The Tax POA POA-1 form plays a crucial role for individuals and businesses when it comes to handling tax matters with the IRS. This form allows taxpayers to designate a representative who can act on their behalf in front of the Internal Revenue Service, ensuring that they have the necessary support to navigate the complex world of tax regulations. By completing the POA-1 form, taxpayers can authorize their chosen representative to receive confidential information, represent them in audits, and even sign documents relating to tax filings. This delegation of authority can make managing tax responsibilities less daunting, whether you’re dealing with routine paperwork or facing an audit. Furthermore, clarity in the designated powers can prevent misunderstandings about what the representative can and cannot do, providing peace of mind to taxpayers as they manage their financial obligations. Understanding the nuances of the POA-1 form is essential for a smooth and effective interaction with the IRS.

RK |

New York State Department of Taxation and Finance |

N¥C |

|

w |

New York City Department of Finance |

|

|

4 ATE |

|

|

|

Power of Attorney |

(6/17) |

Department of Finance |

|

|

Read instructions on the back before completing this form. For estate tax matters, use Form

Filing Form

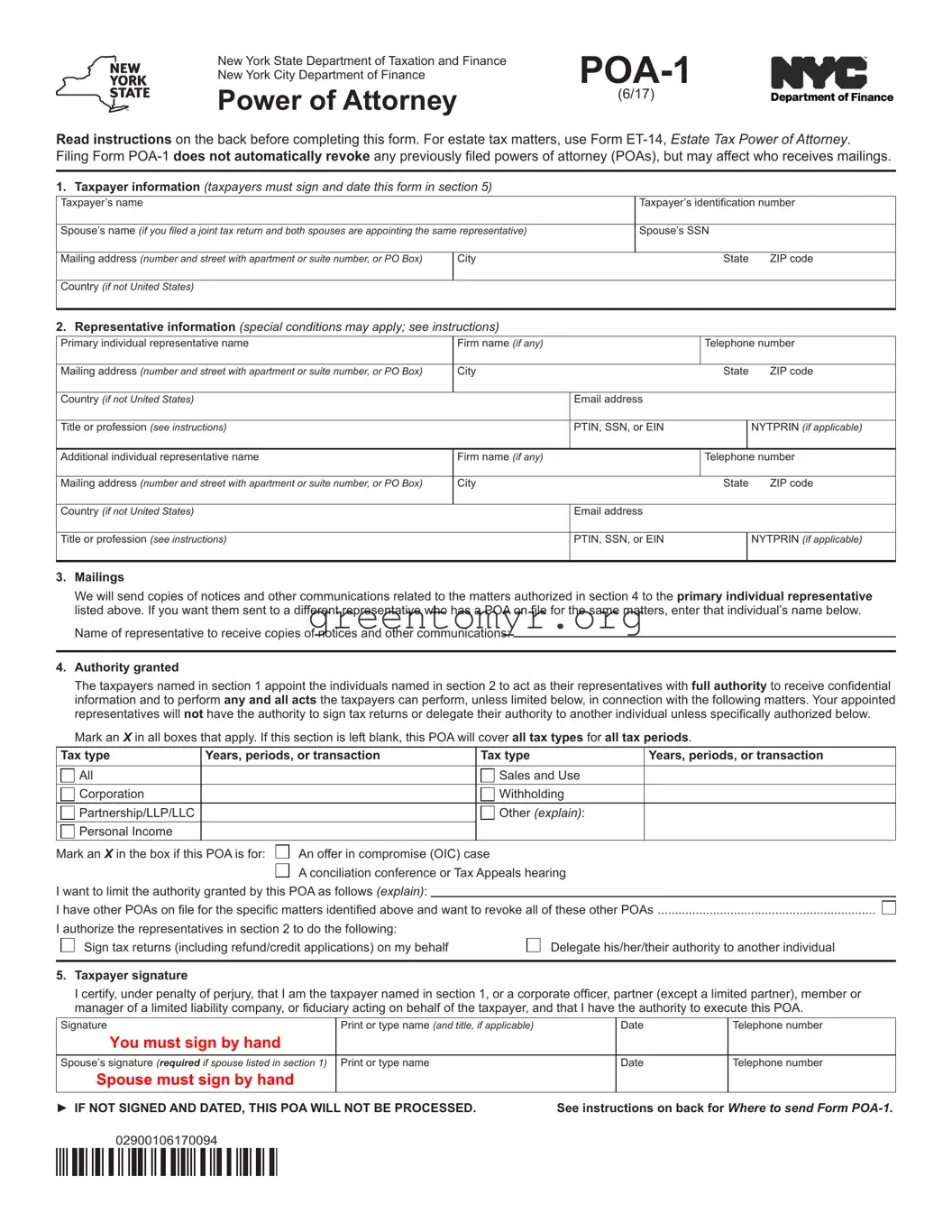

1.Taxpayer information (taxpayers must sign and date this form in section 5)

Taxpayer’s name |

|

|

Taxpayer’s identification number |

||

|

|

|

|

|

|

Spouse’s name (if you filed a joint tax return and both spouses are appointing the same representative) |

|

Spouse’s SSN |

|

||

|

|

|

|

|

|

Mailing address (number and street with apartment or suite number, or PO Box) |

ICity |

|

|

State |

ZIP code |

Country (if not United States) |

|

|

|

|

|

|

|

|

|

|

|

2. Representative information (special conditions may apply; see instructions) |

|

|

|

|

|

|

|

|

|

|

|

Primary individual representative name |

Firm name (if any) |

|

|

ITelephone number |

|

Mailing address (number and street with apartment or suite number, or PO Box) |

City |

|

|

State |

ZIP code |

|

|

|

|

|

|

Country (if not United States) |

|

Email address |

|

|

|

|

|

|

|

|

|

Title or profession (see instructions) |

|

PTIN, SSN, or EIN |

|

NYTPRIN (if applicable) |

|

|

|

|

|

1 |

|

Additional individual representative name |

Firm name (if any) |

|

|

ITelephone number |

|

|

|

|

|

|

|

