The Tax Power of Attorney (POA) Tbor-1 form plays a vital role for taxpayers navigating the often intricate landscape of tax obligations and representation. When individuals or businesses face the complexities of tax matters, they may find it necessary to appoint someone to act on their behalf—this is where the Tbor-1 form comes into play. It empowers an authorized individual, be it a tax professional or a trusted advisor, to communicate and negotiate directly with the tax authorities on behalf of the taxpayer. Essential information is required on the form, including the names of the parties involved, the scope of authority being granted, and the specific tax matters or years that the representation covers. By using the Tbor-1 form, taxpayers can ensure that their interests are adequately represented, providing peace of mind in what could otherwise be a daunting financial situation. This simple yet powerful document facilitates effective handling of tax issues, ranging from filing claims and responding to audits to managing payment arrangements, thereby illustrating the importance of properly documenting one’s intent when it comes to tax representation.

Ohio I ~:::;:ent of |

|

|

IIII |

|

|

I |

|

Ill |

|

|

|

|

|

|

1111111111111111 |

|

|

|

|

|

|

TBOR 1 |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rev. 05/19 |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

P.O. Box 1090 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

16310102 |

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

Columbus, OH |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

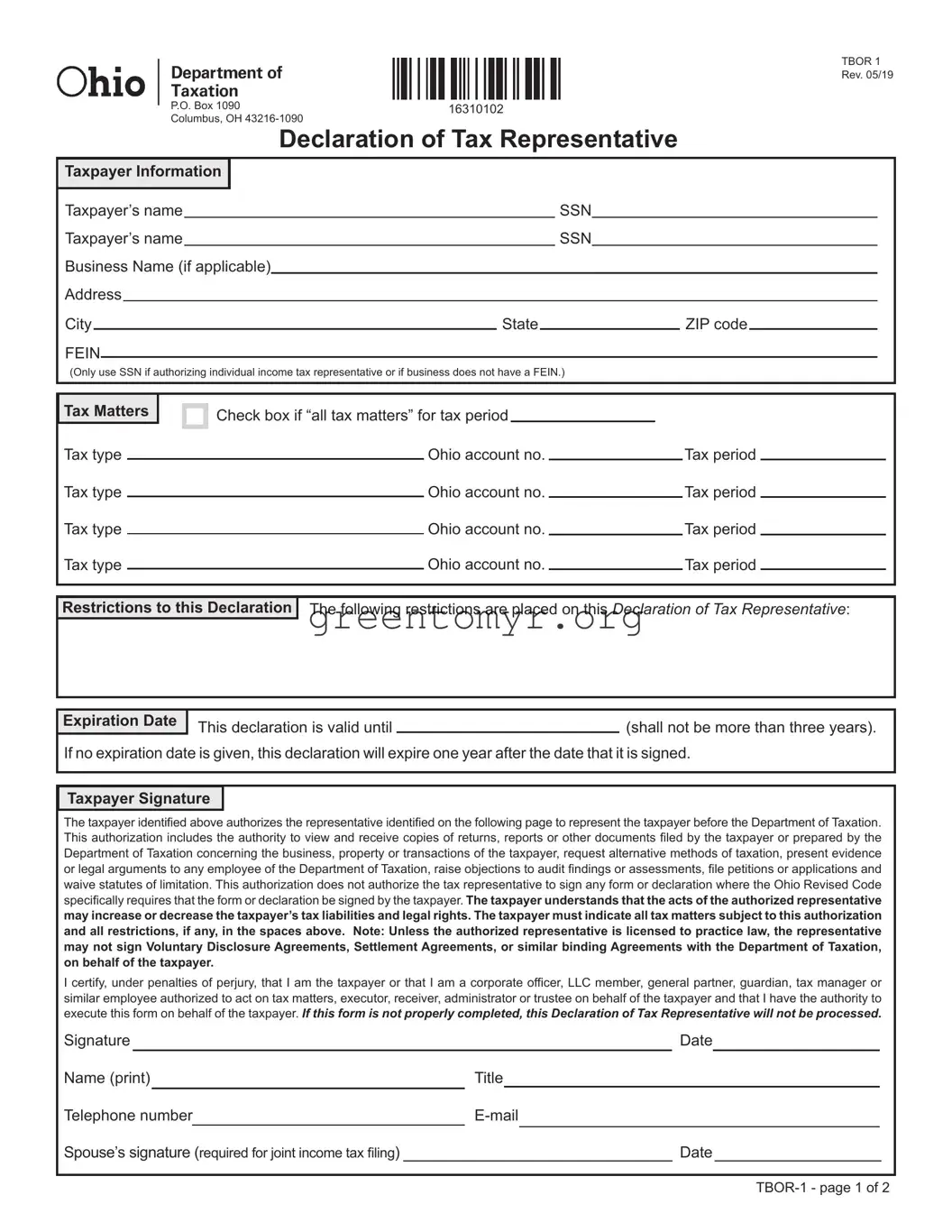

Declaration of Tax Representative |

|

|

|

|||||||||||||||||||||

Taxpayer Information |

I |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Taxpayer’s name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SSN |

|

|

|

|

|||||

Taxpayer’s name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SSN |

|

|

|

|

||||||

Business Name (if applicable) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

City |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

|

|

|

|

|

ZIP code |

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

(Only use SSN if authorizing individual income tax representative or if business does not have a FEIN.) |

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tax Matters I

