The IRS Form 2848, also known as the Power of Attorney and Declaration of Representative, serves as a crucial tool for individuals and businesses navigating the complexities of the U.S. tax system. This form allows taxpayers to appoint a trusted individual, such as a tax professional or attorney, to act on their behalf in dealings with the IRS. By submitting Form 2848, the taxpayer grants authority to their chosen representative to receive and discuss confidential tax information, sign documents, and represent them during tax audits or appeals. This not only simplifies communication with the IRS but also ensures that taxpayers can get expert assistance during challenging tax situations. Importantly, the form requires detailed information about both the taxpayer and the appointed representative, including their identification numbers and the specific tax matters they will handle. Additionally, Form 2848 must be signed and dated by the taxpayer, reflecting their consent and intent. With tax regulations continuously evolving, having a knowledgeable advocate can bring peace of mind and clarity to taxpayers' obligations and rights.

|

|

|

PRINT FORM |

|

RESET FORM |

|

1350 |

|

|

|

|

|

|

|

STATE OF SOUTH CAROLINA |

|

|

|

||

|

|

|

|

|||

|

|

DEPARTMENT OF REVENUE |

|

SC2848 |

||

|

|

POWER OF ATTORNEY AND |

|

|||

|

|

|

(Rev. 2/2/18) |

|||

dor.sc.gov |

|

DECLARATION OF REPRESENTATIVE |

3307 |

|

||

|

|

|

|

|

|

|

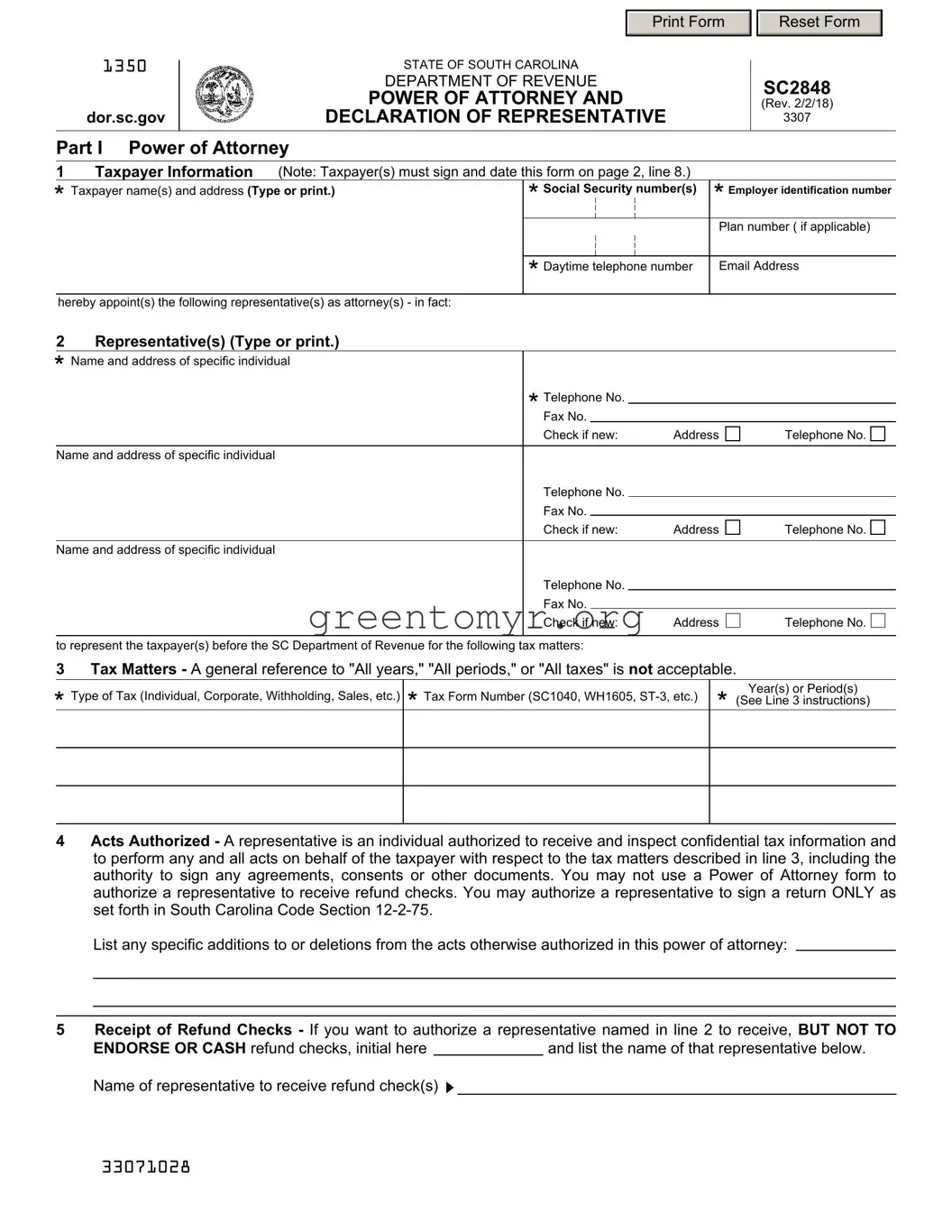

Part I Power of Attorney

1Taxpayer Information (Note: Taxpayer(s) must sign and date this form on page 2, line 8.)

|

|

|

|

|

|

|

|

* Taxpayer name(s) and address (Type or print.) |

*Social |

Security |

|

number(s) |

* Employer identification number |

||

|

|

|

|||||

|

|

|

|||||

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Plan number ( if applicable) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

* Daytime telephone number |

Email Address |

||||

|

|

|

|

|

|

|

|

|

hereby appoint(s) the following representative(s) as attorney(s) - in fact: |

|

|

|

|

|

|

2Representative(s) (Type or print.)