Mailing address (number and street with apartment or suite number, or PO Box) |

City |

|

|

State |

ZIP code |

|

|

|

|

|

|

Country (if not United States) |

|

Email address |

|

|

|

|

|

|

|

|

|

Title or profession (see instructions) |

|

PTIN, SSN, or EIN |

|

NYTPRIN (if applicable) |

|

|

|

|

|

1 |

|

3.Mailings

We will send copies of notices and other communications related to the matters authorized in section 4 to the primary individual representative listed above. If you want them sent to a different representative who has a POA on file for the same matters, enter that individual’s name below.

Name of representative to receive copies of notices and other communications:

4.Authority granted

The taxpayers named in section 1 appoint the individuals named in section 2 to act as their representatives with full authority to receive confidential

information and to perform any and all acts the taxpayers can perform, unless limited below, in connection with the following matters. Your appointed representatives will not have the authority to sign tax returns or delegate their authority to another individual unless specifically authorized below.

Mark an X in all boxes that apply. If this section is left blank, this POA will cover all tax types for all tax periods.

Tax type |

Years, periods, or transaction |

|

Tax type |

Years, periods, or transaction |

|

|

|

|

|

|

|

|

|

All |

|

|

|

Sales and Use |

|

|

Corporation |

|

|

|

Withholding |

|

|

Partnership/LLP/LLC |

|

|

IB |

Other (explain): |

|

|

I~ Personal Income |

|

|

|

|

|

|

Mark an X in the box if this POA is for: □ An offer in compromise (OIC) case |

|

|

|

|||

|

□ A conciliation conference or Tax Appeals hearing |

|

|

|||

I want to limit the authority granted by this POA as follows (explain): |

|

|

|

|

|

|

I have other POAs on file for the specific matters identified above and want to revoke all of these other POAs |

□ |

|||||

I authorize the representatives in section 2 to do the following:

□ Sign tax returns (including refund/credit applications) on my behalf |

□ Delegate his/her/their authority to another individual |

|

|

5.Taxpayer signature

I certify, under penalty of perjury, that I am the taxpayer named in section 1, or a corporate officer, partner (except a limited partner), member or manager of a limited liability company, or fiduciary acting on behalf of the taxpayer, and that I have the authority to execute this POA.

