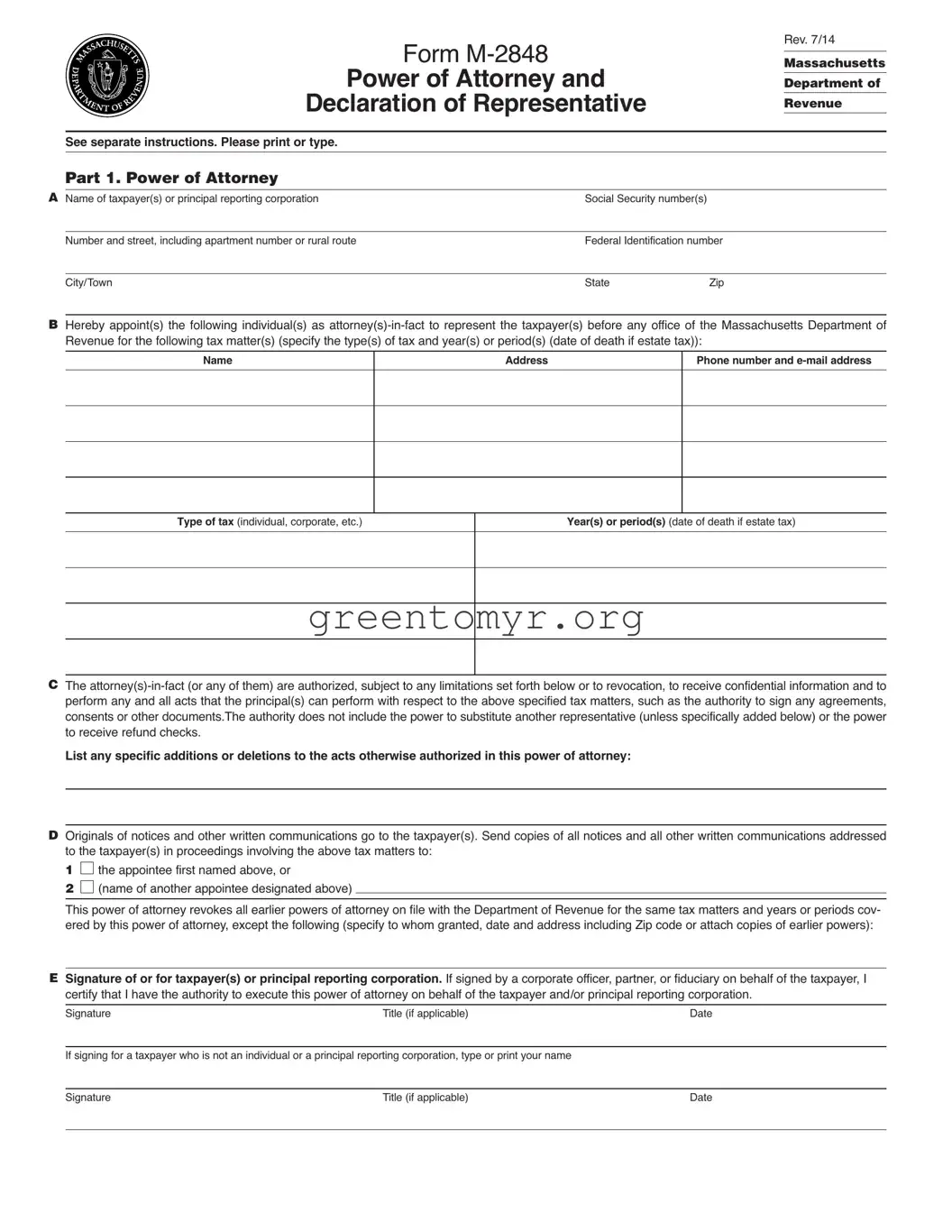

Part 1. Power of Attorney

A Name of taxpayer(s) or principal reporting corporation |

Social Security number(s) |

|

|

|

|

|

|

|

Number and street, including apartment number or rural route |

Federal Identification number |

|

|

|

|

|

|

City/Town |

State |

Zip |

BHereby appoint(s) the following individual(s) as

Name

Address

Phone number and

Type of tax (individual, corporate, etc.)