*Name and address of specific individual

* Telephone No. |

|

|

|

|

|

||

Fax No. |

|

|

|

Check if new: |

Address |

Telephone No. |

|

|

|

|

|

Name and address of specific individual |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

|

Check if new: |

Address |

Telephone No. |

|

|

|

|

|

Name and address of specific individual |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

|

Check if new: |

Address |

Telephone No. |

|

|

|

|

|

to represent the taxpayer(s) before the SC Department of Revenue for the following tax matters: |

|

|

|

3Tax Matters - A general reference to "All years," "All periods," or "All taxes" is not acceptable.

*Type of Tax (Individual, Corporate, Withholding, Sales, etc.)

*Tax Form Number (SC1040, WH1605,

Year(s) or Period(s)

*(See Line 3 instructions)

4Acts Authorized - A representative is an individual authorized to receive and inspect confidential tax information and to perform any and all acts on behalf of the taxpayer with respect to the tax matters described in line 3, including the authority to sign any agreements, consents or other documents. You may not use a Power of Attorney form to authorize a representative to receive refund checks. You may authorize a representative to sign a return ONLY as set forth in South Carolina Code Section

List any specific additions to or deletions from the acts otherwise authorized in this power of attorney:

5Receipt of Refund Checks - If you want to authorize a representative named in line 2 to receive, BUT NOT TO

ENDORSE OR CASH refund checks, initial here |

|

and list the name of that representative below. |

Name of representative to receive refund check(s)

33071028

6Retention/Revocation of Prior Power(s) of Attorney - The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the South Carolina Department of Revenue for the same tax matters for years or periods covered by this document .

If you do not want to revoke a prior power of attorney, check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

YOU MUST ATTACH A COPY OF ANY POWER OF ATTORNEY YOU WANT TO REMAIN IN EFFECT.