□ Check box if “all tax matters” for tax period

Tax type |

|

Ohio account no. |

|

Tax period |

|

|

|||

Tax type |

|

Ohio account no. |

|

Tax period |

|

|

|||

Tax type |

|

Ohio account no. |

|

Tax period |

|

|

|||

Tax type |

|

Ohio account no. |

|

Tax period |

|

|

Restrictions to this Declaration I The following restrictions are placed on this Declaration of Tax Representative:

Expiration Date |

This declaration is valid until |

(shall not be more than three years). |

|

If no expiration date is given, this declaration will expire one year after the date that it is signed.

Taxpayer Signature I

The taxpayer identified above authorizes the representative identified on the following page to represent the taxpayer before the Department of Taxation. This authorization includes the authority to view and receive copies of returns, reports or other documents filed by the taxpayer or prepared by the Department of Taxation concerning the business, property or transactions of the taxpayer, request alternative methods of taxation, present evidence or legal arguments to any employee of the Department of Taxation, raise objections to audit findings or assessments, file petitions or applications and waive statutes of limitation. This authorization does not authorize the tax representative to sign any form or declaration where the Ohio Revised Code specifically requires that the form or declaration be signed by the taxpayer. The taxpayer understands that the acts of the authorized representative may increase or decrease the taxpayer’s tax liabilities and legal rights. The taxpayer must indicate all tax matters subject to this authorization and all restrictions, if any, in the spaces above. Note: Unless the authorized representative is licensed to practice law, the representative may not sign Voluntary Disclosure Agreements, Settlement Agreements, or similar binding Agreements with the Department of Taxation, on behalf of the taxpayer.

I certify, under penalties of perjury, that I am the taxpayer or that I am a corporate officer, LLC member, general partner, guardian, tax manager or similar employee authorized to act on tax matters, executor, receiver, administrator or trustee on behalf of the taxpayer and that I have the authority to execute this form on behalf of the taxpayer. If this form is not properly completed, this Declaration of Tax Representative will not be processed.