Year(s) or period(s) (date of death if estate tax)

CThe

List any specific additions or deletions to the acts otherwise authorized in this power of attorney:

DOriginals of notices and other written communications go to the taxpayer(s). Send copies of all notices and all other written communications addressed to the taxpayer(s) in proceedings involving the above tax matters to:

1 □

the appointee first named above, or

the appointee first named above, or

2 □

(name of another appointee designated above)

(name of another appointee designated above)

This power of attorney revokes all earlier powers of attorney on file with the Department of Revenue for the same tax matters and years or periods cov- ered by this power of attorney, except the following (specify to whom granted, date and address including Zip code or attach copies of earlier powers):

ESignature of or for taxpayer(s) or principal reporting corporation. If signed by a corporate officer, partner, or fiduciary on behalf of the taxpayer, I certify that I have the authority to execute this power of attorney on behalf of the taxpayer and/or principal reporting corporation.

Signature |

Title (if applicable) |

Date |

If signing for a taxpayer who is not an individual or a principal reporting corporation, type or print your name

Signature |

Title (if applicable) |

Date |

|

|

|

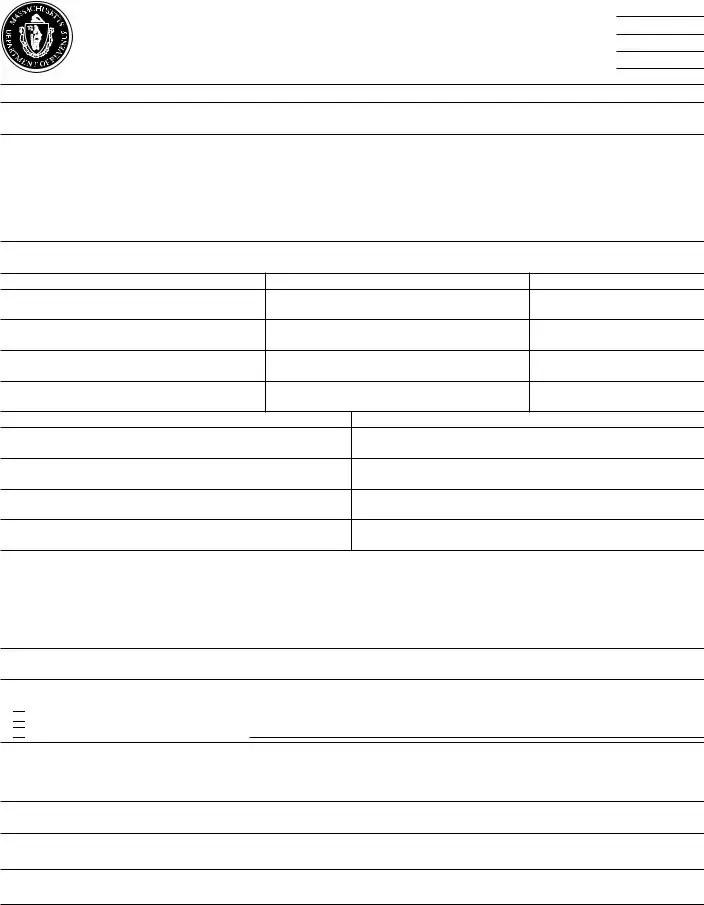

F If the power of attorney is granted to a person other than an attorney, certified public accountant, public accountant or enrolled agent, the taxpayer(s) signature must be witnessed or notarized below.

The person(s) signing as or for the taxpayer(s) (check and complete one):

D

is/are known to and signed in the presence of the two disinterested witnesses whose signatures appear here:

is/are known to and signed in the presence of the two disinterested witnesses whose signatures appear here:

Signature of witness |

Date |

|

|

Signature of witness |

Date |

|

|

D appeared this day before a notary public and acknowledged this power of attorney as a voluntary act and deed. |

|

|

|

Signature of notary |

Date |

|

|

Part 2. Declaration of Representative. All representatives must complete this section.