7Signature of Taxpayer(s) - If a tax matter concerns a joint return, both taxpayers must sign if joint representation is requested; otherwise, see the instructions for SC2848 concerning signature of taxpayer(s). If signed by a corporate officer, partner, guardian, tax matters partner/person, LLC members, executor, receiver, personal representative, or trustee on behalf of the taxpayer, I certify that I have the authority to execute this form on behalf of the taxpayer.

The Department will not accept a Power of Attorney that is not signed.

*

*

|

* |

|

|

|

|

Signature |

Date |

|

Title (if |

applicable) |

|

|

|

||||

Print Name |

|

|

|

|

|

|

|

|

|

|

|

Signature |

|

Date |

|

Title (if |

applicable) |

Print Name |

|

|

|

|

|

NOTICES AND COMMUNICATIONS

All Notices and Communications will be sent to the taxpayer only. However, if you are unable to forward a copy to your named representative, you may contact our office for assistance.

Part II Declaration of Representative

I declare that:

I am authorized to represent the taxpayer(s) identified in Part I for the tax matter(s) specified; and

I am authorized to represent the taxpayer(s) identified in Part I for the tax matter(s) specified; and  I am one of the following:

I am one of the following:

aAttorney - a member in good standing of the bar of the highest court of the jurisdiction shown below.

bCertified Public Accountant - duly qualified to practice as a certified public accountant in the jurisdiction shown below.

cEnrolled Agent - enrolled as an agent under the Requirements of the US Treasury Department Circular No. 230. d Officer - a bona fide officer of the taxpayer organization.

e

f Family Member - a member of the taxpayer's immediate family (i.e., spouse, parent, child, brother, or sister). g Return Preparer.

h Other, please explain.

The Department will not accept a Declaration of Representative that is not signed.

The Department will not accept a Declaration of Representative that is not signed.

I declare that this return and all attachments are true, correct and complete to the best of my knowledge and belief. To wilfully furnish a false or fraudulent statement to the Department is a crime.

*Designation - Insert

above letter

*Jurisdiction (state)

*Signature

*Date

*indicates required field.

33072026

Instructions for SC2848

General Instructions

Purpose of Form

Use SC2848 to grant authority to an individual to represent you before the South Carolina Department of Revenue and to receive tax information. See the instructions for Part I, line 4 for limitations that may apply for certain representatives.

A fiduciary (trustee, executor, administrator, receiver, or guardian) stands in the position of a taxpayer and acts as the taxpayer. Therefore, a fiduciary does not act as a representative and should not file a power of attorney. If a fiduciary wishes to authorize an individual to represent or perform certain acts on behalf of the entity, a power of attorney must be filed and signed by the fiduciary acting in the position of the taxpayer.

Authority Granted

This power of attorney authorizes the individual(s) named to perform any and all acts you can perform, such as signing consents extending the time to assess tax, recording the interview, or executing waivers agreeing to a tax adjustment. However, authorizing someone as your power of attorney does not relieve you of your tax obligations. Delegating authority or substituting another representative must be specifically stated on line 4. However, the authority granted to a power of attorney may not exceed that allowed under SC Code Section

Filing the Power of Attorney

File the original or a photocopy or facsimile transmission (fax) with the applicable office (main or taxpayer service center). The applicable office is the office from which you request information or before which a matter, such as an audit, is pending. Paper forms can be mailed to P.O. Box 125 Columbia, SC

Substitute SC2848

Federal Form 2848 may be substituted for SC2848 even though the instructions for the two forms differ somewhat. Be sure to note the differences and complete the Federal Form 2848 accordingly.

Specific Instructions

Part I - Power of Attorney

Line 1 - Taxpayer Information

Individuals. Enter your name, SSN (and/or EIN, if applicable), and address in the space provided. If a joint return is involved, and you and your spouse are designating the same representative(s), also enter your spouse's name and SSN, and your spouse's address if different from yours.