Signature |

|

|

|

|

Date |

|

|||

Name (print) |

|

Title |

|

||||||

Telephone number |

|

|

|||||||

Spouse’s signature (required for joint income tax filing) |

|

|

|

|

Date |

|

|||

Ohl■O I TaxationDeparJment of |

TBOR 1 |

Rev. 05/19 |

|

IIII IIll 1111111111111111 |

|

P.O. Box 1090 |

16310202 |

Columbus, OH |

|

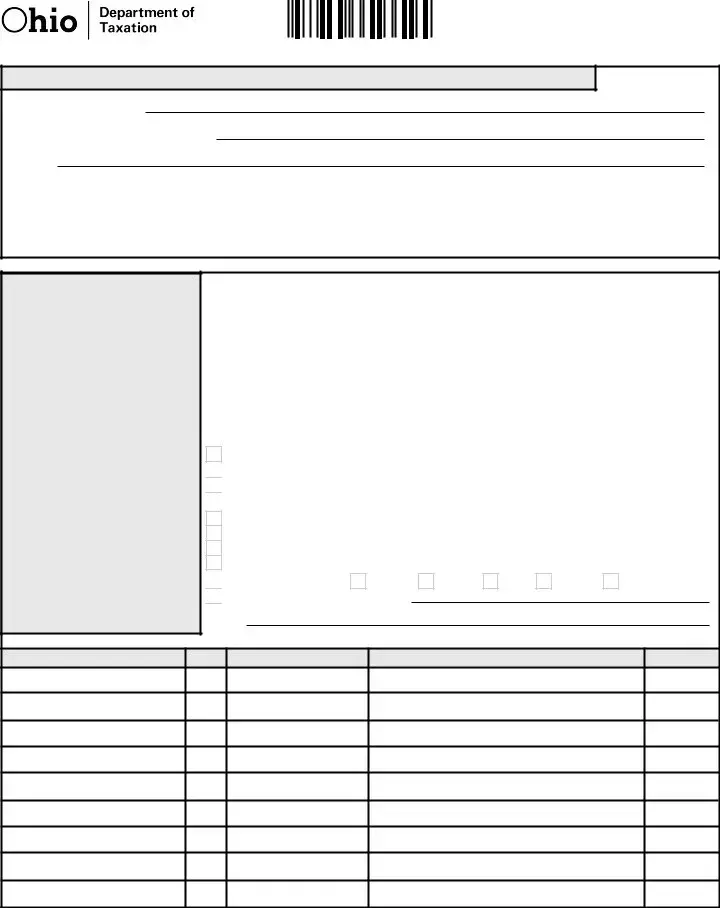

Representative Information - Please indicate if more than one representative in the space below. I

Representative’s name

Representative’s firm (if applicable)

Address

City |

|

|

|

State |

|

|

ZIP code |

|

|

Telephone number |

|

Fax number |

|

|

|

||||

|

|

|

|

|

|

|

|

||

Declaration of Representative

Under penalties of perjury, I declare that:

• I am not currently under suspension or disbarment from practice within the state of Ohio or any other jurisdiction;

• I am aware of the regulations governing my practice in Ohio and the penalties for false or fraudulent statements provided;

• I am authorized to represent in Ohio the taxpayer(s) identified for the tax matter(s) specified herein; and I am one of the following (please indicate by checking the

box beside the appropiate number):

□ 1. Attorney – a member in good standing of the bar of the highest court of the jurisdiction shown below.

n

2. Certified public accountant or public accountant – duly qualified practice in the jurisdiction shown below.

2. Certified public accountant or public accountant – duly qualified practice in the jurisdiction shown below.

3. Enrolled agent – enrolled as an agent under the requirements of the IRS. ~4. Officer – a bona fide officer of the taxpayer’s organization.

5.

6. Family member – a member of the taxpayer’s immediate family (check appro- priate response) nspouse n parent n child n brother n sister

LJ

7. Other – provide explanation

7. Other – provide explanation

Designation (insert no. 1 - 7) State

License Number

Representative Signature

Date

*Mail: P.O. Box 1090, Columbus, OH |

Fax: (206) |

|

(Use the same method to revoke declaration.) |

*Most secure method |

|

|

||

| Fact Name | Description |

|---|---|

| Purpose | The Tax POA tbor-1 form is used to grant someone the authority to represent you before the tax authorities regarding your tax matters. |

| Eligibility | Any individual or business who needs to appoint a representative can fill out this form, as long as they are compliant with state tax requirements. |

| Governing Law | This form is governed by state tax laws applicable in the state where the form is filed. |

| Signing Requirements | The form must be signed by the taxpayer granting authority, ensuring the legitimacy of the representation. |

| Filing Method | It can usually be filed electronically or as a paper document, depending on the state's tax department policies. |

| Expiration | Typically, the authority granted through this form remains effective until revoked or the specified tax matters are resolved. |

| Revocation | If you change your mind, revoking the authority is straightforward and can be done through a specific revocation form. |

| Common Uses | This form is often used for various tax issues, including audits, appeals, and filing returns. |

| Legal Assistance | Consider consulting a tax professional or attorney for guidance in completing this form and ensuring it meets all requirements. |

| State Variability | Different states may have their own versions of this form, so it’s crucial to check your state's specific requirements. |

Completing the Tax POA tbor-1 form requires careful attention to detail. After filling it out, you will submit it to ensure that your agent can represent you before tax authorities. Follow the steps below to accurately fill out the form.