I declare that I am not currently under suspension or disbarment from practice within the Commonwealth or in any jurisdiction, that I am aware of regula- tions governing the practice of attorneys, certified public accountants, public accountants, enrolled agents and others, and that I am one of the following:

1a member in good standing of the bar of the highest court of the jurisdiction shown below;

2duly qualified to practice as a certified public accountant or public accountant in the jurisdiction shown below;

3enrolled as an agent under the requirements of Treasury Department Circular No. 230;

4a bona fide officer of the taxpayer organization or principal reporting corporation;

5a

6a member of the taxpayer’s immediate family (spouse, parent, child or sibling);

7a fiduciary for the taxpayer;

8other (attach statement)

and that I am authorized to represent the taxpayer identified in Part 1 for the tax matters specified there.

Designation (insert appropriate

number from above list)

Jurisdiction (state, etc.)

or enrollment card number

Signature

Date

Made fillable by FormsPal.

printed on recycled paper

printed on recycled paper

Form

General Information

To protect the confidentiality of tax records, Massachusetts law generally prohibits the Department of Revenue from disclosing information contained in tax returns or other documents filed with it to persons other than the tax- payer or the taxpayer’s representative. For your protection, the Department requires that you file a power of attorney before it will release tax information to your representative. The power of attorney will also allow your represen- tative to act on your behalf to the extent you indicate. Use Form

You may use Form

For certain corporate excise matters under MGL ch 63. By executing this agreement an officer of a principal reporting corporation filing under MGL ch 63, § 32B represents that the principal reporting corporation is authorized to execute this agreement as agent for all corporations that par- ticipated in, or were required to participate in, such filing for any component of the corporate excise reported or required to be reported under any sec- tion of MGL ch 63 by any such corporation whether relating to the income measure,

A principal reporting corporation acts on behalf of all corporations that partic- ipated in, or were required to participate in, a filing under MGL ch 63, § 32B, as stated in the preceding paragraph. Consequently, in the case of such a filing by a principal reporting corporation, the references in this agreement to “taxpayer(s)” shall include all such corporations.

Filing the Power of Attorney. You must file the original, a photocopy or facsimile transmission (fax) of the power of attorney with each DOR office in which your representative is to represent you. You do not have to file another copy with other DOR officers or counsel who later have the matter under consideration unless you are specifically asked to provide an addi- tional copy.

Revoking a Power of Attorney. If you previously filed a power of attorney and you want to revoke it, you may use Form

If you want to revoke a power of attorney without executing a new one, send a signed statement to each office of DOR in which you filed the earlier power of attorney you are now revoking. List in this statement the name and address of each representative whose authority is being revoked.

How to Complete Form

Part 1. Power of Attorney

A. Taxpayer’s name, identification number and address.

a.For individuals.Enter you name, social security number and address in the space provided. If joint returns involved, and you and your spouse are designating the same representative(s), also enter your spouse’s name and social security number and your spouse’s address (if different).

b.For a corporation, partnership or association.Enter the name, federal identification number and business address. If the Power of Attorney for a partnership will be used in a tax matter in which the name and social secu- rity number of each partner have not previously been sent to DOR, list the name and social security number of each partner in the available space at the end of the form or on an attached sheet.

c. For a principal reporting corporation. Enter the name, federal identifi- cation number and business address of the principal reporting corporation.

d. For a trust. Enter the name, title and address of the fiduciary, and the name and federal identification number of the trust.

e. For an estate. Enter the name, title and address of the decedent’s per- sonal representative, and the name and identification number of the estate. The identification number for an estate is the decedent’s social security number and includes the federal identification number if the estate has one.

B.Appointee(s) and tax matters and years or periods.Enter the name(s), address(es) and telephone number(s) of the individual(s) you appoint. Your representative must be an individual and may not be an organization, firm or partnership.