Social Security Privacy Act

It is mandatory that you provide your social security number on this tax form. 42 U.S.C 405(c)(2)(C)(i) permits a state to use an individual's social security number as means of identification in administration of any tax. SC Regulation

Corporations, partnerships, or LLC's. Enter the name, EIN, and business address. If this form is being prepared for corporations filing a consolidated tax return (SC1120), do not attach a list of subsidiaries to this form. Only the parent corporation information is required on line 1. Also, line 3 should only list SC1120 in the Tax Form Number column. However, a subsidiary must file its own SC2848 for returns that are required to be filed separately from the consolidated return, such as

Trust. Enter the name, title, and address of the trustee, and the name and EIN number of the trust.

Estate. Enter the name, title, and address of the decedent's executor/personal representative, and the name and identification number of the estate. The identification number for an estate includes both the EIN, if the estate has one, and the decedent's SSN.

Line 2 - Representative(s)

Enter the name of your representative(s). Only individuals may be named as representatives. Use the identical name on all submissions. If you want to name more than three representatives, indicate so on this line and attach a list of additional representatives to the form. Be sure to sign and date all attachments.

Line 3 - Tax Matters

You must enter the type of tax, the tax form number, and the year(s) or period(s) in order for the power of attorney to be valid. For example, you may list "income tax, SC1040" for calendar year "2016" and "Sales tax,

You may list the current year/period and any tax years or periods that have already ended as of the date you sign the power of attorney. However, you may include on a power of attorney only future tax periods that end no later than 3 years after the power of attorney is received by the Department of Revenue. The 3 future periods are determined starting after December 31 of the year the power of attorney is received by the department. You must enter the type of tax, the tax form number, and the future year(s) or period(s).

Line 4 - Acts Authorized

If you want to modify the acts that your named representative(s) can perform, describe any specific additions or deletions in the space provided. The authority to substitute another representative or to delegate authority must be specifically stated on line 4.

Certain Limitations:

If any representative you name is someone other than an attorney, CPA or enrolled agent, the acts that person can perform on your behalf may be limited by SC Code Section

Line 5 - Receipt of Refund Checks

If you want to authorize your representative to receive, but not endorse refund checks on your behalf, you must initial and enter the name of that person in the space provided. Treasury Department Circular No. 230 (31 CFR, Part 10) prohibits an attorney, CPA, or enrolled agent, any of whom is an income tax return preparer, from endorsing or otherwise negotiating a tax refund check. If you are in a licensed attorney/client relationship, your refund may be sent to your licensed attorney.

Line 6 - Retention/Revocation of Prior Power(s) of Attorney

If there is any existing power(s) of attorney you do not want to revoke, check the box on this line and attach a copy of the power(s) of attorney. If you want to revoke an existing power of attorney and do not want to name a new representative, send a copy of the previously executed power of attorney to each office where the power of attorney was filed. The copy of the power of attorney must have a current signature of the taxpayer under the signature on line 8. Write "REVOKE" across the top of the form. If you do not have a copy of the power of attorney you want to revoke, send a statement of revocation to each office where you filed the power of attorney. The statement must indicate that the authority of the power of attorney is revoked and must be signed by the taxpayer. Also, the name and address of each recognized representative whose authority is revoked must be listed. A representative can withdraw from representation by filing a statement with each office where the power of attorney was filed. The statement must be signed by the representative and identify the name and address of the taxpayer(s) and tax matter(s) from which the representative is withdrawing.

Line 7 - Signature of Taxpayer(s)

Individuals. You must sign and date the power of attorney. If a joint return has been filed and both taxpayers will be represented by the same individual(s), both must sign the power of attorney unless one spouse authorizes the other, in writing, to sign for both. In that case, attach a copy of the authorization. However, if a joint return has been filed and both taxpayers will be represented by different individuals, each taxpayer must execute his or her own power of attorney on a separate SC2848.

Corporations or associations. An officer having authority to bind the taxpayer must sign.