Once the form is filled out, ensure that all information is correct before submitting it. Incorrect or incomplete forms may lead to delays. It is advisable to keep a copy for your records.

The Tax POA tbor-1 form is a Power of Attorney document used in tax-related matters. It allows an individual or organization to appoint a representative to act on their behalf when dealing with tax authorities. This representative can be authorized to handle a variety of tasks, from filing tax returns to resolving tax disputes.

Anyone who requires assistance with tax matters may need to file this form. This includes individuals who may not be confident in managing their own tax issues or those who lack the time to handle tax communications. Businesses can also file this form to allow a designated individual, such as an accountant or attorney, to handle their tax-related affairs.

To complete the Tax POA tbor-1 form, you will need to provide the following information:

Make sure that all information is accurate to avoid delays in processing.

You can submit the Tax POA tbor-1 form by mailing it to the appropriate tax authority. The address will depend on your location and the specific tax agency involved. Be sure to check the latest guidelines from the tax authority to ensure you have the correct address and submission method. In some cases, electronic submission may also be available.

Yes, you can revoke the powers granted at any time. To do this, you must provide written notice to your representative and notify the tax authority as well. It's advisable to keep a copy of the revocation letter for your records. Remember that once revoked, your representative will no longer have the authority to act on your behalf.

When people fill out the Tax POA tbor-1 form, mistakes can occur that may lead to delays or complications. One common error is providing incomplete information. It’s essential to submit all relevant details, such as your name, address, and taxpayer identification number, fully and accurately. Missing just one piece of information can halt the processing of your request.

Another frequent mistake is not signing the form. Many individuals overlook the requirement for a signature, thinking that submitting the form electronically makes this unnecessary. However, without a signature, the form is considered invalid, and the IRS will not process it.

Some people also select an incorrect power of attorney. The designated representative must have the appropriate authority to act on your behalf. Ensure that the person you are naming is capable of handling your tax matters. Otherwise, your authorization may be ineffective.

Failure to check the expiration date of the POA can lead to further complications. Once a power of attorney expires, your designated representative can no longer act on your behalf without a new form. Review the terms carefully to avoid disruptions in your representation.

It’s worth noting that many individuals neglect to use the most current version of the tbor-1 form. Tax laws and forms can change, so using an outdated version can create issues. Always verify that you have the latest form before submitting.

Lastly, some people make the mistake of not providing adequate documentation to support their request. Additional paperwork may be required, especially if you are appointing someone who has not acted as your representative in the past. Failing to include these documents could delay approval.

These common mistakes can be easily avoided by reviewing the form thoroughly and ensuring all information is correct and complete. Taking the time to fill out the Tax POA tbor-1 form properly will save you time and frustration in the long run.

The Tax Power of Attorney (POA) TBOR-1 form is an essential document for individuals who wish to grant someone the authority to act on their behalf in tax matters. However, several other forms and documents can complement this process to ensure comprehensive management of tax-related concerns. Below are some commonly used forms that may accompany the TBOR-1.

Choosing the right forms is crucial for ensuring clarity and authority in tax representation. Make sure to consult with a tax professional to determine which documents best fit your specific circumstances.

The Tax POA tbor-1 form is similar to several other documents in its function and purpose. Here are ten documents that share similarities:

When filling out the Tax POA TBOR-1 form, it’s essential to get it right to avoid potential issues. Here’s a list of important dos and don’ts to consider:

Understanding the Tax Power of Attorney (POA) form, known as the tbor-1 form, is essential for taxpayers who wish to allow someone else to represent them before the tax authorities. However, several misconceptions exist about this form. Let’s clarify those misunderstandings:

By addressing these common misconceptions, taxpayers can better navigate the use of the tbor-1 form, ensuring they make informed decisions about representation in tax matters.

When it comes to handling tax matters, the Tax POA tbor-1 form plays a critical role in authorizing someone to act on your behalf. Understanding how to fill it out and utilize it properly can save you time and confusion. Here are nine key takeaways.

By keeping these key points in mind, you can navigate the process of completing and using the Tax POA tbor-1 form with greater ease and confidence.