The Tax POA M-5008-R form serves as a crucial tool in the realm of tax compliance, allowing taxpayers to designate an individual or entity to represent them before the Department of Revenue. This form streamlines communication between taxpayers and tax authorities, typically used when individuals require assistance with their tax matters. By completing the M-5008-R, clients grant their appointed representatives authority to discuss, negotiate, and resolve issues related to their tax obligations. Notably, this form not only helps in authorizing the representation but also specifies the scope of that authority. It includes important sections that require detailed information, such as the taxpayer’s name, identification number, and the representative’s contact information. Furthermore, the form emphasizes the importance of providing clear instructions regarding the extent of the authority being granted, which may encompass a variety of tax-related issues, including audits and compliance matters. It is essential for individuals to verify the details of the form, as any inaccuracies may lead to complications in representation. Understanding the function and proper use of the Tax POA M-5008-R is, therefore, essential for ensuring effective representation in tax matters, ultimately facilitating a smoother experience when interacting with tax authorities.

Appointment of Taxpayer Representative (Form

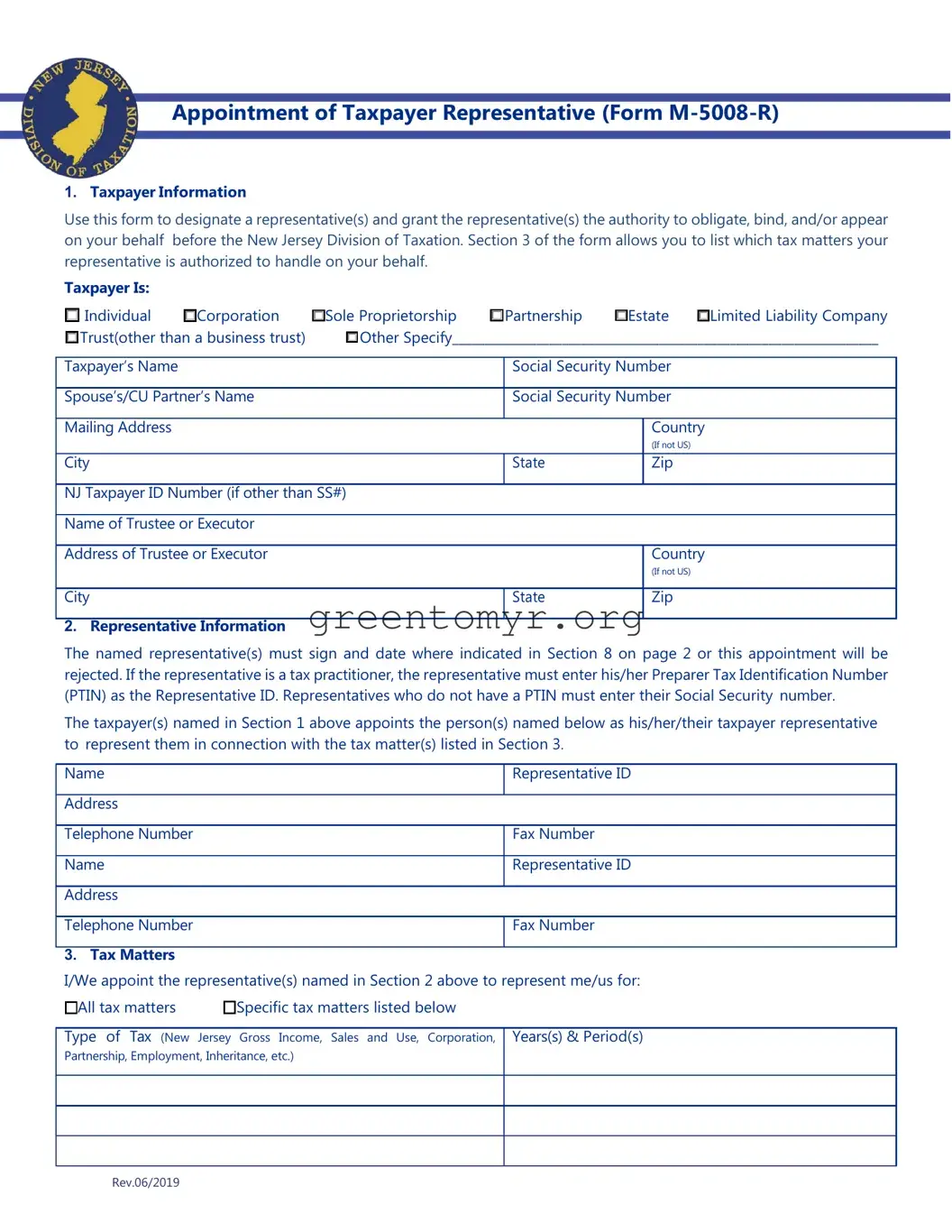

1.Taxpayer Information

Use this form to designate a representative(s) and grant the representative(s) the authority to obligate, bind, and/or appear on your behalf before the New Jersey Division of Taxation. Section 3 of the form allows you to list which tax matters your representative is authorized to handle on your behalf.