Consider each tax imposed by the Commonwealth for each tax period as a separate tax matter. In the columns provided, clearly identify the type(s) of tax(es) and the year(s) or period(s) for which the power is granted. You may list any number of years or periods and types of taxes on the same power of attorney. If the matter relates to estate tax, enter the date of the taxpayer’s death instead of the year or period.

If the power of attorney will be used in connection with a penalty that is not related to a particular tax type, such as personal income or corporate, enter the section of the General Laws which authorizes the penalty in the “type of tax” column.

C. Powers granted by Form

If you do not want your representative to be able to perform any of these or other specific acts, or if you want to give your representative the power to delegate authority or substitute another representative, insert language ex- cluding or adding these acts in the blank space provided.

D. Where you want copies to be sent. The Department of Revenue rou- tinely sends originals of all notices to the taxpayer. You may also have copies of all notices and all other written communications sent to your rep- resentative. Please check box 1 if you want copies of all notices or all com- munications sent to the first appointee named at the top of the form. Check box 2 if you want copies sent to one of your other appointees. In this case, list the name of the appointee.

E. Signature of taxpayer(s). For individuals: If a joint return is involved and both spouses will be represented by the same individual(s), both must sign the power of attorney unless one authorizes the other (in writing) to sign for both. In that case, attach a copy of the authorization. However, if the spouses are to be represented by different individuals, each may execute a power of attorney.

For a partnership: All partners must sign unless one partner is authorized to act in the name of the partnership. A partner is authorized to act in the name of the partnership if under state law the partner has authority to bind the partnership.

For a corporation or association: An officer having authority to bind the en- tity must sign.

For a principal reporting corporation: An officer having authority to bind the principal reporting corporation of a combined group.

If you are signing the power of attorney for a taxpayer who is not an indi- vidual, such as a corporation or trust, please type or print your name on the line below the signature line at the bottom of the form.

F. Notarizing or witnessing the power of attorney. A notary public or two individuals with no stake in the tax matter must witness a power of at- torney unless it is granted to an attorney, certified public accountant, public accountant or enrolled agent.

Part 2. Declaration of Representative

Your representative must complete Part 2 to make a declaration containing the following:

1.A statement that the representative is authorized to represent you as a certified public accountant, public accountant, attorney, enrolled agent, member of your immediate family, etc. If entering “eight” in the “designation” column, attach a statement indicating your relationship to the taxpayer.

2.The jurisdiction recognizing the representative, if applicable. For an attor- ney, certified public accountant or public accountant: Enter in the “jurisdic- tion” column the name of the state, possession, territory, commonwealth or District of Columbia that has granted the declared professional recogni- tion. For an enrolled agent: Enter the enrollment card number in the “juris- diction” column.

3.The signature of the representative and the date signed.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 2848 allows a taxpayer to authorize another person to represent them before the IRS. |

| Eligibility | Any individual or entity can be designated as a representative, including attorneys, certified public accountants, and enrolled agents. |

| Duration | The authorization remains in effect until the taxpayer revokes it or the IRS processes a new form. |

| Revocation | To revoke the authorization, submit a new Form 2848 indicating the revocation or write a separate letter stating the intent to revoke. |

| State-Specific | States may have their own forms for powers of attorney, such as California's Form FTB 3520 or New York's Form POA-1. Check relevant state laws. |

| Signature Required | The taxpayer must sign and date the form for it to be valid. Representatives also sign the form to confirm acceptance. |

| Filing Methods | The IRS allows submission of Form 2848 by mail, fax, or in person, depending on the situation. |

Filling out the IRS Form 2848, also known as the Power of Attorney Declaration, requires careful attention to detail to ensure that the appropriate information is accurately provided. Following the instructions step-by-step will help in effectively completing the form, facilitating a smooth transition for any necessary communication with the IRS.

Upon careful completion and submission of the form, you will await confirmation from the IRS regarding the acceptance of the Power of Attorney. This process typically takes some time, so patience will be essential as your request is processed. Keeping a record of all correspondence will be beneficial in case any follow-up is needed.