Signature |

Print or type name (and title, if applicable) |

Date |

Telephone number |

You must sign by hand |

|

|

|

|

|

|

|

Spouse’s signature (required if spouse listed in section 1) |

Print or type name |

Date |

Telephone number |

Spouse must sign by hand |

|

|

|

|

|

|

|

►IF NOT SIGNED AND DATED, THIS POA WILL NOT BE PROCESSED. See instructions on back for Where to send Form

02900106170094

11111111111111111 111111111111111111 II II

Instructions

General information

Use Form

more individuals the authority to obligate or bind you, or appear on your behalf. You may only appoint individuals (not a firm) to represent you. Note: Authorizing someone to represent you does not relieve you of your

tax obligations.

Use this form for all matters (except estate tax) imposed by the Tax Law or another statute administered by the New York State (NYS) Department of Taxation and Finance (Tax Department) and the New

York City (NYC) Department of Finance. If you and your spouse filed a joint tax return but have different representatives, you must each file a

separate Form

Unless you limit the authority you grant (see section 4), your appointed representative will be authorized to perform any and all acts you can perform, including but not limited to: receiving confidential information

concerning your taxes, agreeing to extend the time to assess tax, and agreeing to a tax adjustment.

You do not need Form

someone to provide information, or prepare a report or return for you.

Only certain types of professionals may act on your behalf before the NYS Bureau of Conciliation and Mediation Services (BCMS), the NYC Department of Finance Conciliation Bureau or at Tax Appeals. Visit the Tax Department’s POA webpage (at www.tax.ny.gov/poa) for more information.

Revocation and withdrawal – New: This POA will remain active until you (the taxpayer) revoke it or your representative withdraws from representing you. Representatives may not revoke a POA.

For information on ways to revoke a POA, or how a representative

can withdraw, see the Tax Department’s POA webpage (at www.tax.ny.gov/poa).

Specific instructions

For additional information on how to complete Form

who must sign as the taxpayer, visit the Tax Department’s POA webpage (at www.tax.ny.gov/poa).

The taxpayer identification number may be a social security number (SSN), employer identification number (EIN), individual taxpayer identification number (ITIN) issued by the Internal Revenue Service, or a tax identification number issued by the NYS Tax Department.

If you want copies of notices and other communications sent to someone other than the primary individual representative listed in section 2 of this POA, enter the name of that representative on the line provided. This

representative must be someone who is listed as a representative for the matters covered by this POA on this or another valid POA on file.

If you do not want copies of notices and other communications sent to any representative, enter None.

Example: On 2/1/2016 you appoint Mr. Smith as your representative for all tax matters for 2015. Mr. Smith will receive copies of mailings for these matters. On 8/15/2016, you appoint Ms. Jones as your representative for all tax matters for 2015. Ms. Jones will now receive copies of mailings for these matters. However, if you want Mr. Smith to continue to receive mailings, you must list Mr. Smith’s name in section 3 of the POA appointing Ms. Jones. Ms. Jones will not receive mailings.

Use this section to specify the matters covered by this POA. By default, this POA will cover all tax types for all tax periods. If you select a tax type, but do not enter a tax period, this POA will cover the tax type selected for all tax periods. If you enter a tax period, but do not select a tax type, this POA will cover the tax period entered for all tax types. For

tax periods other than calendar years, enter the beginning and ending dates for the periods. For taxes based on a specific transaction, enter

the transaction date.

If your tax type is not listed, or if you are granting authority for a special assessment or fee administered by an agency, mark an X in the Other box and explain. To identify a specific audit case or assessment, mark the Other box and enter a case or assessment ID number.

If you want to limit your representative’s authority, explain the limitation.

For example, you can limit your representative’s authority to only receive confidential information, but make no binding decisions for you. If you

need more space to explain the limitation, attach a sheet. The attached sheet must be signed and dated by each taxpayer named in section 1.