Taxpayer Is:

☐Individual ☐Corporation ☐Sole Proprietorship ☐Partnership ☐Estate ☐Limited Liability Company ☐Trust(other than a business trust) ☐Other Specify__________________________________________________________________

Taxpayer’s Name |

Social Security Number |

|

|

|

|

Spouse’s/CU Partner’s Name |

Social Security Number |

|

|

|

|

Mailing Address |

|

Country |

|

|

(If not US) |

City |

State |

Zip |

|

|

|

NJ Taxpayer ID Number (if other than SS#) |

|

|

|

|

|

Name of Trustee or Executor |

|

|

|

|

|

Address of Trustee or Executor |

|

Country |

|

|

(If not US) |

|

|

|

City |

State |

Zip |

|

|

|

2.Representative Information

The named representative(s) must sign and date where indicated in Section 8 on page 2 or this appointment will be rejected. If the representative is a tax practitioner, the representative must enter his/her Preparer Tax Identification Number (PTIN) as the Representative ID. Representatives who do not have a PTIN must enter their Social Security number.

The taxpayer(s) named in Section 1 above appoints the person(s) named below as his/her/their taxpayer representative to represent them in connection with the tax matter(s) listed in Section 3.

Name

Address

Telephone Number

Name

Address

Telephone Number

3.Tax Matters

Representative ID

Fax Number Representative ID

Fax Number

I/We appoint the representative(s) named in Section 2 above to represent me/us for: ☐All tax matters ☐Specific tax matters listed below

Type of Tax (New Jersey Gross Income, Sales and Use, Corporation, Partnership, Employment, Inheritance, etc.)

Years(s) & Period(s)

Rev.06/2019

4.Acts Authorized

The representative(s) is/are authorized to receive and inspect confidential tax records and is/are granted full power to act with respect to the tax matters described in Section 3 above, and to do and perform all such acts as I/we could do or perform. The authority granted by this appointment does not include the power to endorse a refund check.

☐If you want the representative(s) to have limited power, provide an explanation on the lines below and check this box. You may attach additional information as well.

5.Notices and Communications (audit correspondence only)

We will send original notices and other written communications to you and a copy (other than automated computer notices) to the first representative listed in Section 2 unless you check one or more of the boxes below.

☐I/We do not want the Division to send any notices or communications to my representative(s).

☐I/We want the Division to send a copy of notices and/or communications (other than automated computer notices) to both representatives listed in Section 2.

6.Retention/Revocation of Prior Appointment(s) or Power(s)

The filing of this form automatically revokes all earlier Appointment(s) of Taxpayer Representative and/or Power(s) of Attorney on file with the Division of Taxation for the tax matters and years or periods listed in Section 3 unless you check the box below.

☐I/We do not want to revoke any prior Appointment(s) of Taxpayer Representative and/or Power(s) of Attorney. If you check this box, you must attach copies of the previous Appointment(s) and/or Power(s) that you do not want to revoke.

7.Signature of Taxpayer(s)

If the tax matters covered by this appointment concern a joint Gross Income Tax return and the representative(s) is/are being appointed to represent both spouses/CU partners, both must sign below.

If a corporate officer, partner, guardian, tax matter partner, executor, administrator, or trustee signs the appointment on behalf of the taxpayer, the signature below certifies that they have the authority to execute this form on behalf of the taxpayer(s).

This Appointment of Taxpayer Representative Is Void if not Signed and Dated

Taxpayer Signature |

|

IDate |

Print Name |

ITitle (if applicable) |

|

Taxpayer Signature |

|

IDate |

Print Name |

ITitle (if applicable) |

|

8.Acceptance of Representation and Signature

I/ We accept the appointment as representative(s) for the taxpayer(s) who has/have executed this Appointment of Taxpayer Representative.

Representative Signature |

|

IDate |

Print Name |

ITitle (if applicable) |

|

Representative Signature |

|

IDate |

Print Name |

ITitle (if applicable) |

|

Rev.06/2019

Instructions for Form

Use this form to designate a representative(s) and grant the representative(s) the authority to obligate, bind, and/or appear on your behalf before the New Jersey Division of Taxation. Section 3 of the form allows you to list which tax matters your representative is authorized to handle on your behalf.