Partnerships. All partners or members of an LLC must sign unless one partner or member is authorized to act in the name of the partnership. A partner is authorized to act in the name of the partnership if, under state law, the partner has authority to bind the partnership. A copy of such authorization must be attached. For purposes of executing SC2848, the tax matters partner is authorized to act in the name of the partnership. For dissolved partnerships, see US Treasury Regulations section 601.503(c)(6).

Other. If the taxpayer is a dissolved corporation, deceased, insolvent, or a person for whom or by whom a fiduciary (a trustee, guarantor, receiver, executor, or administrator) has been appointed, see US Treasury Regulations section 601.503(d).

PART II - Declaration of Representative

The representative(s) you name must sign and date this declaration and enter the designation (i.e., items

aAttorney - Enter the

bCertified Public Accountant - Enter the

d Officer - Enter the title of the officer (i.e., President, Vice President, or Secretary). e

f Family Member - Enter the relationship to taxpayer (i.e., spouse, parent, child, brother, or sister).

g Tax Return Preparer - Enter the

Note: If the representation is outside the United States, conditions

| Fact Name | Details |

|---|---|

| Purpose | The Tax Power of Attorney Form 2848 allows individuals to designate a representative to act on their behalf in tax matters before the Internal Revenue Service (IRS). |

| Eligibility | Any individual or entity can appoint a representative using Form 2848, but both the taxpayer and the representative must sign the form for it to be valid. |

| Timeframe | Once the form is submitted, it generally takes the IRS a few weeks to process the request. Always keep a copy for your records. |

| State Variations | Some states have their own specific forms for power of attorney in tax matters, governed by local tax laws, such as California's Franchise Tax Board POA form or New York's Form POA-1. |

Once you have the Tax POA SC2848 form ready to complete, follow the steps outlined below. It's important to ensure all details are filled in accurately to avoid any delays in processing your request.

After filling out the form, make sure to send it to the designated IRS address. This step is crucial to ensure the assigned representative can effectively manage your tax-related matters.

The Tax POA SC2848 form is a Power of Attorney document specifically designed for taxpayers in South Carolina. It allows individuals to authorize someone else to act on their behalf when dealing with tax matters. This could include communicating with the Department of Revenue, filing returns, or addressing any issues that may arise regarding tax obligations.

On the SC2848 form, you can appoint various representatives. This may include:

It’s important that your chosen representative understands tax laws, as they will be handling sensitive and complex issues on your behalf.

Completing the SC2848 form requires careful attention. Here are the key steps to follow:

Ensuring that all sections are completed accurately will help avoid delays in processing your request.

After filling out the SC2848 form, you should send it to the South Carolina Department of Revenue. They typically have specific addresses listed on their official website where you can submit your documents. It’s advisable to check the website or contact them directly to ensure you’re sending it to the correct location.

The processing time for the SC2848 form can vary. Generally, the Department of Revenue aims to process forms within a few weeks. However, circumstances such as the volume of applications or specific issues might delay processing. Following up with the department can provide clarity if you haven’t heard back in a reasonable time.

Yes, you can revoke or cancel the Power of Attorney at any time. To do this, you need to submit a written notice to the South Carolina Department of Revenue. It's also a good idea to inform your representative about the revocation to prevent any misunderstandings.

When filling out the Tax Power of Attorney (POA) Form 2848, individuals often make common mistakes that can lead to delays or even the rejection of the form. One frequent error is failing to provide complete contact information for the representative. This includes not only the name but also the address and phone number. If the IRS cannot reach the representative for additional information or questions, it can result in complications for the taxpayer.

Another mistake involves incorrectly specifying the tax matters for which the POA is granted. It is essential that taxpayers clearly indicate all applicable tax years or periods. Omitting a specific year or incorrectly stating the types of taxes involved can create confusion and may limit the authority granted to the representative.