You or someone who is authorized to act for you must sign and date Form

If a joint tax return was filed and both spouses will be represented by the

same representatives, both spouses must sign and date Form

You may use Form

other communications unless you direct otherwise in section 3. If you are appointing more than two representatives, attach a sheet that provides all of the information requested in section 2. The attached sheet must be signed and dated by each taxpayer named in section 1.

Caution: This POA cannot be partially revoked or withdrawn. If you appoint more than one representative on this POA and later choose to revoke one representative or one representative withdraws, the revocation or withdrawal will apply to all representatives, and none will have ongoing authority to represent you. You must file a new POA to appoint the representatives that you want to continue representing you.

All representatives are deemed as authorized to act separately unless you explain that all representatives are required to act jointly on the line in section 4 that allows you to limit the authority granted by this POA.

For each appointed representative, enter the title or profession or, if your representative is not a professional, enter the representative’s relationship to you. If the representative is not licensed in NYS, also

include the state where licensed (for example, Florida attorney). Enter each representative’s federal preparer tax identification number (PTIN),

SSN, or EIN. If applicable, also enter each representative’s New York tax

preparer registration identification number (NYTPRIN).

For matters administered by the NYS Tax Department:

FAX to: (518)

Mail to: NYS TAX DEPARTMENT

POA CENTRAL

W A HARRIMAN CAMPUS

ALBANY NY

See Publication 55, Designated Private Delivery Services, if not using U.S. Mail.

For matters administered by NYC Department of Finance, send to the office in which the matter is pending.

Privacy notification

New York State Law requires all government agencies that maintain a system of records to provide notification of the legal authority for any

request for personal information, the principal purpose(s) for which the

information is to be collected, and where it will be maintained. To view this information, visit our website at www.tax.ny.gov, or, if you do not

have Internet access, call (518)

The Commissioner of the New York City Department of Finance is authorized to require disclosure of identifying numbers by

section

02900206170094

11111111111111111

II

II

I IIIIII I Ill I IIII

I IIIIII I Ill I IIII

II II

II II

| Fact Name | Details |

|---|---|

| Purpose | The Tax POA POA-1 form is used to authorize an individual to represent a taxpayer before the tax authorities. |

| Importance | This form is crucial for enabling designated representatives to handle tax matters on behalf of taxpayers. |

| Filing Requirement | Taxpayers must submit this form to ensure their representative can act in an official capacity. |

| Governing Law | The use of the POA-1 form is governed by state tax law, such as the Internal Revenue Code and specific state tax regulations. |

| Eligibility | Any taxpaying individual or entity can appoint a representative using this form. |

| Expiration | Generally, the authorization remains valid until revoked or until the taxpayer's account is settled. |

| Submission Method | The form can be submitted via mail, fax, or electronically, depending on state regulations. |

| Common Use Cases | This form is frequently used for audits, tax disputes, and other tax-related communications. |

After obtaining the Tax POA POA-1 form, you are ready to complete it for submission. Following the steps below will ensure that you fill out the form correctly and provide the necessary information for the process.

Once completed, review the form for accuracy and compliance with the required guidelines. Prepare it for submission according to the instructions provided with the form.

The Tax POA POA-1 form, or Power of Attorney form for tax matters, is a legal document that grants an individual or an organization the authority to act on your behalf regarding tax-related issues. This could include interacting with the IRS or state tax authorities, representing you during audits, or handling tax disputes. By completing this form, you allow your designated representative to make decisions and provide information related to your taxes, thereby relieving you of direct involvement in the process.

You can appoint a variety of individuals or entities as your representative on the POA-1 form. Common choices include tax professionals such as certified public accountants (CPAs), attorneys, or enrolled agents. It’s essential that the person you select is trustworthy and knowledgeable about tax matters, as they will be managing important aspects of your financial obligations. Ensure that your representative is willing and capable of taking on this responsibility before completing the form.

Completing the POA-1 form involves several straightforward steps:

After submission, you may want to confirm that the form was received and processed correctly, ensuring that your representative can begin acting on your behalf.