The Tax Power of Attorney (POA) Form 2848 is a document that allows you to authorize another person, often referred to as a representative, to act on your behalf regarding your tax matters. This could involve dealing with the IRS, accessing your tax information, or representing you in discussions about your tax returns. By completing and submitting this form, you grant your representative the authority to perform specific actions in your stead.

Form 2848 allows you to appoint various types of representatives. These may include:

Make sure whoever you choose is reliable and knowledgeable about tax matters, as they will have significant authority under this form.

To complete Form 2848, you’ll need to follow these steps:

Ensure all sections are filled out accurately to avoid any delays in processing.

You typically need to submit Form 2848 directly to the IRS. Once you've completed and signed it, you can send it to the appropriate IRS office handling your tax account. However, if your representative files it on your behalf, they can submit it for you. After submission, you will receive a confirmation from the IRS, indicating that your appointment is recognized.

The authority granted under Form 2848 generally remains valid until:

To revoke the form, you must submit a new Form 2848 with the relevant sections filled out indicating the revocation of the authority previously granted. It’s essential to keep track of any changes and ensure that your representation remains updated as needed.

Filling out the IRS Form 2848, Power of Attorney and Declaration of Representative, can be a daunting task. Mistakes on this form can lead to delays or even rejections of your authorization request. Here are six common errors people make when completing this important document.

One frequent mistake is providing incorrect or incomplete information. Test your attention to detail. Ensure that the name, address, and taxpayer identification number (TIN) of both the taxpayer and the representative are accurate. If any of this information is wrong, the IRS can reject the form, leaving you without the designated representative's assistance.

Another common error involves signing the form. Often, individuals assume that only the representative needs to sign. In reality, both the taxpayer and the representative must sign the form. Missing a signature can halt the processing of the application. Always double-check who needs to sign before submitting.

Many people do not specify the tax matters clearly enough on the form. A vague description can lead to confusion. Be explicit about the types of tax matters for which the power of attorney is granted. Whether it’s income tax, estate tax, or payroll tax, detailed clarity helps ensure that the representative can act on your behalf in the specified areas.

Another mistake is neglecting to check the expiration date of the power of attorney. The IRS does not provide an unlimited time frame for representation. Confirm that you indicate the appropriate duration for which the power of attorney is valid, or be ready to provide a specific date by which you want the authority to expire.

Some taxpayers forget to consider the needs of their representative. Not all professionals hold the same qualifications. Make sure that the person you designate is authorized to represent you before the IRS. This includes verifying their credentials and ensuring they can legally act on your behalf.

Finally, tardiness can lead to issues. Submitting the form too late can render the POA ineffective, especially if the representative needs to act promptly on critical tax matters. Ensure that the application is submitted well in advance of any deadlines or issues that may arise.

When navigating the complexities of tax matters in the United States, it’s essential to complement the IRS Form 2848, also known as the Power of Attorney (POA) form, with several other documents that can enhance the process. These documents serve various purposes and facilitate communication between taxpayers and the IRS. Below is a list of forms often used in conjunction with the Tax POA Form 2848.

Understanding these additional forms enhances taxpayer readiness and compliance, ensuring that they can efficiently manage all interactions with the IRS. Careful documentation can alleviate potential issues and foster a smoother tax experience.

When filling out the Tax POA (Power of Attorney) Form 2848, it's important to be careful and thorough. Here are some helpful tips to ensure the process goes smoothly.

Following these guidelines can help ensure that your Tax POA Form 2848 is filled out correctly and efficiently processed.

Many individuals have misunderstandings about the Tax Power of Attorney (POA) Form 2848. This form allows a designated representative to handle tax matters on someone’s behalf. Here are some common misconceptions:

Understanding these points can help ensure that you use Form 2848 effectively, enabling your designated representative to assist you with your tax matters smoothly.

Filling out and using the Tax Power of Attorney (POA) Form 2848 can be a straightforward process with the right guidelines. Here are some key takeaways to keep in mind:

By following these steps, you can efficiently complete and utilize Form 2848, ensuring that your tax matters are managed appropriately.