People often overlook the proper signatures required on the form. Both the taxpayer and the designated representative must sign the form. Missing one of these signatures can render the document invalid. It is also crucial to ensure that the signatures are dated; otherwise, this may further complicate the IRS’s processing of the form.

Another common oversight is not understanding the implications of granting authority. Taxpayers should carefully consider whether they wish to give full or limited authority to their representative. The choices are crucial; granting too much authority can lead to unintended consequences, while granting too little can impede the representative's ability to assist.

Many individuals do not check the form for errors before submission. Simple typos or incorrect entries, such as wrong identification numbers, can lead to significant issues. It might seem trivial, but even a small mistake can create roadblocks in the communication between the taxpayer and the IRS, resulting in delays.

Additionally, people may forget to file the form in a timely manner. The IRS requires that the 2848 be filed before the representative can act on the taxpayer's behalf. If submitted too late, it can invalidate any actions the representative may want to take regarding the client’s tax matters.

Understanding the limits of the POA can also be a challenge. Some individuals may mistakenly assume that granting a POA gives the representative complete control, when in fact, there are boundaries, especially concerning the sharing of confidential information. Taxpayers must know the extent of the authority they are granting to avoid surprises.

Lastly, many people fail to follow up after submitting the form. It's important to confirm with the IRS that the POA has been accepted. Neglecting this step can lead to unexpected difficulties, especially if the representative needs to communicate with the IRS and finds that their authority has not been recognized.

When dealing with tax matters, the IRS Form 2848, also known as the Power of Attorney (POA), is often complemented by other essential forms and documents. These documents serve various purposes, from granting authority to representatives to providing necessary information for tax-related processes. Below are several forms that frequently accompany the Tax POA Form 2848.

Understanding these forms and their purposes is crucial when preparing for interactions with the IRS. Each document plays a specific role in ensuring compliance and clarity in your tax affairs. Always consult a qualified professional if you have questions about these forms or their application.

When filling out the Tax Power of Attorney (POA) Form SC2848, certain practices can help ensure the process goes smoothly. Here are some essential do's and don'ts to keep in mind:

The IRS Form 2848, often referred to as the Power of Attorney (POA) for tax purposes, is essential for allowing someone to represent a taxpayer before the IRS. However, several misconceptions exist surrounding this form that can lead to confusion. Below are seven common misconceptions about Form 2848, along with clarifications for each.

It can only be used for individuals. Contrary to this belief, Form 2848 can also be utilized by businesses, estates, and trusts. Any entity requiring representation before the IRS may file this form.

Once submitted, the Power of Attorney is permanent. This is incorrect. The authority granted under Form 2848 is not indefinite. Taxpayers or representatives can revoke or limit the powers assigned at any time by submitting a new form.

You must be present at the IRS office to submit Form 2848. Many assume that in-person submission is necessary. However, the form can also be mailed or faxed to the IRS, making the process more accessible.

Form 2848 can only be signed by the taxpayer. While the taxpayer typically signs the form, in specific circumstances, a duly authorized representative may sign on their behalf if proper documentation is provided.

Submitting Form 2848 affects all tax matters forever. This misunderstanding arises from the use of the term "Power of Attorney." The form only pertains to the tax matters specified. For new issues, a separate authorization may be necessary.

There is a fee for filing Form 2848. Individuals often believe that a fee is required for submission. In actuality, there are no fees associated with filing this form.

Form 2848 needs to be filed annually. This misconception leads many to think regular re-filing is necessary. However, Form 2848 remains valid until updated or revoked, thus not requiring yearly submissions.

Understanding these misconceptions can help taxpayers navigate the complexities of representation and taxation more efficiently. Accurate information is vital for ensuring compliance with IRS regulations and protecting taxpayer rights.

When dealing with tax matters, it's important to understand how to fill out and utilize the Tax Power of Attorney (POA) Form SC2848. Here are nine key takeaways that can guide you through this process:

By taking these steps, you can ensure that your tax affairs are managed efficiently and with the appropriate support.