You may authorize the representative(s) to receive your confidential tax information. Unless otherwise indicated, the representative(s) may also perform any and all acts that you can perform regarding your taxes. This includes consenting to extend the time to assess tax or agreeing to a tax adjustment. Representatives may not sign returns or delegate authority unless specifically authorized to do so on this form.

Form

•When an individual appears with you or with a representative who is authorized to act on your behalf. For example, this form is not required if a representative appears on behalf of a corporate taxpayer with an authorized corporate officer;

•If a trustee, receiver, or attorney has been appointed by a court that has jurisdiction over a debtor;

•If an individual merely furnishes tax information or prepares a report or return for you;

•When a fiduciary stands in the position of, and acts as, the taxpayer. However, if a fiduciary wishes to authorize an individual to represent or act on behalf of the taxpayer, the fiduciary must sign and file Form

Limitations

Appointing a representative does not relieve you of tax responsibilities or obligations. This form allows another person to represent you in most matters concerning tax administration, tax investigations, examinations/audits, and other meetings with the Division. Because you remain responsible for your tax obligations, a representative’s authority does not extend to some aspects of the collection process. Examples of the collection process are: judgments, levies, liens, and seizures. In these instances, we may require telephone communication, direct contact, and/or interaction with the taxpayer.

Who Can Execute the Appointment of Taxpayer Representative?

•An individual, if the request pertains to a personal Income or individual Use Tax return filed by that individual (or by an individual and his or her spouse/CU partner if the request pertains to a joint Income Tax return and joint representation is requested). If joint representation is not requested, each taxpayer must file his or her own form.

•If the taxpayer is a limited liability company (LLC), a manager of the LLC. If there is no manager, a member of the LLC authorized to act on tax matters on behalf of the entity.

•A sole proprietor.

•A general partner of a partnership or limited partnership.

•The administrator or executor of an estate.

•The trustee of a trust.

•If the taxpayer is a corporation, a principal officer or corporate officer who is authorized to act on tax matters and has legal authority to reach agreements on behalf of the corporation; any person who is designated by the board of directors or other governing body of the corporation; any officer or employee of the corporation upon written request signed by a principal officer of the corporation and attested by the secretary or other officer of the corporation; or any other person who is authorized to receive or inspect the corporation’s return or return information under I.R.C. §6103(e)(1)(D).

Tax Matters

You may enter more than one tax type and indicate the tax year(s) and/or tax period(s) applicable in Section 3. If you designate a specific tax but no tax year or period, the

Rev.06/2019

Retention/Revocation of Prior Powers of Attorney and/or Appointments of Taxpayer Representative

By executing and filing the

You may not partially revoke a previously filed Form

Signature of Taxpayer(s)

You, or an individual you authorize to execute the Form

Individuals. If the matter for which the appointment is prepared involves a joint Income Tax return and the same individual(s) will represent both spouses/CU partners, both must sign Form

Corporations. The president,

Partnerships. All partners must sign Form

Limited Liability Companies (LLC). A member or manager must sign Form

Fiduciaries. In matters involving fiduciaries under agreements, declarations, or appointments, Form

Estates. The administrator or executor of an estate may execute Form

Others. Form

Instructions for Submission

Completion and submission of this form is only required when you are communicating – either in person or in writing – with the Division on behalf of another person.

In Person

If you are planning to visit a Regional Information Center on behalf of another individual, you must bring:

•The completed form, signed by both the representative and the taxpayer; and

•One form of

In Writing

If you are responding to a notice sent by the Division, submit your documentation to the PO Box on the notice. You must include with your correspondence:

•The completed form, signed by both the representative and the taxpayer;

•A copy of the notice; and

•Any corresponding documentation.

Rev.06/2019

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA m-5008-r form is used to appoint a representative to act on behalf of a taxpayer in dealing with tax matters. |

| Eligibility | This form can be utilized by any individual or business entity needing to authorize someone to represent them before tax authorities. |

| Governing Law | The form is governed by state tax laws, which vary by state. For instance, in New York, it falls under the New York State Tax Law. |

| Submission | The completed form must be submitted to the appropriate tax agency, either by the taxpayer or the designated representative. |

| Revocation | Taxpayers can revoke their power of attorney at any time by submitting a revocation form to the taxing authority. |

| Duration | The authority granted lasts until revoked, or until the specific tax year or issue for which it was granted is resolved. |

The Tax POA m-5008-r form is crucial for authorizing someone to act on your behalf concerning tax matters. Once you gather the necessary information, including details about the taxpayer, the representative, and the scope of authorization, you will be ready to complete the form. Follow these steps to ensure accurate completion.