Yes, you have the authority to revoke or change your designated representative at any time. To do so, you would typically need to complete a new POA-1 form, marking it clearly as a revocation of the previous powers granted. Be sure to communicate your decision to both your new representative and the previously appointed representative to avoid any confusion. Filing the new form appropriately with the tax authority will ensure that your current wishes are accurately reflected in their records.

Filling out the Tax POA POA-1 form can often be a daunting task, and mistakes can lead to delays or complications in handling tax matters. One common mistake is failing to include all necessary information. Individuals may overlook crucial details like their Social Security number or Taxpayer Identification Number. Omitting this information can cause the form to be returned or delayed, meaning the Power of Attorney may not be effective when needed most.

Another frequent error happens when people neglect to sign the form. While it may seem obvious, some individuals get caught up in the details and forget to include their signature. Without a signature, the IRS will not process the form. This simple oversight can result in frustration, as individuals find themselves unable to take advantage of their chosen representative’s assistance.

In addition to forgetting signatures, individuals may not keep a copy of the completed form. It’s best practice to maintain a copy for personal records. Having a copy of the submitted form can help track the process and provide clarity should any questions arise in the future. Relying solely on memory or the assumption that everything was submitted correctly can lead to misunderstandings.

Another mistake to be aware of is providing incorrect or outdated information about the representative. Ensuring that your chosen representative’s information is current is vital. This includes their contact information and address. Outdated details can lead to further complications and hinder communication, which is crucial when dealing with tax matters.

Finally, misunderstanding who should fill out the form can lead to errors. The taxpayer must complete the form and not the representative. Miscommunication in this regard can create confusion and delays in the process. It’s important to clarify roles to ensure that the Power of Attorney is set up correctly and efficiently.

The Tax Power of Attorney (POA-1) form serves as an important tool for individuals who wish to authorize someone else to act on their behalf when dealing with tax matters. Alongside this form, several other documents may be necessary or useful to facilitate the process of managing tax obligations and communication with tax authorities. Below is a list of commonly used forms and documents that complement the Tax POA-1 form.

In conclusion, utilizing the Tax POA POA-1 form in conjunction with these additional documents can streamline the management of your tax situation. Each form serves a purpose, whether it is to authorize representation, obtain information, or comply with state requirements. Completing these forms accurately is crucial to ensure that your intended representatives can effectively act on your behalf.

IRS Form 2848: Power of Attorney and Declaration of Representative - This form enables a taxpayer to grant authority to someone to represent them before the IRS. It is similar because it allows individuals to authorize others to act on their behalf regarding tax matters.

IRS Form 8821: Tax Information Authorization - This document permits a third party to receive the taxpayer's confidential tax information from the IRS. Like the Tax POA POA-1 form, it provides a mechanism for communication between the IRS and the taxpayer’s appointed representative.

State Power of Attorney Forms - These forms allow individuals to appoint representatives for various legal matters at the state level, similar to how the Tax POA POA-1 form functions for tax-related issues. Both types of documents typically outline the authority granted to the designated representative.

Financial Power of Attorney - This document allows a person to manage another individual's financial affairs. Though primarily financial, it shares the core purpose with the Tax POA POA-1 form by enabling someone to act in the best interest of another individual concerning specific matters.

When filling out the Tax POA POA-1 form, there are important guidelines to follow. Here’s a simple list of dos and don’ts to help you through the process.

By following these tips, you can make the process smoother and avoid common pitfalls.

Misconceptions about the Tax Power of Attorney (POA) form can lead to misunderstandings and errors in managing tax responsibilities. Here are ten prevalent misconceptions regarding the Tax POA POA-1 form:

Understanding these misconceptions can help ensure that taxpayers utilize the Tax POA POA-1 form correctly and effectively manage their interactions with the IRS.

Filling out and using the Tax POA (Power of Attorney) POA-1 form can be a crucial step in managing your tax affairs. Below are key takeaways to keep in mind:

By following these key points, you can ensure that the process is smooth and your interests are well represented in tax matters.