After submitting the form, keep a copy for your records. Your authorized representative will be able to assist you with your tax matters as specified once the authorization is processed.

The Tax POA m-5008-r form is a Power of Attorney (POA) document that authorizes an individual, typically a tax professional or an accountant, to represent you in tax matters before the state taxing authority. This form allows your designated representative to act on your behalf, filing tax returns, addressing tax issues, and communicating with tax authorities during audits or disputes.

You can appoint anyone you trust as your representative, but it is common to choose a tax professional, such as a CPA or an enrolled agent. It’s essential to ensure that the individual you designate has the appropriate knowledge and experience to handle your tax matters effectively.

To complete the Tax POA m-5008-r form, follow these steps:

Yes, you need to submit the completed Tax POA m-5008-r form to the appropriate state tax authority. Ensure that you check the specific requirements for your state, as some may offer electronic filing options while others may require mailed submissions.

Absolutely. You have the right to revoke the Power of Attorney at any time. To do so, you should submit a written notice of revocation to the tax authority as well as inform your appointed representative of your decision.

Once you submit the Tax POA m-5008-r form to the taxing authority, it generally becomes effective immediately. You should confirm with your representative to ensure they are recognized by the tax authority and can begin acting on your behalf.

The form can cover a wide range of tax matters, including but not limited to:

No, the Tax POA m-5008-r form is specifically designed for state tax matters. For federal tax representation, you would need to use the IRS Form 2848, which serves a similar purpose at the federal level.

If you suspect that your representative is misusing the Power of Attorney, you should act quickly. You can revoke their authority by submitting a written notice to the taxing authority and informing the representative of your decision. It may also be advisable to consult legal counsel if needed.

Filling out the Tax POA M-5008-R form can sometimes feel daunting. Many taxpayers make mistakes that can delay the processing of their authorization request. One common error is providing incomplete information. Not including all required fields, such as your contact details or tax identification number, can lead to rejection or require additional steps to correct.

Another frequent mistake involves selecting the wrong categories of representation. The form allows for different types of representation, and choosing the incorrect option may prevent your representative from acting on your behalf as you intended. This is particularly crucial when considering various legal or tax matters, as it can limit the scope of your agent's authority.

Many people overlook the importance of signatures. The Tax POA M-5008-R form generally requires signatures from both the taxpayer and the representative. Failing to secure both signatures can result in processing delays. If the signatures are not clear or legible, it could also complicate matters further.

Finally, misunderstanding deadlines can lead to problems. Some taxpayers submit the form close to important dates, thinking it will be processed immediately. However, processing times can vary. It’s advisable to allow ample time for the form to be processed to avoid any last-minute issues, particularly around tax season.

The Tax POA M-5008-R form is a document that allows taxpayers to authorize someone else, typically a tax professional, to act on their behalf in matters concerning state tax obligations. Along with this form, other documents and forms may be necessary to ensure a smooth process when dealing with tax-related issues. Below is a list of common forms and documents that are often used in conjunction with the M-5008-R form. Each entry is briefly described to provide a clear understanding of its purpose.

In summary, the Tax POA M-5008-R form is just one component of the process surrounding tax obligations. Understanding and organizing these accompanying documents can make tax filing and resolution more efficient and manageable. Each of these forms serves a specific function, highlighting the complexity and necessity of thorough and accurate tax documentation.

Filling out the Tax POA M-5008-R form is an important step in ensuring that your tax matters are handled efficiently. To help you navigate this process, consider the following dos and don’ts:

By keeping these points in mind, you can help ensure your form is processed smoothly and without unnecessary delays.

When dealing with tax matters, clarity is crucial to ensure compliance and proper representation. The Tax Power of Attorney (POA) M-5008-R form is no exception. Here are seven common misconceptions that can lead to confusion:

Understanding these misconceptions can greatly simplify the process of appointing a representative for tax matters. Proper knowledge leads to informed decisions and smoother handling of tax responsibilities.

Filling out and using the Tax POA m-5008-r form is an important task for anyone who needs to designate someone to act on their behalf in tax matters. Here are some key takeaways to keep in mind:

Being proactive and informed can greatly ease the process of handling tax matters through a Power of Attorney. Stay organized and communicate clearly with your chosen representative, and you'll navigate the system with greater confidence.